Pork Wrap November 4

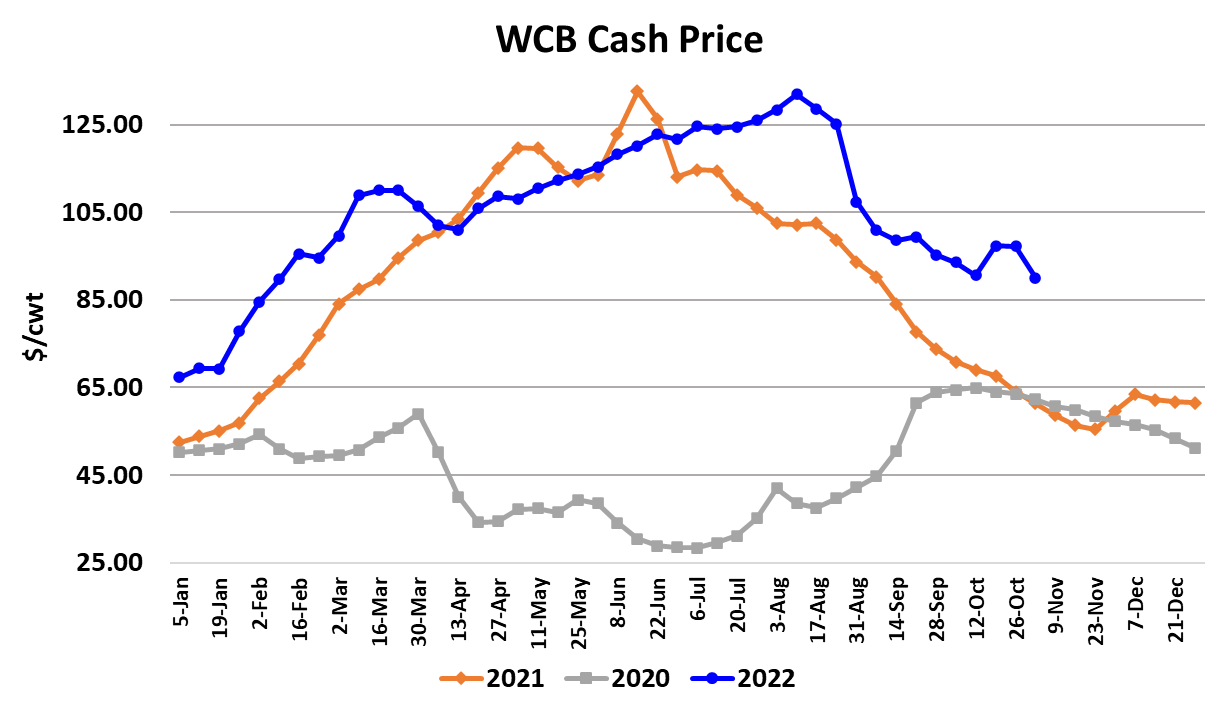

The biggest feature in the hog and pork complex this week was a

significant softening in the negotiated hog market. The Western

Corn Belt market averaged right at $90/cwt this week, down over

$7 from the week before. The NDD market was down $5.66/cwt.

But before we declare the cash hog market dead, it is important to

recognize that we have seen weeks before where the negotiated

hog market softened one week and then bounced back the

following week. It will be important to watch for some rebound

next week. If it posts another big drop, then I’d say the party is

over for now. The negotiated market wasn’t all that struggled this

week—the cutout was also softer, losing $2.30/cwt. to average

$97.29. The losses in negotiated hogs and the cutout have yet to

be fully reflected in the LHI, which was down only $1.50 this

week, but is likely to see bigger losses next week unless

something changes dramatically.

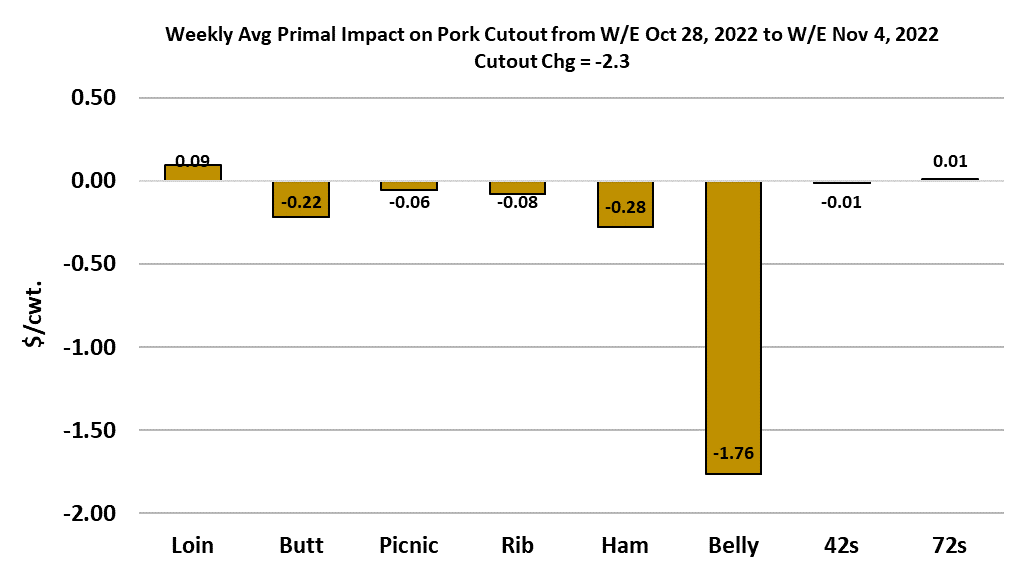

The attached chart shows that the weakness in the cutout this

week was almost exclusively related to the belly primal, which lost

almost $11/cwt and averaged $129.21. Compared to that, the

contributions of the other primals to the cutout’s loss were

minimal. I wasn’t surprised that the bellies turned lower, but the

magnitude of the one-week drop was surprising. Bellies are now

clearly in a downcycle that will probably last at least 2-3 more

weeks and very well could contain the lowest belly prices of 2022.

Bacon slicers will likely be busy scooping up some of those cheap

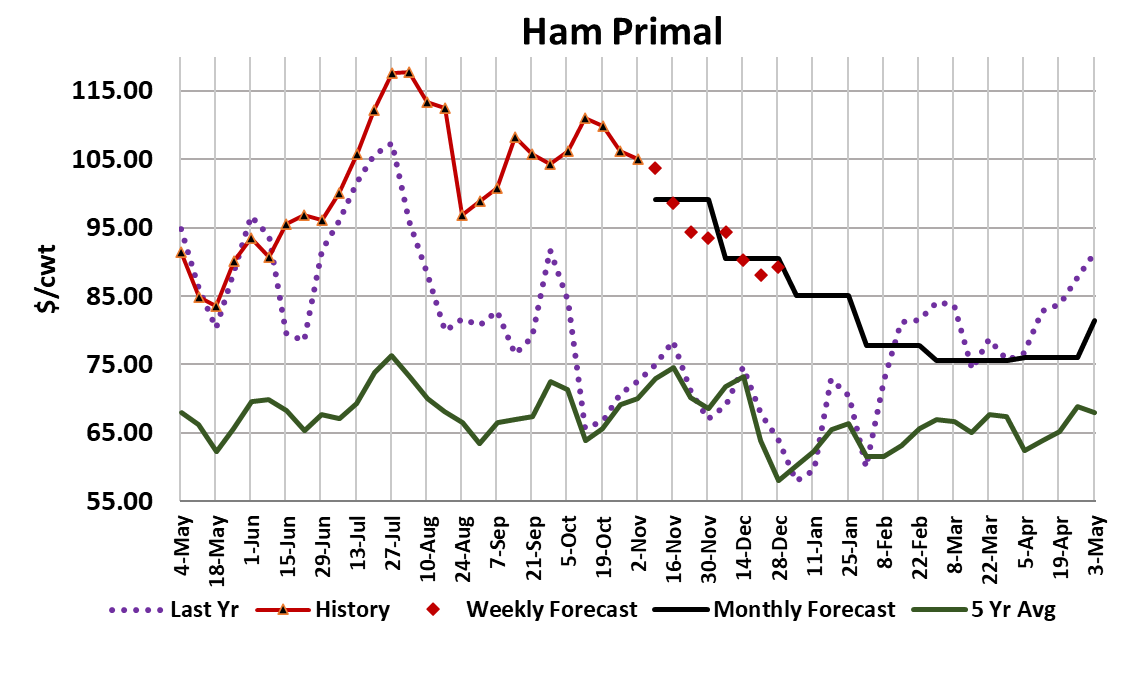

bellies to add to freezer stocks for use next spring. Hams were

down just a tad this week, but probably face further losses in the

next few weeks as the processing window for Christmas hams

closes. No ham processor in his right mind is putting hams away

at today’s price levels. Instead, they will wait for the last two

weeks of December, which is when the lowest ham prices of the

year typically occur.

The attached chart indicates that I am forecasting a relatively

steep decline in ham prices over the next few weeks. I think the

risk is that hams hold up better than I expect and provide more

support to the cutout than I anticipate. The loin primal was a little

higher this week after a long string of declines. My feeling is that

the loin primal is near a bottom and will get decent support once

Thanksgiving is behind us. Still, with both the hams and bellies

forecast lower over the next few weeks, it is nearly impossible to

see how the cutout could post a gain. I think it continues to ease

over the next few weeks and then makes a bottom in the low $90s

in early December. By the time the pork cutout futures expire in

the middle of December, the cutout could be back into the $93-95

range. Pork demand seems pretty stable right now.

We are seeing some normal seasonal price weakness, but a lot of that is

probably due to seasonally large supplies. There is a risk that demand

eases some as pork fatigue sets in. Ham clearance for Thanksgiving will

be important to watch. With turkey prices elevated, retailers are expected

to lean a little more on hams for holiday advertisements this year. With

all that said, I’ve got a fairly soft demand structure dialed in for Q4, and it

makes me think that the odds favor demand being a bit better than what

I’m currently forecasting. That would mean price a bit higher than the

what the current forecast implies. This week’s slaughter was reported to

be 2.58 million head and that was actually a good bit smaller than what I

thought at the beginning of the week. Both Friday and Saturday showed

smaller kills than expected. This was a “big Saturday” week, with the

Saturday kill estimated at 164k. Next Saturday is likely to be smaller,

maybe even less than 100k.

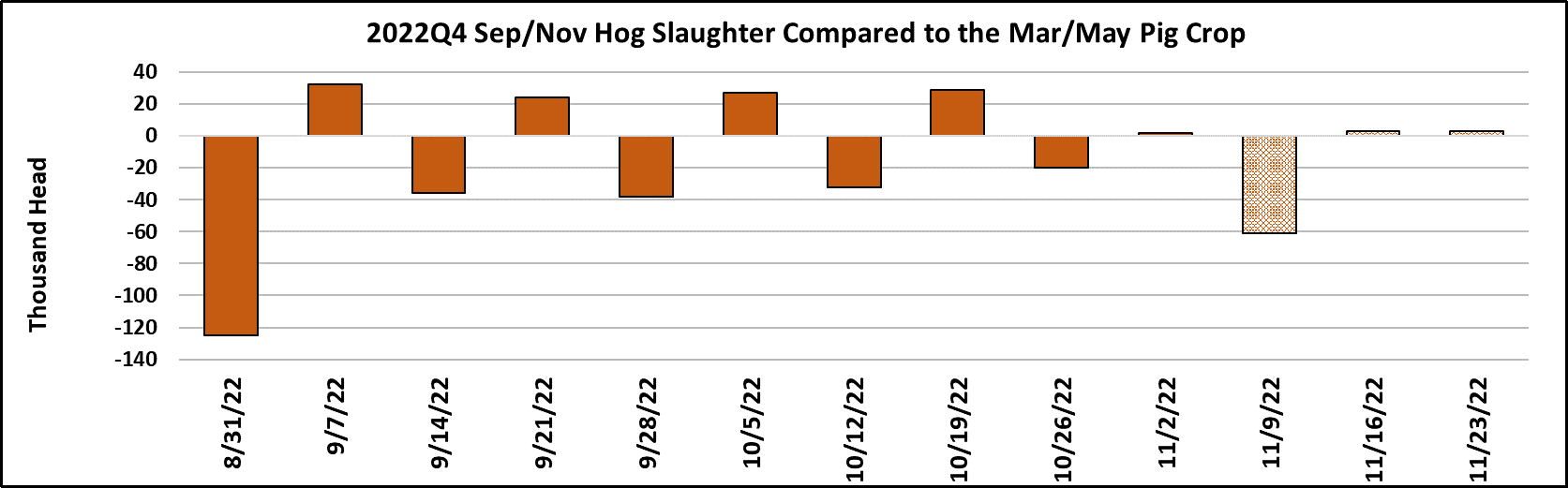

We have yet to hit the 2.61 million head level that I calculate as the

practical top based on USDA’s Mar/May pig crop estimate. This week’s

slaughter was almost dead-on with what the pig crop implied, but next

week is likely to fall short. So, as we near the end of the Sep/Nov

quarter, it looks to me like the industry is going to under-kill the pig crop

by about 200,000 head. That is rather small in terms of past errors in the

pig crop estimate. Hog weights continue to run lighter than expected.

Barrow and gilt carcass weights have been stuck at 212 pounds for the

last three weeks and may repeat that again next week. Seasonally,

weights should be increasing, but they haven’t done much of that lately.

That means that hog producers are probably still pretty current on their

marketings and increases the risk that the negotiated market will rebound

at some point in the near future. Lean hog futures appear to be pretty

closely aligned with my fundamental forecast through July of next year

and then are over-priced by about $8/cwt. from August through the end of

2023.

Of course, that is a long way off and those forecasts are based on pig

crops that haven’t happened yet, so there could be some substantial

adjustments to those deferred forecasts as we get into 2023. ERS

provided its trade data for September today and it showed total pork

exports almost even with last year. Canada and Mexico’s numbers were

softer than last year, but that was made up by gains in many of the other

traditional destinations such as Japan and S. Korea. China only saw a

slight YOY increase in exports. Pork imports were down 7% YOY in

September. Next week, the focus is going to be on the negotiated hog

markets and the belly primal. Both were substantially lower this week

and the two combined for most of the decline in the LHI. Whether or not

that repeats again next week will have a big bearing on how rapidly the

LHI declines and how aggressively traders will be inclined to sell the Dec

futures.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}