Pork Wrap November 17

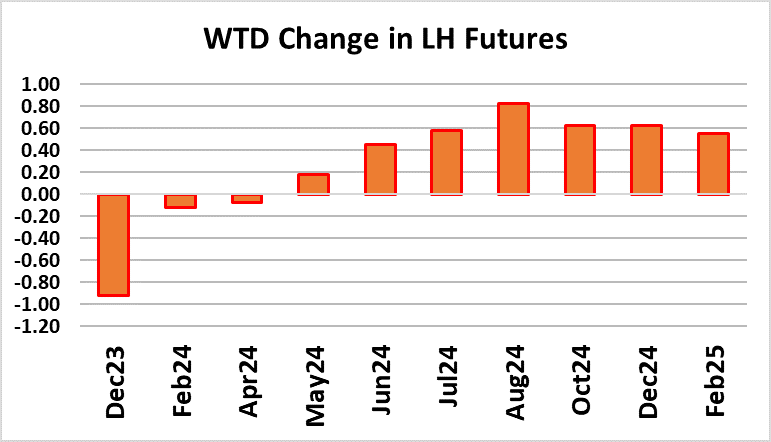

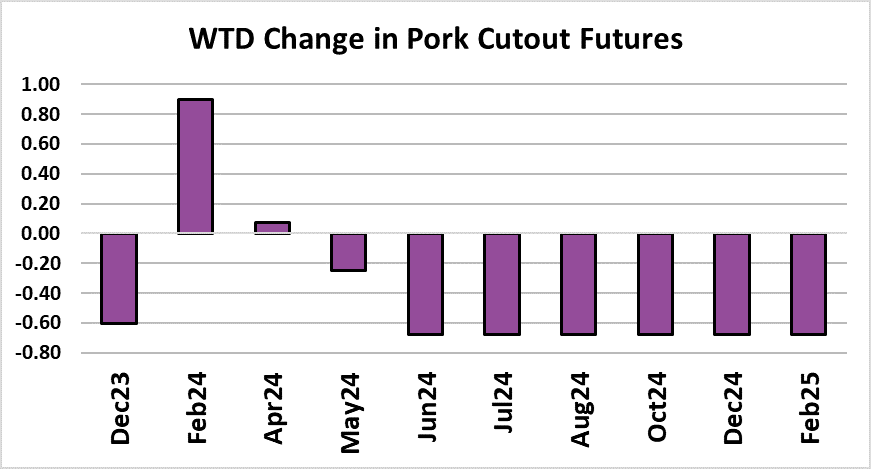

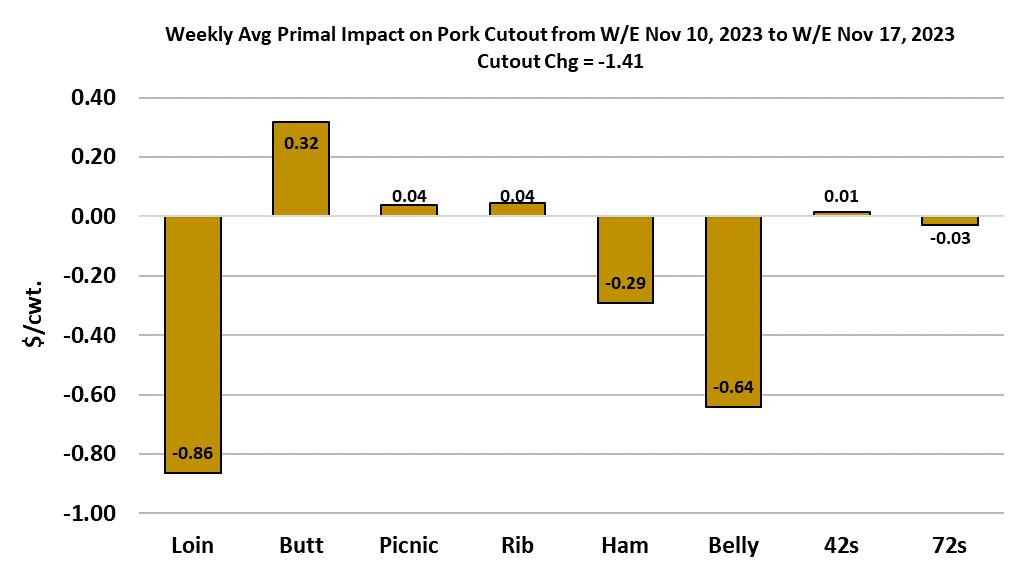

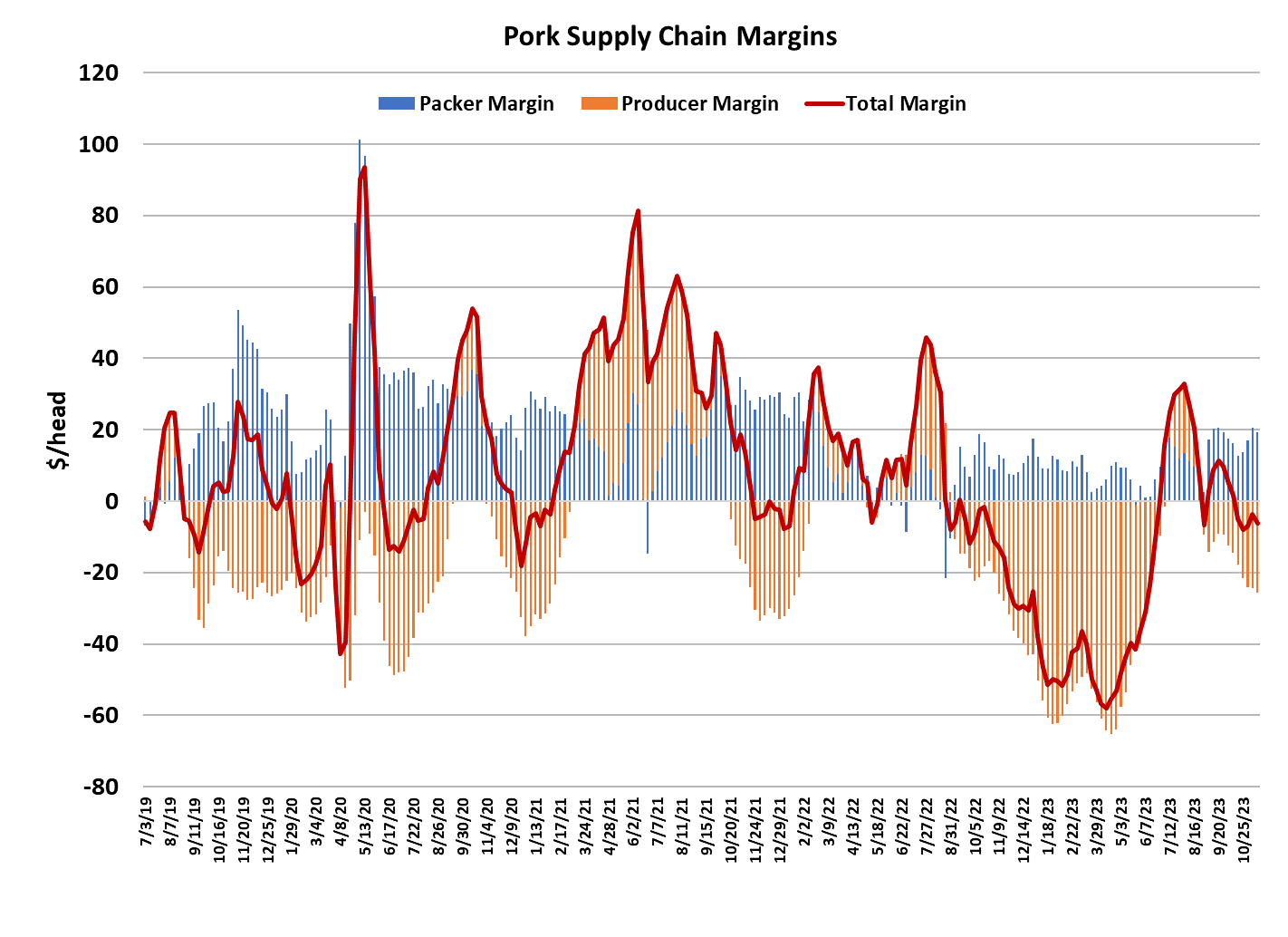

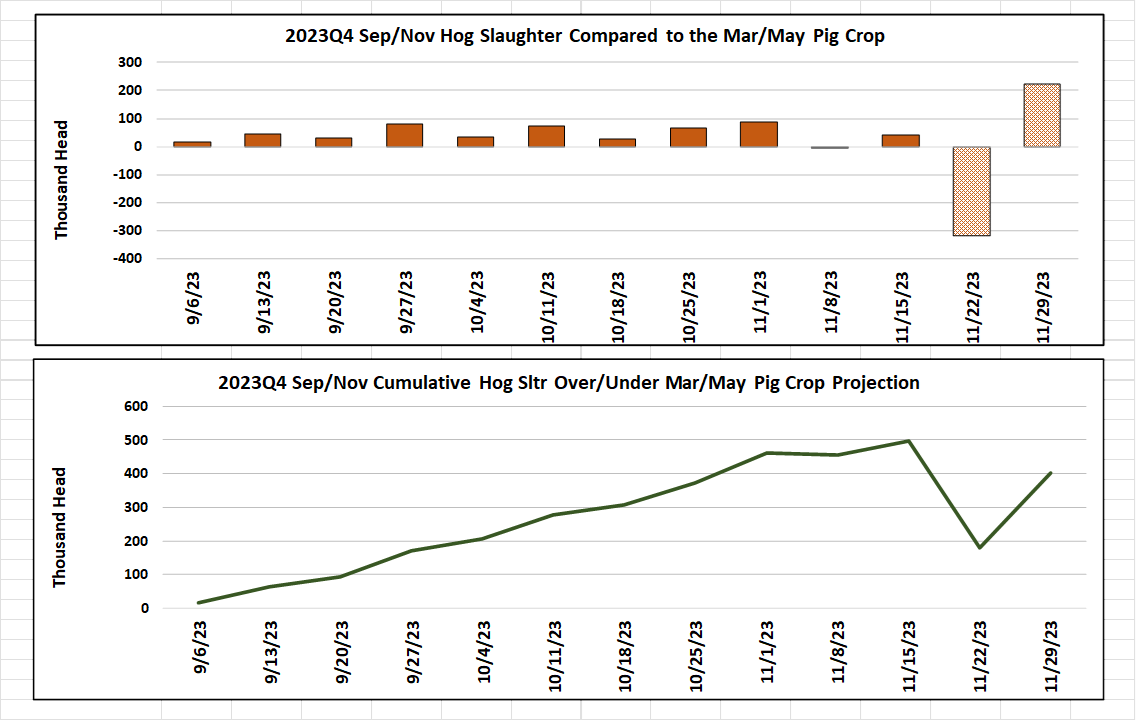

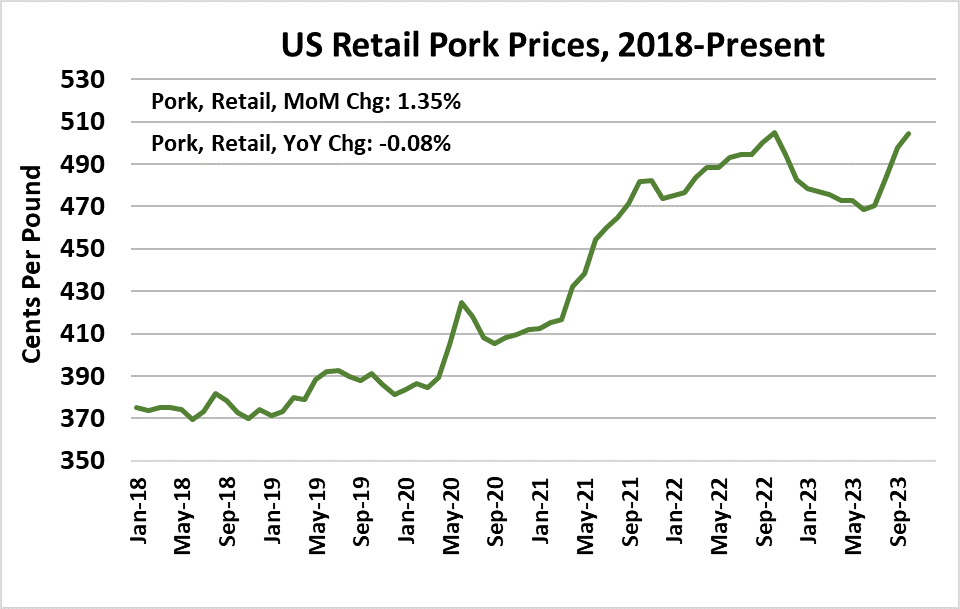

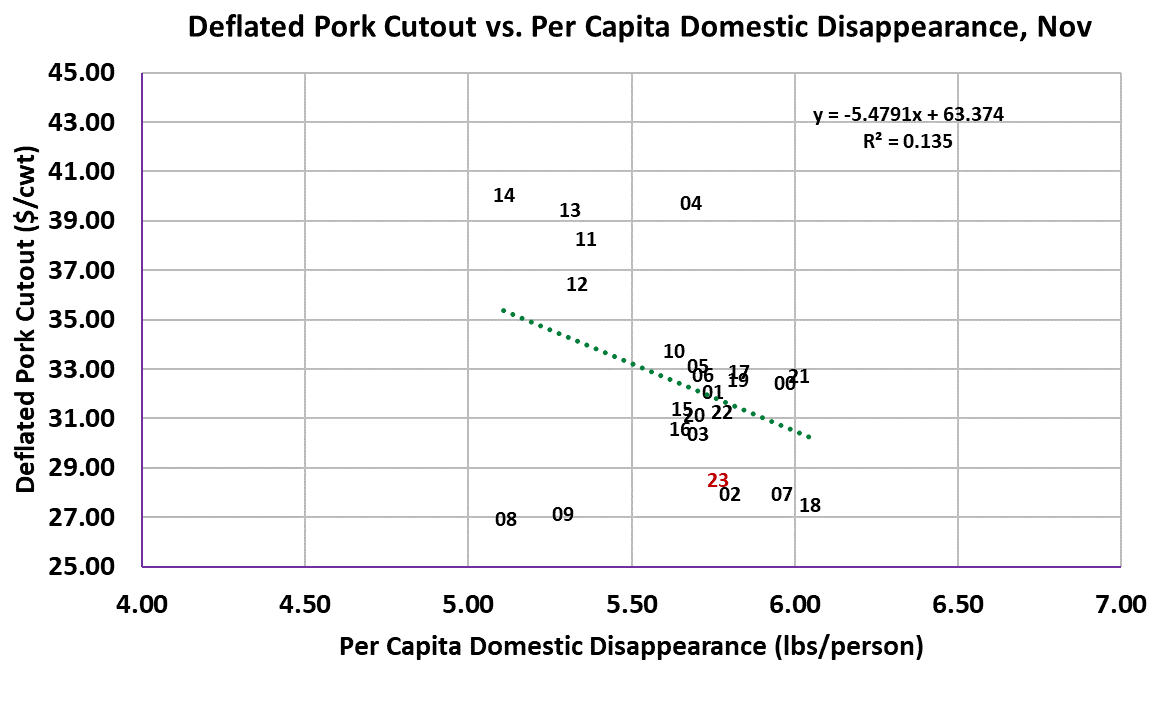

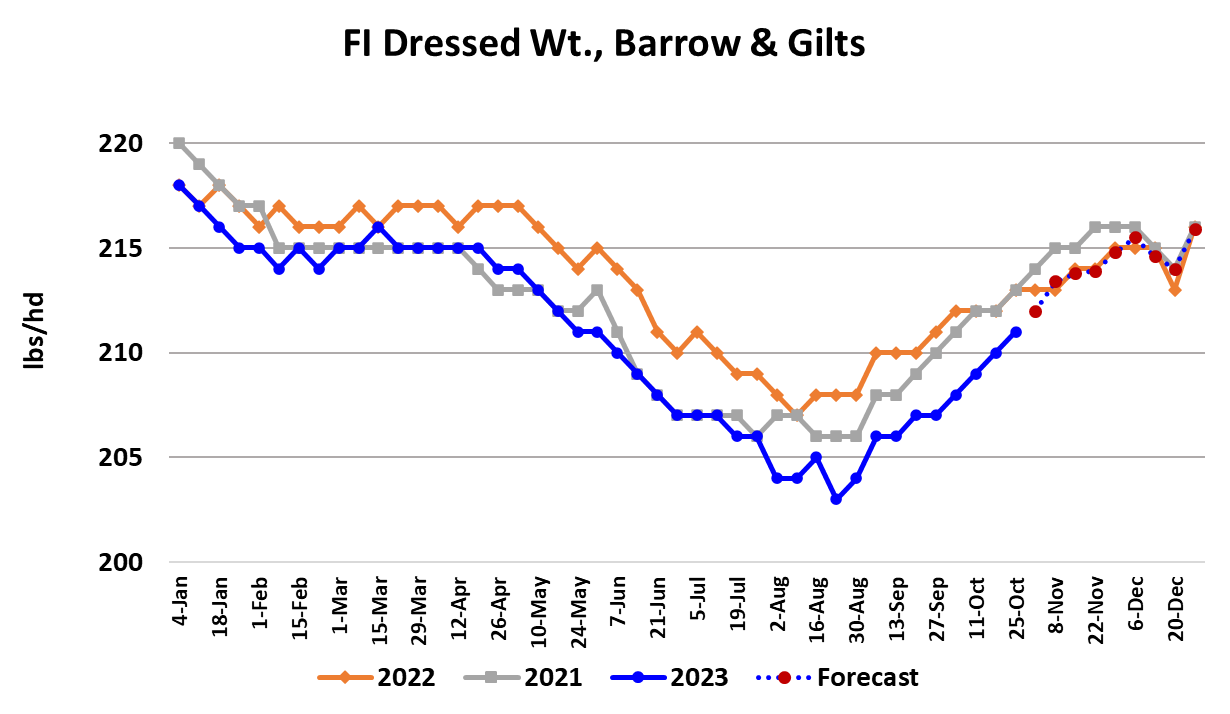

After a couple of weeks of small increases, the pork cutout posted a modest decline this week. On a weekly average basis, it was down $1.41 to $87.05/cwt. Loins were the biggest drag on the cutout, but the hams and bellies also contributed to the decline. The biggest concern right now is the hams, which had been working higher, but started to soften late in the week and thus the ham primal ended up averaging a little over a dollar lower than the week before. Time has likely run out for processing hams in order to have them ready and in the stores ahead of Christmas, so that might have played a role in the downturn. Bellies continue to languish and occasionally print strong but then come crashing back down in subsequent prints. The belly primal was reported below the $100 level twice this week, but finished stronger than that on Friday. I’m having trust issues with the bellies right now. Every time they seem poised to climb out of the cellar, they turn around and go right back down into it. Processing demand for bellies will likely be soft next week because of the holiday, so some further sub-$100 prints are likely. The loin primal continues to hug last year’s price level and if that carries forward, it wouldn’t bottom until the middle of December. I’m forecasting it to show some gains in early December and break out of that pattern, but I could be wrong on that. So there is some additional downside risk to the cutout. Butts and picnics have been the star performers over the past few weeks and I’d look for that to continue, but if either or both stumble then the cutout will be in trouble. The near-term forecasts for the cutout have been reduced a little and I now have it trading down to around $84 in the next couple of weeks before turning a little higher driven by strengthening loins. If the loins don’t cooperate, then a cutout in the low $80s could materialize by early December. Negotiated hog prices dropped again this week, with the NDD price down $3.86/cwt. on a weekly average basis to $63.75. I’d look for negotiated hog prices to follow the cutout over the next few weeks. If the cutout softens, then further declines in the negotiated market are likely, but if the cutout stabilizes or moves higher, then some strength could return to the negotiated market. Packer margins contracted a little bit this week, dropping about $1 to $19/head. Given that hog supplies continue to run above expectations, it is possible that packer margins will move back over $20 in the next few weeks. That would put additional pressure on the Lean Hog Index, should it occur. Pork demand is still tracking very weak, as the attached scatter illustrates. Prices in general continue to ease very slowly in a controlled manner, but the important question is whether or not a bottom is near. I tend to think that the bottom is not far away, especially since kills are now at, or near, their apogee, but continued erosion can’t be ruled out. Retail prices for October were released this week and it was a bit of a shock to see retail pork prices up almost 1.4% from September, especially since wholesale prices were easing during that period. Retail prices are now almost even with last year. That won’t help in the battle with beef and chicken for the consumer’s protein dollar. This week’s slaughter clocked in at 2.65 million head, up 73,000 head from the week before but below the 2.67 million head reported two weeks ago. The holiday will likely constrain next week’s kill to less than 2.25 million head. Every week so far in the Sep/Nov quarter has seen slaughter above what the pig crop implied. The overkill now sits at 500,000 head. It is very likely that USDA will revise the March/May pig crop higher when they release the next issue of Hogs and Pigs on December 22nd. Producer margins are running about $25/head in the red right now, which is typical for this time of year. Within a couple of weeks, I’d expect those to be more than $30 in the red. This has been a terrible year financially for producers. I estimate that for 2023 as a whole, producer margins will be close to -29/head. Of course, that is skewed a lot by the -$60 margins that were experienced in Q1 and early Q2 this year. If that forecast is close, it would be the worst margin year in my dataset going back to 2007. Producers are actively reducing the breeding herd in an effort to improve profitability next year, but at the same time productivity seems to have improved greatly and that is negating most of the supply reduction that would come from reducing breeding stock. It is starting to look like breeding herd liquidation will need to be deeper, and last longer, than I originally expected. On a positive note, producers do seem to be staying current on their marketings, thus there is little danger of hogs backing up in the production pipeline. Once December arrives, the industry will start working through the Jun/Aug pig crop, which USDA reported to be up only 0.4% YOY back in September. Of course, with recent kills coming in larger than what the pig crop implied, there is substantial risk that the same thing will happen in the Dec/Feb quarter and thus we will once again have more hogs than expected. Pork exports appear to be in good shape based on the weekly data, but they are having trouble keeping pace with the strong numbers that were posted last year at this time. Barrow and gilt carcass weights were reported one pound higher again this week, as the seasonal uptrend in weights continues. Weights are still two pounds behind last year, however. Next week, watch for further softening in the hams and loins to drive another dollar or two loss in the cutout. Negotiated hog prices could also soften early in the week as packers will have less need heading into Thursday’s holiday.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}