Pork Wrap October 21

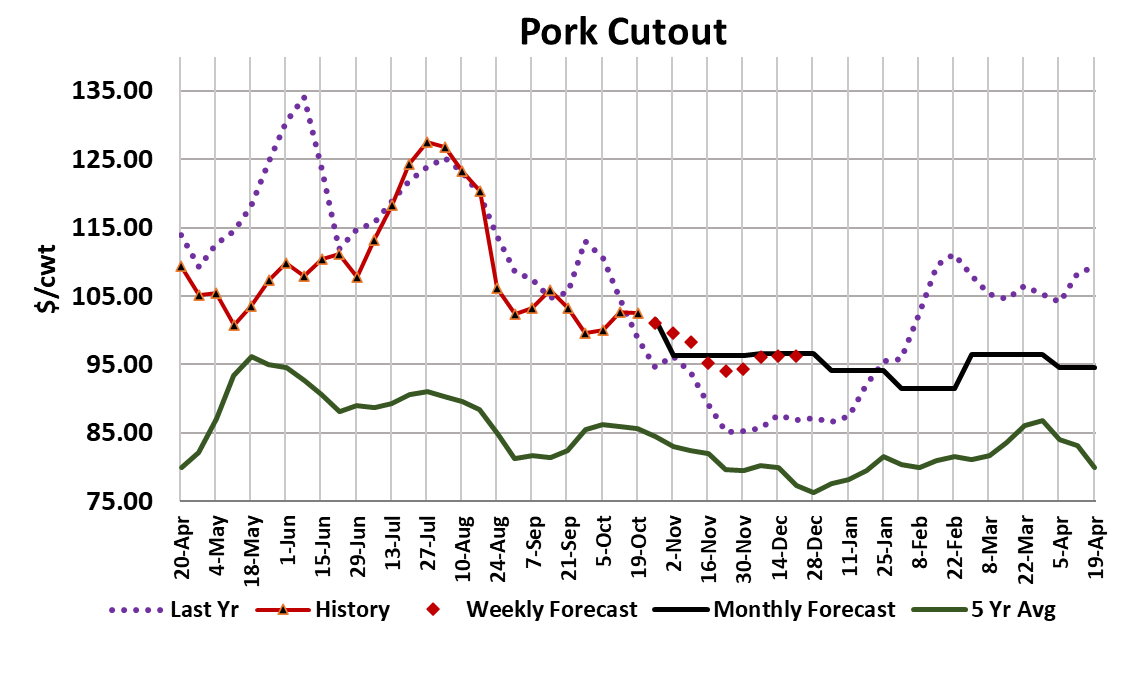

This week saw the pork cutout stall, averaging $102.46/cwt.,

down $0.23/cwt. from last week’s average. A $102 cutout in late

October is pretty impressive, but what is even more impressive is

the renewed strength in cash hog prices. This week the WCB

negotiated market averaged $97.38, up $6.75 from the week

before. The NDD negotiated market was up $4.37. A flat cutout

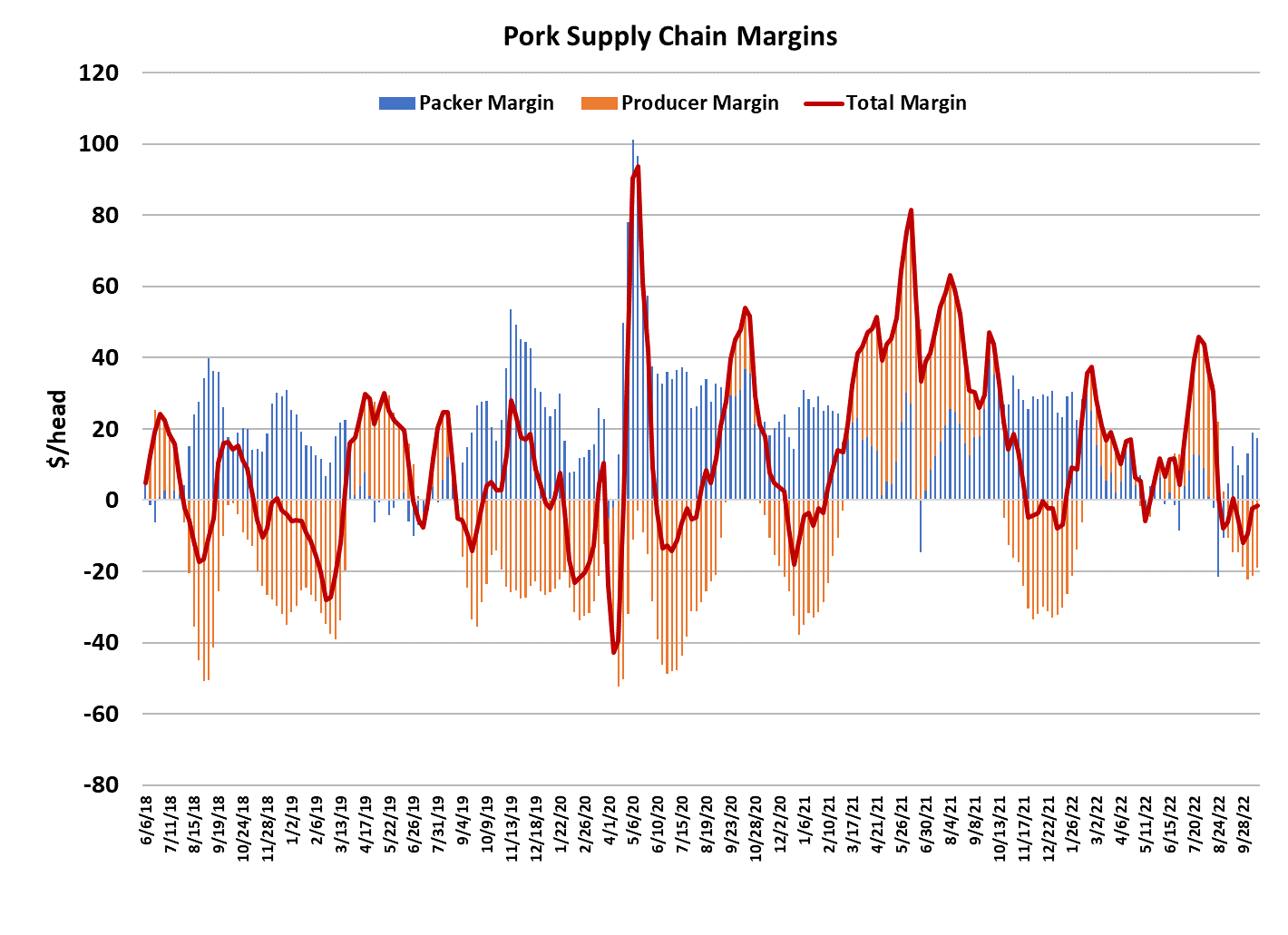

combined with rising hog prices spells trouble for packer profits.

Packer margins declined about $2/head this week to $17, but all

of the increase in the cash hog price has yet to be reflected in the

LHI, so I’m looking for margins to drop another $4 or so next

week. Over the past five years, packer margins near the end of

October have averaged about $26/head, so it is very clear that

margins are well below normal this year. Packers have only 2

choices if they want to fix their margin problem: raise pork prices

or lower cash hog prices. It seems to me that they might not

have much power to do either, so they may just have to live with

below-normal margins for a while.

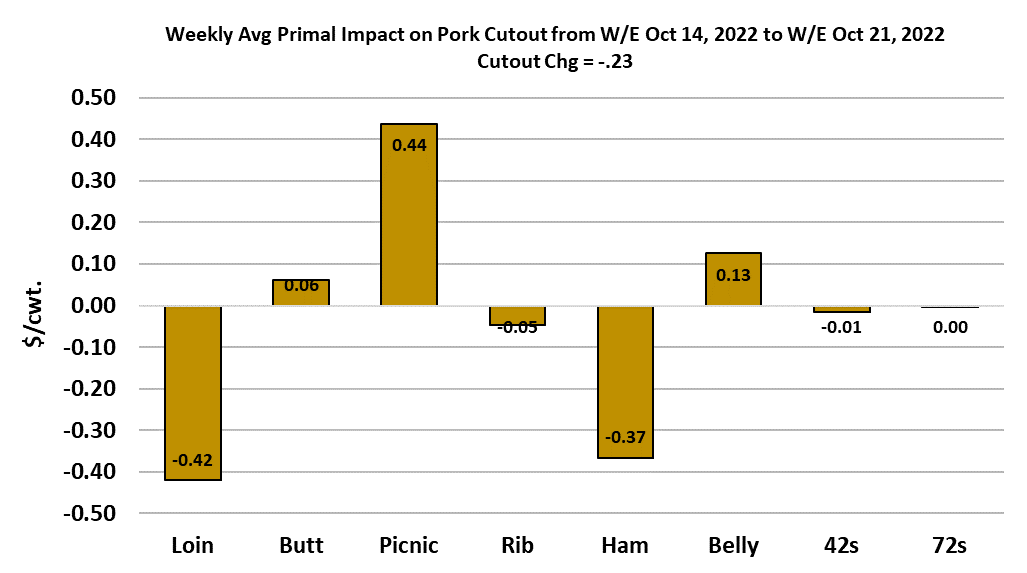

It is hard to see how they could add much to the cutout in the

current environment where kills are close to annual highs. This

week, loins and hams exerted the most downward pressure on

the cutout, but that was mostly offset by strength in the picnic and

belly primals. I’m expecting both the bellies and hams to ease a

little next week, so that may be enough to move the cutout lower.

I think we should still see another week or two of the cutout

averaging over $100, but soon it will slide into the upper $90s,

where it is likely to spend most of the remainder of 2022. The

combined margin was a little higher this week and, while it seems

that we should be in a demand upcycle, it is hard to see where the

additional strength will originate from. Producers are likely to gain

a little margin from packers due to the strong cash hog market,

but that doesn’t help the combined margin.

I could be wrong about the bellies and hams and we may see

further strength there, I guess. I think packers will have a strong

incentive to try and push pork prices higher early next week to try

and compensate for the stronger hog market. Whether or not they

are successful with that attempt remains to be seen. The fact that

the WCB negotiate market is still being quoted near $100/cwt in

late October tells me that the hog supply is pretty tight in that

region. That fact alone should be pretty bullish for the hog and

pork complex in the next few weeks. In the past when cash hog

prices were stubbornly high, packers have seemed to find a way

to raise pork prices. Maybe that will be the case again this time.

It is pretty clear that packers are having to compete more

aggressively to fill out their kill schedules than they have at they

have at this time of year in the past.

The same situation is occurring in beef, resulting in much smaller margins

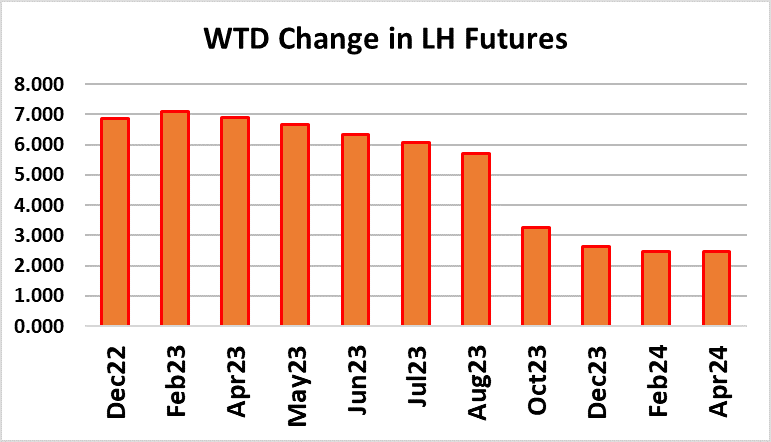

than what packers have become accustomed to. This surprising lateyear strength in the hog market has really kept the futures market on the

move. Today, the Dec contract traded very close to $90 for a period of

time. A little over two weeks ago it was trading at $74. The rally in Dec

over the past two weeks has been impressive and it wiped out everything

that Dec lost when the market swooned in September. The back of the

futures curve has taken notice too, and we saw the summer 2023

contracts gain close to $6 this week. Those issues still look a little

under-priced relative to the fundamental forecast, but the fall 2023

contracts are now $8-10 above the fundamental forecast. USDA had

some issues getting reports out in a timely fashion this week as one or

more packers were late in submitting their daily data. That problem now

appears to be corrected. This week’s slaughter registered 2.57 million

head, up 20k from the week before. This was a “big Saturday” week and

that meant that packers over-killed the pig crop slightly.

Still, for the Sep/Nov quarter as a whole, so far the kill has only fallen

short of the pig crop by a little over 100k. Not a big miss, and not much to

be concerned about. Next Saturday’s kill should be smaller and we may

see the total kill drop back to 2.55 million head. The Mar/May pig crop

projects the maximum weekly kill this fall at 2.61 million head, so we are

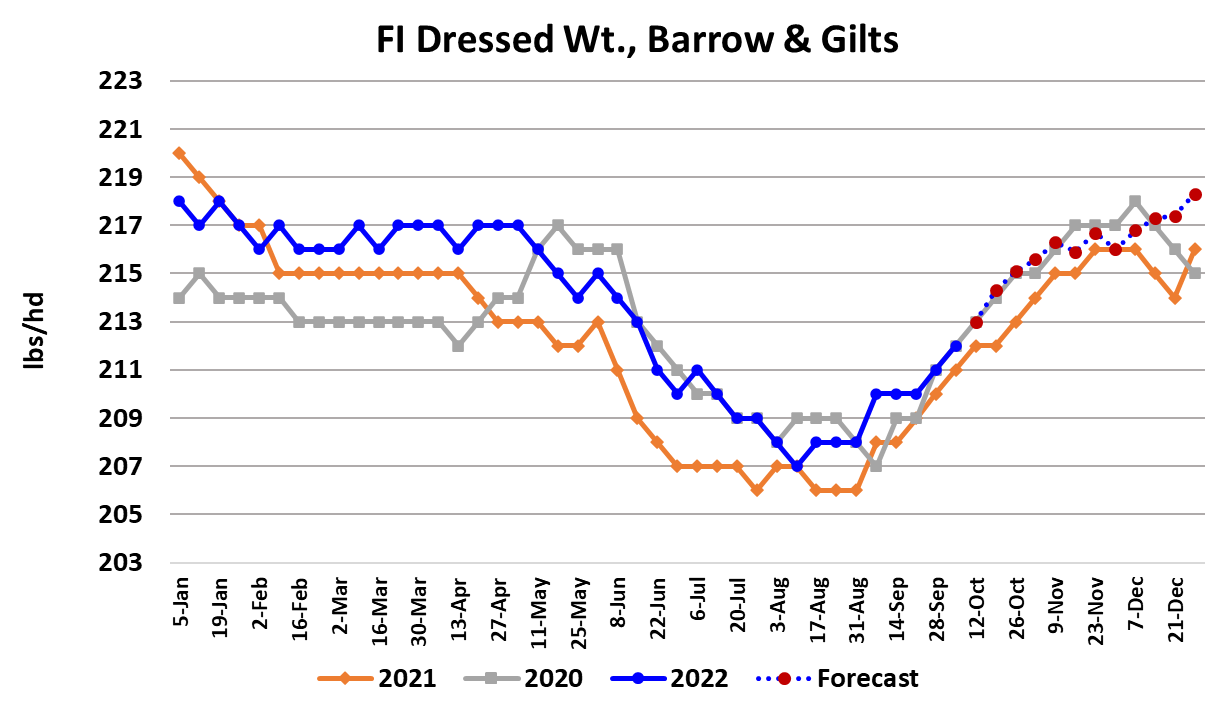

getting really close to a top in slaughter levels. Hog carcass weights

were one pound higher this week, but that is typical for this time of year

and the DTDS weights aren’t indicating any problem with hogs backing

up in the system. Low water in the Mississippi River system has

hampered efforts to export corn and we are now seeing cash corn in the

Midwest go discount to the futures for the first time since early June.

Even so, corn costs for hog producers are way higher than in recent

years and are likely a big factor discouraging expansion in the hog

production sector. Hog and pork prices in China have been steadily

increasing and that has raised hopes that soon Chinese buyers will

increase their orders for US pork. Some of the recent strength in the

deferred futures is probably linked to trader hopes for stronger pork

exports to China in 2023. It is possible that we could see improved

interest from China over the next few weeks as the deadline for shipping

pork to arrive in time for the Chinese New Year moves closer. Next week

watch the early-week cutouts closely for signs that packers have been

able to coax more money out of pork buyer to help cover their higher hog

costs. Keep an eye on the negotiated hog markets also, because the

longer they remain at these elevated levels, the more bullish the outlook

becomes.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}