Pork Wrap October 22

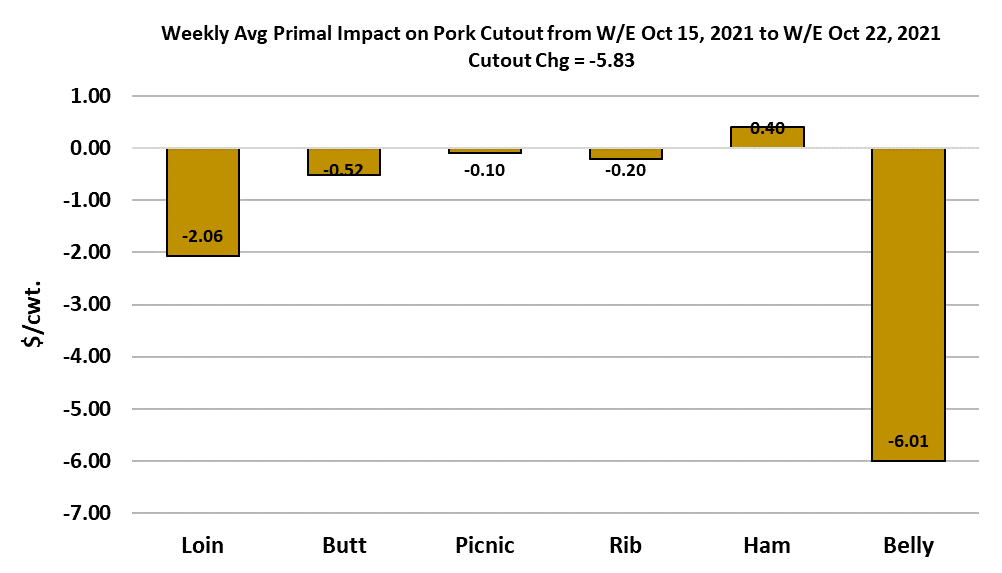

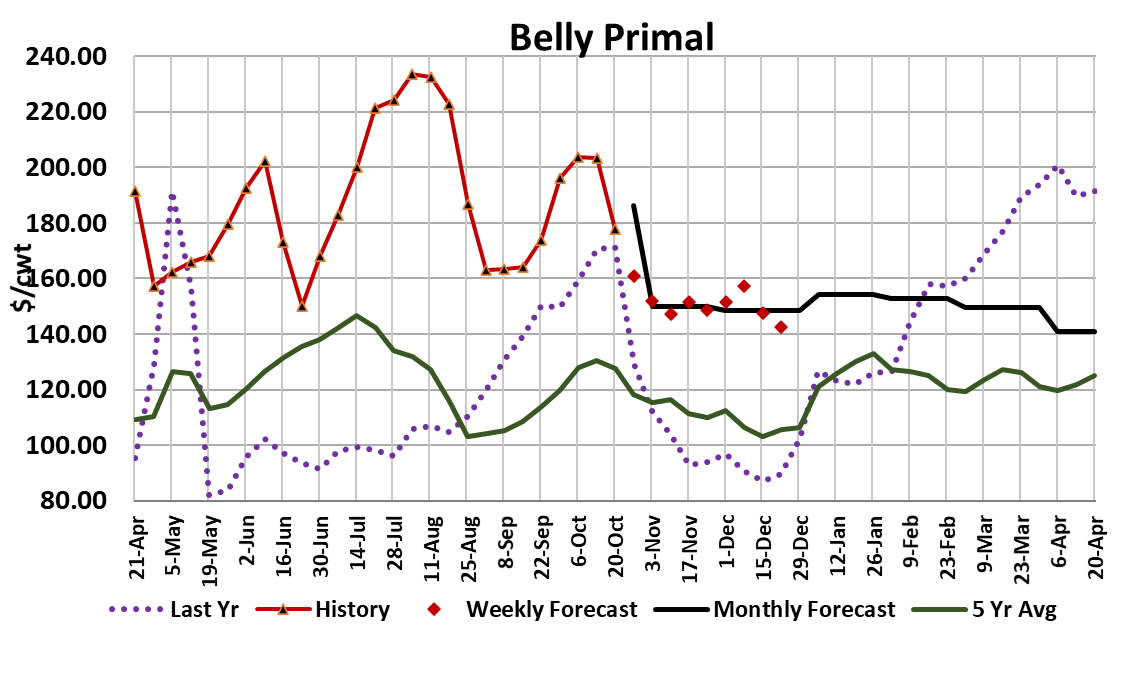

This week it was the bellies’ turn to pressure the cutout lower.

The chart to the right indicates that after several weeks of being the

bad guy, hams actually added a small amount to the cutout. But

that wasn’t nearly enough to offset the pressure that came from

the belly primal. On a weekly average basis, the cutout dropped

almost $6 this week. Cash hogs also moved lower, but not as

much as the cutout. WCB negotiated hogs were only down $1.40

this week. The LHI lost a little over $3.50, reflecting the drop in the

cutout in addition to the smaller decline in cash hog prices. With

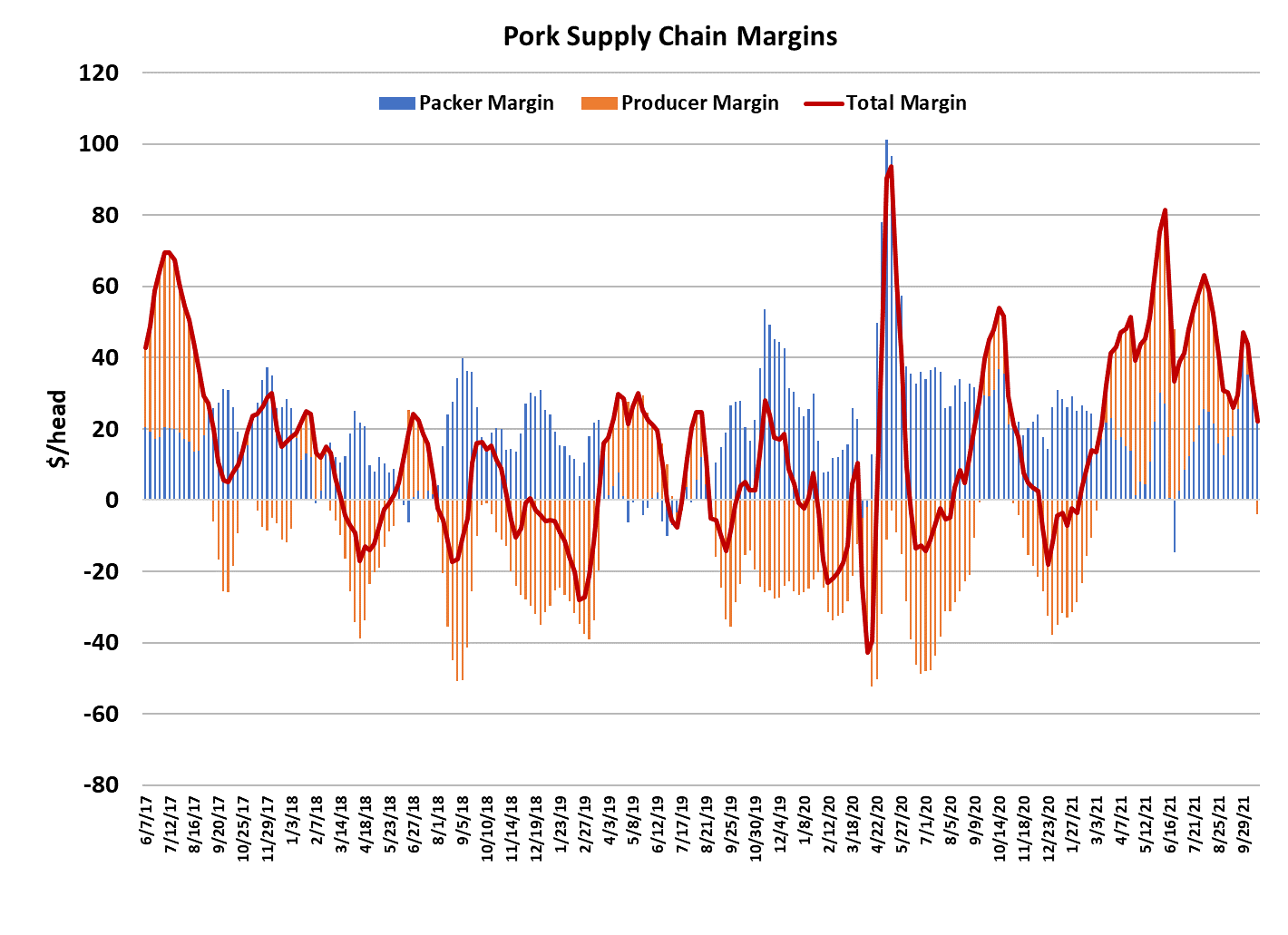

pork prices down more than hog prices, packer margins shrank.

I estimate packer margins at $26/head, down about $5 from last

week. The pork drop credit is also declining as kills increase

seasonally. Margins are very close to the five-year average for

this time of year, but with demand still very strong, I expected them

to be larger. Perhaps the smaller supply of hogs this fall is

working to counter the margin enhancement that should arise from

stronger-than-normal demand. Packers posted a 2.6 million head

kill this week, slightly smaller than last week. The difference was

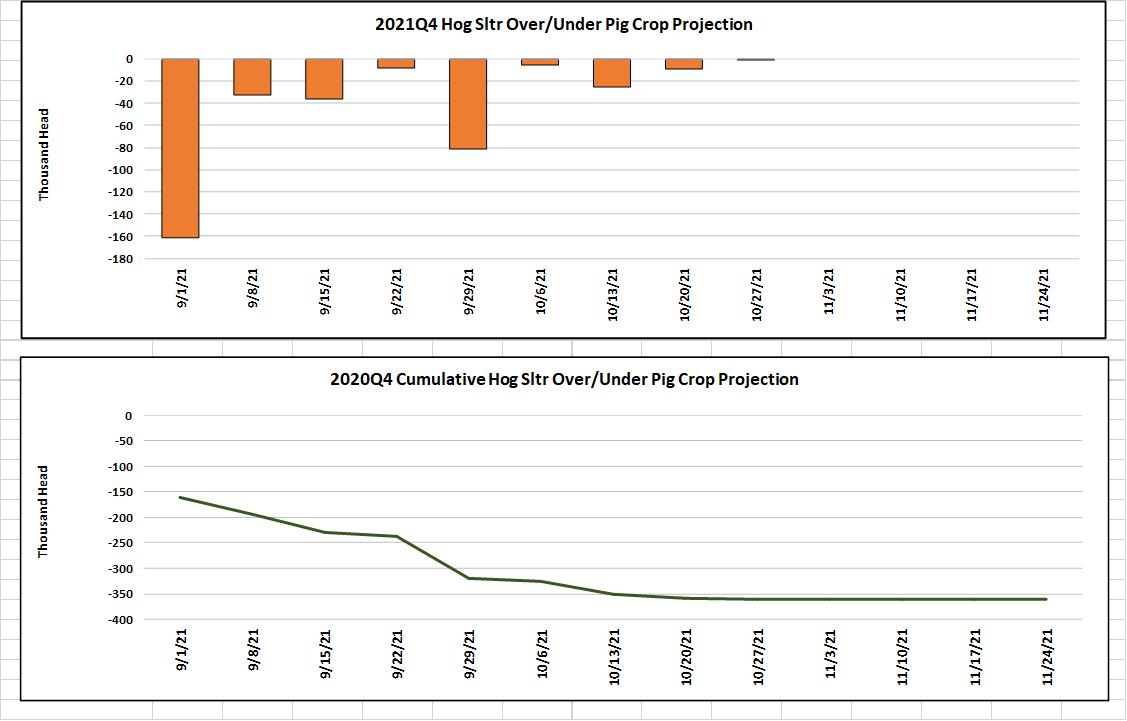

a little bit smaller Saturday kill this week. However, that kill was

nearly dead on with what the March/May pig crop implied. The bar

chart to the right shows that the kill in recent weeks has been a lot

closer to the pig crop than it was earlier in the quarter. That gives

me some confidence that I’ve likely got the projected kills right

over the next few weeks. We are not far away from the peak kill

which should total around 2.68 million head near the end of

November. Carcass weights are rising seasonally now and that is

also adding to production. Unfortunately, the export market

doesn’t appear to be soaking up as much product as it has in

recent years.

Still, strong domestic demand can cover for a lot of sins and

demand is definitely strong in an historical context. I’m looking for

the Q4 cutout demand index to come in around 1.12, which is

below the 1.17 average of the first three quarters in 2021, but the

second highest Q4 demand ever recorded. The combined margin

chart tells us that demand has resumed its near-term decline after

a brief, but large, head fake a couple of weeks ago. Clearly, we

have seen belly demand erode over the last 10 days or so, but I

also think we are seeing some slippage in demand for the retail

items. Hams may be close to a bottom now. It is hard to imagine

that 23/27 hams below $48 won’t be seen as a great value by

buyers.

Of course, many of the buyers that use bone-in hams process

them further and so perhaps labor is constraining their demand

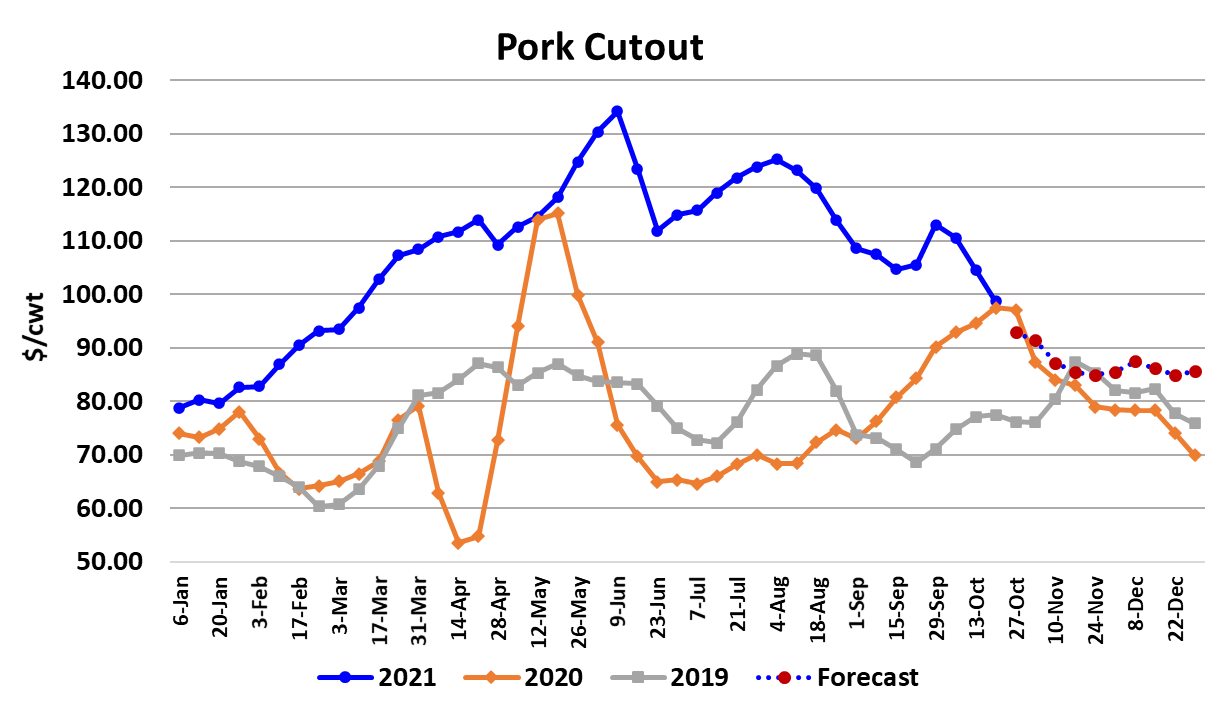

for hams this fall. The cutout has now printed below $100 four

days in a row and it looks like it has further downside potential

as kills expand further in the next few weeks and belly demand

stays on the defensive. I’m forecasting the cutout to move into

the mid $80s sometime around Thanksgiving. I think the risk is

that it may go there sooner. The lack of Chinese interest in US

pork is one of the more disappointing features of the market this

fall. The weekly export volumes to China continue to decline

and their forward book doesn’t indicate that they plan on

ramping up imports from the US anytime soon.

In addition, retailers have jammed pork prices to all-time highs

after several months of super-high wholesale pricing. That is

likely to cool consumer interest in pork and it is coming right

when the biggest production of the year occurs. Pork has very

inelastic demand, meaning that relatively small changes in the

quantity available can result in big changes in price. That is

partly why I’m concerned that a mid $80s cutout could come

sooner than most expect. Hog producers have enjoyed great

margins for most of 2021 (chart to the right), but the recent decline

in cash hog prices has producer margins on the verge of going

red. The last two months of 2021 are likely to see producer

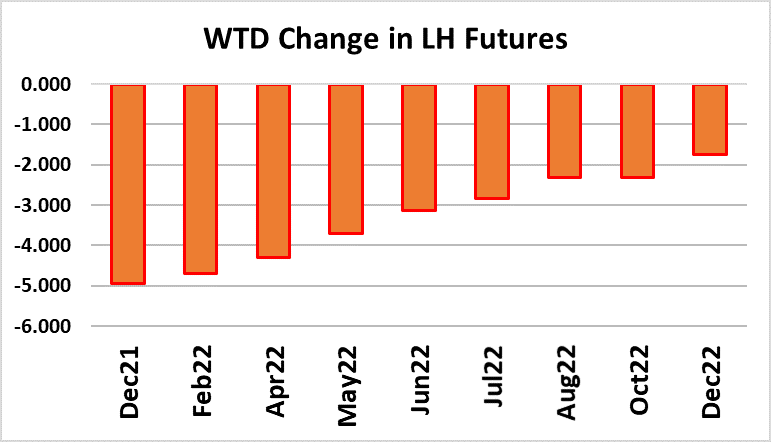

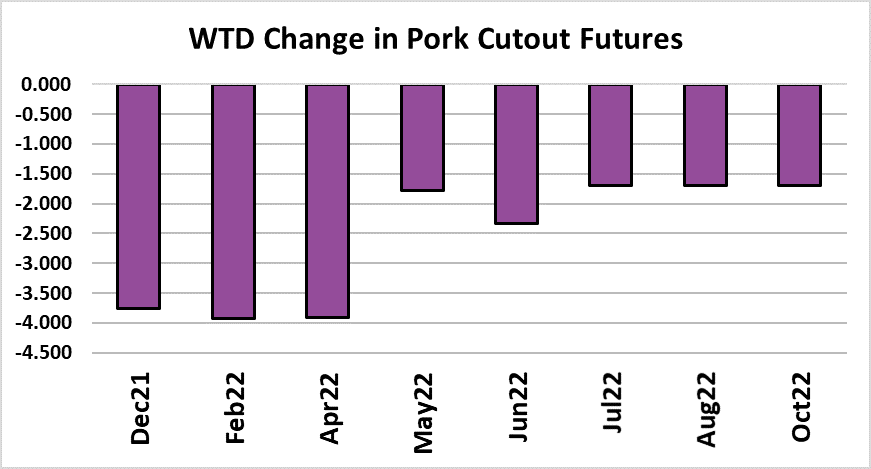

losses of more than $20/head. Lean hog and pork cutout

futures were lower on the week, with the biggest losses coming

in the front end of the curve.

Traders were quick to adjust their price expectations as the

cutout moved below $100 and the bellies made their downward

trajectory clear. Dec hogs lost $5 on the week and are now

about $9.50 under the LHI. With seven weeks to go until

expiration, it is reasonable to expect the Dec contract to remain

well below the index as long as the cutout and index are

trending lower. Next week, watch those bellies for further

softening and keep an eye on the hams in case low prices

should start to attract some buying interest.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}