Pork Wrap November 18

It was more of the same this week in the US hog and pork complex,

with most hog and pork prices continuing to leak lower and thus

forcing the futures traders to reconsider their pricing of the Dec

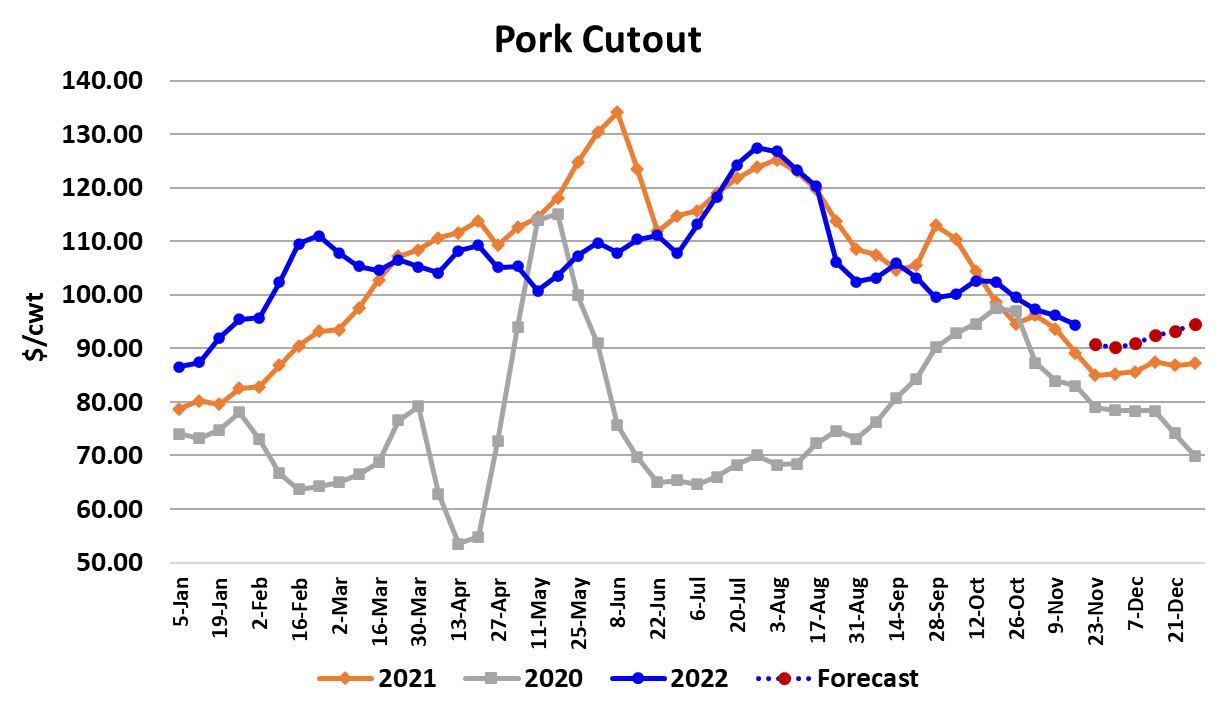

contract. The cutout lost $1.75/cwt. on a weekly average basis and

the NDD negotiated hog market was down $1.88/cwt. Packer

margins also dropped a bit, now at $11.45/head. The LHI hasn’t

yet fully registered all of this week’s decline, but once it does, it

should be close to $86. The Dec futures traded at that level a few

times this week, but by late week it was clear that, with everything

trending lower, traders weren’t comfortable with $86 and the

contract settled just above $84 on Friday. That still isn’t leaving

much cushion for a contract that still has over three weeks to trade.

It is close to my estimate of fair value, but only because I have the

index moving down below $84 and then rising back to that level as

expiration approaches. I could be wrong about that we might just

see hog and pork prices continue to track lower right into expiration.

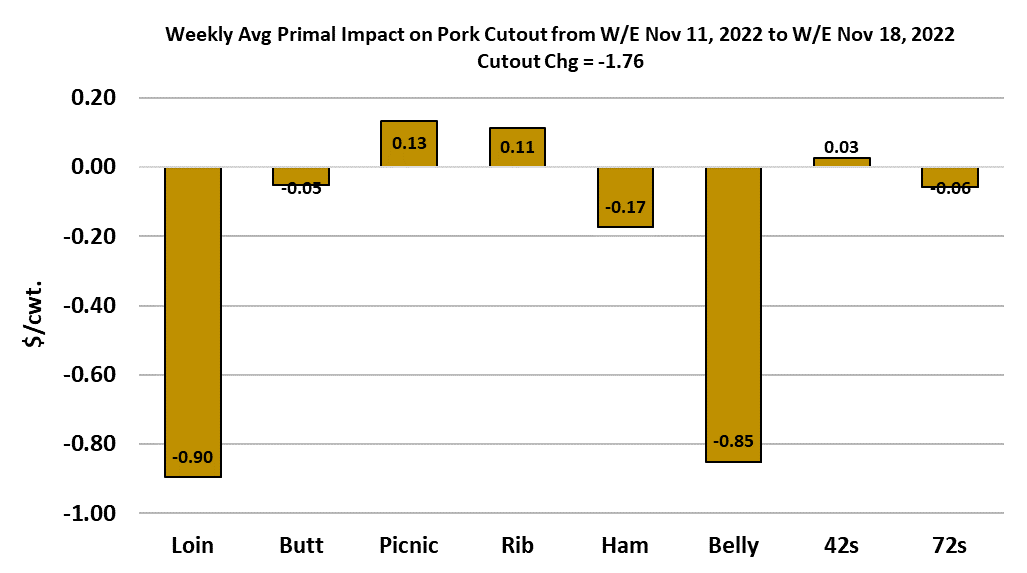

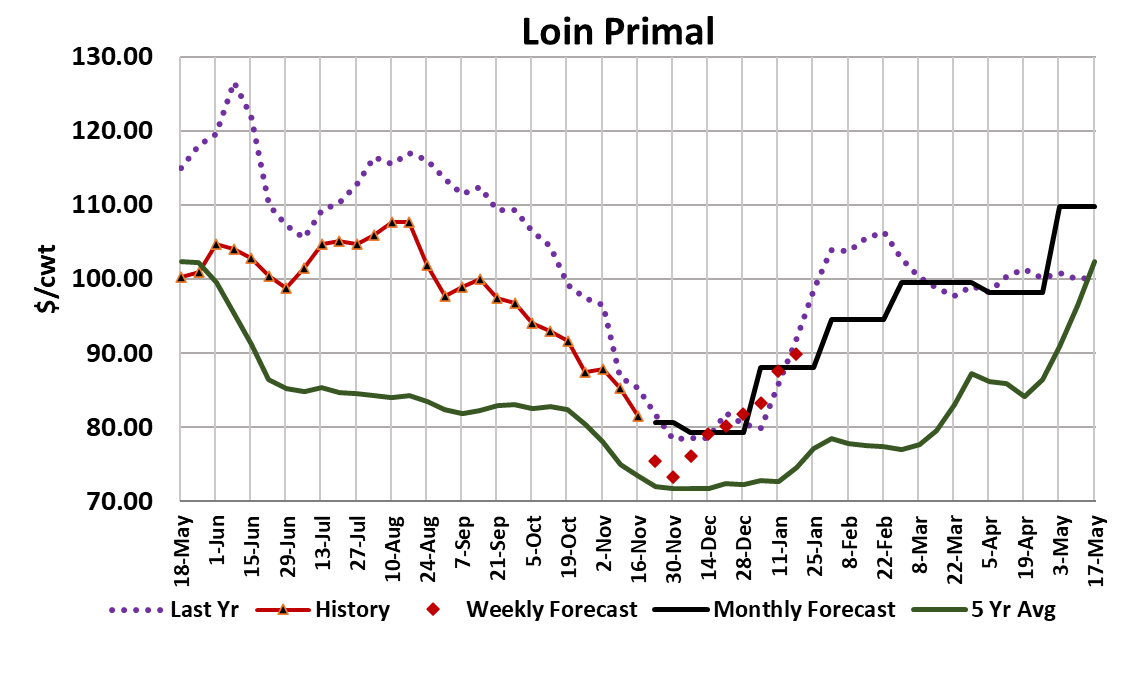

This week it was the loin and belly primals that were the biggest

drag on the cutout. Consistent declines in the loins forced me to

move the forecast lower for that primal through the end of 2022.

The softness in belly prices wasn’t that big of a surprise, but they

are now getting down to a low enough level that some users might

find it attractive to freeze them for use next spring. The down

move in the loins concerns me the most because if demand is

softening now for loins, it probably won’t be long until it also softens

for the butts. Hams have been a huge pillar of support for the

cutout over the past several months, but this week they ticked a

little lower, with the biggest losses coming late in the week.

If the hams are now starting to track lower, it will be very difficult to

move the cutout higher in the next few weeks. Another concerning

feature that arose this week was a significant softening in trim

prices. The 72s lost over $11/cwt. on a weekly average basis and

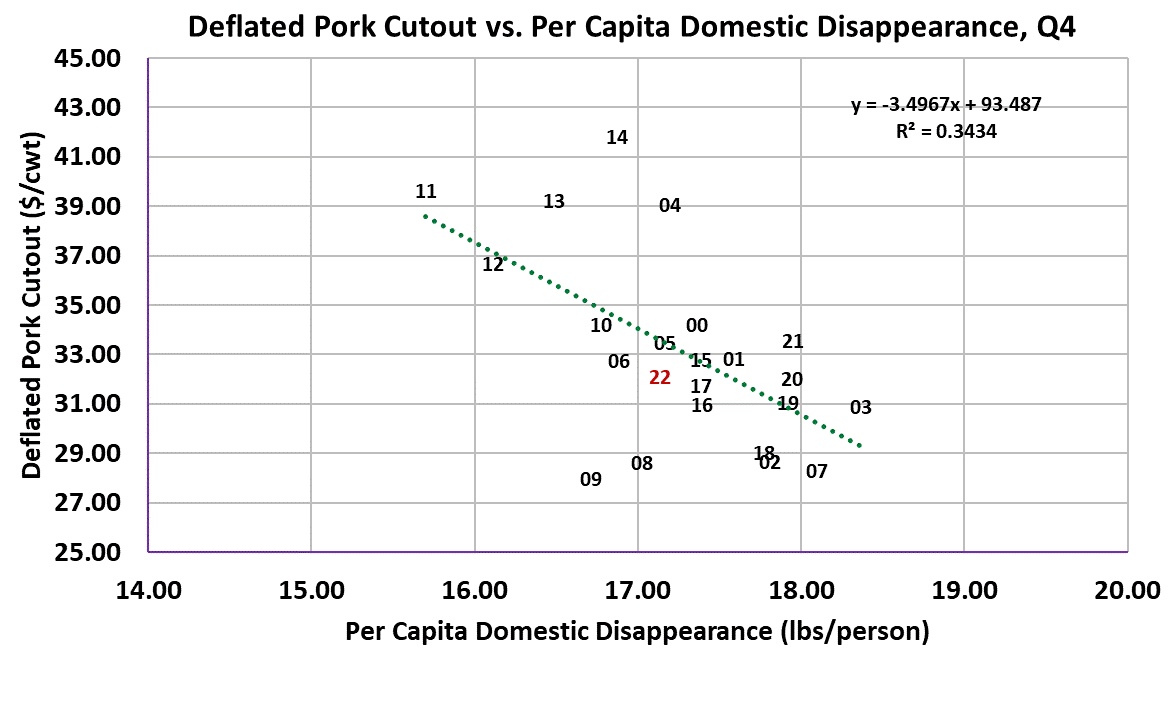

the 42s dropped over $7/cwt. Pork demand appears to be

struggling at present and this can be clearly seen in the combined

margin chart as well as the demand scatter for Q4. The combined

margin is at its lowest level since the fall of 2020 and it is at a level

that rarely visits. Domestic ham demand has probably peaked

now that Thanksgiving is upon us and Christmas is just around the

corner, so any further improvement in ham demand will likely have

to come from our international trading partners. The forecast has

both the ham primal and the cutout continuing lower in the next

couple of weeks and there is a risk that the slide could extend even longer.

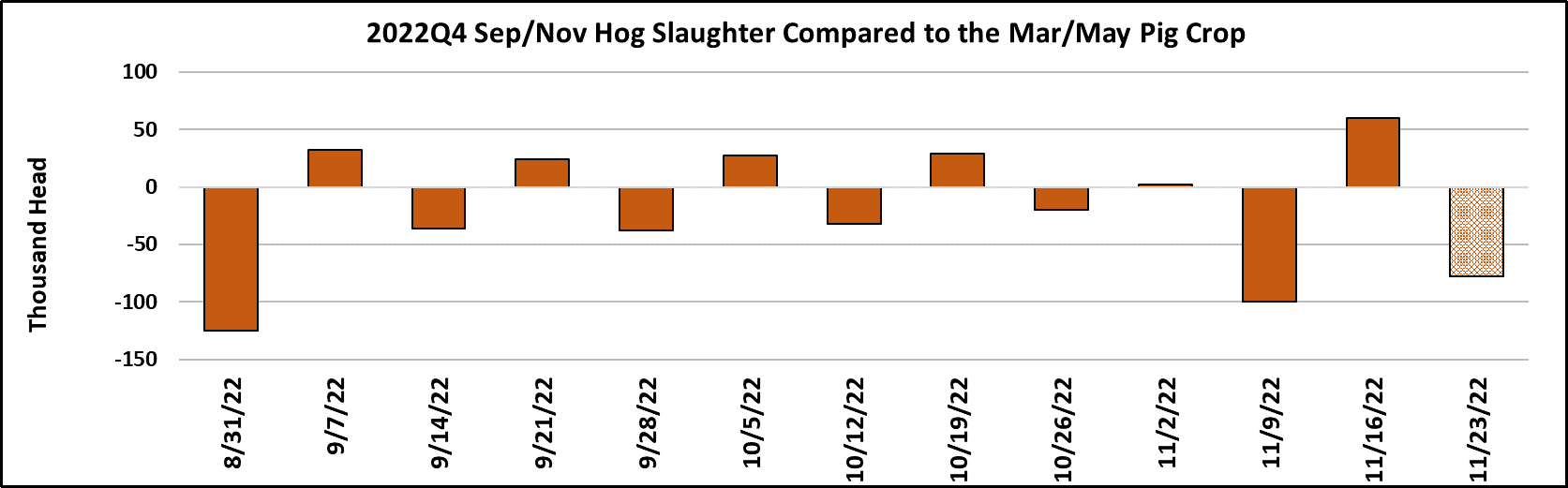

This week’s slaughter came in at 2.61 million head and very

well could be the peak kill of the fall season. Obviously

packers wanted to build some inventory ahead of next week’s

holiday-reduced kill expect that to be only 2.25 million head. It

would make sense then that the best chance for some

improvement in the cutout will come in the week following

Thanksgiving when packers are still a bit short on product.

Look for kills in the 2.5-2.6 million head range during the

weeks between Thanksgiving and Christmas. This was a “big

Saturday” week and that lifted the kill above what the pig crop

implied for this week. However, it still looks like total slaughter

for the Sep/Nov quarter will come up about 250k shy of what

the pig crop implied. Barrow and gilt carcass weights were

unchanged in this week’s data release and the daily weight

data makes it seem like weights are running a little light. It

seems like hog producers are remaining current in their

marketings although pricing in the negotiated hog markets

seems to have cooled down a bit. Export demand continues

to run softer than last year and that will likely remain a feature

for the foreseeable future. There has been no indication in the

weekly data that China is stepping up purchases of US pork as

they sometimes do at this time of year. That just makes the

softening in domestic demand all the more important. Corn

prices remain elevated and hog producers are losing about

$25/head on every animal that they sell. Poor producer

margins are normal at this time of year and producers hope to

recoup the losses in the spring and summer when supplies

tighten and demand is much better.

It seems pretty certain that supplies in the first half of 2023 will

be smaller than this year, given that the breeding herd has

been in contraction mode for several quarters now. However,

we must question whether or not demand next summer can

live up to the high bar that was set in the summer of 2022.

Next week, watch the cutout early in the week for signs that

the market is struggling to digest this week’s large production.

Hams will be the key. If they continue to work lower then

expect the cutout to be down and keep in mind that the futures

still haven’t built in much downside cushion for the LHI in a

period where kills are big and demand is soft. The market may

need to correct that if it becomes clear that the cutout wants to continue lower.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}