Pork Wrap October 13

This week’s surprise in the

hog and pork complex was an increase in cash hog prices. The WCB

negotiated market added $1.40/cwt. and the National Daily Direct negotiated

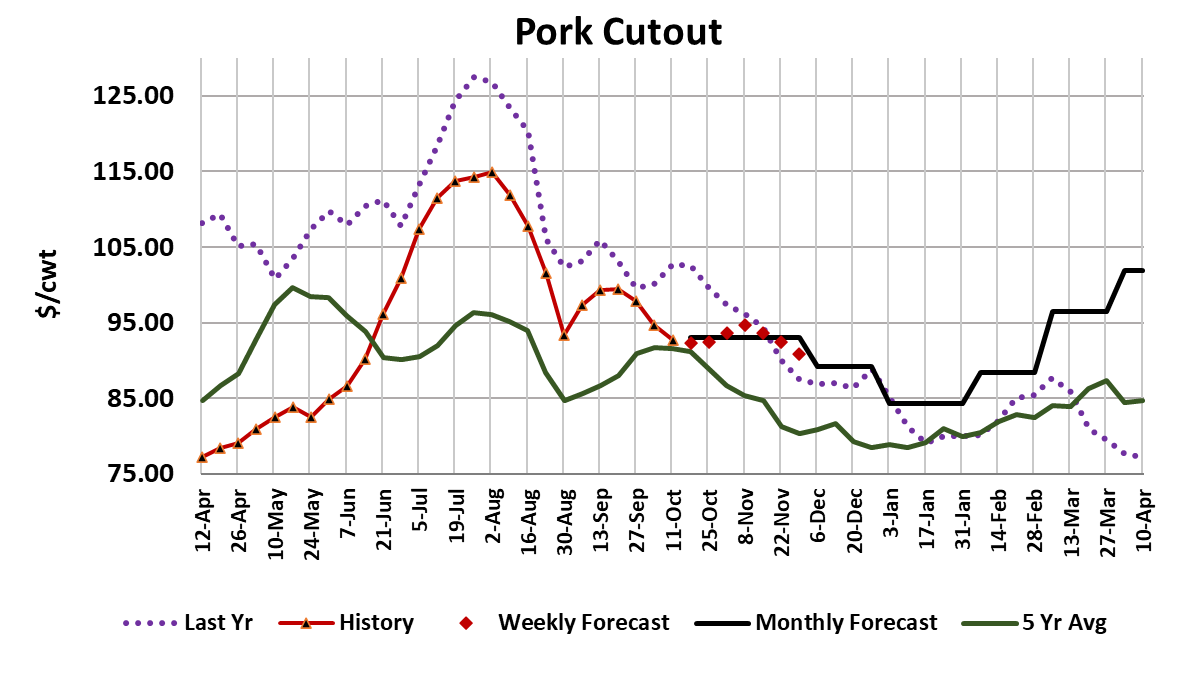

market averaged $1.42/cwt. higher. At same time, the pork cutout was

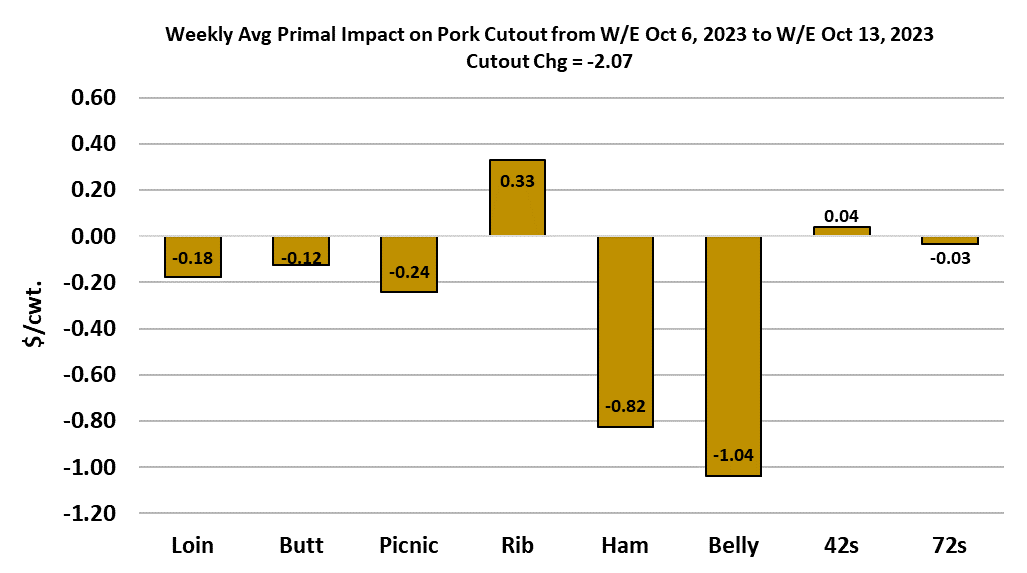

continuing on its downward path, dropping $2.06 to average $92.63. That

put some pressure on packer margins, moving them down to about $15/head.

It does make one wonder what prompted packers to pay up for negotiated

hogs this week if the cutout was declining. Maybe packers are just trying

to run the kill too hard for available supplies because their margins are

relatively good. This week’s slaughter came in at 2.61 million head, up

2.1% from last year. Next week’s kill is likely to be smaller, perhaps

down around 2.58 million head. We are starting to see the return of the

alternating “big kill then smaller kill” pattern, but in reality the

differences aren’t huge. I don’t expect the weekly kill to exceed 2.63

million head this fall, so we are now pretty close to the largest kills of the

year. Of course, this begs the question, “if kills aren’t expanding much

beyond current levels, does the pork cutout need to decline much beyond current

levels?” The quick answer would be no, but there is a certain cumulative

effect that happens when production stays very large for many weeks. Some

observers have used the phrase “pork fatigue” to describe this

phenomenon. It happens because hot retail features can keep product

moving out of the stores briskly at first, but if a retailer tries to feature

pork every week eventually consumers have filled their freezers and the feature

becomes less effective. Product movement slows and lower prices are

needed to encourage commercial users to put product into cold storage as a

hedge against higher pricing the following spring and summer. So,

even though slaughter levels won’t grow much from here, we should still see

some modest ongoing pressure on the cutout. That said, Dec pork cutout

futures at $79 looks way too pessimistic to me. I would vote for a

mid-December cutout in the mid to high $80s. It is fairly common for

traders to believe that something that has been trending lower will continue

that way, especially after last winter and spring where it seemed like the

downtrend in prices would never end. That kind of thinking has probably

pushed the Dec LH and cutout futures too low, but traders might not be willing

to rally those until they actually see the price declines slow or reverse.

There will almost certainly be one or more weeks between now and Dec expiration

when the cutout bumps higher. That will get trader’s attention and

everyone will be wondering how those contracts got so low in the first

place. For now though, the bearish psychology is in place. This

week, both the bellies and the hams helped drive the cutout lower. The

belly primal was quoted close to $110 on Friday afternoon and has struggled in

recent days. Last year, on similar availability, the belly primal went

all the way to $90 before flattening out. However, this year the industry

has worked cold storage stocks down and thus there should be more need for

“freezer filling” at low price levels. My guess is that will keep the

belly primal above $100 this year. Further, bacon has huge exposure to

the QSR sector, where it is used as a taste enhancer for boring burgers and

chicken sandwiches. As consumer spending slows and consumers trade down,

I would expect the QSR sector to see better sales and thus strengthen its demand

for bacon. Last year, the avian influenza outbreak wiped out a lot of

turkeys and turkey prices skyrocketed. As a result, a lot of Thanksgiving

demand was diverted from turkeys to hams, boosting ham prices. That

dynamic isn’t in play for this Thanksgiving, so it is reasonable the think ham

demand will turn out to be softer this year compared to last. There have

been a few new avian influenza hot spots reported recently, but the timing is

such that it probably won’t affect buyers decisions for Thanksgiving, which is

only five weeks down the road. That said, the ham primal has moved

lower for 4 weeks in a row now and should be starting to look attractive at

current price levels. High hog and pork prices in Mexico should continue

to encourage good movement south of the border. From here, I think the

downside risk in hams is limited but it might be another week or two before

they turn higher. The retail items continue to slowly ease as we move

deeper into the fall. That pattern is likely to remain in place until

Christmas. At some point however, a bounce in the bellies or hams is

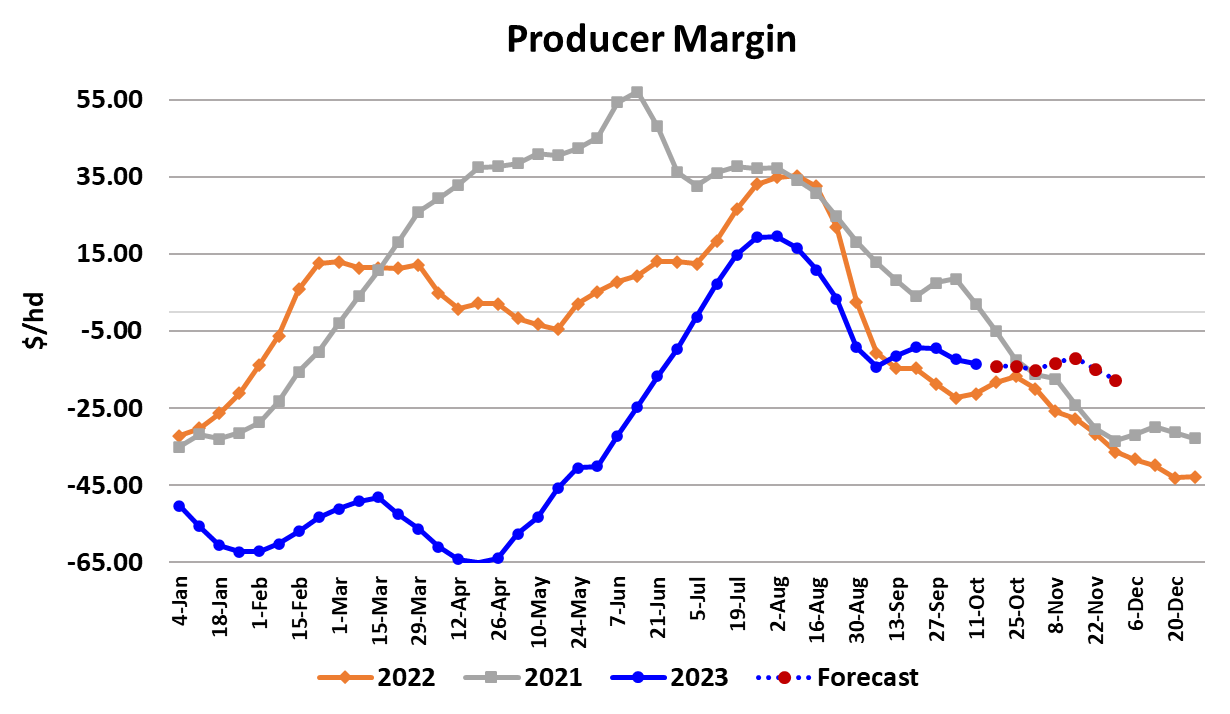

likely bump the cutout higher. With respect to cash hogs, I suspect that

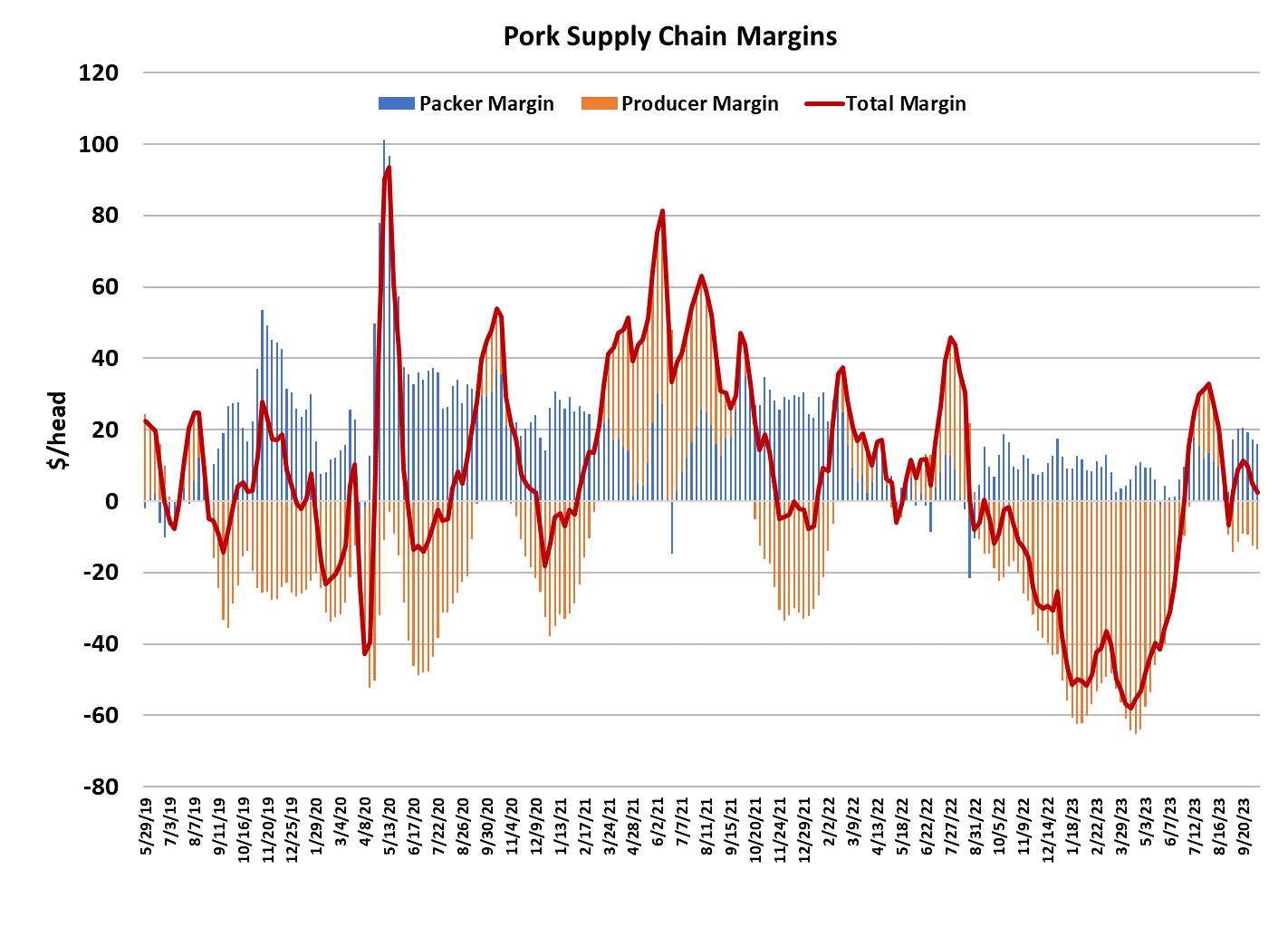

they will return to their downtrend in pretty short order. Packers have

been very good at managing margins over the past couple of years and I expect

that they will be quick to recognize when the kill is too large for the

available supply of hogs and dial it down enough to keep hog prices moving

lower. Hog prices often bottom in early December, so there may only be

another six weeks or so where hog prices are on the defensive. Barrow and

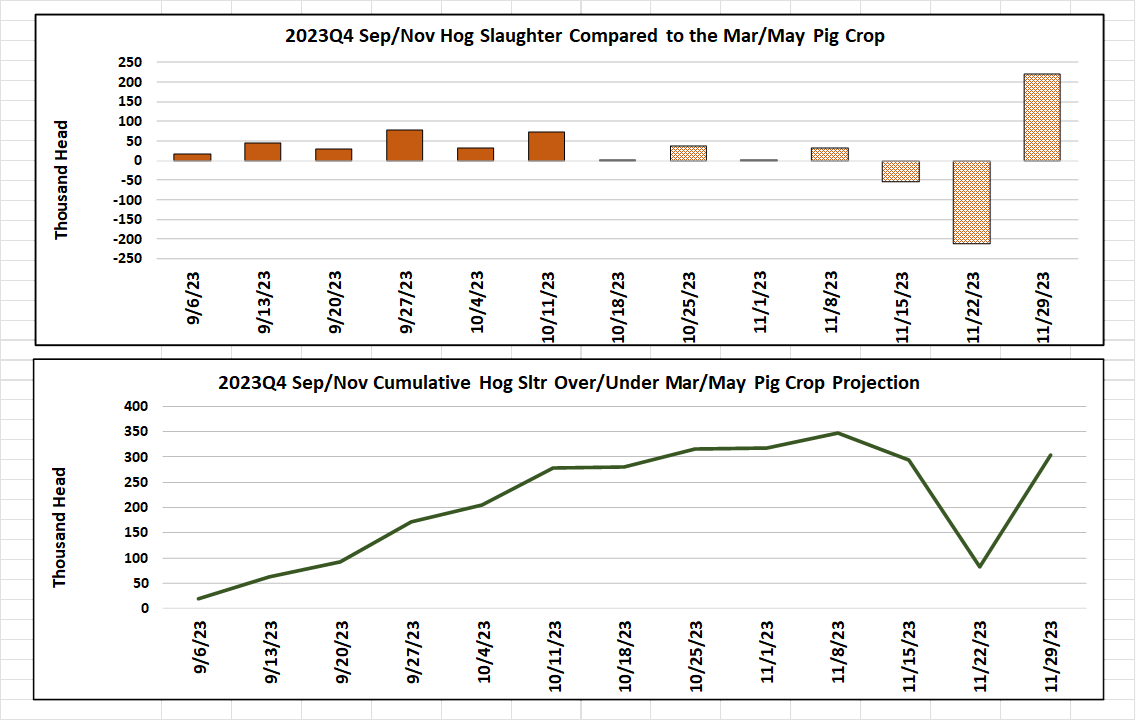

gilt carcass weights held steady this week at 207 pounds, but are still in a

seasonal uptrend. I’d see weights peaking around 214 pounds near the end

of the year. The de-trended and de-seasonalized weight continue to track

at very low levels, so it seems that producers are keeping current on their

marketings and there is little risk of a backlog developing this fall.

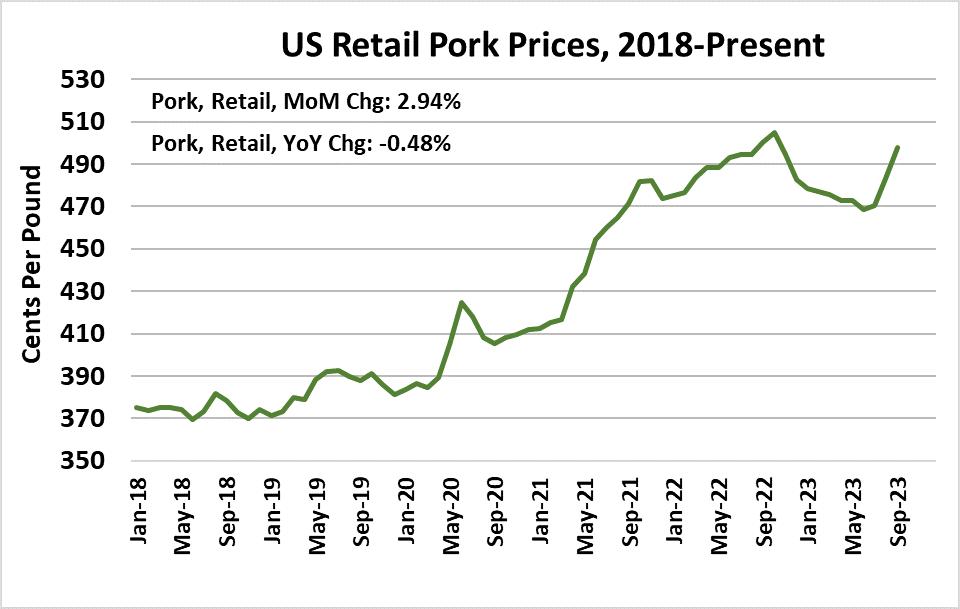

One piece of bad news that came across the wires this week was a sharp increase

in retail pork prices during September. USDA’s survey indicated that

retail prices gained almost 3% between August and September. That is a

huge month-to-month increase and will make pork look a bit less competitive in

the retail meat case. I’m not sure why retailers felt the need to jack up

prices because the cutout averaged about $8 lower in September compared to

August. Their margins on pork must be looking pretty good now. In

any case, higher retail prices are bad news for movement through the retail

channel any time that they happen, but they can be especially detrimental in

the fall when the industry is needing to move its largest production of the

year. Next week, it will probably be more of the same: gentle easing

of the cutout and negotiated hog prices. Packer margins should get a

little better and producer margins a little worse.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}