Pork Wrap October 15

The cutout was lower for the second week in a row, dropping $6

on a weekly average basis. The negotiated hog markets were

down less, losing only about $2/cwt. That caused packer margins

to compress about $5 on the week, now sitting just a hair below

$30/head. Further erosion in ham prices are largely responsible

for the decline in the cutout this week, although by the end of the

week, some of the retail items were starting to soften. That

leaves bellies as the sole item providing support to the cutout and

that primal could be just about to turn lower also.

This leaves the cutout at risk of falling below the $100 mark in the

near future. The breaking of that arbitrary, but psychologically

important barrier, could give pork buyers a reason to pull back

unless they have immediate needs. That said, there is no

guarantee that hams are going to continue to weaken. I’m calling

them a little lower next week, but then rallying into month’s end. If

the hams do indeed turn higher and the bellies continue to hold at

current levels, then there is a possibility that the sub-$100 cutout

could be delayed a bit. All of the buying for “pork month” is now

behind us and retailers will probably be looking to give beef a little

more ad space between now and Thanksgiving. That could leave

the retail items—loins, butts, ribs—taking a back seat as we move

into November. I don’t want to give the impression that pork

demand is not strong, because in a historical context it is very

strong.

However, the combined margin (chart below) took a significant

turn lower this week after only two weeks of strength. So the

previous two weeks are starting to look more like a head fake in an

overall downtrending demand environment. And maybe that is

how it will go as demand starts to cool after a year and a half of

super-strong demand. The overall trend could be lower, but it

may be punctuated with periodic strengthening episodes as one

primal or another catches fire for a brief period. Meanwhile, on

the supply side, kills are increasing seasonally and will continue to

do so for 6-8 more weeks. This week’s slaughter came in at 2.64

million head, including more than 250k on Saturday. That should

improve availability next week and is another reason why we might

see further losses in the cutout. The kill was very close to what

the pig crop implied for the second week in a row after several

weeks of running below what the pig crop projected.

Of course, the inventory numbers in the last Hogs and Pigs

report pointed to a 5.8% YOY reduction in weight categories

that will be slaughtered in late October and through November.

I don’t normally put a lot of faith in those inventory numbers,

preferring instead to track the pig crop through to slaughter.

This week’s kill was 3.3% below what looks like a very big

number from last year.

So right now, the supply of market hogs appears pretty ample.

That could change, but I’ve never seen the hog supply get

really tight in Nov/Dec. It just doesn’t happen. Detectable

tightness in supply might start to surface around the holidays

and into January as the industry starts working on the Jun/Aug

pig crop, which was reported down 6% YOY. Between now and

then however, I look for hog supplies to be plenty adequate.

The price that packers pay for negotiated hogs was under less

pressure this week than it has been in earlier weeks, but I really

don’t expect to see negotiated prices turn upward and march

higher at this time of year. Packers will likely struggle to push

all of the market ready hogs through the plant this fall, given

their labor issues and so I don’t see them having much

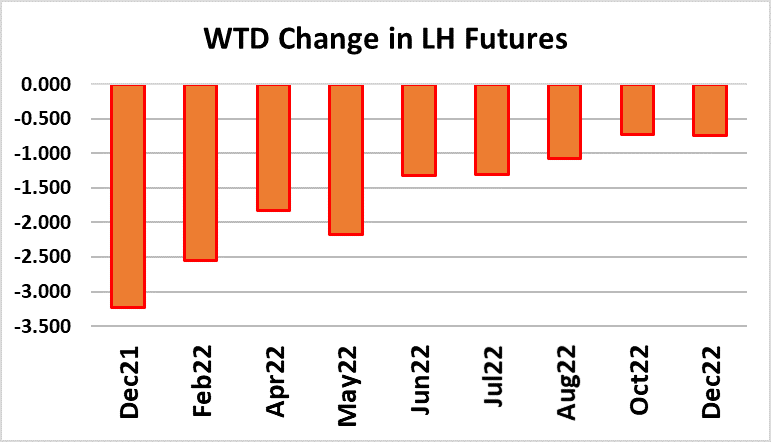

incentive to chase after negotiated hogs. The futures curve for

hogs pressed lower this week, with the biggest losses coming

in the front end of the curve.

The market was led lower by the expiring Oct contract, which

will cash settle at $87.60 on Monday. At expiration time on

Thursday, the final trades were done at $88.20, so someone

left a lot of money on the table. There were 9,300 Oct contracts

left open at expiration that will cash settle. The gap between

the last trade price and the cash settlement price amounts to

$2.2 million that will be transferred from the open longs to the

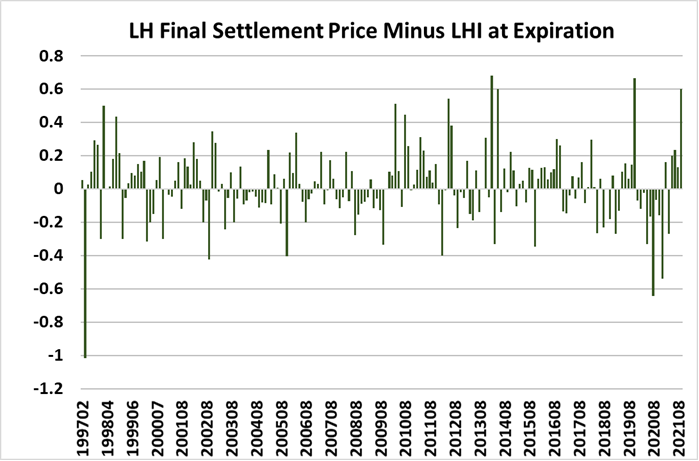

open shorts next week. This expiration was one of the six

worst misses since cash settlement was instituted for lean hogs

back in 1997 (chart below). Next week, look for the hams to

finally find a bottom and turn higher. That may just about the

same time that the bellies decide to break lower.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}