Pork Wrap November 12

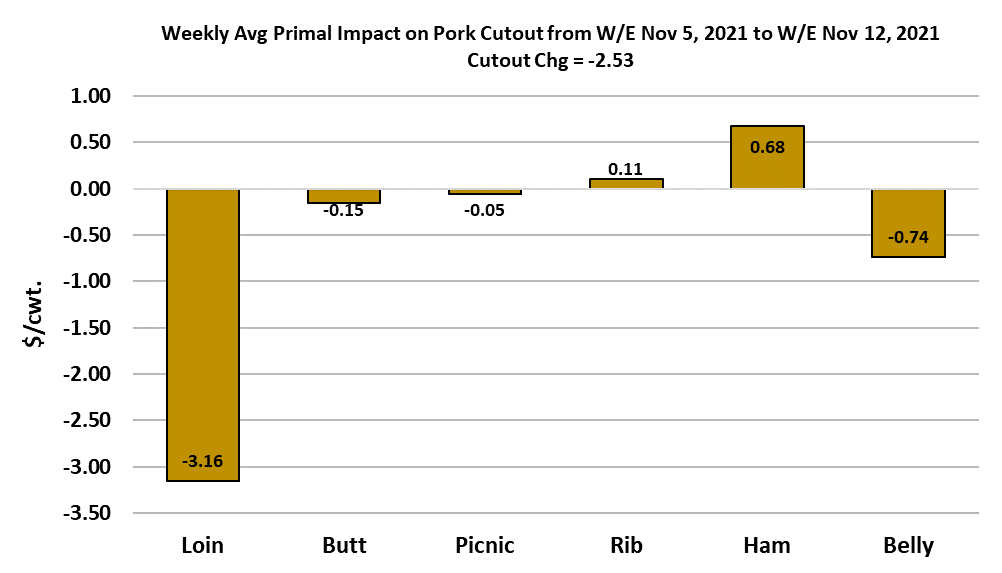

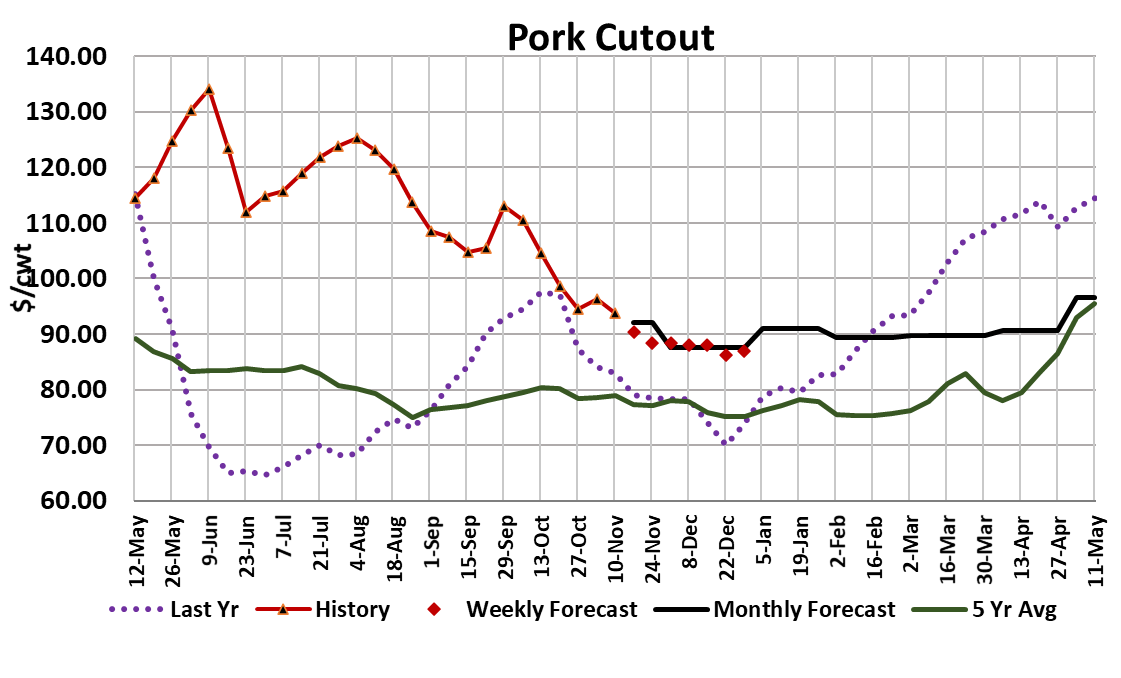

The hog and pork complex eased a bit this week as the cutout dropped

about $2.50 on a weekly average basis and the negotiated hog markets

were down a similar amount. The gains that the cutout posted last

week were erased this week by a downdraft in the loin primal. Hams

were a little higher and bellies were a little lower, but the big move lower

in the loins outweighed all of that. I’ve been concerned that the retail

cuts would weaken under the pressure of seasonally-big kills and softer

demand as people do less cooking at home. This week it was the loins.

Next week it could be the butts or the ribs. The market will have to

deal with bigger production next week due to a slightly larger kill this

week and heavier carcass weights. Further, retailers and consumers

both will be focused on turkeys and hams since it will be the week

before Thanksgiving. Thus, I wouldn’t be too surprised if the retail cuts

slip a bit lower next week.

Hams are still working higher, but that might not last more than about

another week. Bellies also have a strong tendency to work lower from

now to the end of the year, so there is some risk there as well.

However, if the market can just get through next two weeks without

much concession then the short Thanksgiving week kill could pump

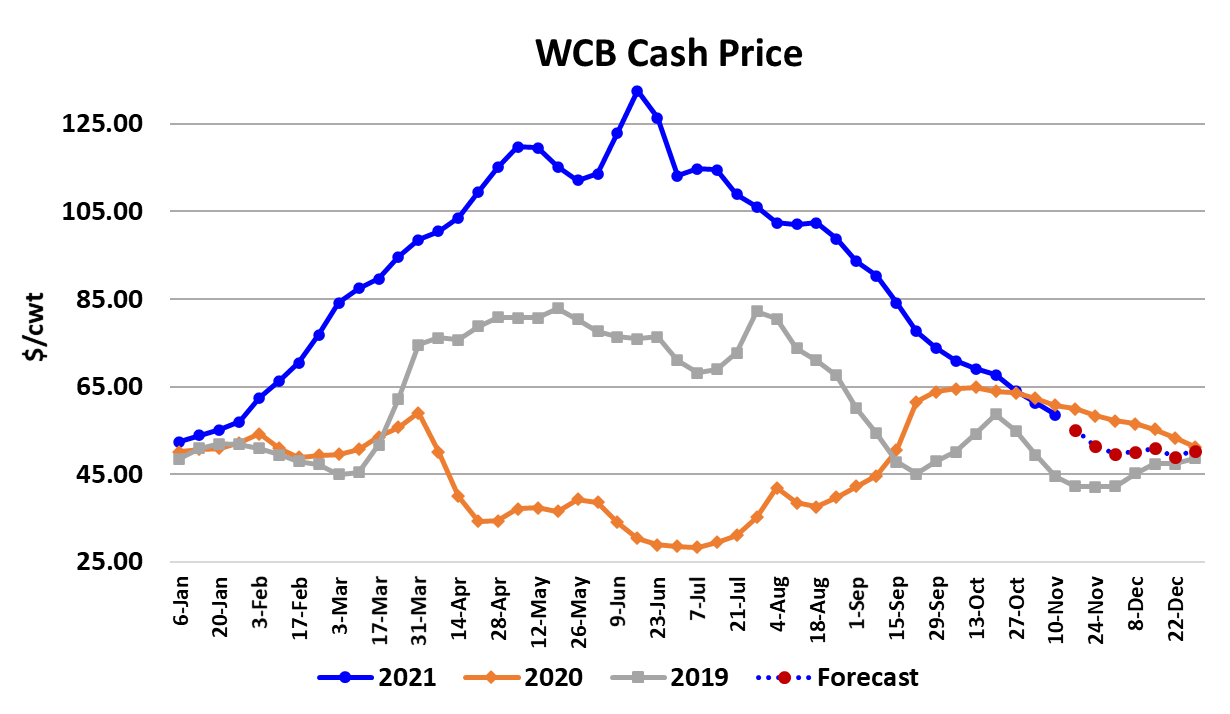

prices back up during the first week in December. This week’s kill

came in at 2.61 million head, which was about 4.5% below last year.

Estimated pork production, which takes into account the fact that

carcass weights are slightly below last year, came in 5.4% below last

year. Meanwhile, the pork cutout averaged almost 12% stronger than

last year at this time. In 9 of the last 10 years, the cutout has finished

the year below where it was in the second week of November, with an

average decline of about $4 (disregarding last year’s massive $14

decline). This year might buck the trend if hog supplies tighten up as

suggested by the last Hogs and Pigs report. The industry will soon

start killing the Jun/Aug pig crop which was estimated to be down 6%

from last year.

There is a contingent of analysts that think that there is a hole coming in

hog supplies that will surprise buyers and force the cutout higher. That

is certainly possible, but I wouldn’t call it a “hole” but more like a gradual

tightening. Whether or not that can translate into higher prices depends

upon what demand does. Right now it appears to be slowly softening,

so it is possible that we could have hog supplies tighten in December

yet not get much of a price increase because demand is weakening.

One thing that we need to keep an eye on is an uptick in COVID

infections here in the US. Medical professionals have started to warn

about another COVID wave this winter as more activities are held

indoors. I wouldn’t expect it to be as bad as last winter’s wave, simply

because we have 65% of our population vaccinated this time around,

but any significant surge will likely result in more meal preparation at

home, which we already know is positive for pork demand.

Carcass weights were reported one pound higher this week, which is

perfectly normal for this time of year. I estimate that weights will

probably increase about 3-4 more pounds before they plateau near

the end of the year or early in January. The next Hogs and Pigs

report is due out on Dec 23 and I’ve scaled back my expectations for

herd growth after the last report showed producers reducing the

breeding herd even though they had enjoyed strong profitability for

most of 2021. Producers are likely concerned about high corn

prices (Dec corn futures gained 24 cents per bushel this week) and

softening exports to China. There is also the increased risk of ASF

jumping to the US now that it has emerged in Hispanola.

They probably also know that it is impossible for demand to stay at

the super-strong levels that we saw in 2021. All of that makes me

think that the next report might not show any increase in the breeding

herd, or a small one at best. That will help keep supplies

manageable well into 2022, but that doesn’t necessary translate into

stronger pricing because I think that the demand erosion will

continue and thus could cancel out any benefit from smaller hog

supplies. The weekly export data continues to look soft, especially

for product shipping to China. I estimate that in Q4 the US will export

22% of its production. Last year in Q4 we were exporting 25% of

production. The market will also have to deal with California’s

Proposition 12 next year and that could further temper domestic

demand for pork. It seems to me that less pork will flow into

California after the first of the year and the product that does go there

will be higher priced, thus California’s pork consumption is likely to

fall. That means more pork that has to be consumed in the other 49

states and we all know from economics class that consumers will

only accept larger quantities when prices are lowered (all else equal).

No one really seems to know what to expect from Prop 12, but just

the uncertainty that it creates is not good for the market. Futures

traders have decided that prices for both hogs and pork won’t get

much cheaper than they are now. The Dec pork cutout futures

settled today at almost $94, which is less than a dollar under where

the cutout printed this afternoon. Lean hog futures traded around

$76 today and by my calculation, the LHI will print $76.40 on

Monday. Traders have been whipsawed a lot lately, mostly as a

result of wild variability in primal values depending on how much

boneless product is in the mix on any given day. As a result, the

futures market has decided to hang very close to the LHI. It is not

trying to anticipate either an increase or decrease from here. I

guess that is the sign of a well balanced market. Next week, watch

for signs of weakening demand in the retail cuts. That could decide

the direction of the cutout, and of course, movements in the cutout

tend to heavily influence movements in the futures and cash hog

markets.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}