Pork Wrap November 26

The hog and pork complex has remained on a downward trajectory in

recent days. The pork cutout has lost almost $10 over the past seven

trading days and the NDD cash hog market is down $2.60 over the

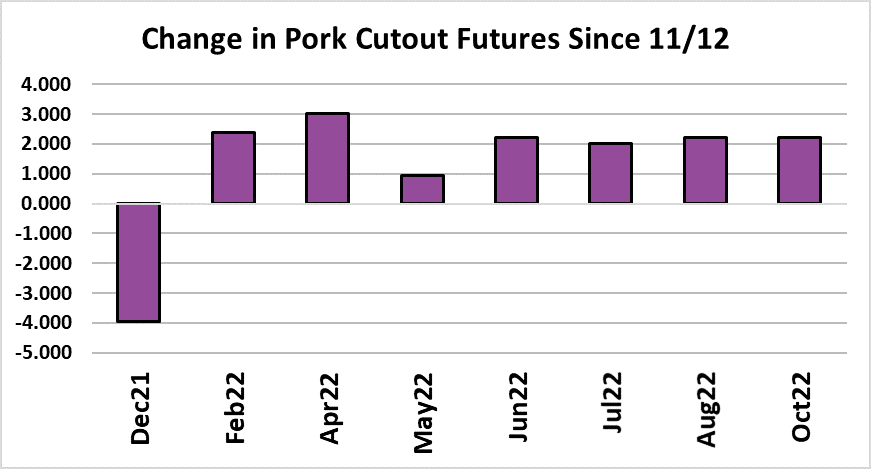

same period. Futures traders have remained optimistic that a

turnaround is coming as the nearby Dec LH contract dropped less than

$2 and the pork cutout futures were down only $4 over the period.

Packer margins are shrinking as the losses in the cutout outpace the

decline in cash hogs. Packer margins averaged about $26/head last

week and will likely remain close to that this week. Those margins will

be about $10 per head less than where they were in early October,

when kills were smaller than they are today.

That suggests some modest tightening in the hog supply has occurred,

but pork buyers care very little about that. Instead, buyers are reacting

to softer demand from their customers and that is helping push pork

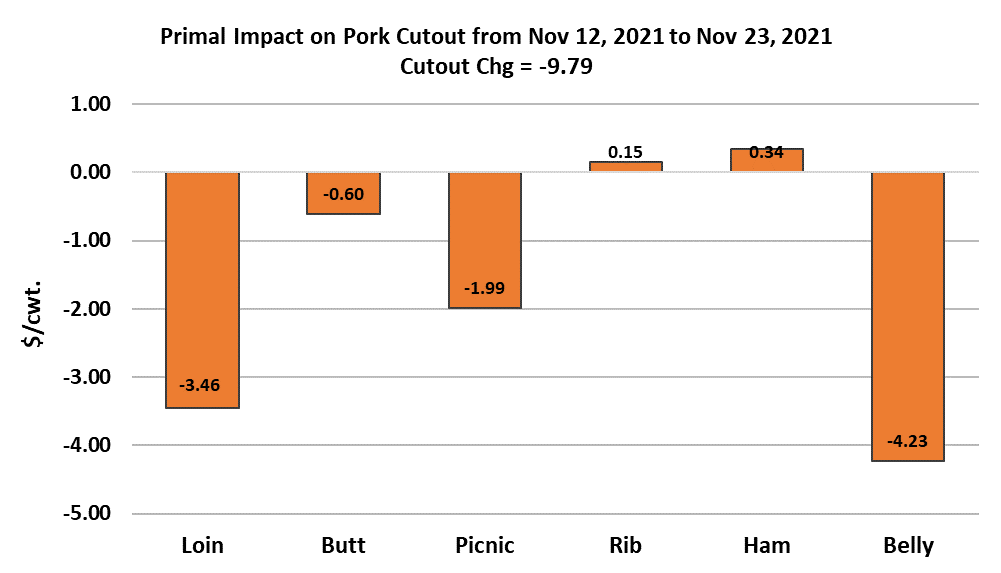

prices lower as we approach Thanksgiving. The softness in the cutout

over the past week and a half has been driven by softer belly, loin and

picnic pricing. Hams have held steady, but are beginning to look like

they might also soften in the days ahead. Without Chinese buyers

scooping up US pork with both hands like they have done in the past

two Novembers, price levels have sagged. It is clearly more of a

demand-side problem than anything on the supply side because kills

are running well below last year’s level. Last week’s kill clocked in at

2.63 million head and that may very well be the largest kill weekly kill of

Q4. My estimate for this week’s kill is right at 2.28 million head.

Packers are planning on a huge Saturday kill to help offset some of

what will be lost on Thursday. The smaller kill could support pork prices

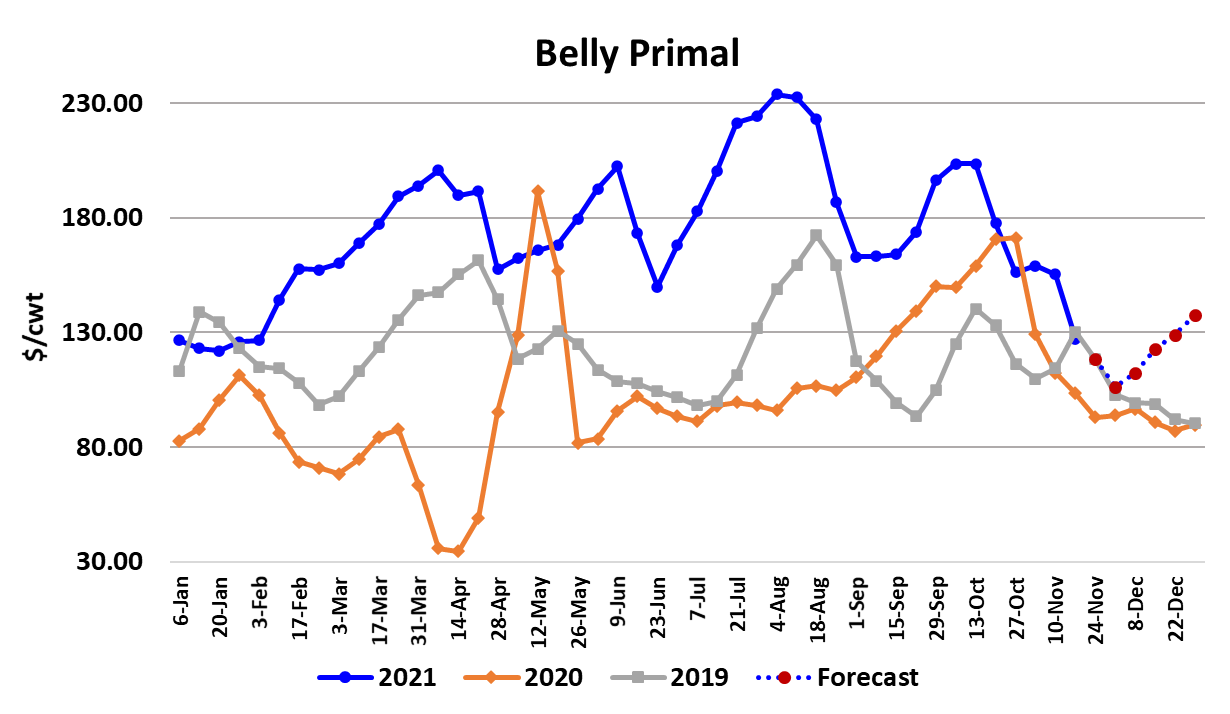

next week, but it is not a sure thing. For one, bellies need to gain some

traction in order for the cutout to reverse its current downtrend, but this

is the time of year when belly demand for processing is generally light.

In the old days, November was prime time for users to move bellies into

the freezer as a hedge against high prices next spring.

In the last few years, there has been less of that “storage buying” in the

fall. As a result, I think there is a good chance that the belly primal

continues lower for another couple of weeks and may test the $100

level before it starts to move higher. At the same time it also looks like

the hams have topped and are starting to work slowly lower. One

reason is that boneless ham premiums to the bone-in have declined

recently, but the bigger effect is likely a softening of demand for

processing now that December is right around the corner. I find it hard

to forecast the cutout higher with bellies steady-weak and hams

softening in the next couple of weeks. Trim has also declined a lot

lately and there is little reason to call that higher in the near-term. I

think the retail items can hold close to current levels though and that

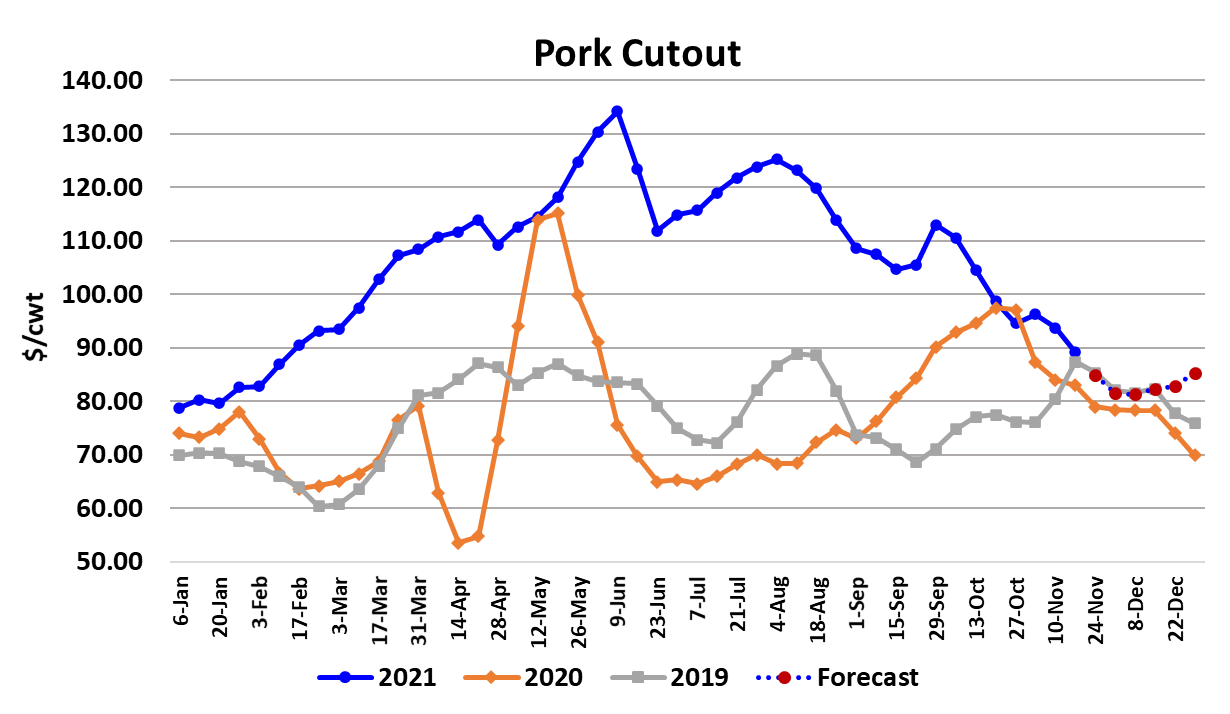

means that the downside risk in the cutout might be limited to the $80

mark—only about $5 below where it printed this afternoon.

I don’t rule out a brief trip back up to $90 next week as the short kill

works through the system, but in general my forecast is for the cutout

to remain in the low to mid-$80s until Christmas. The risk to that

forecast probably lies to the downside. The cash hog market is a

little more difficult for me to read at the moment. It does appear to be

stabilizing in the mid $50s, but we’ve seen that happen before only to

be followed by further downward movement. Packers are probably

not too happy with their margins at present and would like to them

closer to $40/head as they have been in the past near the end of the

year. They may not explicitly cut the kill, but they probably will take

advantage of the time around holidays to give their workforce a much

needed break and thus help prevent snugger hog supplies from

impacting margins too much in the weeks ahead.

Everyone is aware that USDA called the summer pig crop down 6%

YOY and that pig crop will start coming to slaughter next week. Over

the past four weeks swine kills have averaged 3.2% below last year,

so clearly we are not to the point where hog supplies are down 6%

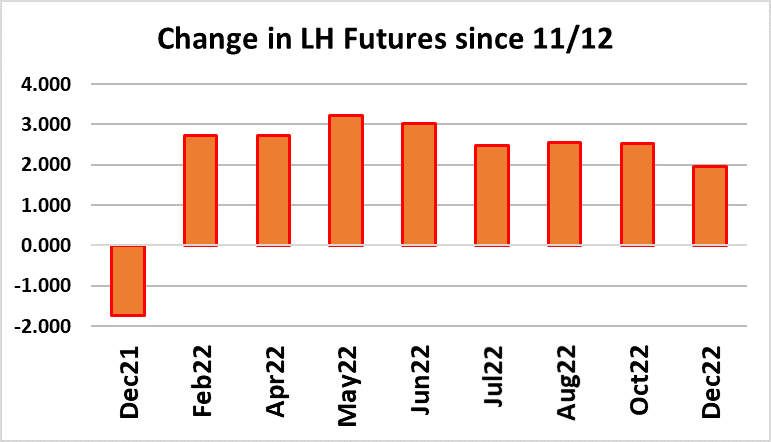

yet. But it seems as though futures traders are expecting that shoe

to drop soon. They have been reluctant to press the Dec contract

below $74 and have priced in nearly a $10 increase between Dec

and Feb expirations. Someone is betting on this market turning

higher soon. Time will tell, but I tend to go with what the immediate

data is telling me and that suggests that there are sufficient hogs

available to prevent a quick run-up in the cash market. Besides, the

demand side of the pork market seems to be slowly softening and

thus we could get a moderate tightening in hog supplies without

much in the way of pork price increases. The combined margin chart

below clearly points to a demand downcycle in progress and it is

interesting that the combined margin is now approaching zero, which

is a level it hasn’t come close to in almost a year. Last year at this

time the combined margin was in a similar position and it continued

lower, bottoming around -$18 near Christmas.

Is something similar in store this year? If it is, that suggests that the

cutout will move below $80 and could test $75. That is more

pessimistic than my current forecast, but I don’t rule it out. Without

China picking up as much of the slack this year, any loss of domestic

demand will have a bigger impact on the cutout than it did last

holiday season. This week’s kill won’t tell us much due to the

holiday, but watch the following week’s slaughter closely. If it falls

back close to 2.55 million head, then that is consistent with a 6%

smaller Jun/Aug pig crop and maybe USDA’s survey is correct.

However, if it remains in the 2.6-2.65 million head range, then

possibility that the pig crop is larger than the survey indicated must

be considered.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}