Pork Wrap November 5

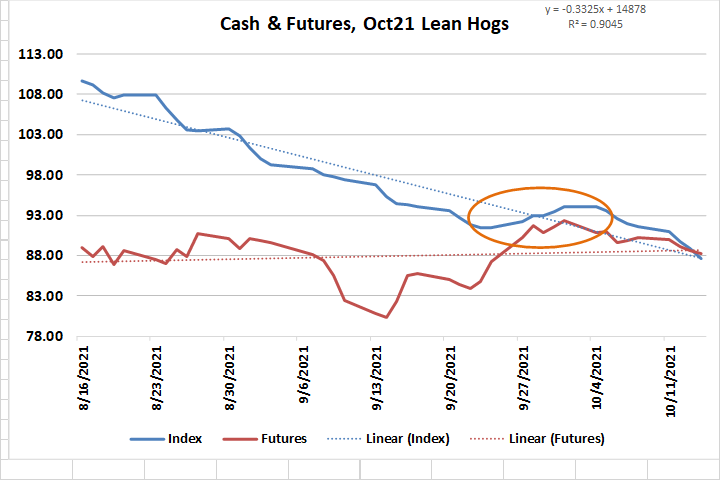

Uh-oh, here we go again. After several weeks of trending lower,

the cutout posted a $1.65 increase this week. We have seen this

behavior before. The chart below shows the LHI and nearby

futures between the Aug and Oct expirations. Here the index was

in a steady downtrend until about Sept 20, when some transitory

gains in the cutout turned the index higher for a couple of weeks.

It eventually resumed its downtrend. Back in September, this

event forced the futures to rally since it had been carrying a

discount to the index. The same thing appears to be happening

now.

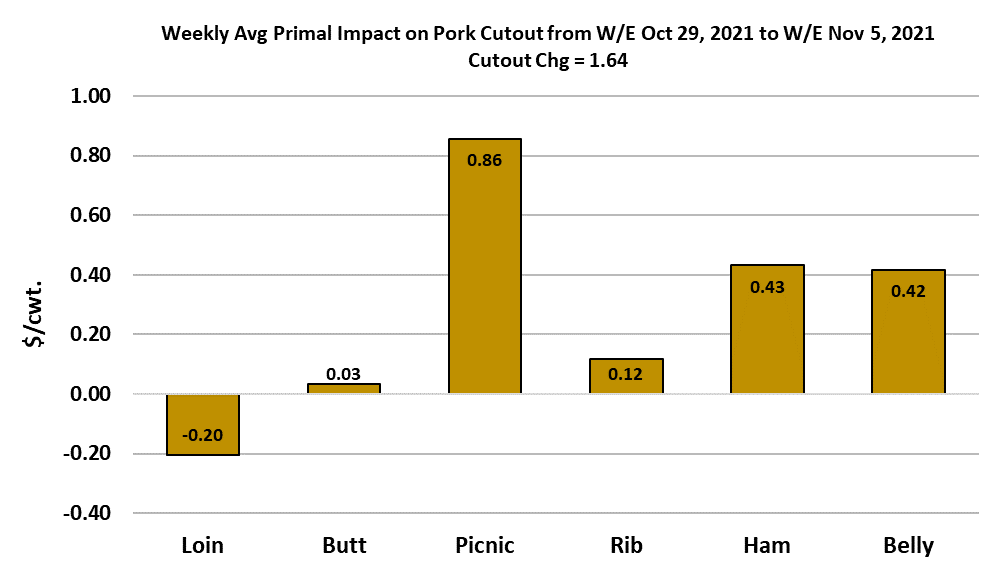

Modest gains in both the bellies and hams this week combined

with a surprise surge in picnic prices to push the cutout back up

into the high $90s. The strength could be associated with last

week’s relatively light kill, but it has certainly changed the

complexion in the futures market. The Dec contract moved lower

today, but is still only $2.40 under the LHI. I’ve had to revise

forecasts higher in response to this development and now have

the cutout forecast holding in the high $90s for three more weeks.

Because the hams and bellies both seem to be in an upcycle at

the same time, I wouldn’t rule out cutouts in the low $100s at some

point. This is all likely to be transitory, just like back in September,

but for the next couple of weeks it could provide a lot of support to

cutout and the nearby futures. The retail cuts seem to be holding

in a sideways pattern, so it will likely come down to the hams and

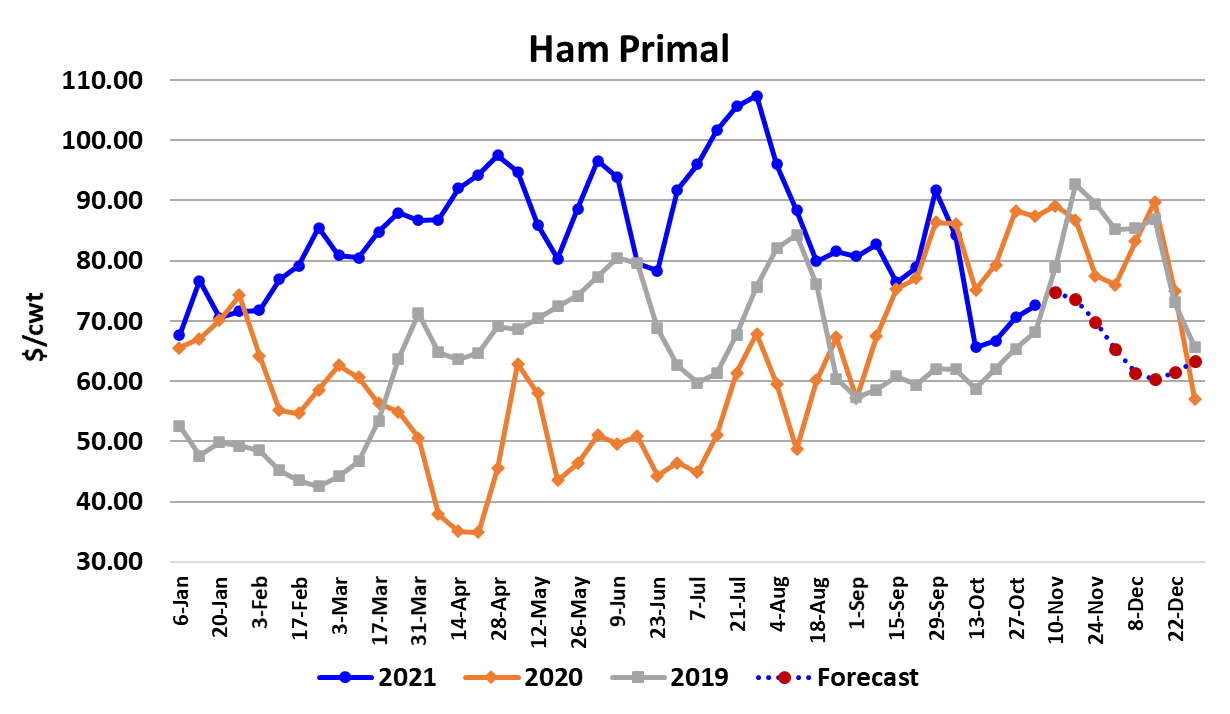

bellies for cutout direction in the near-term. Hams are clearly

strengthening now and this is the third week of increasing ham

prices.

The chart below shows that I’m only expecting another week or

two of stronger ham prices before they turn lower again. There is

some risk to that forecast, however. The hams are recovering

from their lowest price of the year and the primal has spent much

of 2021 in the $80-100 range. My forecast has the primal topping

out around $75 and that may be too low. If the ham primal runs

back above the $80 level then I think that will almost guarantee

that the cutout moves back above $100. Hams have a well

known seasonal tendency to break in mid-December. I’m looking

for them to break in mid-November this year, so I might be too

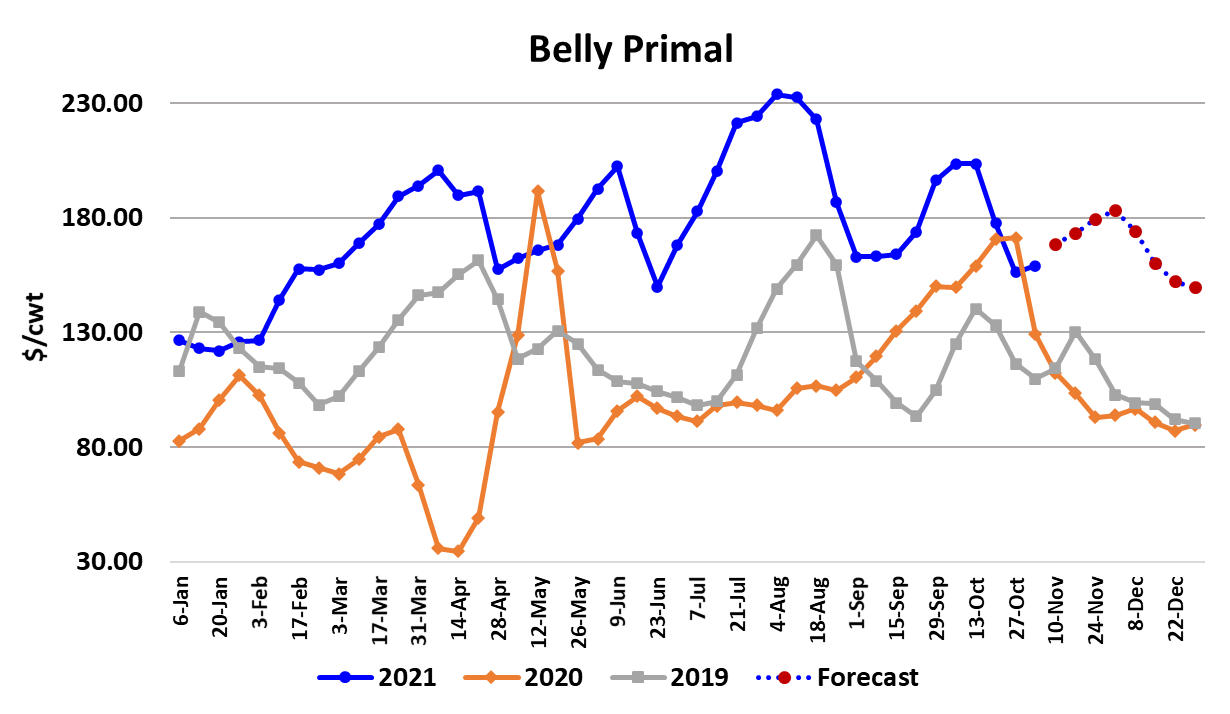

early on that. The bellies, on the other hand, have just begun to

move higher, so they could be a bigger source of support for the

cutout over the next few weeks. I’m projecting the belly primal to

top just over $180 in early December.

That would be the 5th belly primal top this year. The other tops

have been above $200, so I might be a little too conservative on

this one, but it is my sense that bellies don’t typically outperform

in the latter weeks of the year. Of course the factor that will

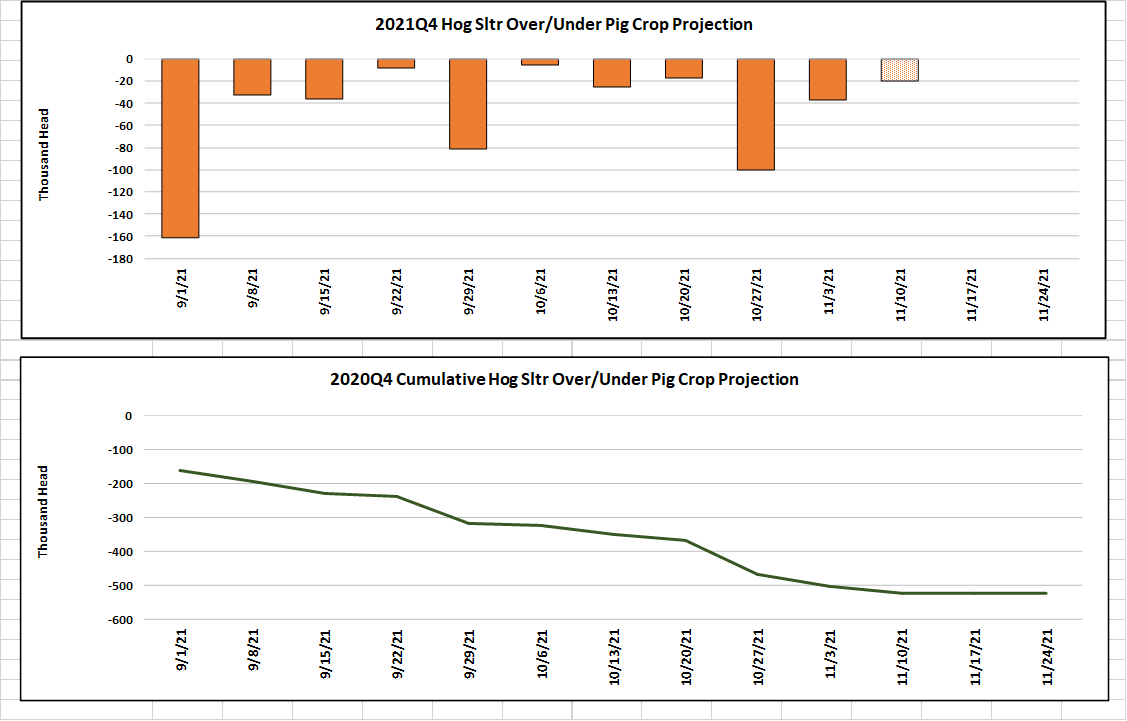

work against these two important upcycles is the fact that kills

are near the largest of the year. This week’s total was 2.61

million head, with a larger Saturday than last week. Even so,

the kill was below what the pig crop projected once again.

With 3 weeks to go in the Sep/Nov quarter, slaughter has

underperformed the pig crop by about 500,000 head. I’m

projecting next week’s kill at 2.65 million head and that may be

the fall top.

When December arrives the industry will start working on the

Jun/Aug pig crop, which was reported down 6%. So we are

getting pretty close to the point in the calendar where pork

production will turn lower and of course there are 3 major

holiday disruptions between now and the end of the year that

will also restrict production. Negotiated hog markets finished

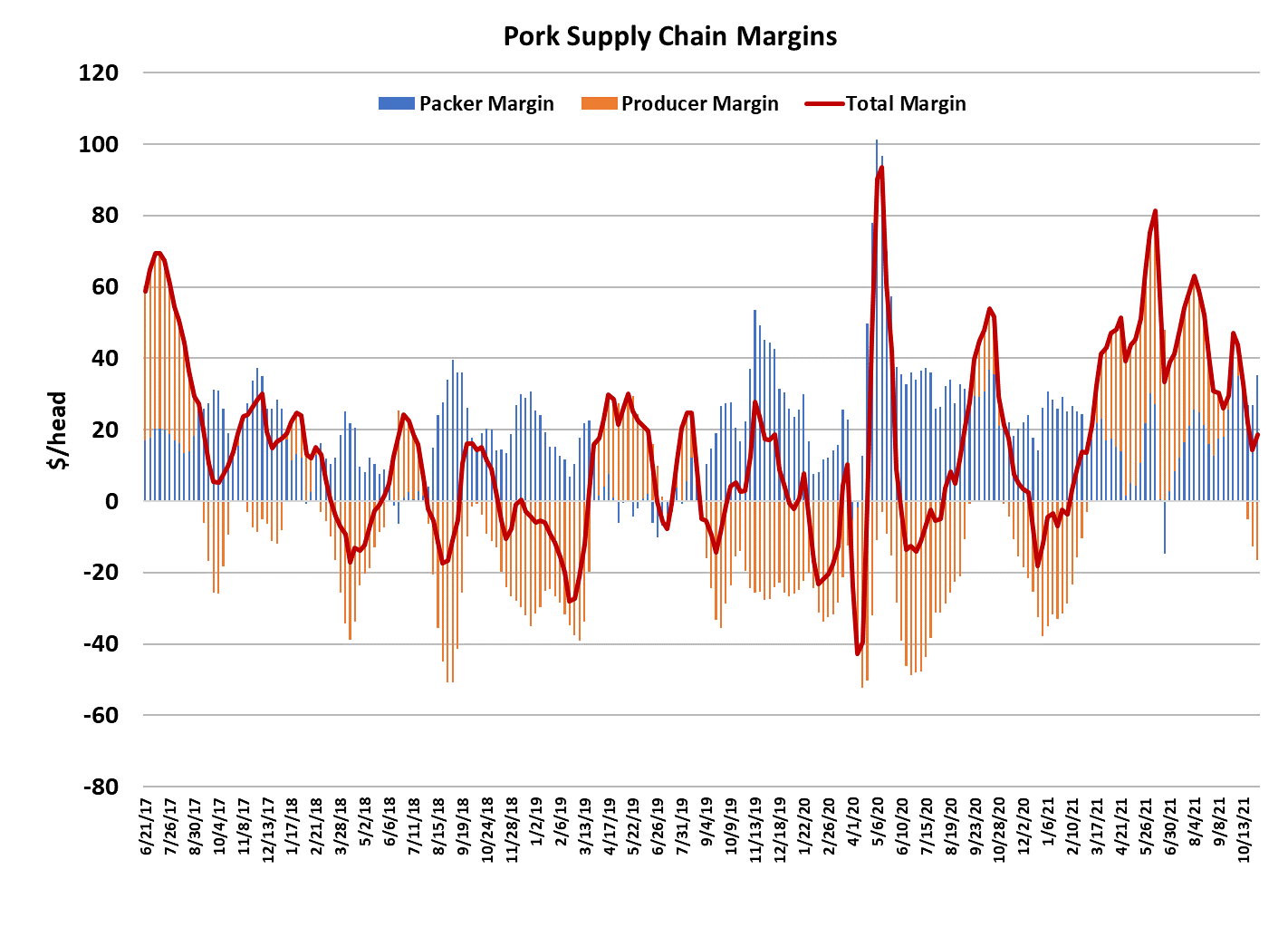

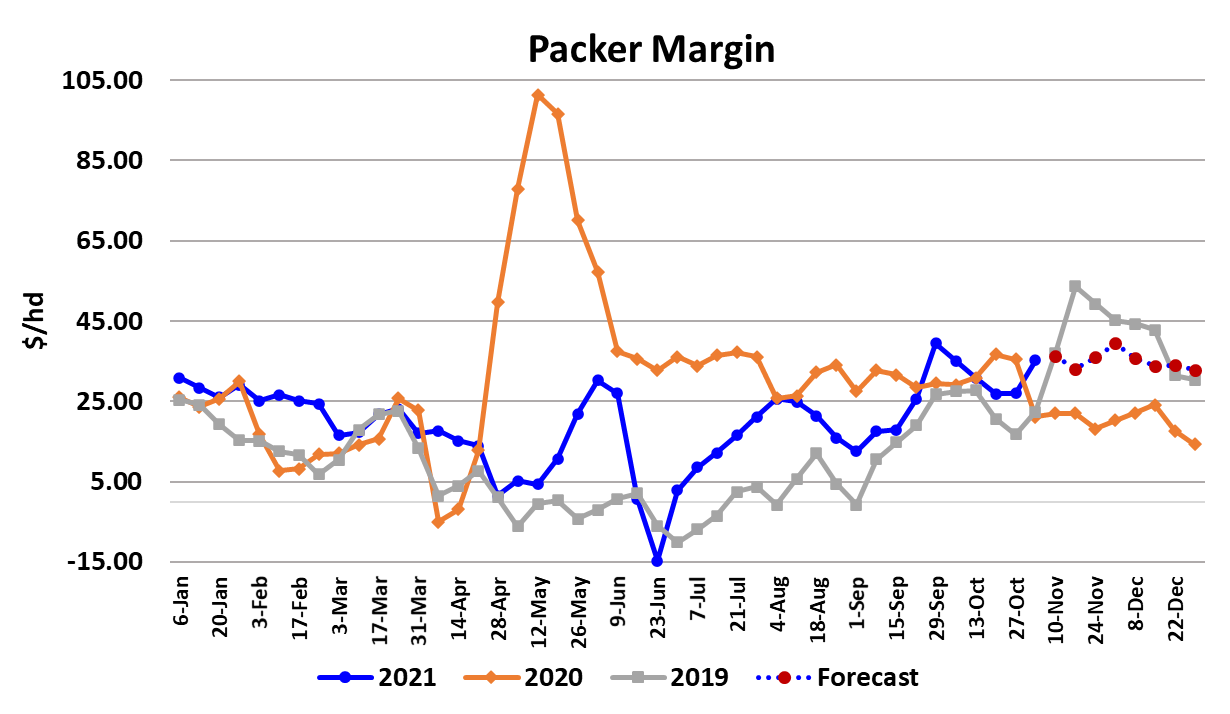

the week about $2 lower than where they closed last Friday.

Packer margins swelled about $9 to $35 this week. So far,

negotiated hog prices and packer margins don’t suggest that

labor problems are limiting the kill. Outside of the short-term

strength projected in the bellies and hams, I do think that

overall pork demand is going to be leaking lower as we close

out the year although it might not show up in prices strongly

because of supply tapering during December.

I’d expect the demand softening to become more obvious after

the holidays, but even then it could be masked somewhat by

that 6% smaller pig crop that the industry will be slaughtering.

USDA released official export numbers for September today

and they pegged total pork exports down 6.4% from last year.

The YOY comparisons will likely only get worse in the final

three months of the year because China has a much smaller

appetite for US pork than it did at this time last year. Next

week, watch for the cutout to flirt with the $100 mark again if the

hams and bellies can maintain their upward trajectory.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}