Pork Wrap October 14

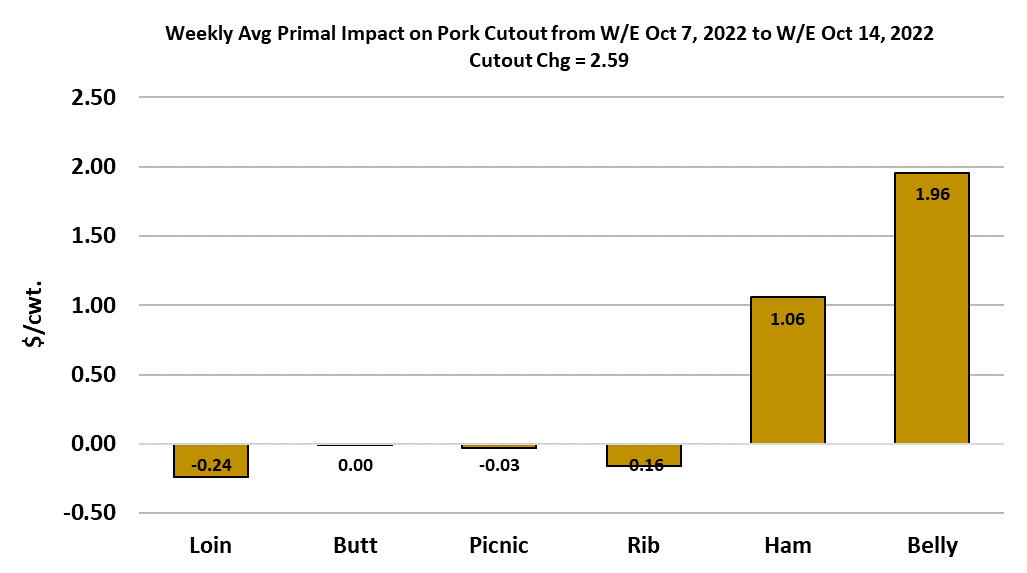

The pork cutout pressed higher for the second week in a row,

averaging $102.68/cwt., up $2.59 from the week before. Almost all of

this gain was accomplished on the back of the bellies and hams. The

retail primals were all steady to slightly weaker. While the pork was

gaining value, the hog market was slipping lower. The NDD

negotiated market was down $1.06/cwt. this week. The gains in the

cutout almost offset the softer negotiated markets to keep the LHI

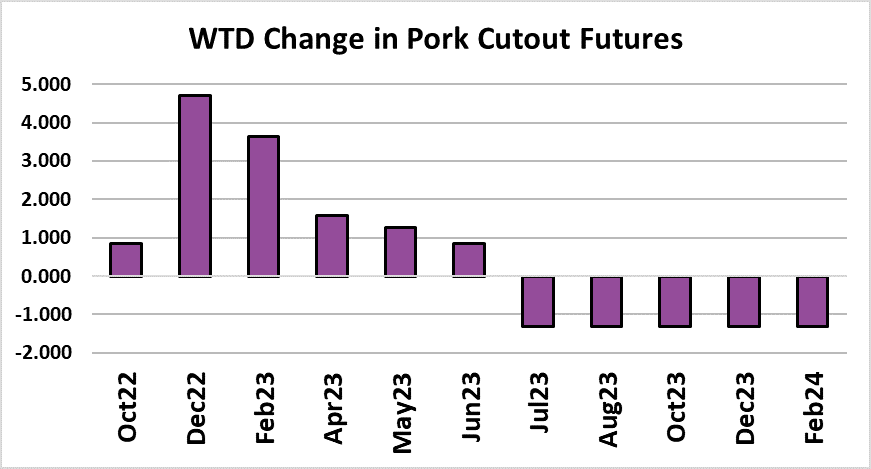

mostly steady for the week. The Oct futures went off of the board

today at $93.38, about seven dollars lower than where it was when

the August contract expired and Oct became the nearby. Aug LH

futures expired near $122 and Oct expired near $93, indicating an

almost $30 drop in the LHI over the past eight weeks. That is a very

rapid decline in a historical context, but the index was at an extreme

level when the move began. I don’t think we should expect the drop

between Oct and Dec to be anywhere near that large. In fact, there is

an outside chance that Dec could expire relatively close to the where

Oct made it’s exit.

Right now, the fundamental forecast is projecting the LHI at $87 for

the second week of December. The conditions are way different now

as compared to when Aug expired. The cutout is working higher, not

lower, and there is very little seasonal pork production increase left to

occur. I don’t think that the cutout has a lot of additional upside

potential, but I’m forecasting it to hold over $100 for another 2-3

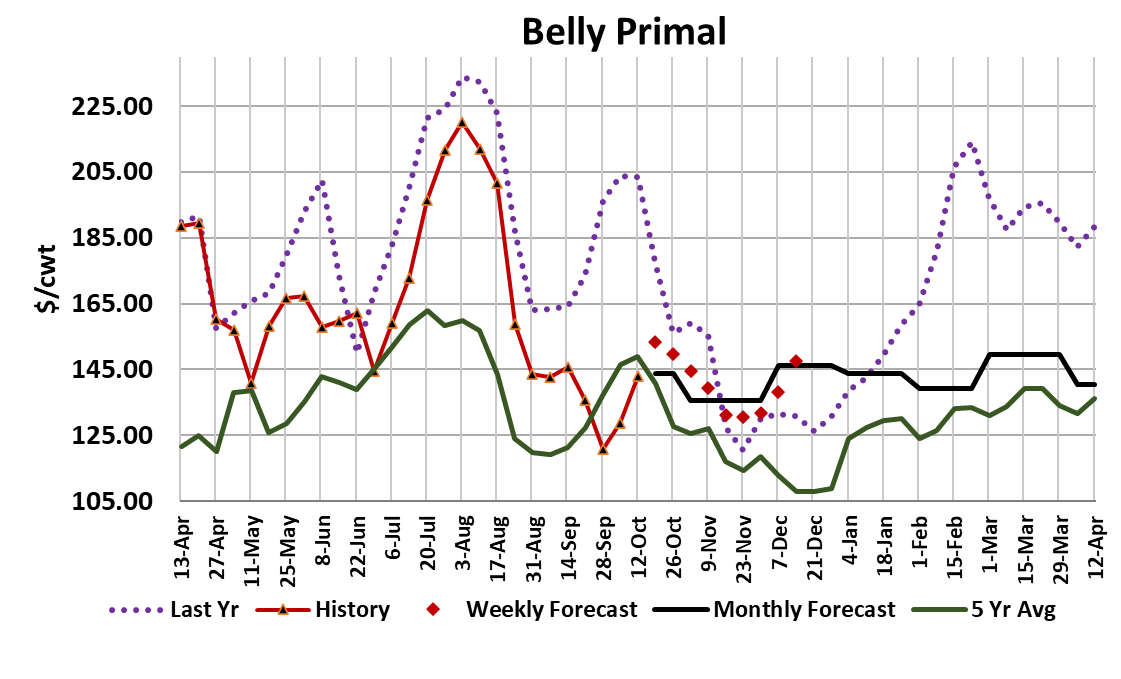

weeks before it starts to sink into the upper $90s. The bellies look like

they may be running out of gas soon and without that help it is going

to be difficult to maintain an upward trajectory in the cutout. Still, the

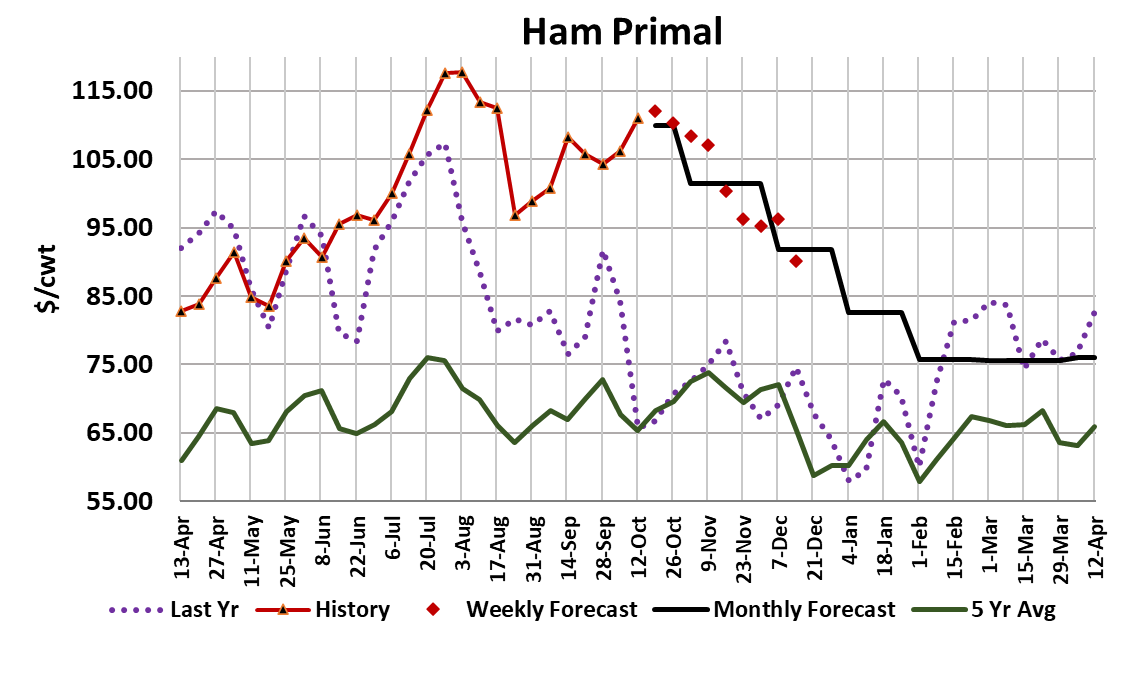

hams are performing exceptionally, and if that continues then the

downside risk in the cutout is probably limited to the low to mid $90s.

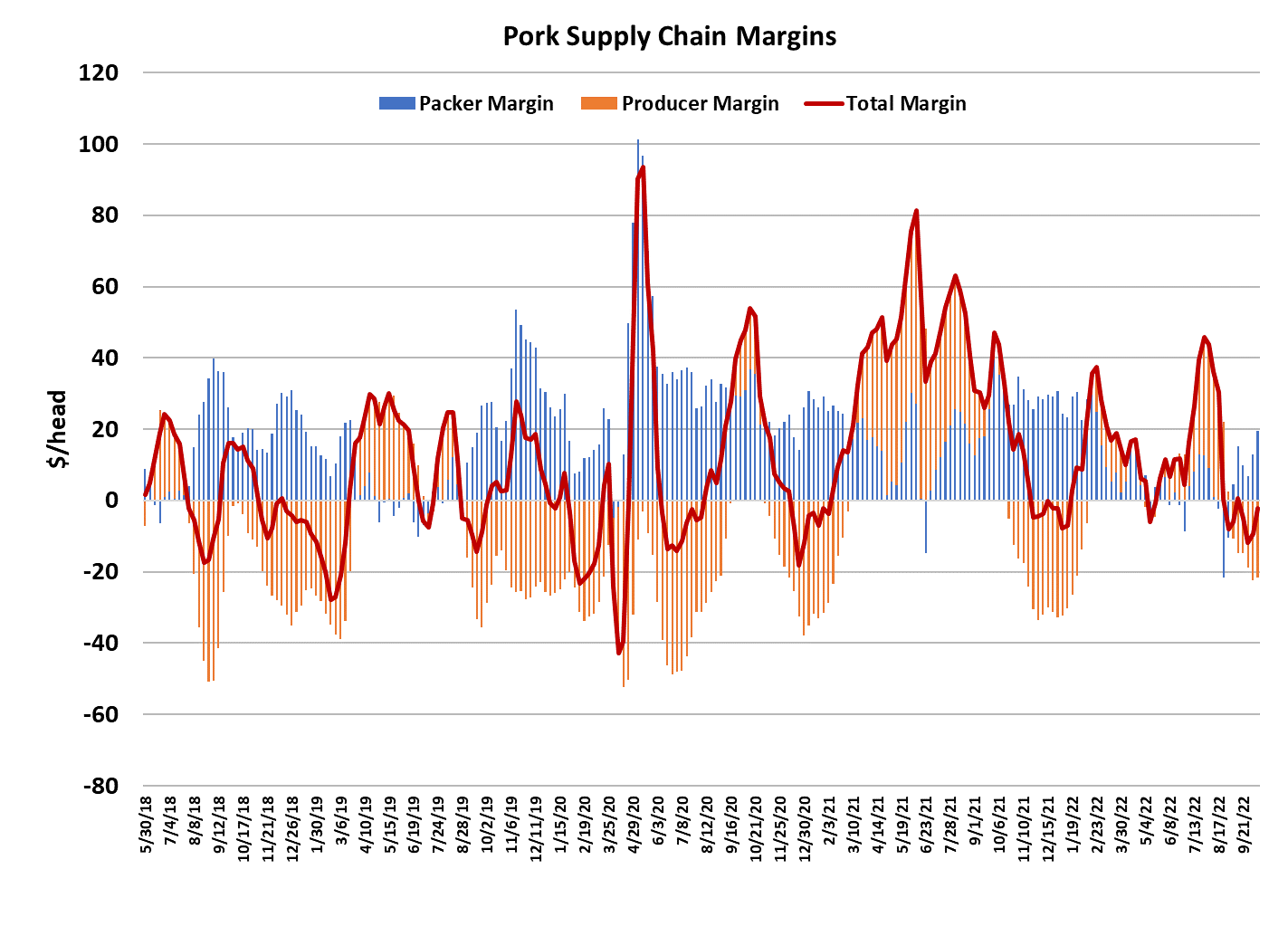

Packer margins improved to $19/head this week. up about $6 from

last week. That margin is still below normal for this time of year, but it

is a lot closer to normal than it was just 2-3 weeks ago. It turns out

that the cutout saved the day for packers.

Their margin improvement came largely from the cutout halting its

drop and turning higher—not from serious pressure in the cash hog

market. In fact, cash hogs seem to be holding up very well given the

seasonal increase in supplies. Last year at this time the WCB

negotiated market was averaging close to $70 and this year it is very

near $90. That tells me that the supply of hogs is a little snugger than

packers would like and they are having to compete a little harder for

those negotiated hogs than they have in years past. Also, last year at

this time packers were struggling with labor issues that effectively cut

their processing capacity and thus gave them more leverage in the

cash hog market. This year, the labor issues have been solved and

packers want to utilize their capacity as best as they can. The

forecast has packer margins holding in the $15-25/head range

through the balance of the year. That is smaller than normal for Q4,

but it makes me feel a lot more comfortable that I can now get to believable cutout and LHI forecasts without having to assume excessively

tight packer margins.

Hams and bellies have really helped in that regard. I’m calling the bellies higher for one more week and then expect them to ease lower through most of November when peak production occurs. Hams are a more difficult call. Right now they are about $42/cwt. over last year and the

five-year average. It doesn’t seem likely that huge gain will persist, so I’ve got them working lower in the weeks ahead and by the time we get to the middle of December they may only be $15-20/cwt over last year. I think the current strength in hams is related to strong export interest into Mexico and some last minute processing demand ahead of the holidays. It is really hard to get big drops in the cutout without the hams pressing lower so the cutout is forecast to hold above $90 for the remainder of the year and may very well hold above $95. One thing that makes me somewhat bullish on the cutout is that the combined margin now looks like it has turned decidedly higher after making a low in the area where lows used to occur prior to the pandemic.

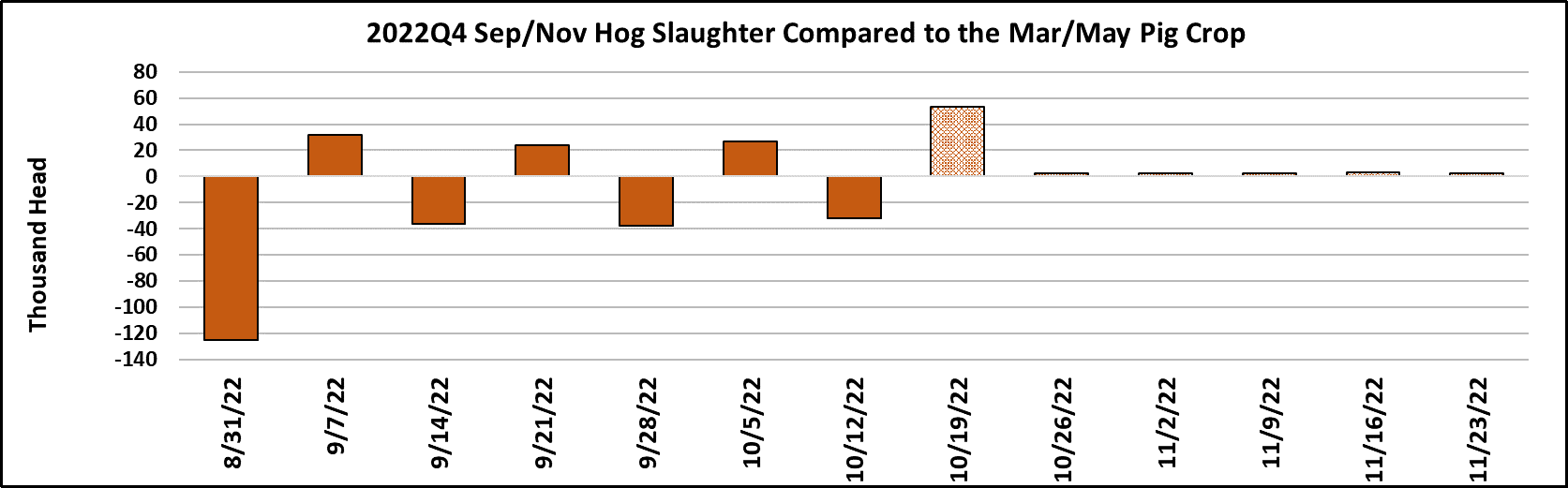

Another factor to consider is that pork production isn’t really going to grow a whole lot larger than what it registered this week. Slaughter was estimated at 2.55 million head and it looks like next week may be closer to 2.59 million head because packers are planning a larger Saturday kill next week. Note the alternating pattern in the “slaughter compared to pig crop” chart. On balance, the positive deviations offset the negative ones so that actual slaughter in the Sep/Nov quarter so far isn’t too far off what the pig crop implied. However, it seems like at least one or more major packers is

alternating big Saturday kills with smaller ones. This week was a smallish

Saturday kill at 113k and next week will be a larger Saturday at 165k. I don’t really remember seeing that type of pattern in previous Q4s, so something out of the ordinary must be going on. If USDA’s estimate of the Mar/May pig crop was correct, and so far it seems that way, then the peak kill this fall should be close to 2.61 million head. We are almost there.

So if demand is entering an upcycle and supply really won’t grow a whole lot larger, then it is possible to make the case for a rising cutout over the next few weeks. Dec futures bears should take note. Carcass weights are still behaving normally. Barrow and gilt weights were up one pound this week and probably have a few more pounds to add in the next couple of months before they reach their seasonal top. The DTDS is still relatively low, which suggests that hog producers are remaining current in their marketings. One more bullish factor to throw into the mix is that the weekly export data is showing some improvement in shipments and sales to China again. That may reflect buying in anticipation of the Chinese New Year holiday, or it could just be due to higher pork prices within China, but anytime a buyer the size of China starts to show signs that they want more US pork, it tends to wake up the bulls. This trend is just getting started, but should be watched closely in the weeks ahead. Next week, look for the cutout to build on this week’s gains and that might even add a couple of dollars to the LHI. As usual, hams and bellies will be the key to making that happen

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}