Pork Wrap October 20

Hog and pork prices continued

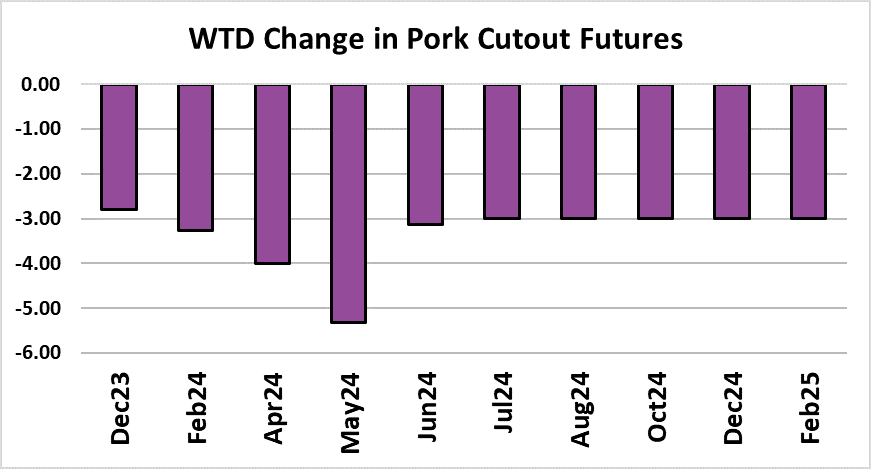

lower in normal seasonal fashion this week. The cutout dropped $3.87/cwt.

on a weekly average basis to $88.76/cwt. and the WCB negotiated market was

$1.38 lower to average $72.58/cwt. Given that the cutout was down

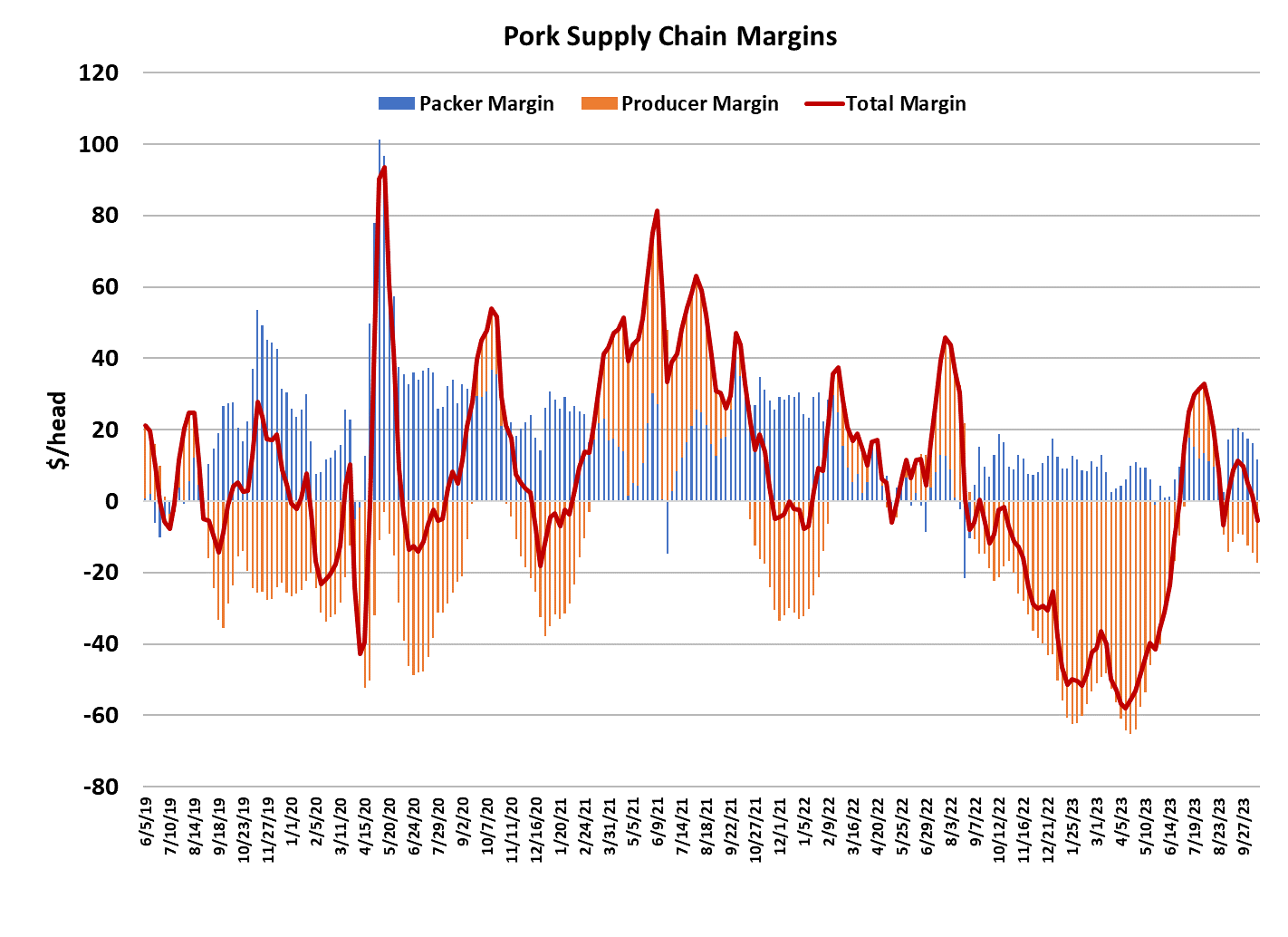

more than cash hogs, packer margins compressed. I estimate packer margins

at a little over $12/head this week, down about $4 from last week. The

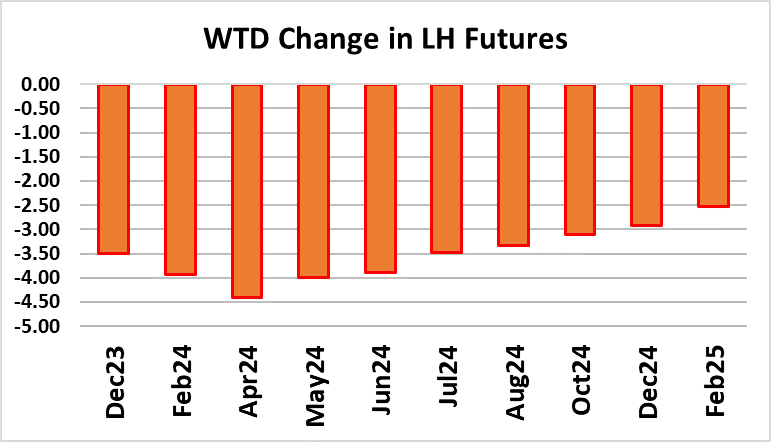

futures market didn’t like this week’s action much at all as most contracts

lost more than $3 on the week. The decline in the cutout was a bit

larger than last week and thus traders may sense that the downtrend is

steepening and thus the need for a bigger discount on the Dec contract.

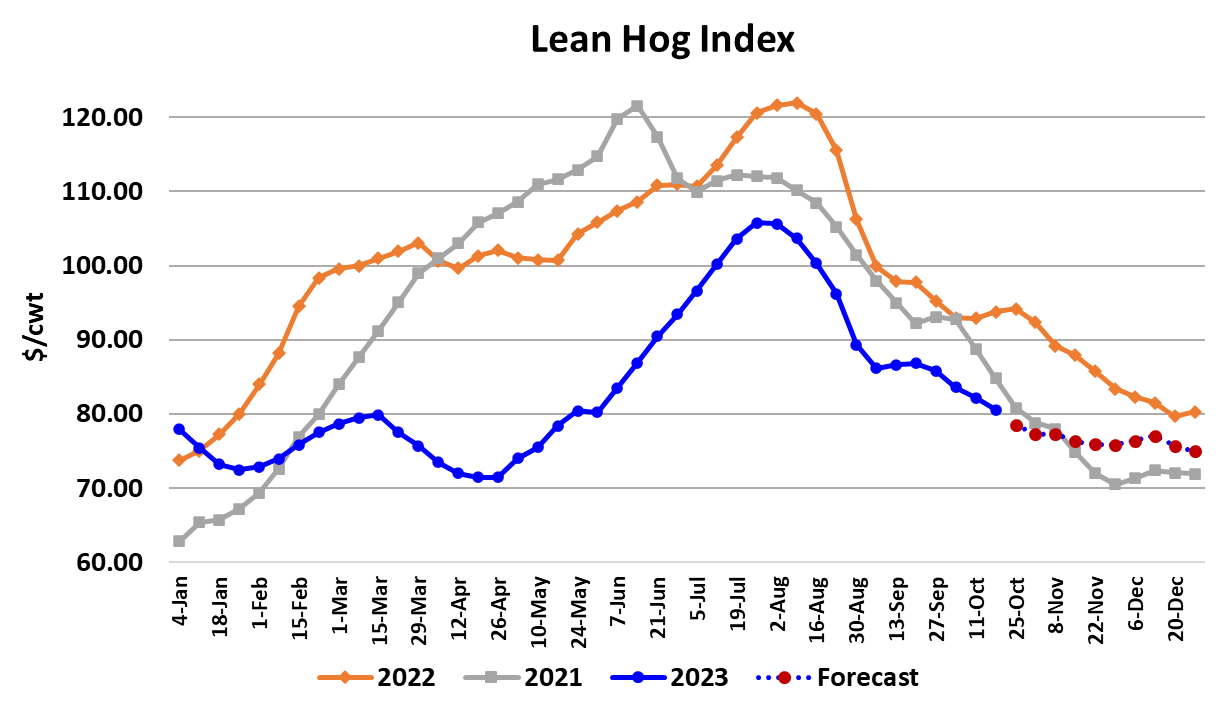

However, the basis is very near -$13/cwt. and that seems excessively large in a

year where there are no signs of hogs backing up or demand eroding rapidly.

It is certainly possible that the LHI could lose $13 over the next seven weeks

and reach the $66 level that traders put on the Dec contract today, but that

seems like a stretch. I would vote for something closer to the

mid-$70s. For one thing, we should expect packer margins to remain rather

narrow in a historical context this fall and winter because the hog herd is in

decline but packing capacity remains static. We saw this last year in the

fourth quarter when packer margins averaged $12.20/head—well below the 10-yr

average of $25/head. This year I am plugging in an average margin

of $16/head for Q4 and think that maybe that could be too large. The

smaller the packer margin, the higher the LHI for a given cutout. I think

that the fact that we saw cash hog prices hold up well this week compared to

the cutout is a sign that margins this fall are not going to blow up to the

$30-50/head range that we have seen at times in the past during Q4.

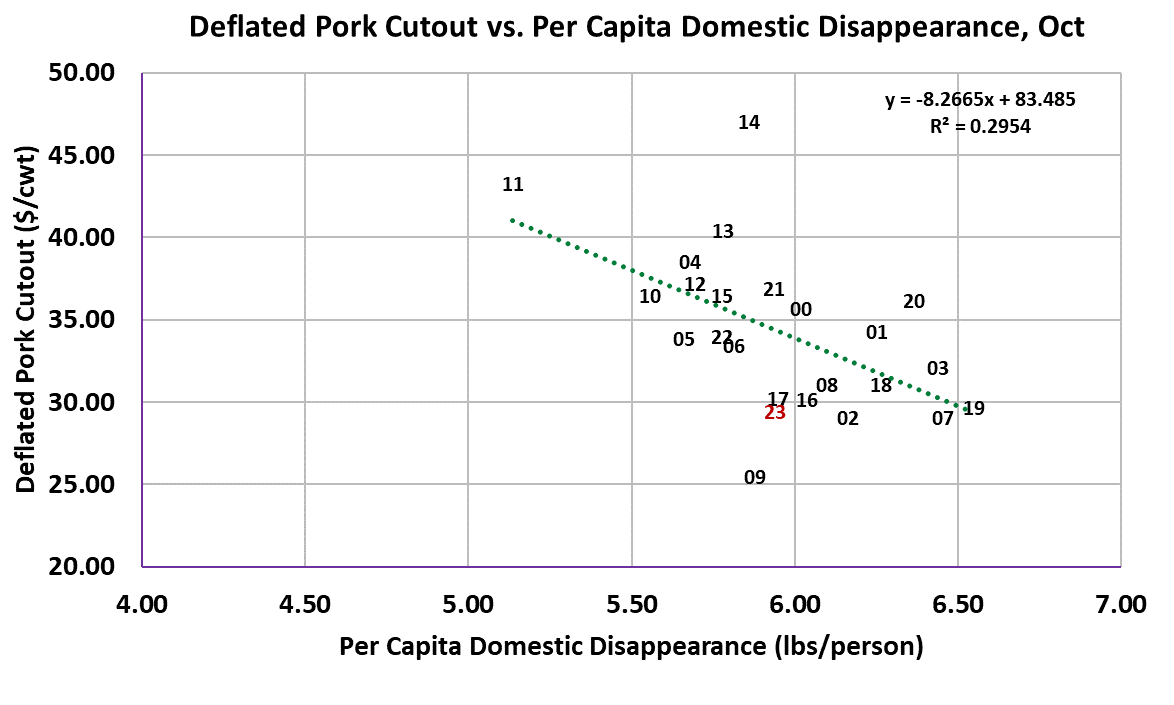

Demand is already fairly weak (see attached scatter) so do we really want to

bank on it getting a lot weaker? The combined margin is still in a

downtrend, but those small demand cycles normally only last 6-8 weeks, so we

should be getting close to the point where that margin stabilizes and perhaps

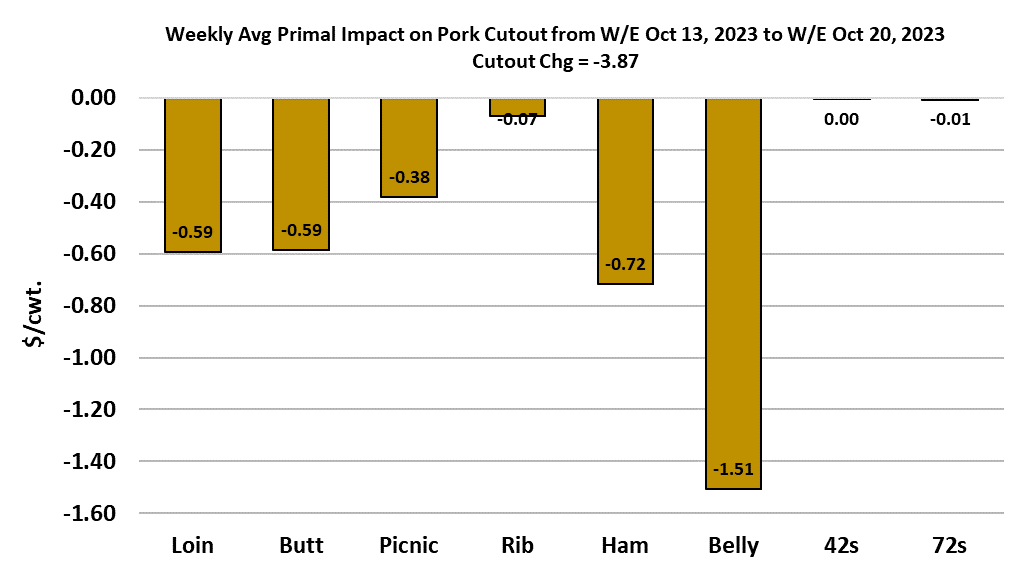

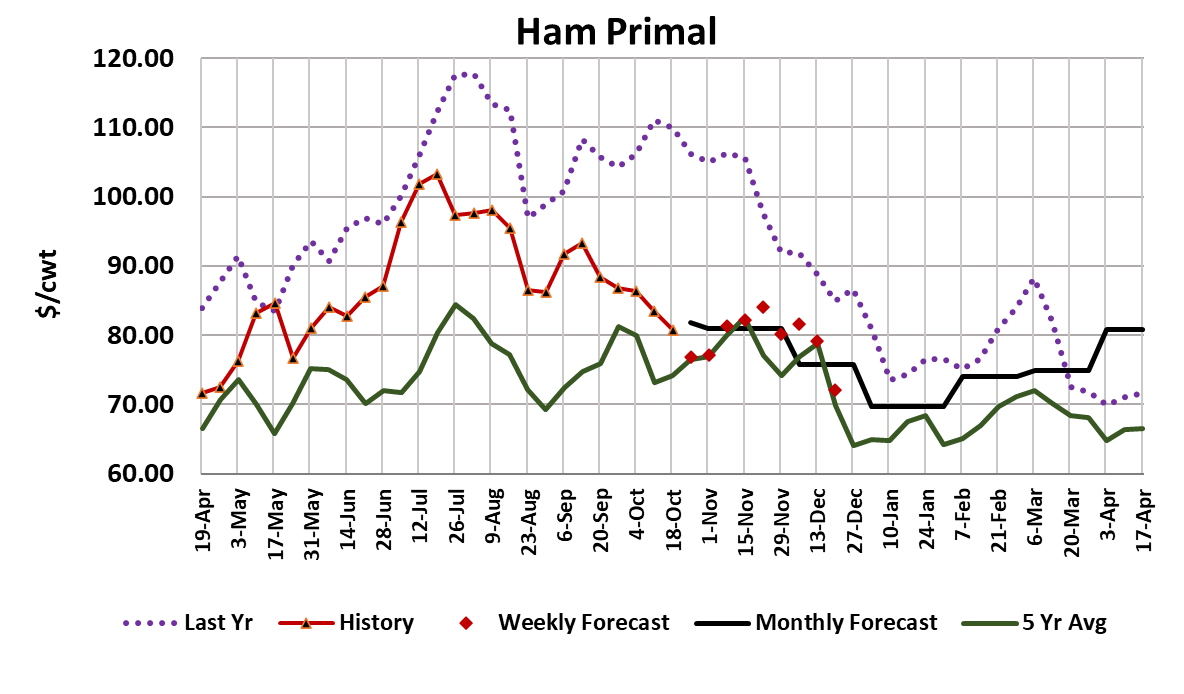

turns higher again. This week, all of the primals were lower with the

bellies leading the way once again. Belly prices should be getting

low enough now that they encourage users to start stockpiling in cold

storage. The slide in ham prices seems to be slowing, so perhaps that

primal is approaching a near-term bottom. This is the time of year that

we normally count on Mexico to help clear the market for hams. Mexico’s

internal hog and pork prices are high, so that should encourage strong interest

in cheap US hams. Hams are such a big contributor to the cutout that, if

they turn higher, the cutout will also likely post some gains. Prices for

the retail items continue to work lower and that is probably tied to big kills

and packers having to lower prices to clear big production. This week’s

slaughter was pegged at 2.61 million head. That was only a tiny bit

larger than last week’s total and the largest weekly kill since the second week

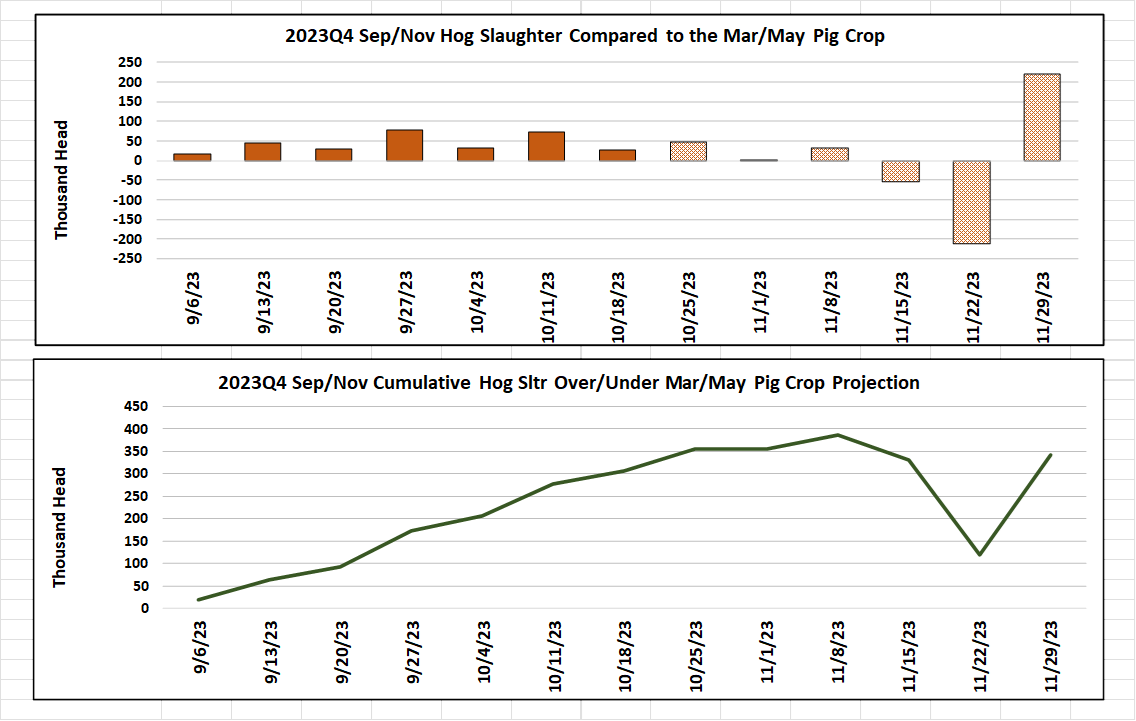

of January. Kills are running larger than what USDA’s estimate of the

March/May pig crop suggested. That pig crop was up 1% YOY and slaughter

so far in the Sep/Nov quarter is running about 1.5% stronger than last

year. These overkills haven’t been huge, but they have been consistent

(see attached chart), and that makes me think that the pig crop is larger than

advertised. However, barrow and gilt carcass weights are still 4 pounds

below last year and that has largely negated the impact of the bigger

kills. If I assume that the overkills are going to continue at the same

pace through the balance of the Sep/Nov quarter, then I can see the possibility

of one or two weekly kills near 2.63 million head this fall. That would

be the top and isn’t very far from where kills are at today. So, going

forward, there should be very little additional supply side pressure on prices

and further price declines will need to reflect deteriorating demand

conditions. We’ve already established that demand is pretty weak right

now, so the potential for substantially softer demand in the next couple of

months would seem rather low. Of course there is the fatigue effect that

can happen as large kills continue week after week and consumers can’t, or just

don’t have the need, to stuff more pork in their freezers. The short kill

in Thanksgiving week often provides some relief from the fatigue effect and

demand often picks up following that holiday. As a result, I think

that the prices this fall might take the path of gentle easing from now until

the end of November and then turn higher as the calendar turns to December.

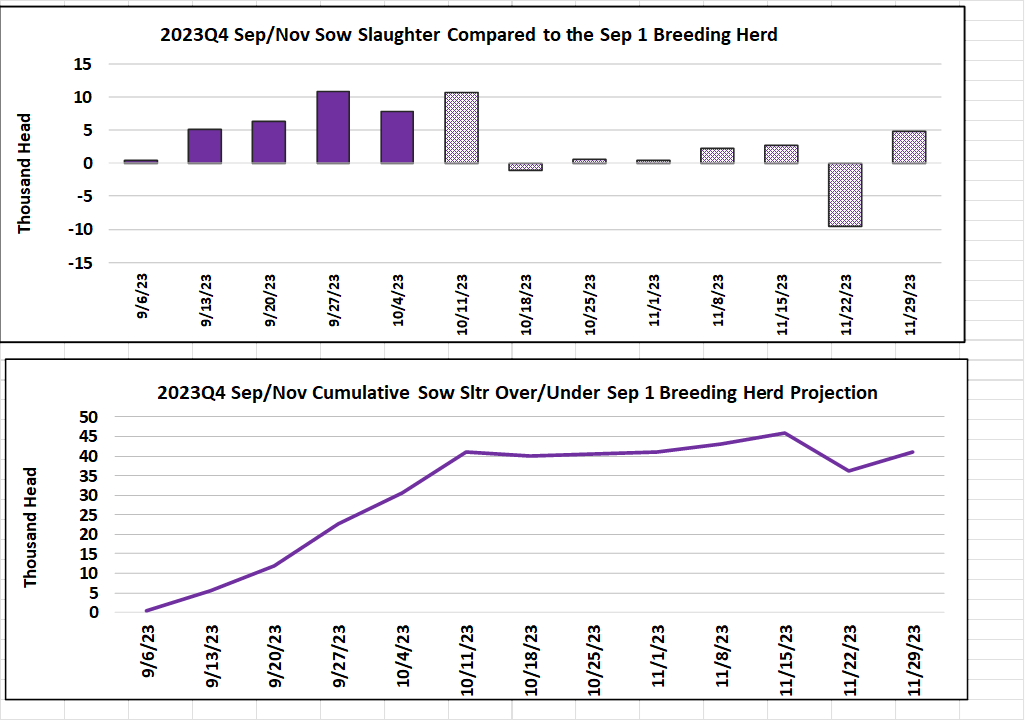

Hog producers are actively liquidating sows. It looks like producers have

already sent 40,000 more sows to slaughter in the current quarter than what

would be expected given the breeding herd size on Sep 1. That is a clear

signal that supplies are going to tighten in 2024 and unless there is a serious

demand collapse, price levels should be higher next year than what we saw this

year. The summer 2024 futures continue to get dragged lower by the

extreme pessimism in the front of the futures curve and that has generated a

big gap between where those contracts are currently trading in the low $90s,

and the fundamental forecast for something above $100. Next week is

likely to bring more of the same—modest declines in the cutout and cash hogs.

At some point, perhaps soon, traders will look to correct the very wide basis

to the nearby contract.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}