Pork Wrap November 11

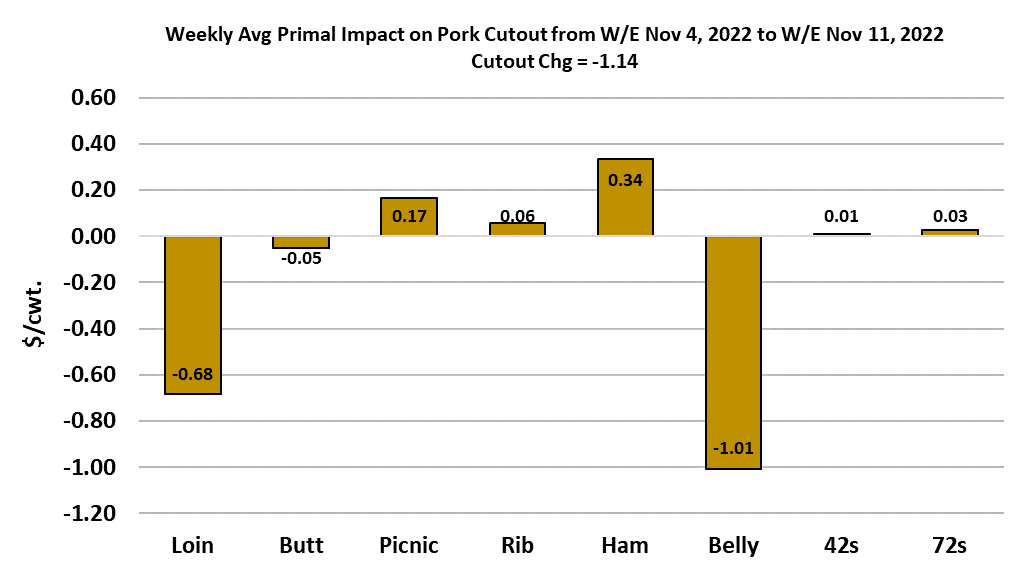

It was a another soft week for the US hog and pork complex. The

cutout fell $1.14/cwt on a weekly average basis and the negotiated

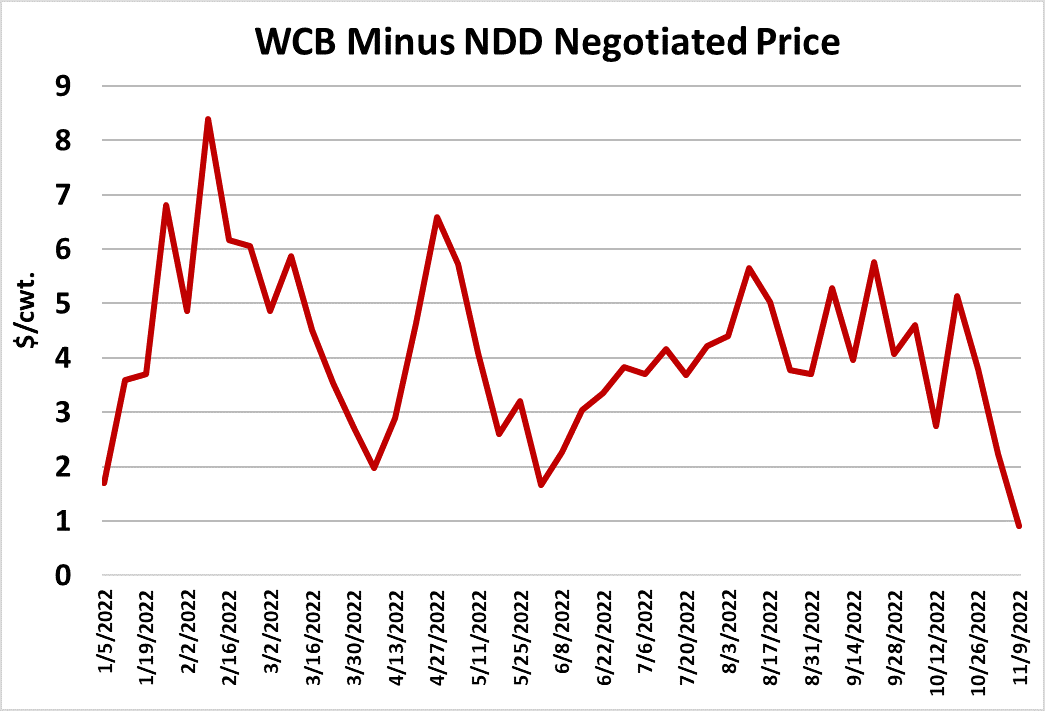

hog markets were also lower. In fact, something very unusual

happened in the negotiated markets today as the WCB cash price

actually fell below the National price. On a weekly average basis,

the WCB price was less than $1 premium to the NDD and the

attached chart shows that is the narrowest that spread has been so

far in 2022. Is this signaling that the tight supply conditions in the

WCB have finally receded? It is probably to early to know for sure,

but if it is true then that should be considered bearish for cash hog

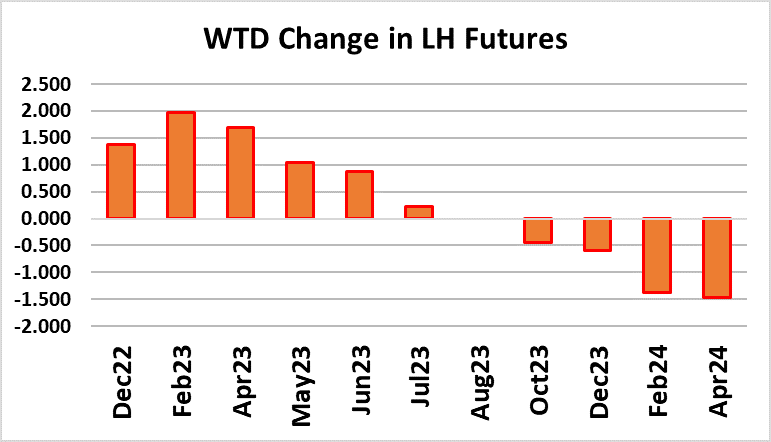

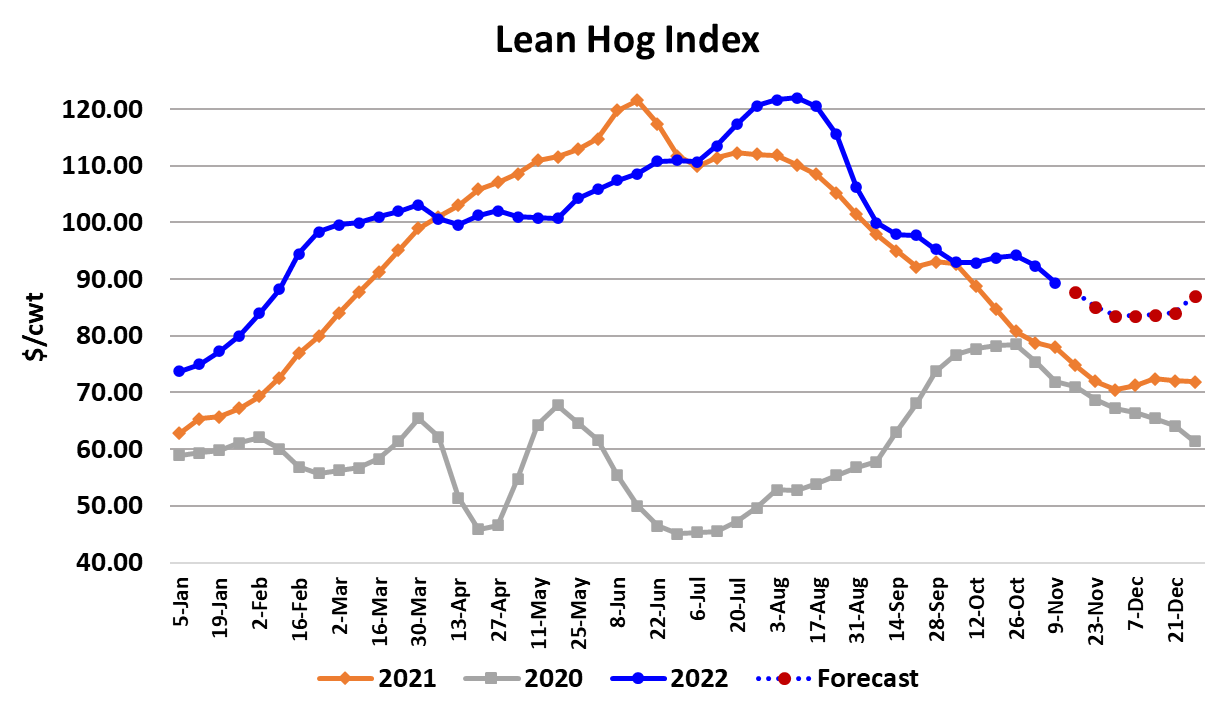

prices and for the LHI. Speaking of the LHI, it was down almost

exactly $3/cwt this week as the recent losses in the cutout and

negotiated markets became fully reflected in the Index. The LHI

currently sits at $88.63 and it will take further softness in the cutout

and/or negotiated markets to drive it any lower. The Dec futures

finished the week at $84.35, so traders are looking for the LHI to

decline less than $1 per week for the next five weeks between now

and expiration.

I can’t argue too much with that, although I suspect that the LHI will

move below $84 briefly in late November before rallying a couple of

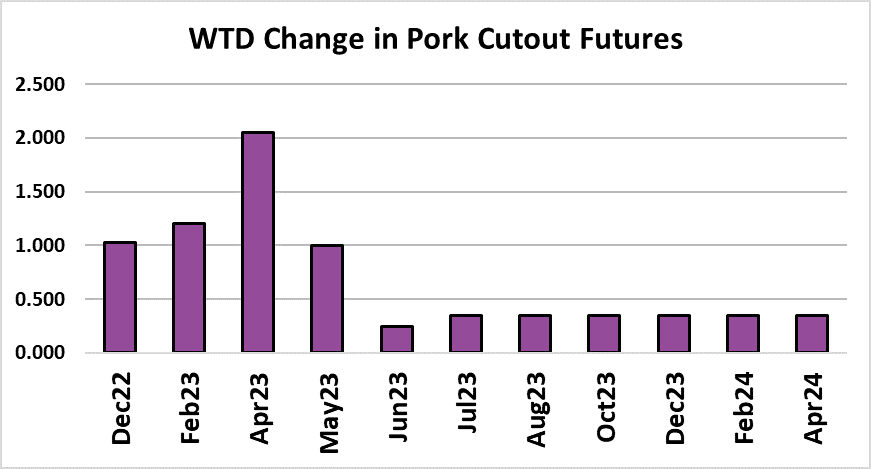

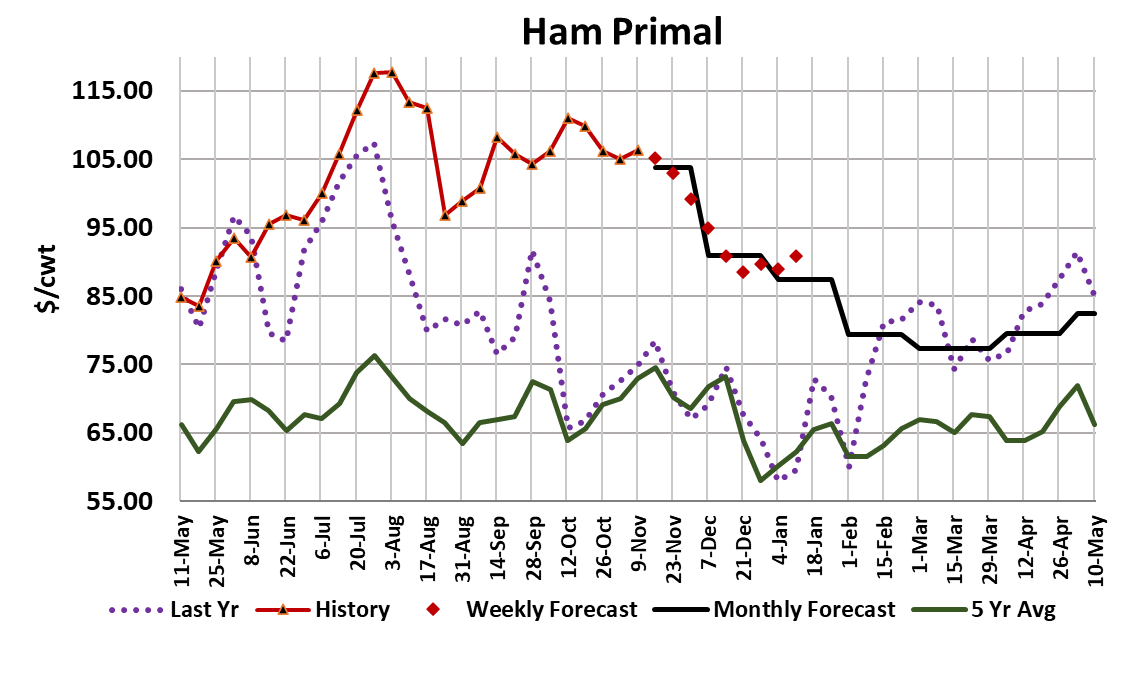

dollars in early December. This week, the bellies and loins were the

biggest drags on the cutout, but that was partially offset by some

modest strengthening in the hams. It seems like every part of the

carcass except the hams is behaving normally for this time of year.

The price strength that hams are demonstrating in the midst of some

of the largest kills of the year is very impressive. I have to believe

that this isn’t all domestic ham demand. Some international buyers

must be soaking up large quantities of US hams. At present the

ham primal is priced about $30/cwt. over last year and the five-year

average. Every week, I keep looking for the hams to break lower

and every week I have to raise the forecast because the hams just

don’t cooperate.

Without this unusual strength in the hams, the cutout would likely be

$5-10 lower than it is today. The belly primal traded $6 lower this

week, but that wasn’t much of a surprise. I expect that bellies will

remain on a downward trajectory until the end of November. This

week I made some significant downward adjustments to the loin

primal forecast because it keeps under-performing and appears as

though it is going to keep working lower in the near term. So the

cutout remains a balancing act, with strong hams at least partially

offsetting weak bellies and loins so that the cutout only trickles

downward a little every week. The forecast has the cutout moving

down to the low $90s by early December and then rising a bit to

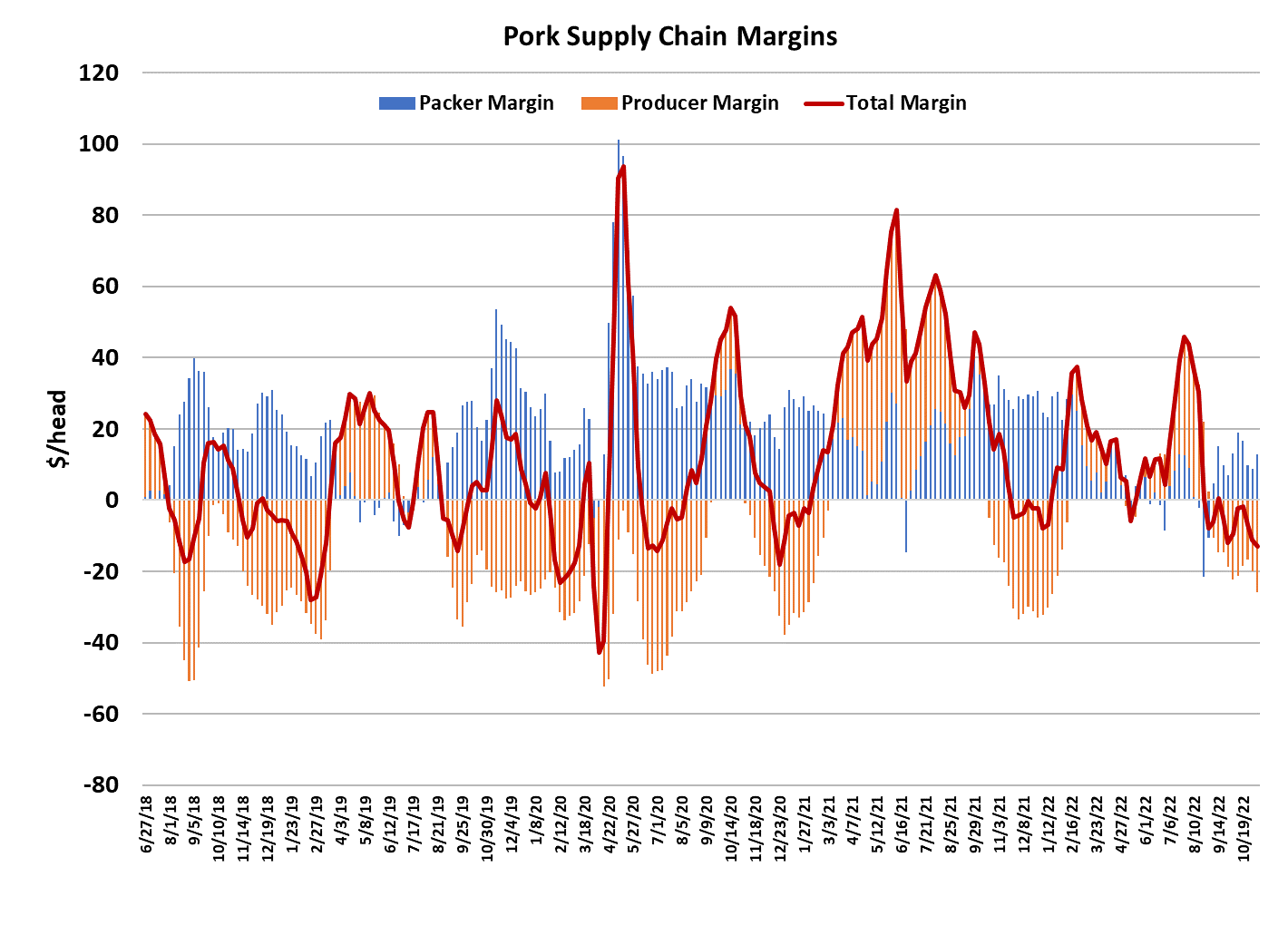

close out the year. Pork packing margins continue to run much

tighter than in recent years and this week’s margin came in just

under $13/head. If the narrowing of the spread in the negotiated hog market portends better hog availability in the weeks to come, then we

could see margins move toward a peak around $20/head near the end of

the year.

That would still be tighter than normal. USDA released its retail

price survey for October this week and it showed retail pork prices advanced

to another all-time high at $5.05/lb. Given that the cutout has been trending

mostly lower since July, this implies that retail margins on pork are quite

strong right now. That’s great for retailers, but high retail prices hinder

movement and that is not a good thing at this time of year when pork

production is near its annual maximum. Next week, retailers will be taking

delivery on their hams for Thanksgiving and we will be eager to see how well

those hams move. Turkey prices are very high this year, so the expectation

is that hams will get more ad exposure than normal and that should result in

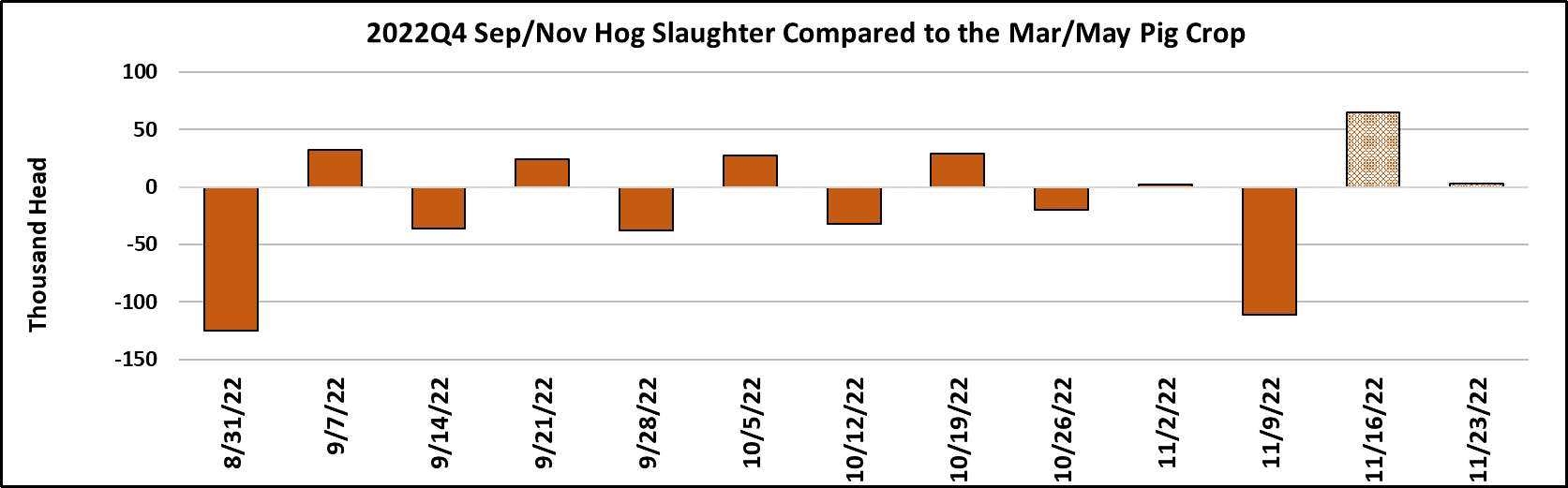

better-than-average sales volumes. This week’s slaughter was smaller than

expected, registering only 2.49 million head. That was about 100k below

what the pig crop implied and the biggest miss so far in the Sep/Nov quarter.

To be fair, this was a “small Saturday” week and there could have been

some reduction in the Friday and Saturday kills due to the tropical storm that

is passing through North Carolina this weekend. If the storm did reduce the

kill, then I’d expect packers to run harder next week to help make up the

shortfall. Next week looks like it could be a “triple witching” week for

slaughter where we have three events all converging to produce possibly the

largest kill of the year: possible storm make-up, a “big Saturday” week, and

the week before a short kill week. I’m forecasting next week’s slaughter total

at 2.61 million head. Of course, that will be followed by Thanksgiving week

where the kill might only be about 2.33 million head. As we approach the

end of the Sep/Nov quarter, slaughter levels are telling us that USDA overestimated the March/May pig crop by about 200-250,000 head. Recall that

USDA over-estimated the pig crop prior to that by a little over 700,000 head.

So I guess their estimates are improving, but it could be that we have a trend

of routinely over-estimating pig crops on our hands. Post-Thanksgiving, kills

should remain in the 2.5-2.6 million head range until we reach the end-ofyear holidays. Carcass weights advanced one pound this week, but that

was in line with expectations for this time of year. So far, the weight data

continues to paint a picture of hog producers that are current on their

marketings. That’s a bit at odds with what we are seeing in negotiated hog

prices, but hopefully the picture will become clearer with a couple more

weeks of data. The hog and pork complex seems to be in good balance

right now. Production is seasonally large and prices are working lower as

they should at this time of year. The nearby futures seem to have honed in

on a reasonable value for the LHI in mid-December. The two things that are

a bit out of the ordinary are super-high ham pricing and relatively narrow

packer margins. Next week, watch the hams for potential weakening under

the weight of bigger kills, because there isn’t much outside of the hams that

is supporting the cutout right now.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}