Pork Wrap November 24

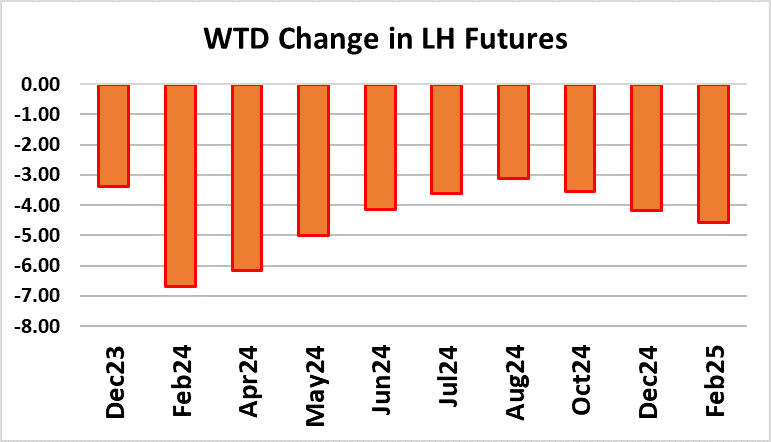

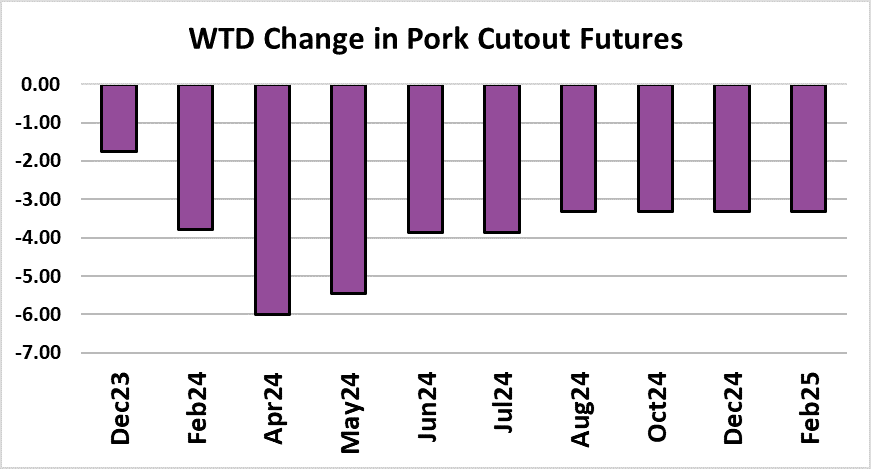

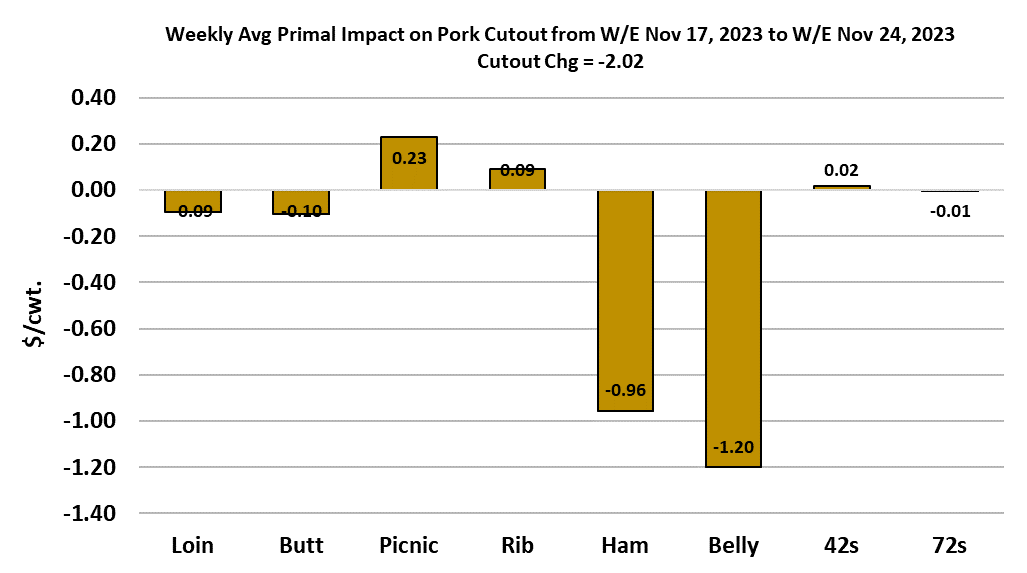

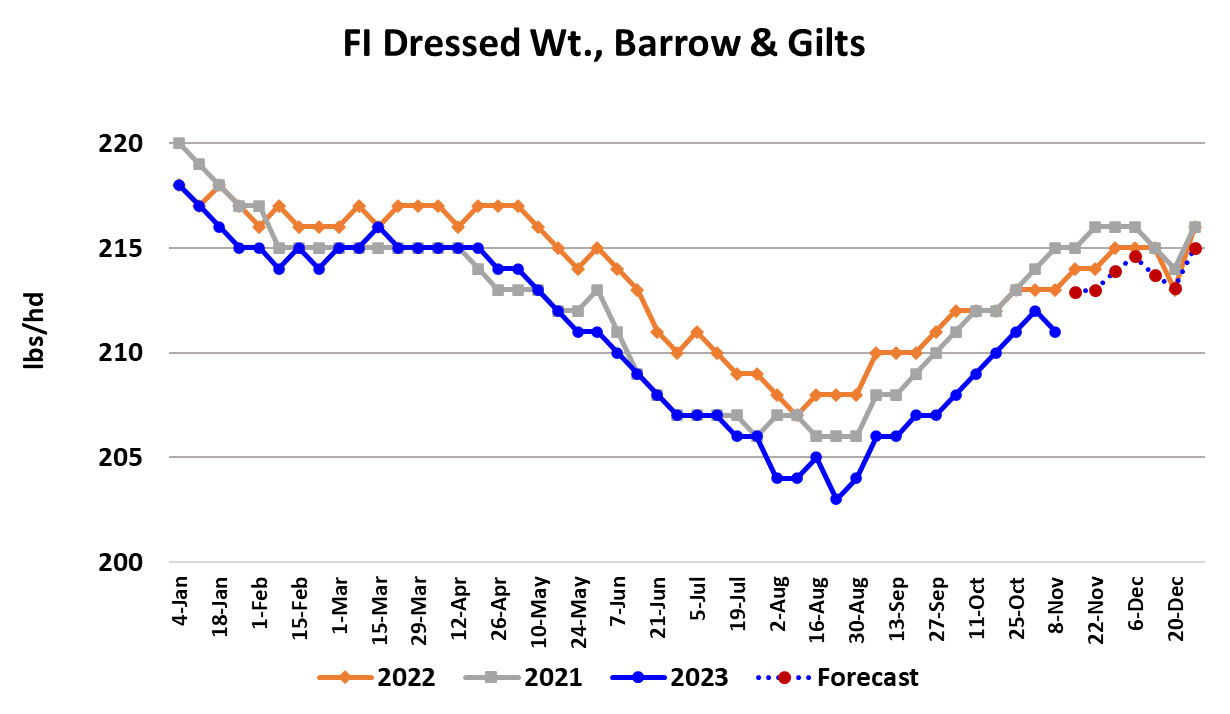

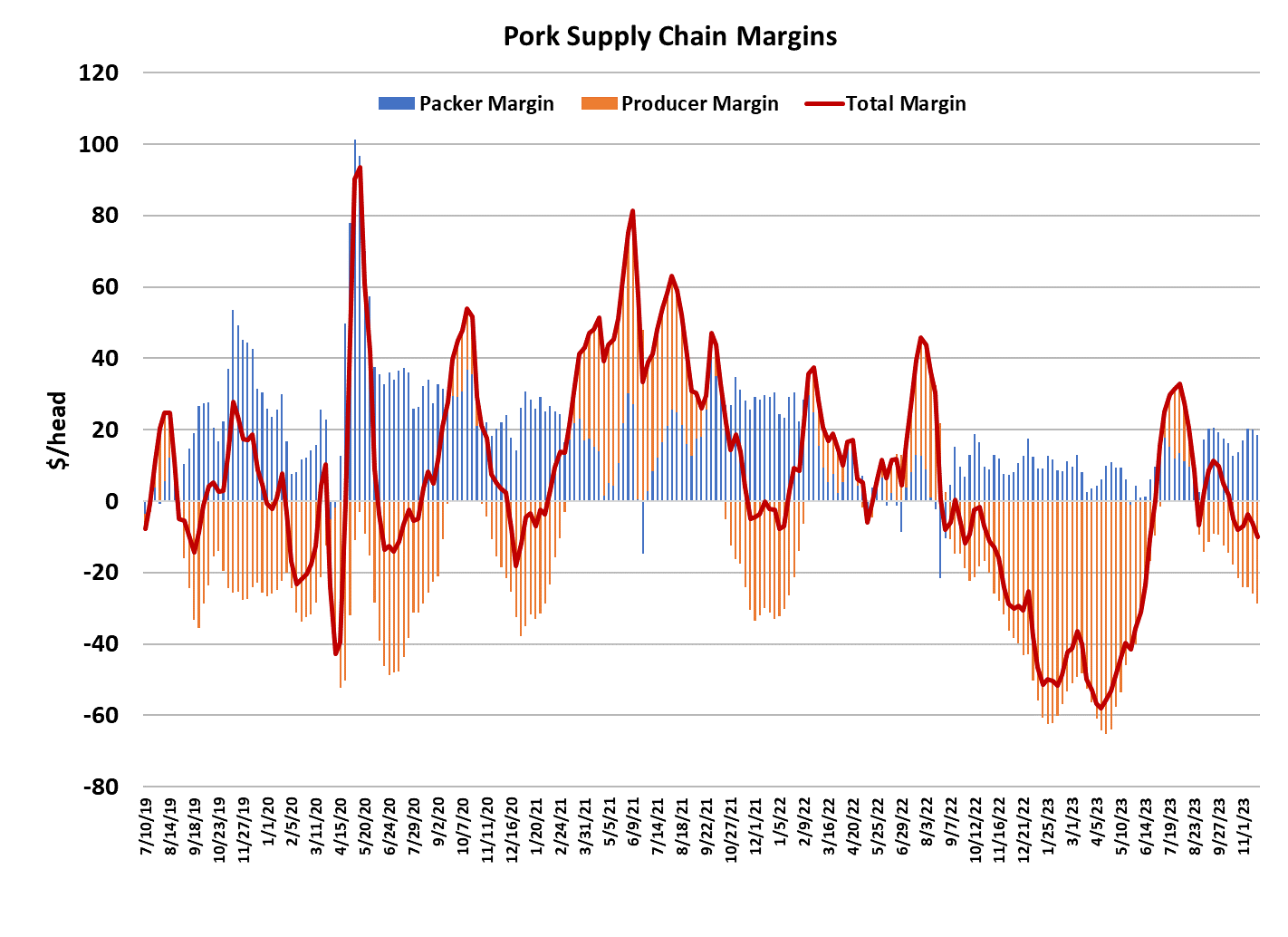

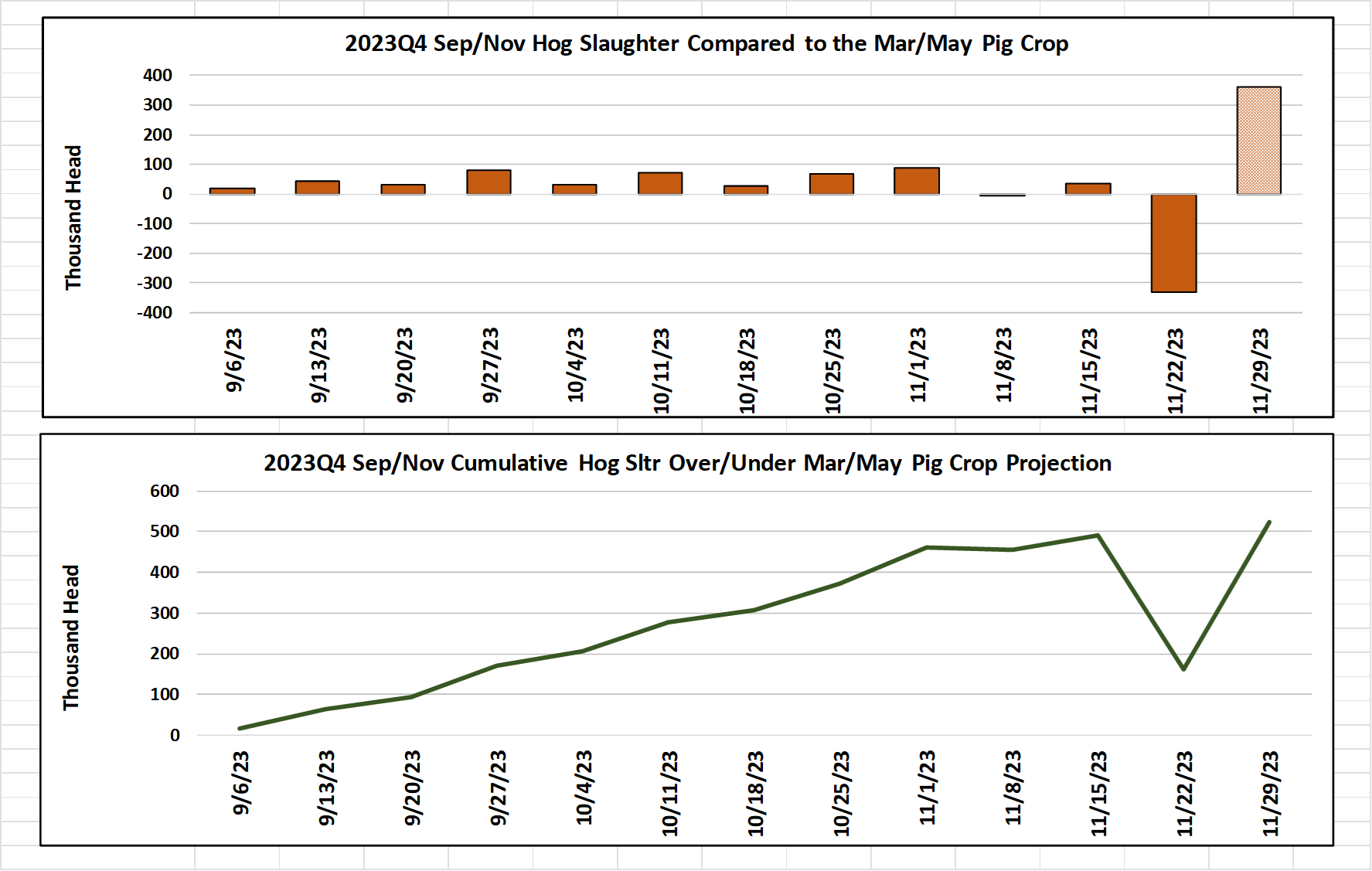

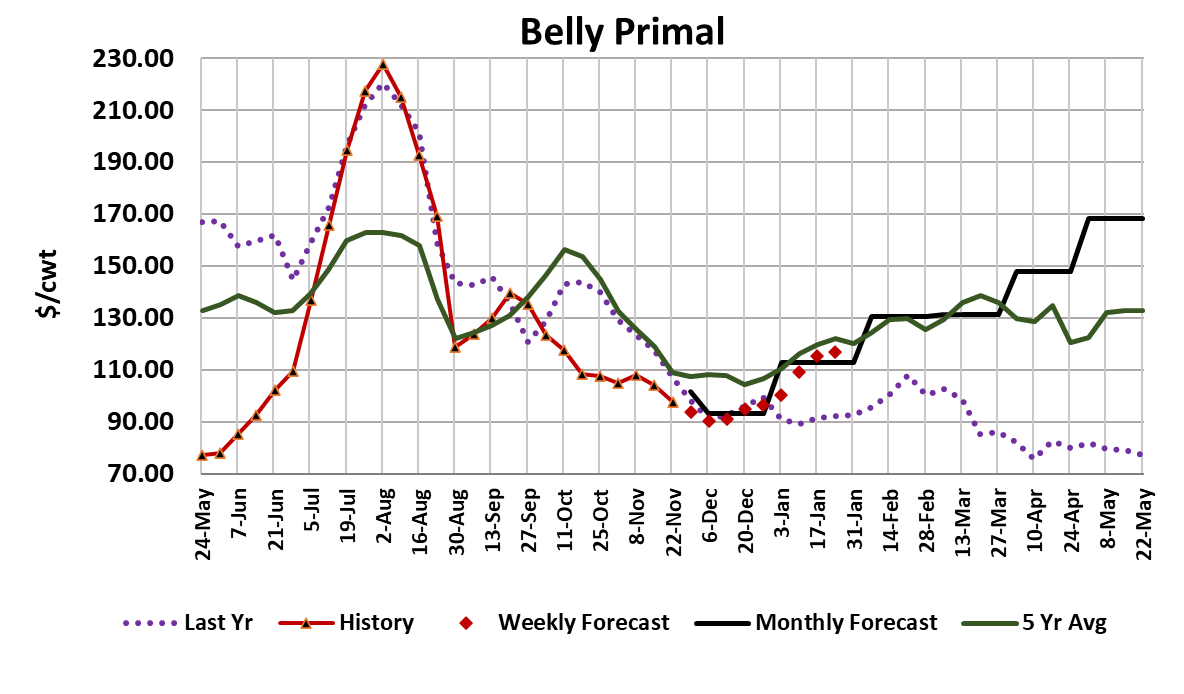

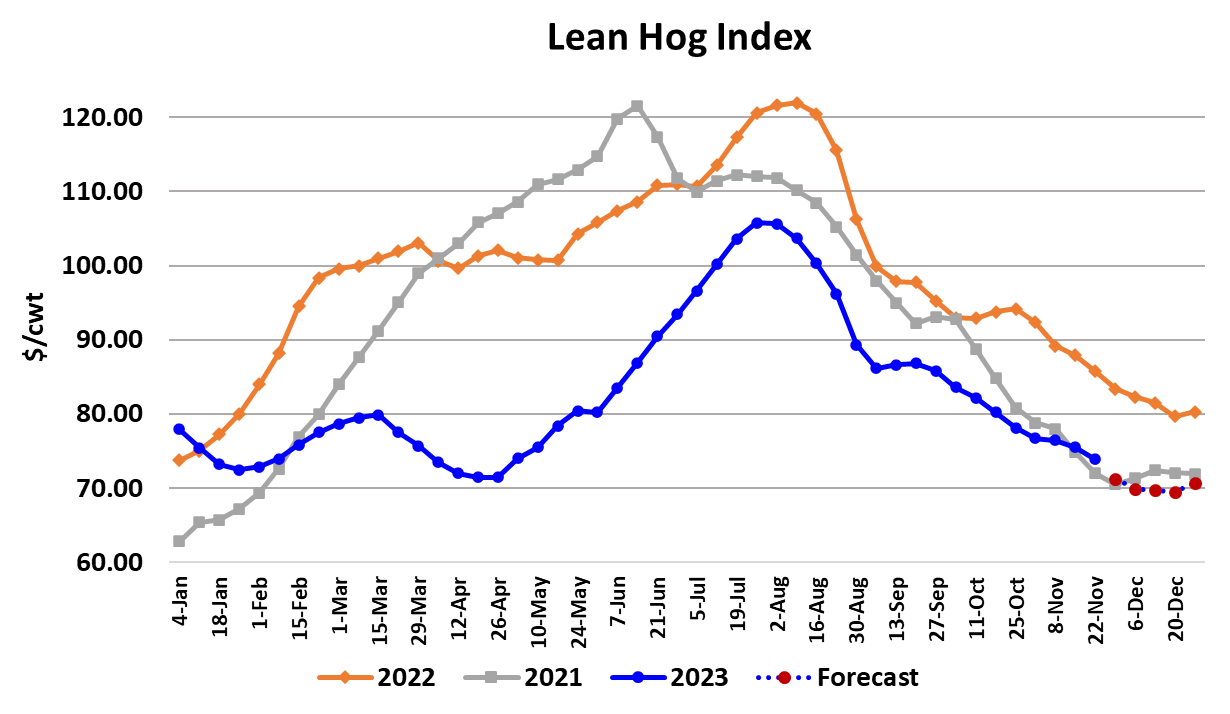

The cash hog markets moved lower again this week, with the WCB negotiated price dropping $3.72/cwt. to average $59.44. That is the first sub $60 weekly average since early December, 2021. The cutout also eased lower, dropping $2/cwt. to average $85.04. There were a lot of buyers on holiday this week and thus demand was pretty light. The biggest losses in the cutout came from the bellies and hams, which probably reflects an effort by processors to work down their raw material inventories ahead of holiday down time. There is a good chance that they will be a stronger force in the market next week. Still, there is no denying that overall pork demand is soft right now and we can see that clearly in the combined margin, which is back to trending lower after a couple of upticks. I lowered forecasts quite a bit this week, with the bellies, hams and loins the primary targets. They just haven’t lived up to expectations. I had been banking on the cutout to rally a bit post-Thanksgiving, but that is looking less likely and thus the revised forecast has the cutout holding in the low $80s through the end of the year. If I’m wrong about that, I’m probably still too high. It looks to me like the belly primal will trade down to $90/cwt. or maybe a little lower in coming weeks. Hams don’t seem to have much direction right now, printing up one day and down the next. If there are price gains to be had there, they are probably small. The weekly export numbers to Mexico have looked soft lately and that may be a sign that hams are going to struggle for a while. This week’s holiday-reduced kill clocked in at 2.21 million head, but it is already starting to look like packers are planning a massive kill next week that could approach 2.7 million head. Kills continue to run stronger than what the March/May pig crop implied and it looks like the deficit will be close to 500k once the quarter closes next week. Very big supplies and very soft demand makes for a pretty bearish story in this market. Futures traders are seeing that too, and this week they trimmed $6-7 off of the Feb and Apr contracts. I think there may also be a misconception that Prop 12 is going to kick in on Jan 1 and that is adding to the bearish tone in the 2024 issues. However, Prop 12 has been in effect since last summer and the only change that will happen Jan 1 is that users will no longer be able to sell non-compliant product that was produced before July 1. Most of that product has likely been already used, and if there is any left in the freezer, it quality has probably deteriorated significantly. So, I don’t think that the end of the year will bring any significant market impact as a result of Prop 12. One saving grace in this large supply environment is that carcass weights are still running two pounds below last year. They ticked down a pound in this week’s data, but I think that was mostly due to rounding and next week they should continue moving seasonally higher. Weights may catch up with last year by the end of December and from that point, I’d expect them to move mostly sideways until spring. This week, USDA provided another update in its Cold Storage report that showed total pork inventories down 14.5% from the same period last year. Total pork in cold storage moved lower from September into October, mostly as a result of hams being pulled out and processed in anticipation of Thanksgiving. It is clear that cold storage inventories aren’t nearly as burdensome as they were last year and perhaps that will help the industry escape a repeat of last spring when large stocks helped keep spot prices under pressure. As the cash market has softened, the front end of the futures curve has moved lower in anticipation of further price weakness, but in the process it has dragged down the 2024 issues to the point that they now all look well underpriced relative to the fundamental forecast. The same thing happened last spring as the market was grinding through a rough patch and the pricing on those deferred issues turned out to be way too low once the summer market arrived. We will get our next look at the supply picture on Dec 22 when USDA releases the next Hogs & Pigs report. It is widely expected that the report will show further liquidation of the breeding herd, but it is unclear whether or not that reduction will be large enough to offset the strong improvements in productivity that have resurfaced in the past couple of quarters. Prices in the back of the futures curve suggest that traders think that the breeding herd reductions won’t be large enough push production down to a level that would give us stronger pricing in 2024. They may also be factoring in a softer demand structure than in 2023, but that was a low-water mark that may be hard to beat. Next week, look for some modest recovery in the negotiated hog markets as packers gear back up for a full kill. The cutout likely continues to slowly ease unless the hams and/or bellies can attract some fresh buying interest.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}