Pork Wrap November 25

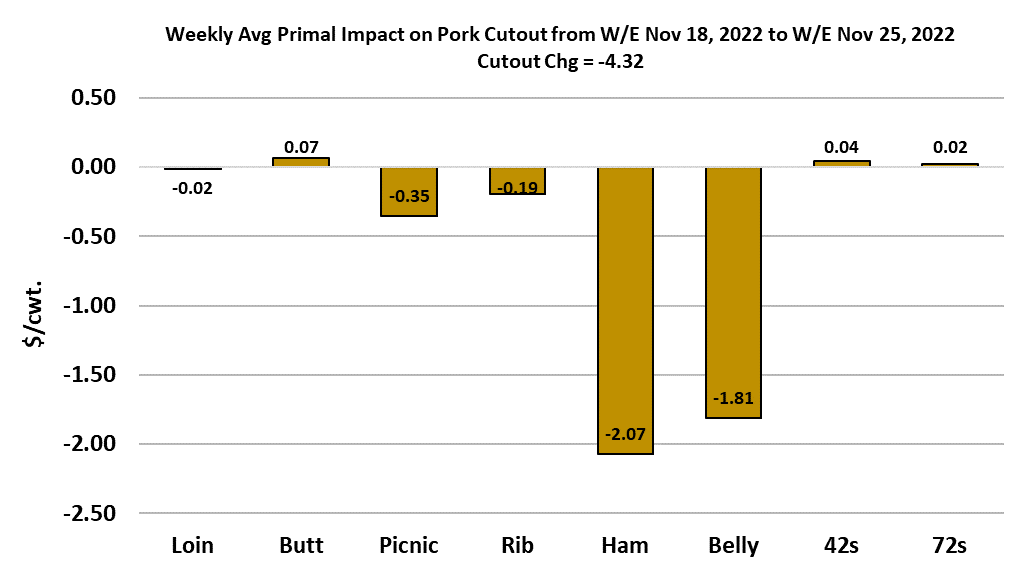

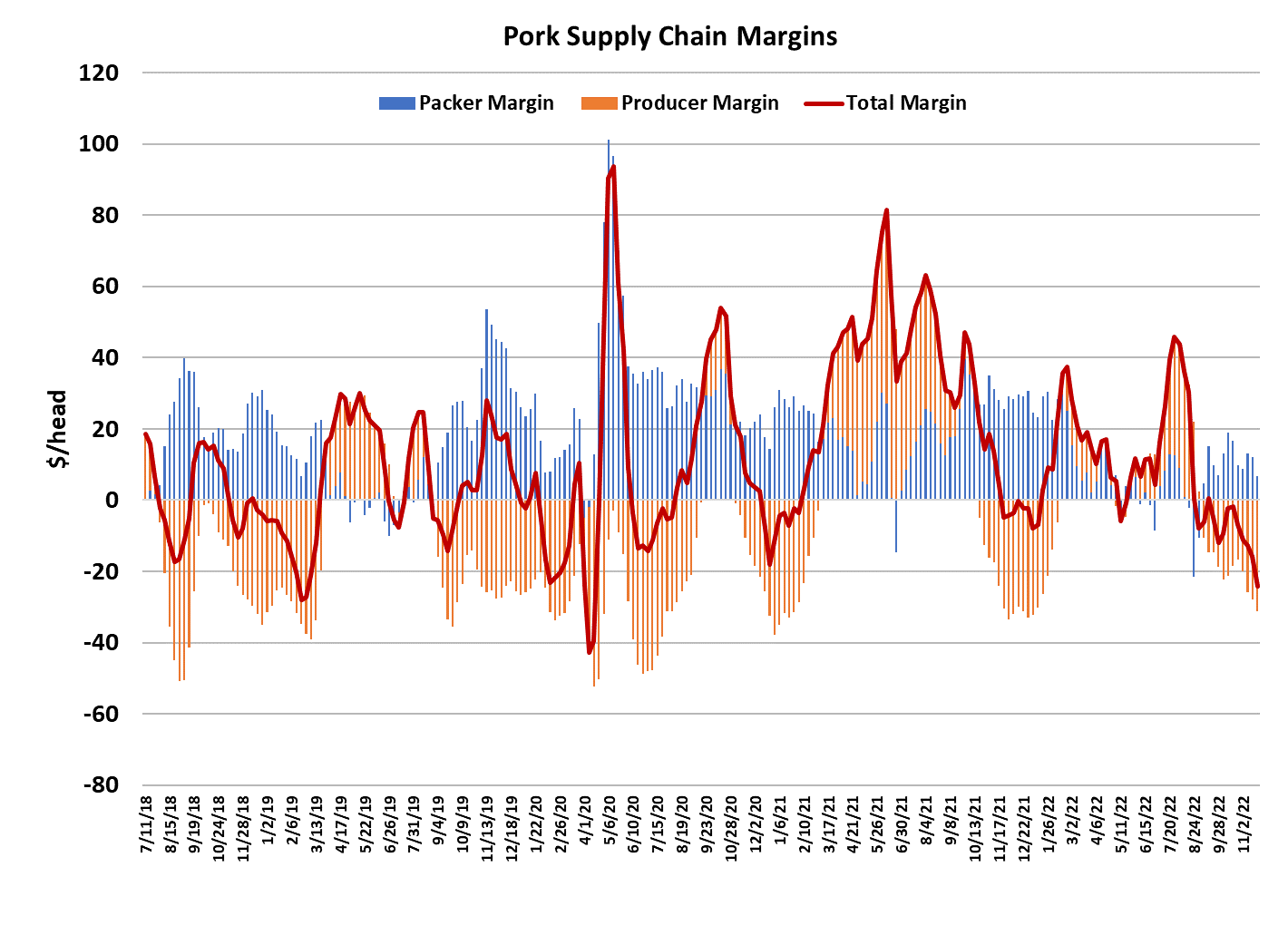

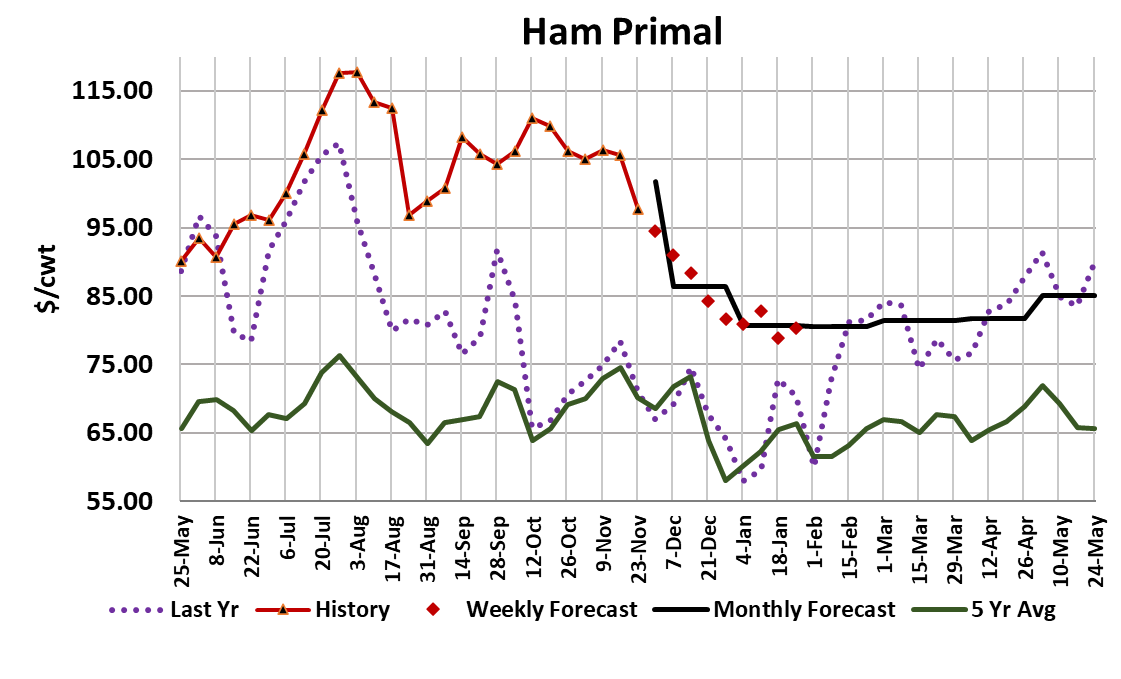

This week, the pork cutout finally gave up some major ground, dropping $4.32 on a weekly average basis to finish just a hair over $90/cwt. This drop was all about weakness in the processing items. The ham primal lost nearly $8/cwt. and the belly primal lost almost $11/cwt. To be fair, the market was asked to digest last week’s large production in a holiday week where many buyers weren’t at their desks. The fact that it was the processing items that suffered the most probably is at least partly due to a slowdown in processing plants around the holidays when more workers are seeking time off. That said, the demand side of the pork market is not looking very good at all. Just take a look at the combined margin chart. This may qualify as a demand air pocket. I haven’t had to call one of those in quite a while. Futures traders have yet to believe it though.

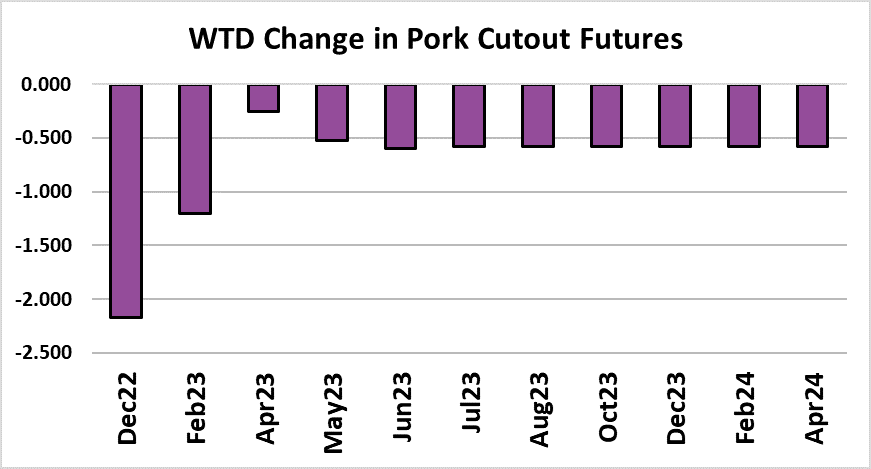

The Dec contract settled today just under $84/cwt and my calculation indicates that the LHI will be at $84 by Tuesday. That just doesn’t seem to be showing enough respect for an Index that is coming down in big chunks now. I guess that traders are expecting the market to turn higher in the remaining 13 trading sessions before the Dec expires, but that is a very big gamble because if the Index continues on its current trajectory, it could be well under $80/cwt by expiration day. Some will write off this week’s action as not representative of the true market because of the holiday week. That is possible, but again, a big gamble. The combination of bellies and hams moving lower at the same time is a powerful one. The normal seasonal pattern in the cutout at this time of year is for it to go sideways from late November until Dec expiration and then move substantially lower into year’s end. Often, the lowest cutout of the year will print in the week between Christmas and New Years. So, while the combined margin looks like it should be getting close to a bottom, I wouldn’t want to bet on a strong recovery during December.

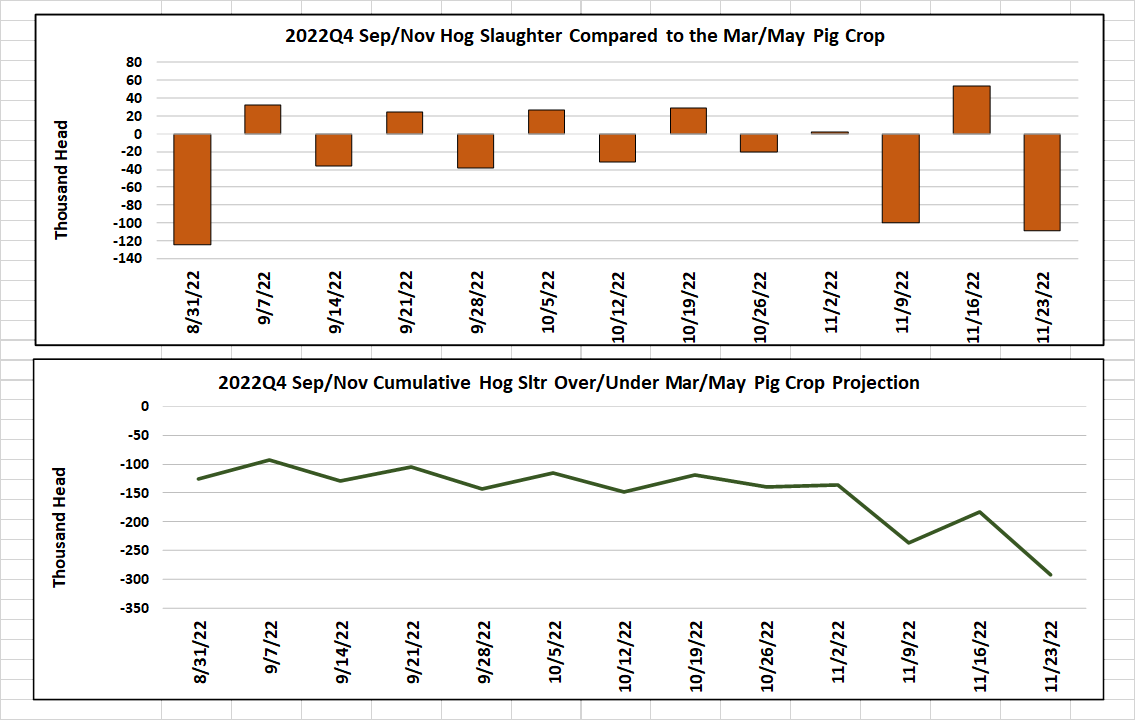

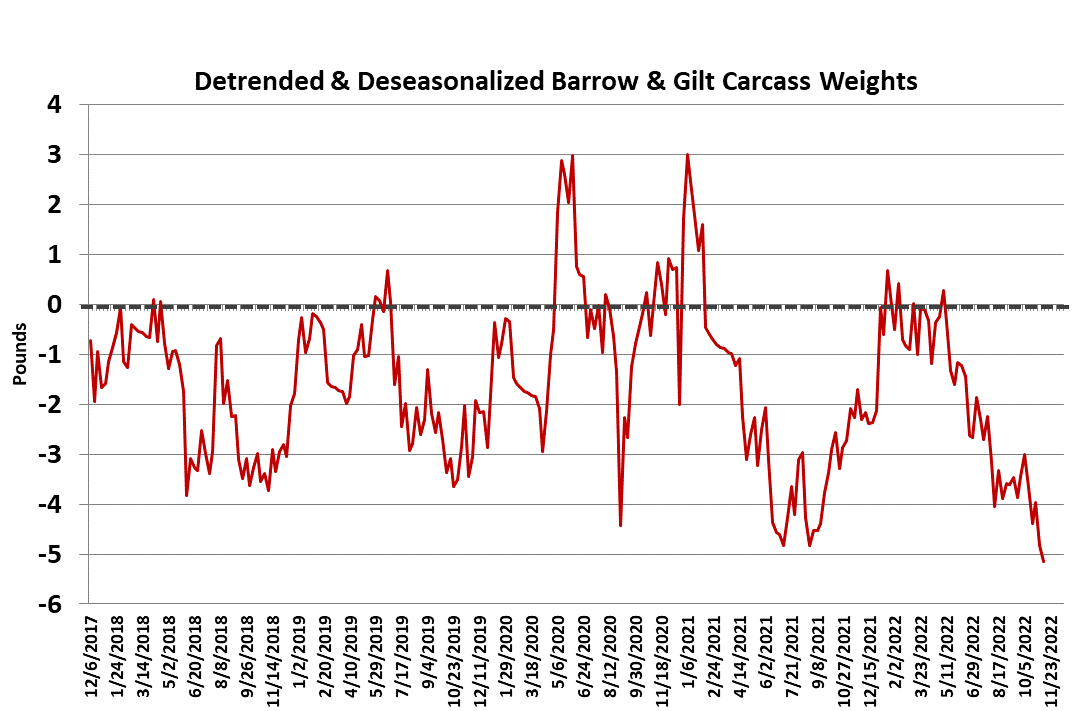

Interestingly, all of this is happening against the backdrop of relatively firm hog pricing. The NDD negotiated market was down only $0.40/cwt. this week and the WCB was actually a little higher. This is creating a big headache for packers and I calculate that this week’s margin is a little less that $7/head. Who would have guessed that packer margins in late November would be in the single digits? This situation is very similar to what is going on in beef where the cutout is struggling yet animal prices are firm. The solution to the problem is to cut the kill, but just like beef packers, the pork packers have been reluctant to do that. This week’s holiday-reduced kill registered 2.22 million head and packers needed a huge Saturday kill to get to that level. Next week, the kill is expected to bounce right back to 2.59 million head. It should stay close to that level until Christmas week and then we could see it drop down to 2.0 million head until after New Years. The data really makes it look like hog producers are current on their marketings right now and that probably explains why packers haven’t been able to crater the negotiated hog market like they normally do at this time of year. Barrow and gilt carcass weights were reported steady at 213 pounds this week. The normal seasonal would have weights climbing higher at this time of year and since that isn’t happening, the DTDS weights are very depressed and are now at their lowest level in over five years. We have now finished the Sep/Nov quarter and it looks like slaughter is coming up about 275k short of what the March/May pig crop projected. Not a huge miss, but it may mean that the Dec/Feb slaughter will come up short of the Jun/Aug pig crop also.

Another thing to note is that sow slaughter during the most recent quarter has been about 30k above normal given the size of the sow herd on Sep 1. That makes me think that producers are still liquidating and that the breeding herd will be lower again when we get the next Hogs & Pigs report on Dec 23. That likely means that smaller-than-normal packer margins will persist into 2023, simply because the hog herd is too small relative to the amount of packing capacity. That will be the most price supportive during the summer months when hog numbers become the tightest. Next week, watch for further weakness in the processing items, particularly hams. I’m not too worried about further erosion in belly prices, but hams still have a lot of air under them and could drop further. Also, look for futures traders to reluctantly give Dec more respect to the downside as the runway to expiration shortens.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}