Pork Wrap November 03

The

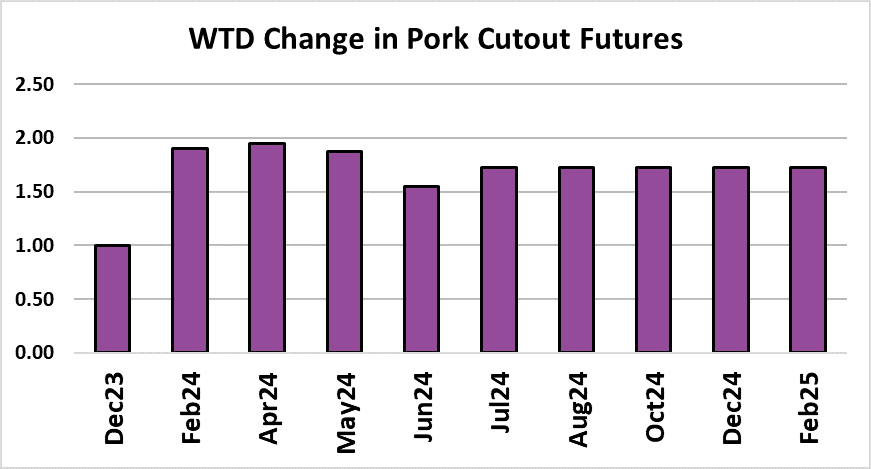

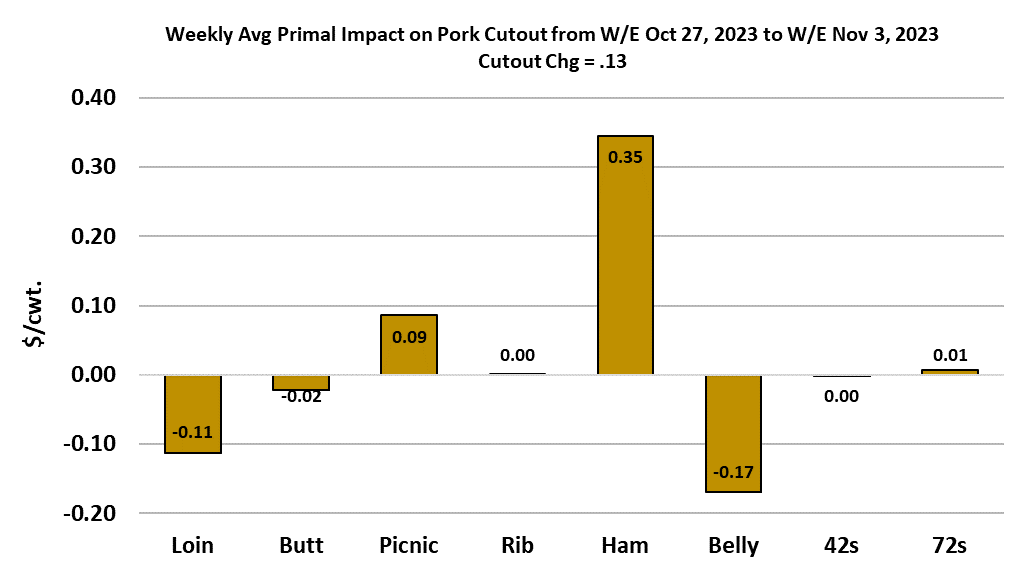

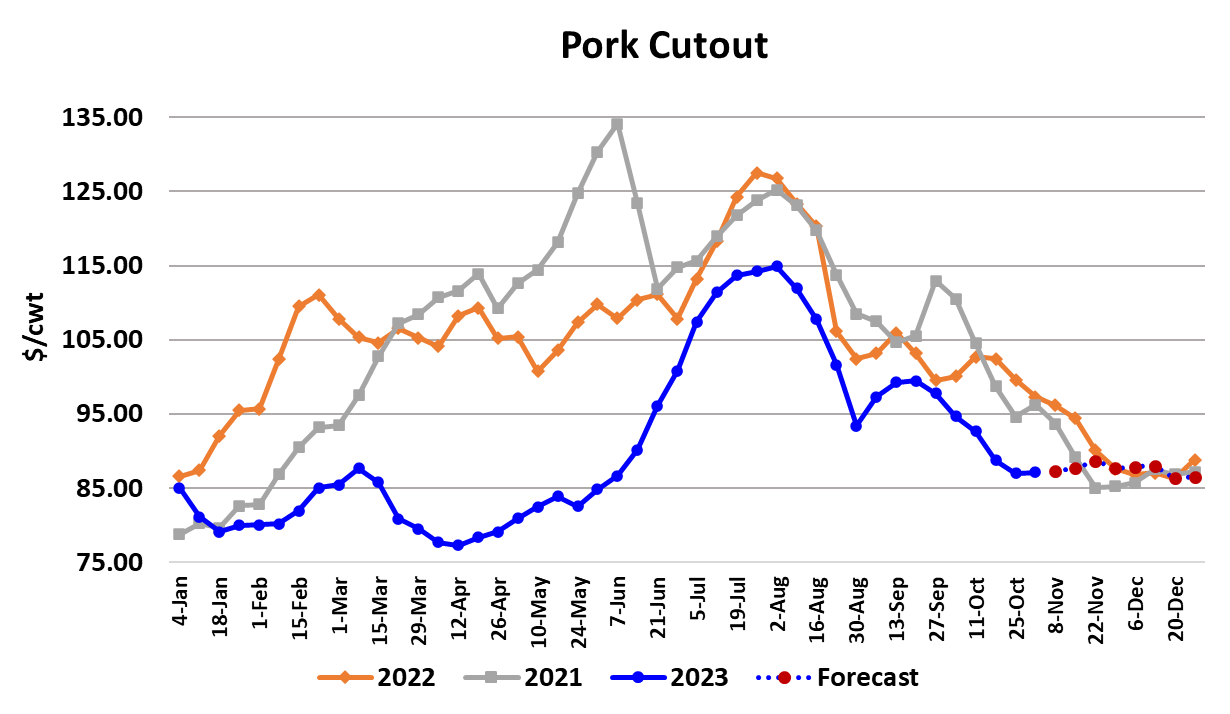

biggest surprise in the hog and pork complex this week was the failure of the

cutout to decline. We have become accustomed to weekly $1-3 declines in

the cutout this fall, but this week the cutout actually averaged $0.13/cwt.

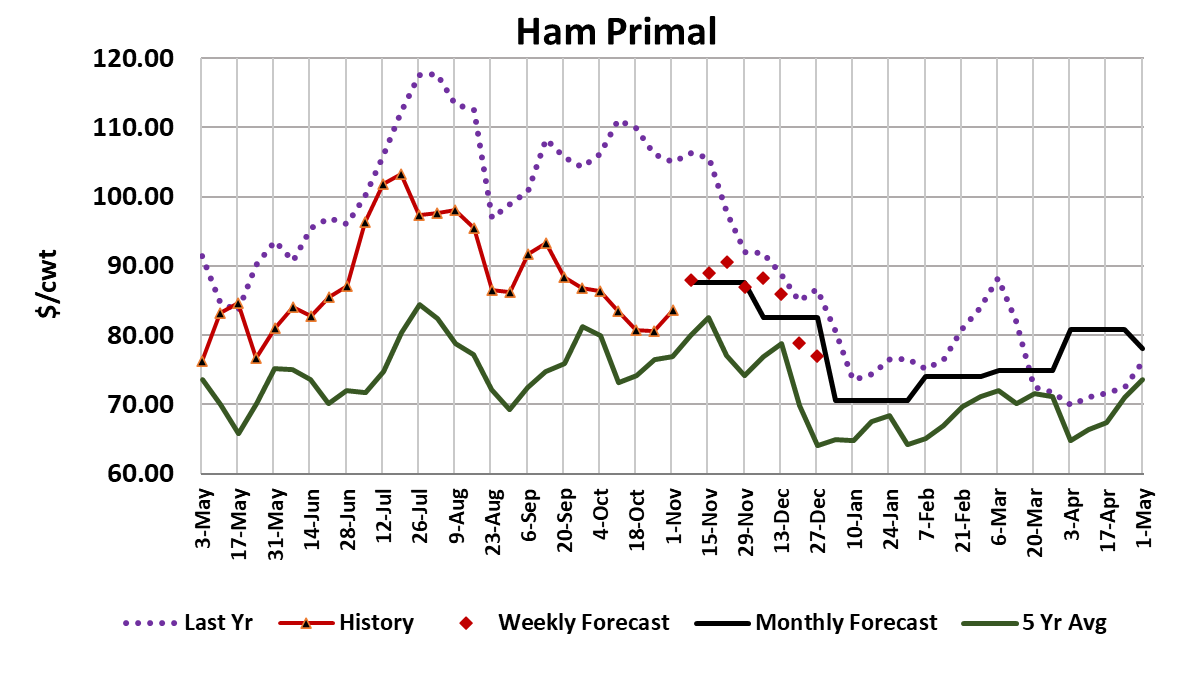

higher than the week before. The big driver of this change in

direction was the hams, which finally got some traction after declining for six

weeks in a row. To be sure, the gains were small and we need to see some

follow through next week, but a turn higher in ham prices was a huge boost for

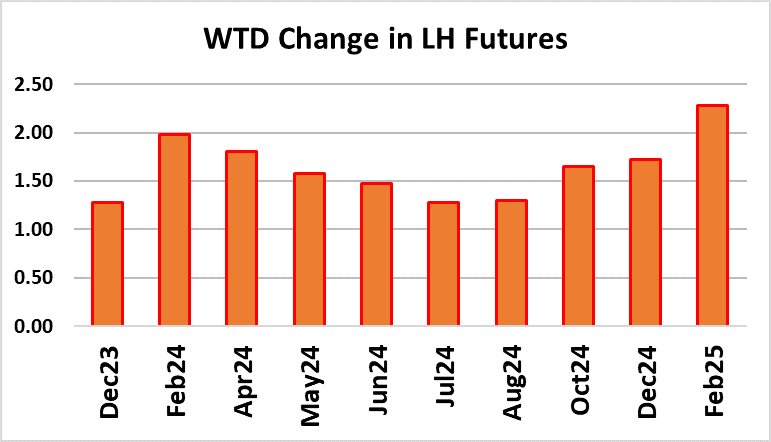

the market bulls. The front of the futures curve gained about $1.50/cwt.

on the week, with the Dec contract trading over $73 for a bit on

Thursday. That was a far cry from the $66 level that the market traded

less than 10 days ago. The belly primal moved a little lower on the week,

but that primal was showing some signs of stabilizing near the end of the

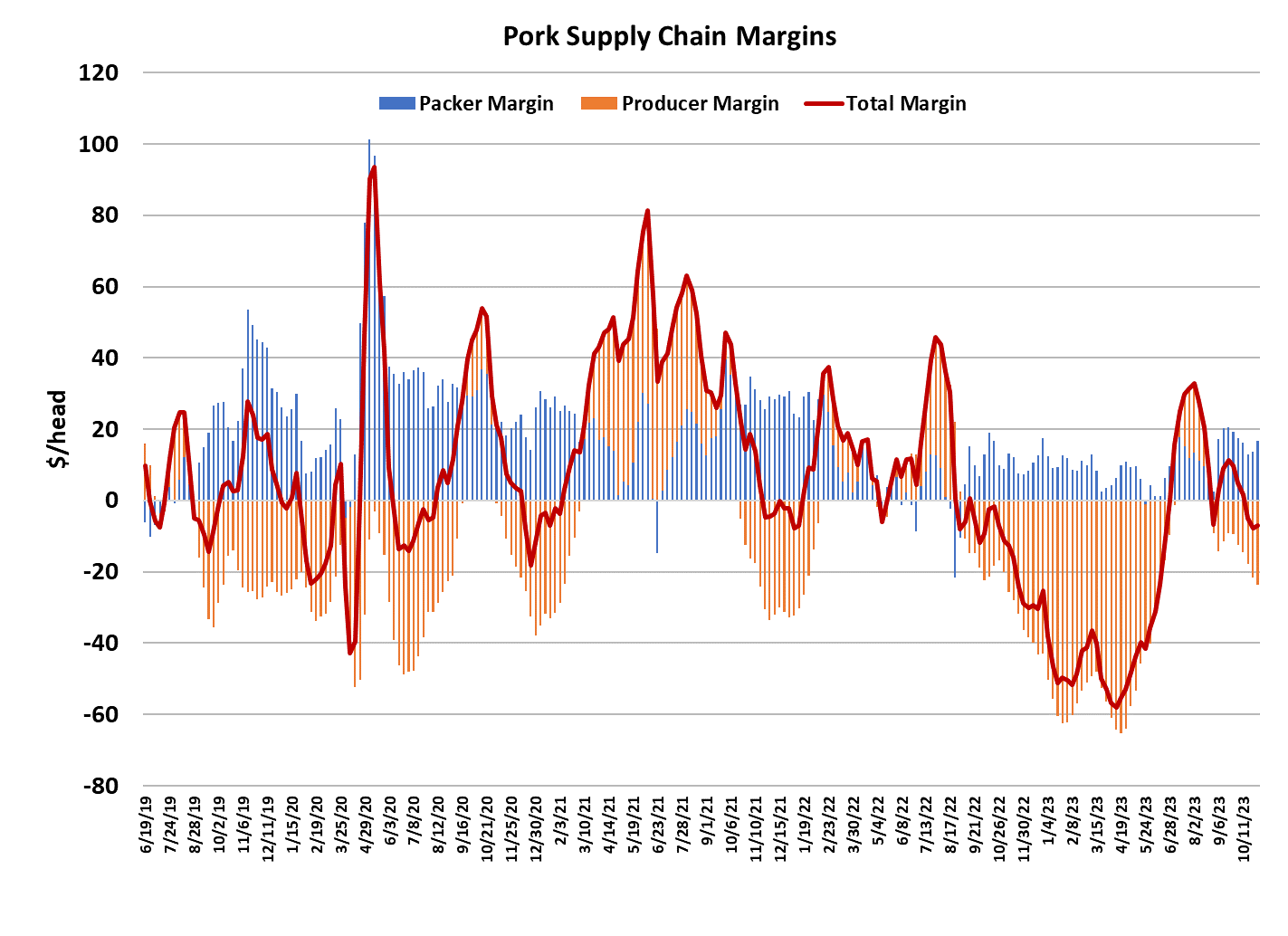

week. The combined margin posted a small uptick this week after

trending lower for the past six weeks. While one data point isn’t enough

to call an end to the downtrend in demand, it is an encouraging start. It

looks to me like we have two things going on right now. The processing

items (bellies, hams and trims) are showing a very slight uptrend in the works

and the retail primals are still showing slight downtrends in prices. The

two almost offset one another, hence the nearly flat cutout this week.

Stronger demand would be especially welcomed next week, when the industry will

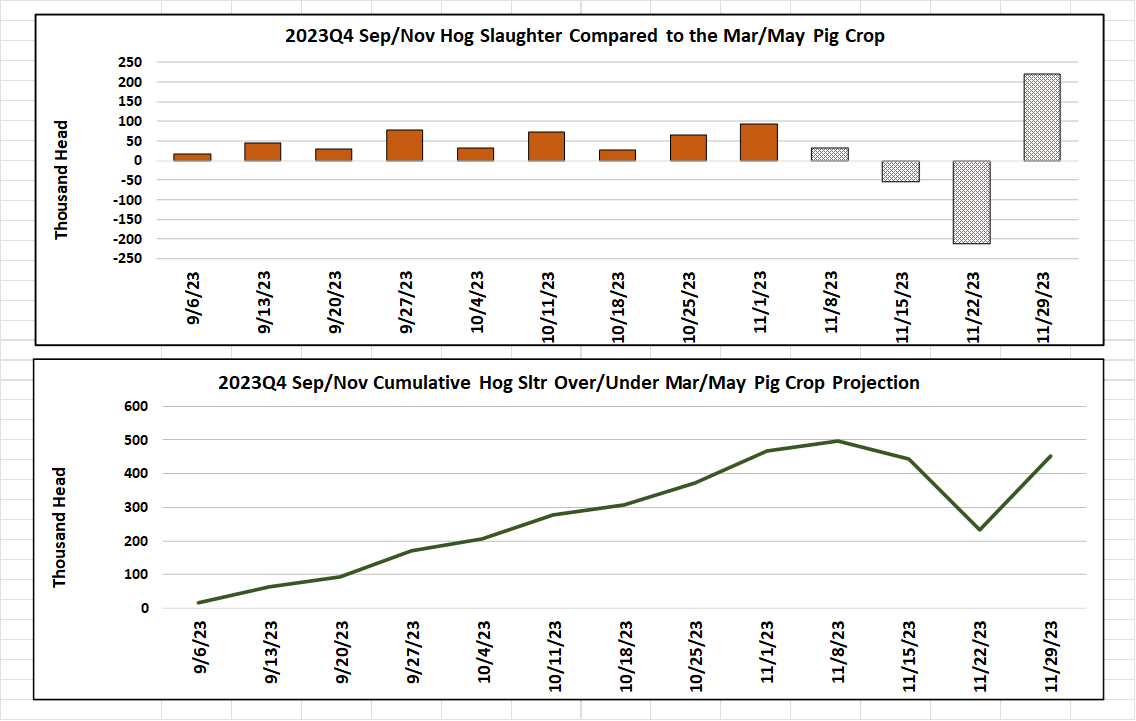

need to work through this week’s huge production. Total swine slaughter

was estimated at 2.68 million head this week. That is way bigger than the

max kill I was expecting this fall and a clear sign that there are more hogs

out there than advertised by the March/May pig crop. It does look like

packers are on the alternating “bigger then smaller” Saturday kills and this

Saturday was a big one at 260k. By comparison, last fall’s biggest Saturday

kill not associated with a holiday was 203k and that came in the middle of

December. With four weeks left to go in the quarter, it looks like the

industry has overkilled the pig crop by close to 500k head. Needless to

say, it is likely that USDA will revise the March/May pig crop higher in the

December H&P report. So, there was a lot of pork produced this week

that must be sold next week, but we have seen the market handle

bigger-than-expected production at times this fall without a serious price

collapse. It is also possible that packers may have a strong book of

holiday-related contracts to deliver on and thus all of the extra production

might not show up in the spot market. I’m currently projecting next

week’s kill at just a little under 2.6 million head (a smaller Saturday week),

so the average of this week and next might fall closer to 2.64 million head—still

bigger than expected, but not grossly out of line with the pig crop.

Negotiated hog prices declined this week, with the NDD price averaging

$2.77/cwt. lower than last week’s average. With the cutout steady

and cash hogs falling, packer margins expanded to nearly $17/head this

week. It isn’t unusual to see bigger packer margins in November compared

to October, so we shouldn’t read too much into the margin increase.

Margins are still smaller than normal for this time of year and I’m forecasting

them to remain that way through the balance of the year. It would

surprise me to see a packer margin much larger than $20/head during Q4.

If it is going to happen, it most likely happens near the end of November and

then margins narrow again during December. The forecast has the pork

cutout holding in the mid to high $80s for the next several weeks and the LHI

holding in the mid-$70s. It seems pretty bold to call the cutout steady

from this point forward, particularly given the big production we saw this week,

but I’m counting on some upward momentum to build in the hams and that could be

enough to offset small declines in the other primals. That forecast also

assumes that belly pricing doesn’t get much worse than where it is at

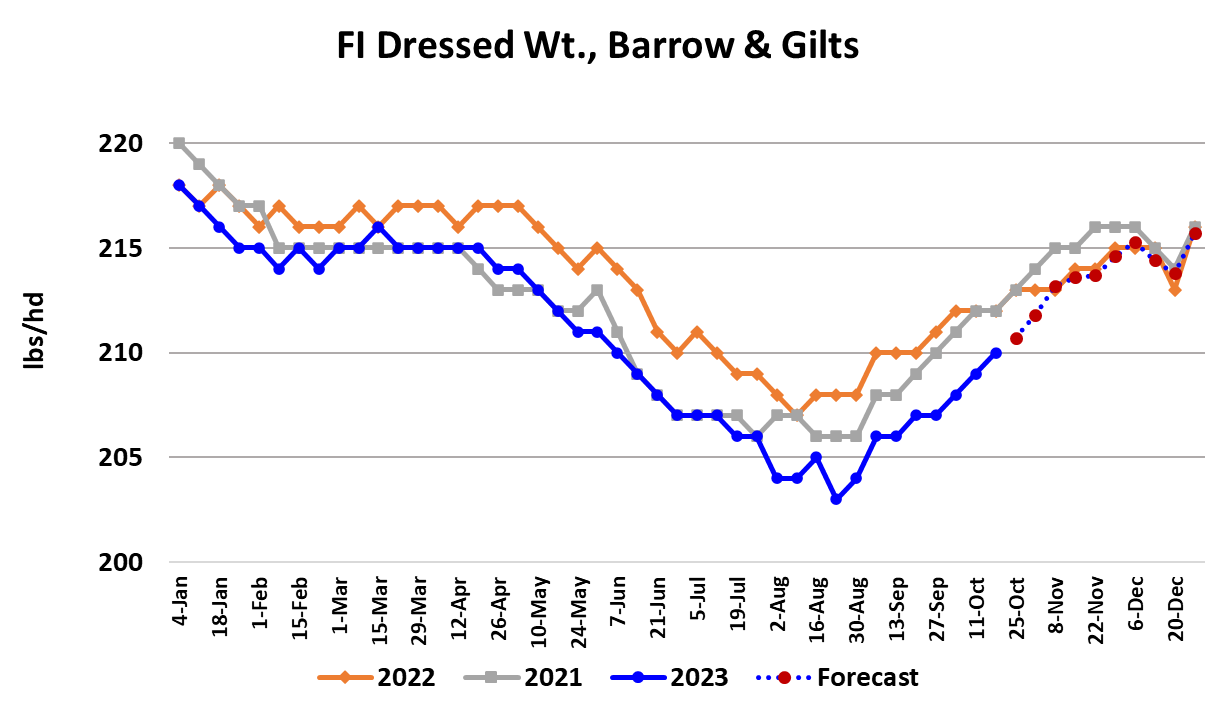

today. Time will tell on that one. Hog weights continue to increase

in normal seasonal fashion, gaining another pound this week, but the DTDS

weights are still relatively low, thus I don’t see much chance of hogs backing

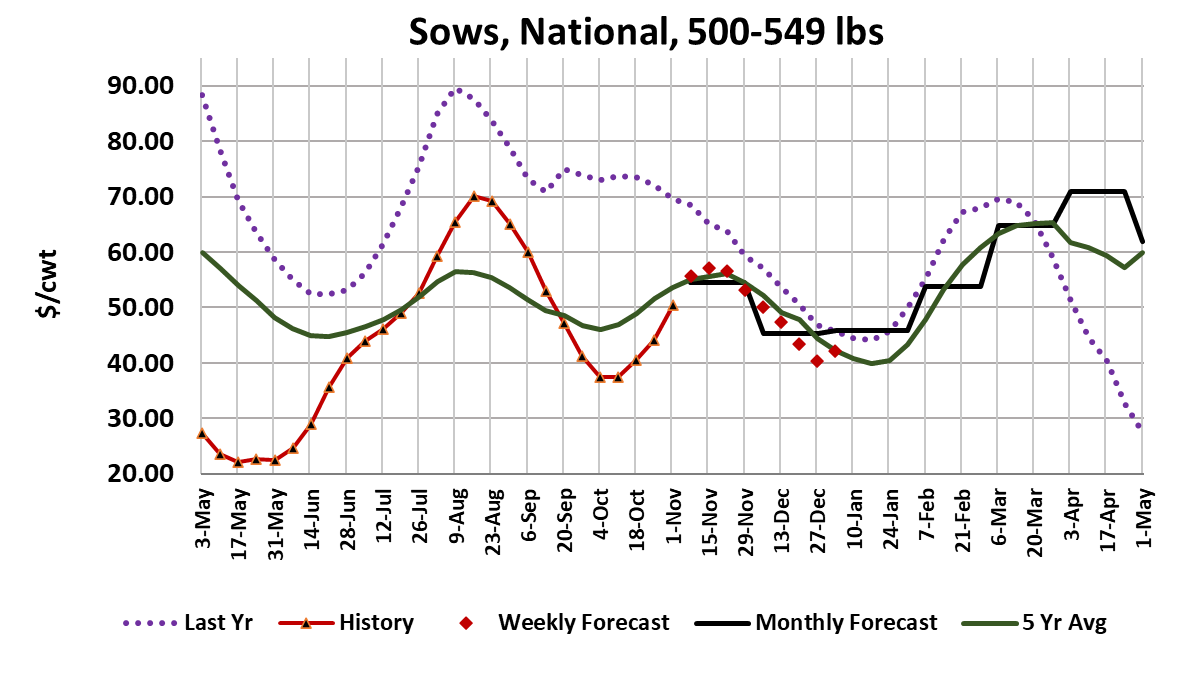

up this fall. Sow kills continue to run larger than expected given the

size of the breeding herd on Sep 1, so that is likely a sign that producers are

still liquidating breeding stock. Interestingly, sow prices are on the

rise. That seems somewhat odd given that more sows are going to

slaughter, but this is the time of year when sow processors are cranking up

production of breakfast sausage to meet increasing demand brought on by cooler

weather. Next week, it will be important to see how well the market

handles this week’s big production. If it can get through the week with

little or no price concession, then I would take that as a very good omen that

points toward some modest demand improvement. Cash hogs are unlikely to

advance given how large the supply is currently, but if they could just hold

steady to slightly lower, that should be considered a victory for

producers. Watch for further gains in the hams to stir up the bulls in

the LH futures once again.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}