Pork Wrap October 1

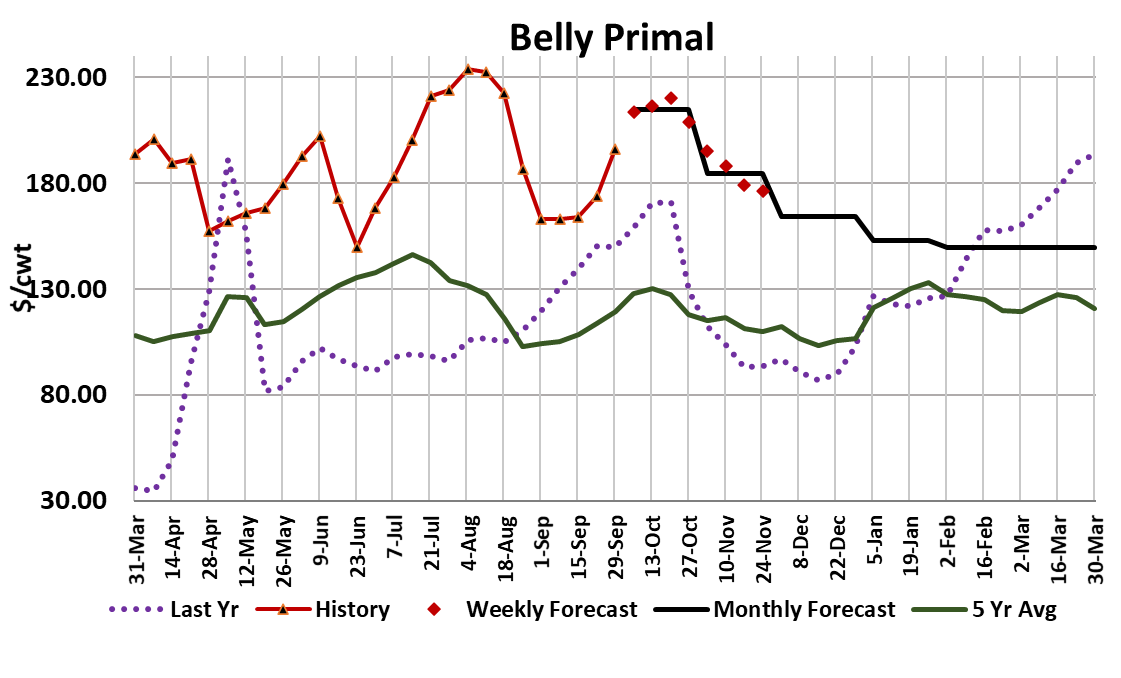

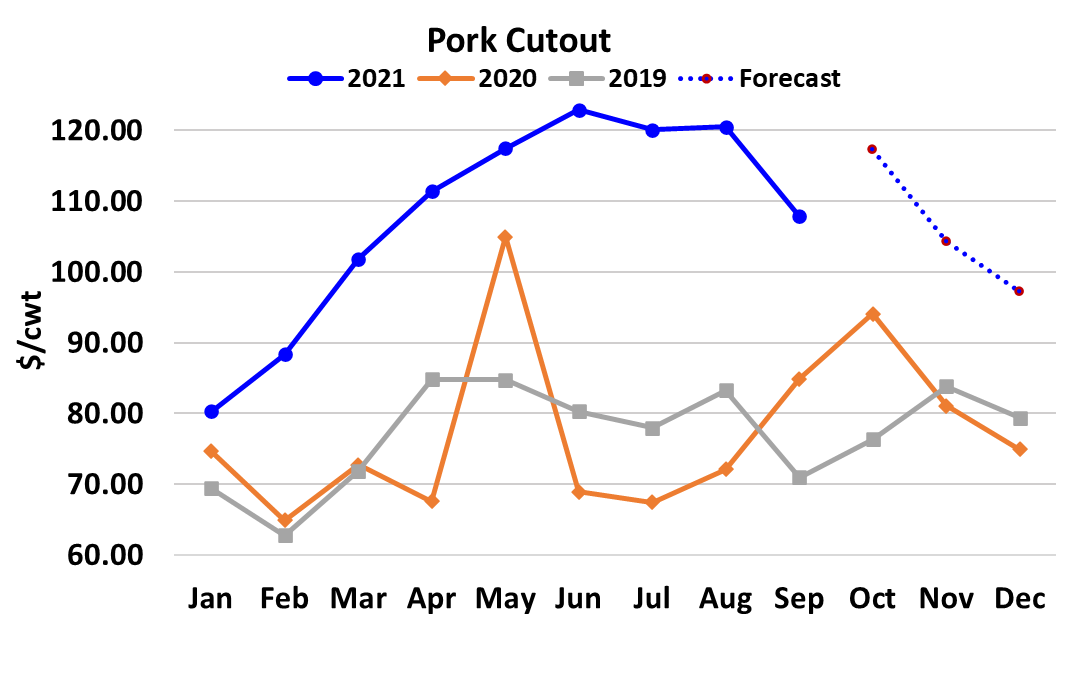

The big news in the hog and pork complex this week was a $7+ surge

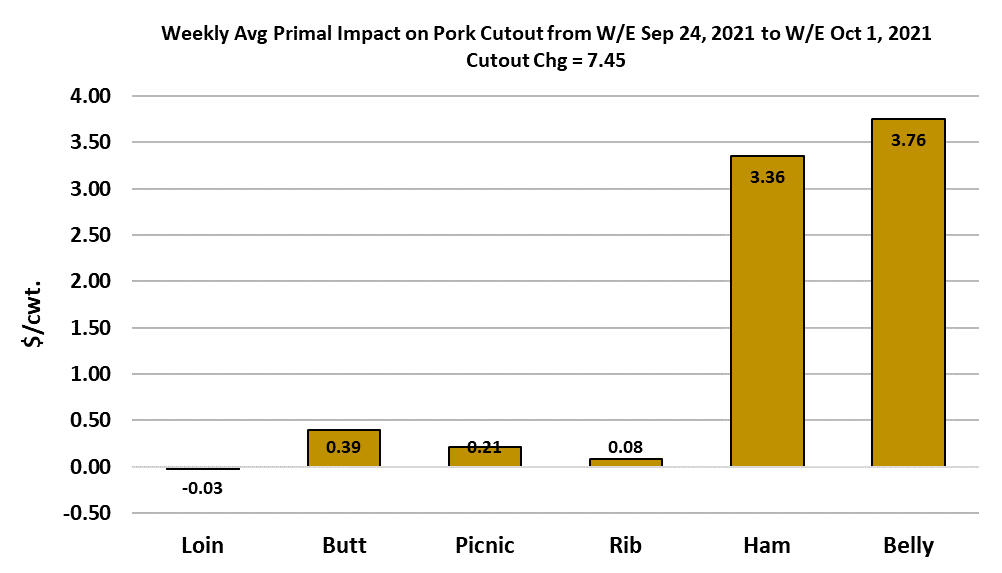

in the cutout (weekly average basis) that was driven primarily by strong

gains in the hams and bellies (chart below). The remaining primals

were pretty much steady on the week. The cutout gains were

impressive considering the size of last week’s kill. That makes me

pretty confident that pork demand has entered a new upcycle. The

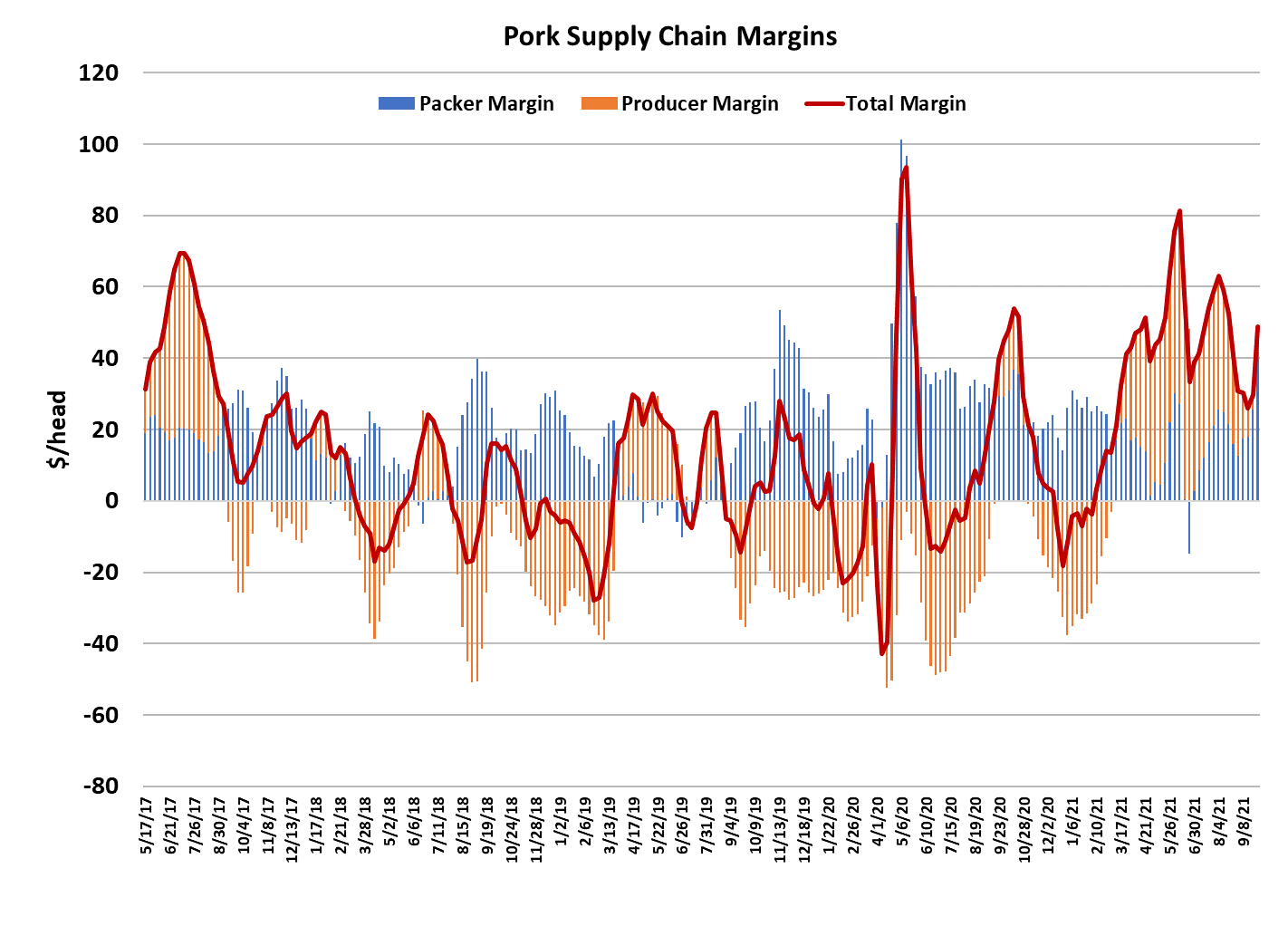

combined margin chart has been suggesting that for a couple of weeks

now, but the move this week really solidified that idea.

The turn higher in demand wasn’t too far off of the normal 8-week cycle

that has been typical in the past, since demand last peaked around

early August. Hams are seeing demand strength from processors

looking to fill needs as the holidays close in and also from Mexican

buyers. My guess is that we could see 2-3 more weeks of stronger

ham pricing before demand for hams starts to abate. Bellies and

hams seem to be closely aligned their price cycles right now, so I’d

also guess that the bellies continue to work higher for another 2-3

weeks also. Bellies probably have more upside potential than the

hams do at this point and everyone knows how fast a rally in belly

prices can lift the cutout. However, just because demand is in an

upcycle it doesn’t necessarily mean that prices are going to soar from

this point forward. Supplies will also have a say. Kills are set to grow

seasonally from now until mid-December and that will be the counterbalance that probably keeps price levels below the peaks seen earlier

this summer.

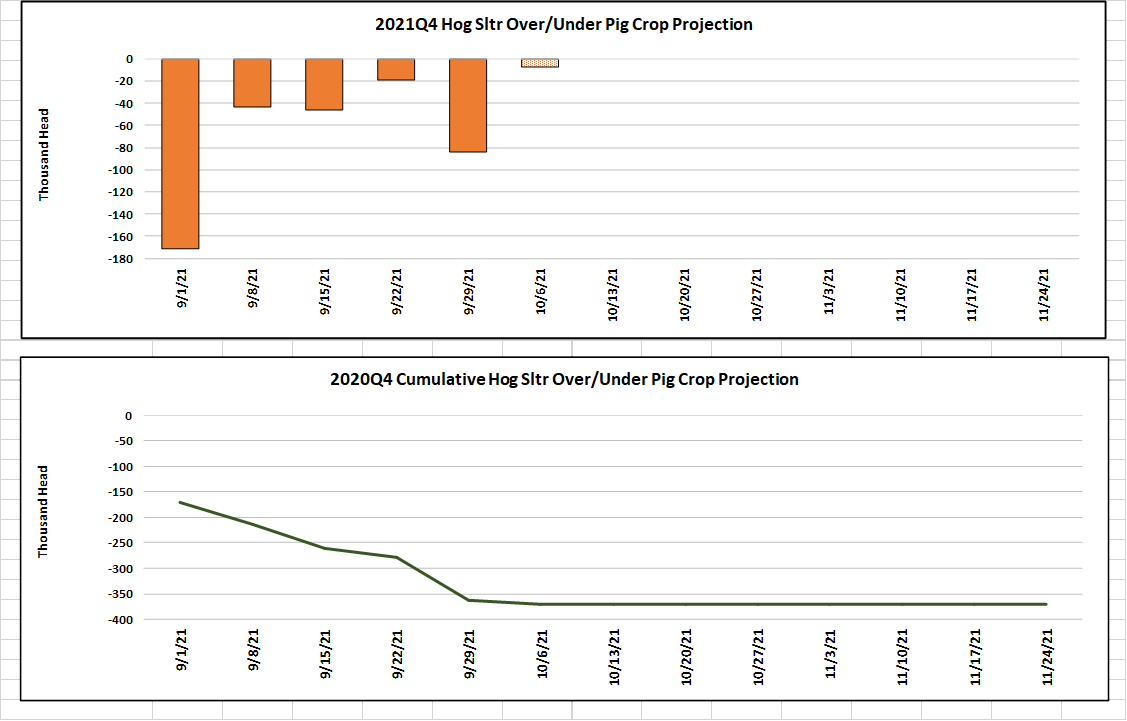

This week’s kill was a bit disappointing at only 2.52 million head, which

was 50k below last week. That means availability will be a little

snugger next week than it was this week when the cutout was able to

put on $7. That makes me think that further price increases could be

just ahead. Once again, we are seeing kills fall well short of what

USDA’s pig crop estimate projected. The kill has been below the pig

crop projection in each of the five weeks so far in the Sep/Nov quarter.

The deficit over those five weeks has been almost 400,000 head. That

is almost a full day’s production. If the under-kill continues at this rate,

the industry will slaughter about a million head less than advertised in

this quarter. Recall that in the most recent summer quarter the kill was

1.3 million head less than advertised. It is pretty concerning that

USDA seems to be routinely over-estimating the hog supply now. The

recent Hogs and Pigs report pegged the Jun/Aug pig crop down 6%.

What if they over-estimated that one by a million head also? That

would imply some very tight pork availability in the upcoming Dec/Feb

quarter. There are concerns about packers having enough labor to kill

all of the hogs this fall, so perhaps a smaller-than-advertised kill would

be a blessing in disguise, particularly for hog producers.

I am a little worried that packers are already struggling to kill the

available hog supply. This week packer margins ballooned out to

over $40/head. That may pull back into the upper $30s early next

week as the LHI comes to fully reflect the gains in the cutout from

this week, but that is still a very wide margin for this time of year.

Packers seem to have no problem pushing negotiated hog prices

lower and that would also be a symptom of packing capacity being

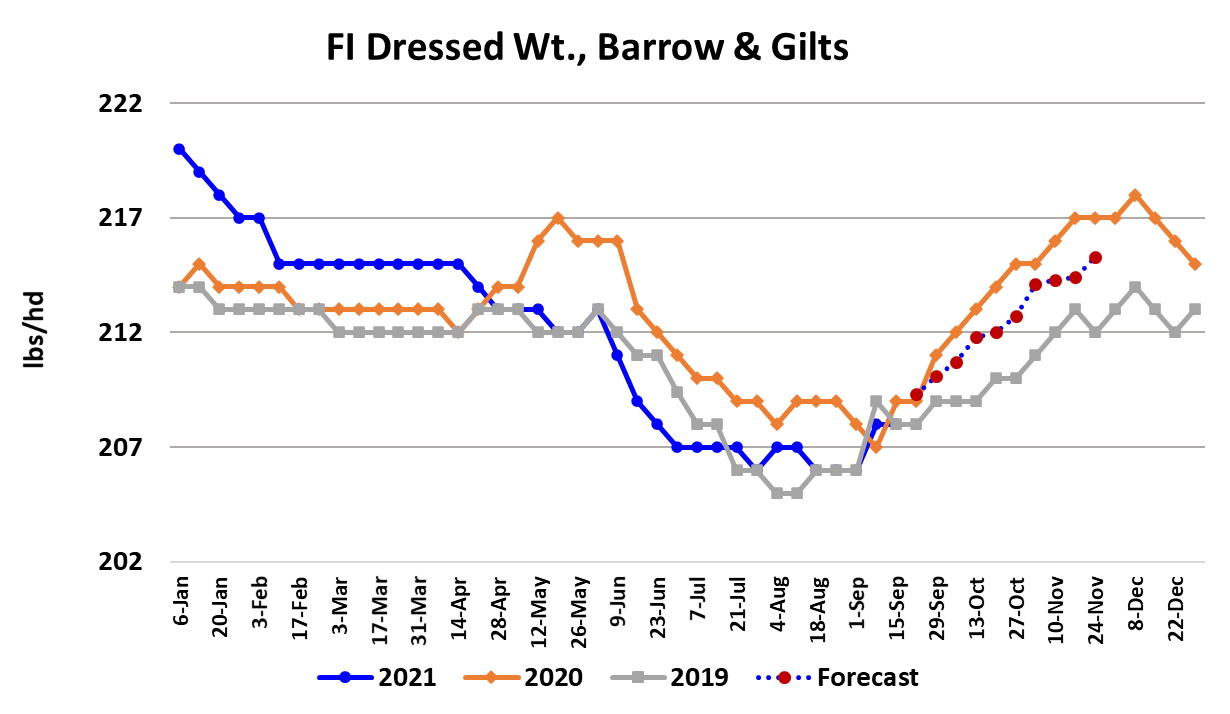

insufficient. It may still be early in the process because we really

haven’t seen any abnormal weight gains recently and that would

definitely be a feature if producers were having trouble getting their

hogs slaughtered on schedule.

Weights are increasing seasonally, but so far the DTDS data

doesn’t indicate a backup. Stay tuned, because that could change

quickly. Since the LHI is dependent both on the cutout and the

negotiated cash hog market, we will have two opposing forces

working to move the index over the next few weeks, with the cutout

trying to pull the LHI higher and the negotiated market pulling it

lower. Right now the cutout is winning the tug-of-war and the LHI is

rising. I estimate it will print close to $95 early next week. Since

Oct only has nine trading days until expiration, that has energized

the bulls and we have seen gains in the Oct contract for six of the

last seven sessions. With next week’s production being

constrained by the smaller Saturday kill this week, I’d expect some

further gains in the cutout and that puts the Oct contract on track to

enter its final week with a LHI above $95. Much will depend on

continued strength in the bellies/hams and there is always the risk

that the bellies shoot higher as they are sometimes prone to do.

Belly volume has been very light on the negotiated pork report, so it

wouldn’t take much to move them in either direction

Exports continue to look like they are softening, but there is always

the chance that the Chinese will step up orders later this month as

they try to get ahead of the logistics logjam in order to get product

delivered in time for their New Year’s holiday and the winter

Olympics, both of which happen in early February. Next week,

watch the bellies and hams for further strength and also watch the

daily kills for signs that the packers are struggling to manage large

kills.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}