Pork Wrap May 6

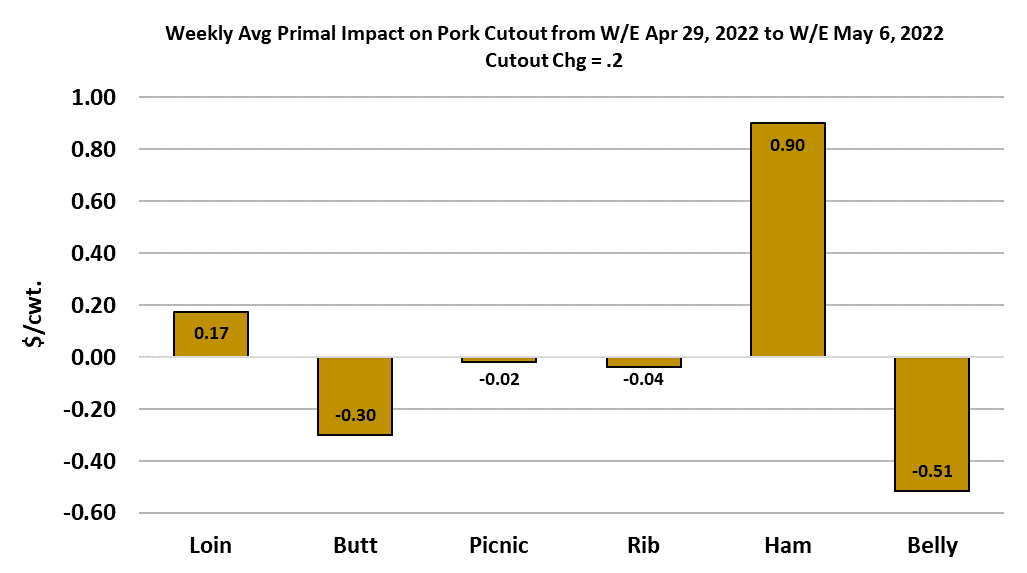

It was steady-as-she goes again this week in the pork complex. The

cutout averaged a mere $0.20/cwt higher than last week and the NDD

cash hog market gained $0.29/cwt. That is about as boring as it gets for

hogs and pork. The one little piece of excitement was a futures rally on

Tuesday and Wednesday in response to a brief upward jiggle in the

negotiated markets and cutout. Bellies also tried to provide some

excitement with a significantly higher quote on Thursday, but it turns out

that was a false flag and the belly primal finished the week lower, losing

about $3 on a weekly average basis. Given that almost nothing is moving

significantly in either the hog or pork markets, futures traders thought that it

might be prudent to remove a little more of the premium in the summer

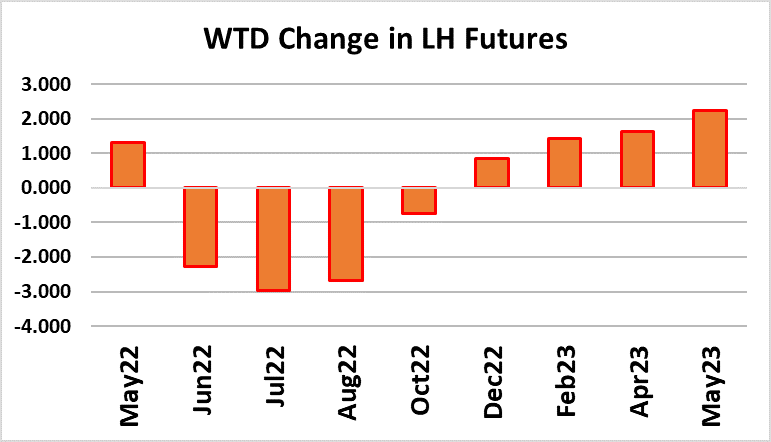

contracts and those lost from $2-3 on the week. That has now pushed the

Jun and Jul contracts below the fundamental forecast, but Aug still looks

several dollars too rich. There is no doubt that there has been a reset of

expectations in the hog and pork complex.

No longer do traders believe that disease issues are going to make the

hog supply so tight this summer that packers will be paying $130 for any

hogs they can find. Instead, it looks like pork availability will be larger this

summer than last due to drastically smaller exports. USDA reported

March exports down 25% this week and that brought the Q1 export total to

20% below last year. I’m forecasting Q2 to be down about 14%. By the

time we get to Q3, we could see some small YOY gains in exports, but that

is only because we will have reached the point where exports really

dropped off last year. Similar to beef, pork imports were up sharply—46%

YOY. So with exports way down and imports way up, it is easy to see

how there could be more pork available in the domestic market this

summer than last year. Another concern that is beginning to creep into

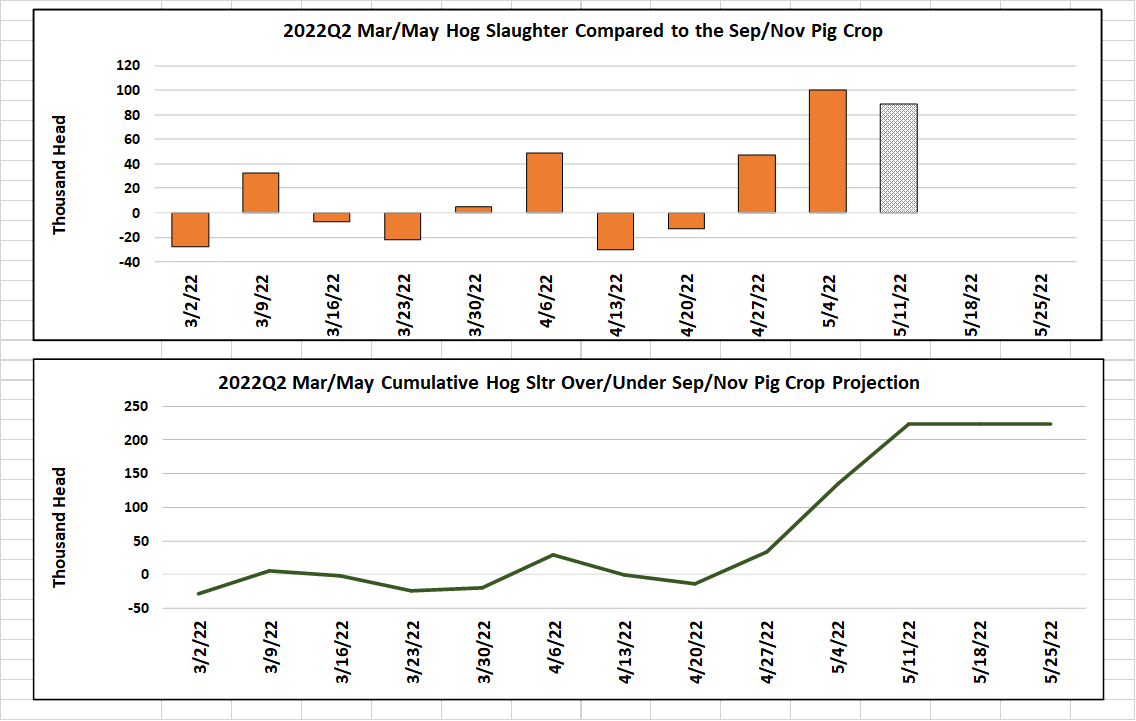

the picture is that it is starting to look like USDA might have underestimated the Sep/Nov pig crop which is now being slaughtered. This

week’s kill came in at 2.42 million head, which was about 100k more than

what the pig crop suggested. Further, it looks like packers could be

planning a similar sized kill next week and if that is the case then the

cumulative over-kill for the March/May quarter would be about 225k.

That’s not a huge miss, but it does make me wonder if we will start to see

consistently bigger-than-expected kills heading into summer. To put things

in perspective, this week’s kill was essentially the same size as the kill in

late March/early April. The normal seasonal pattern would be for early

May kills to be smaller than those. Perhaps packers will revise next

week’s kill downward and we could quickly get back on track relative to the

pig crop, but for now we are seeing production a little larger than expected.

This week I’ve included a chart on the sow kill, which is forecast based on

the size of the breeding herd at the start of the quarter. Here, the positive

and negative bars exactly cancel each other which means the sow kill this

quarter has been almost perfectly aligned with the breeding herd. We are

not liquidating sows or retaining them at this point. Hog weights have not

yet started to decline seasonally, as USDA reported barrow and gilt

weights up one pound to 217 this week. So, the bottom line is that pork

availability next week will be every bit as large as it was this week and thus

we are not yet seeing the normal seasonal tendency toward smaller

production.

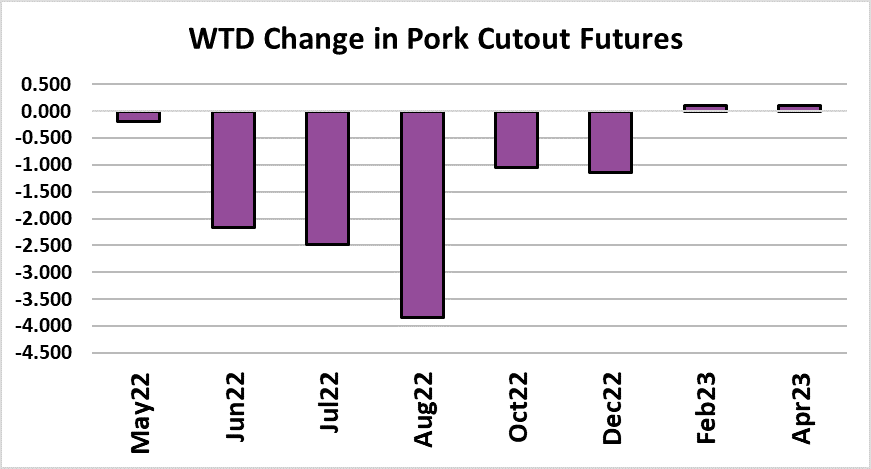

Will the cutout be able to hold its ground without smaller kills? Maybe

not. I’m of the opinion that pork demand is slowly fading as consumers

retreat back down the protein ladder in the face of economic headwinds,

so I am counting on smaller production to give the cutout a little lift

heading into summer. That smaller production may be delayed a

couple of weeks and that could create a bit of pressure on the

cutout, but eventually I think production will decline and price levels

will rise modestly. Right now, the fundamental forecast calls for the

cutout to top around $113 in mid-June. A decent recovery in the bellies

could quickly get us there. I’m calling bellies slightly higher next week,

but bigger gains will probably come around Memorial Day. I don’t think

that we need to fear another big downdraft in the bellies. That said, it

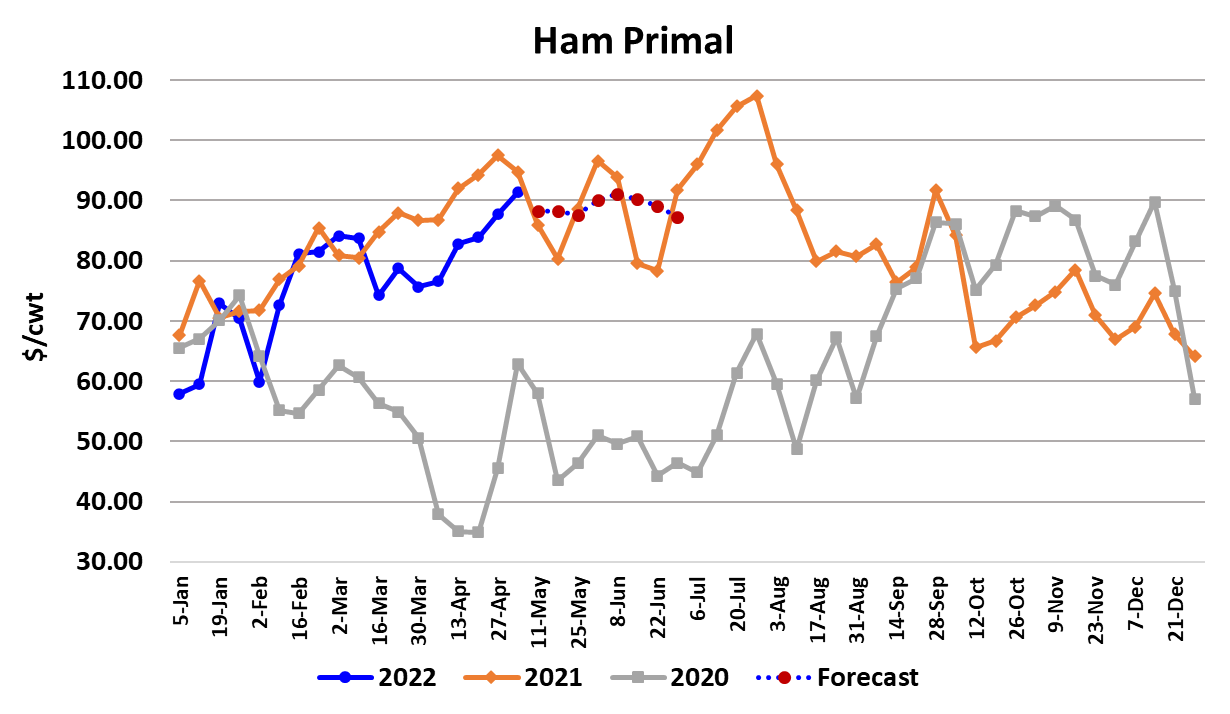

looks to me like the hams could be nearing a top. This week’s

average ham primal was almost dead on with last year, and that was

pretty rich ham pricing.

At this time of year, ham is often purchased for processing into lunch

meat products in anticipation of kids being out of school for summer. I

also get the feeling that Mexico has been a big buyer of hams over the

past few weeks and wonder if they will continue that at current price

levels. It is pretty clear from the pricing data that packers are doing more

ham boning and more product is leaving in boneless form. That alone has

a tendency to lift the ham primal since those boneless products tend to

generate a higher primal value than the bone-in product does under

USDA’s current conversion formula. I’m calling the hams more

sideways to slightly lower in the next few weeks, which means that if

the bellies can generate a reasonable rally, we should see the cutout

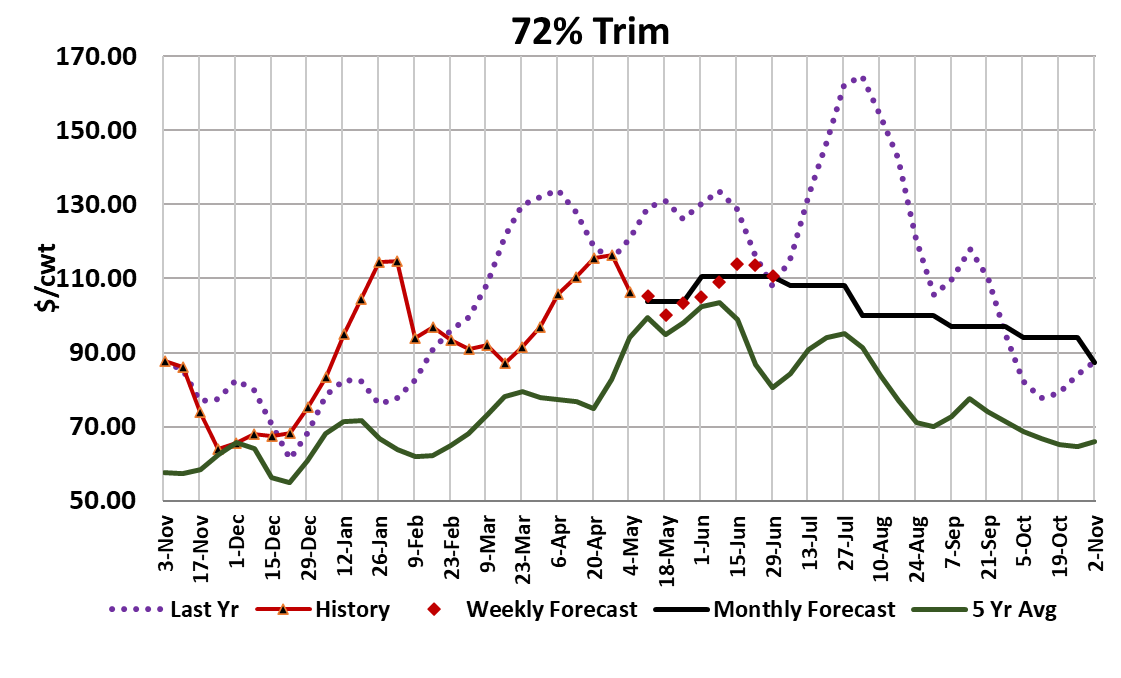

improve. On the bear side of the ledger, I will note that trim markets

seem to have stalled recently and may not be able to muster much

additional upside. Sow prices are also declining rapidly (down $6 this

week) and that can sometimes be an ominous sign for the trim markets

because sausage makers will substitute trim for sow meat when sow

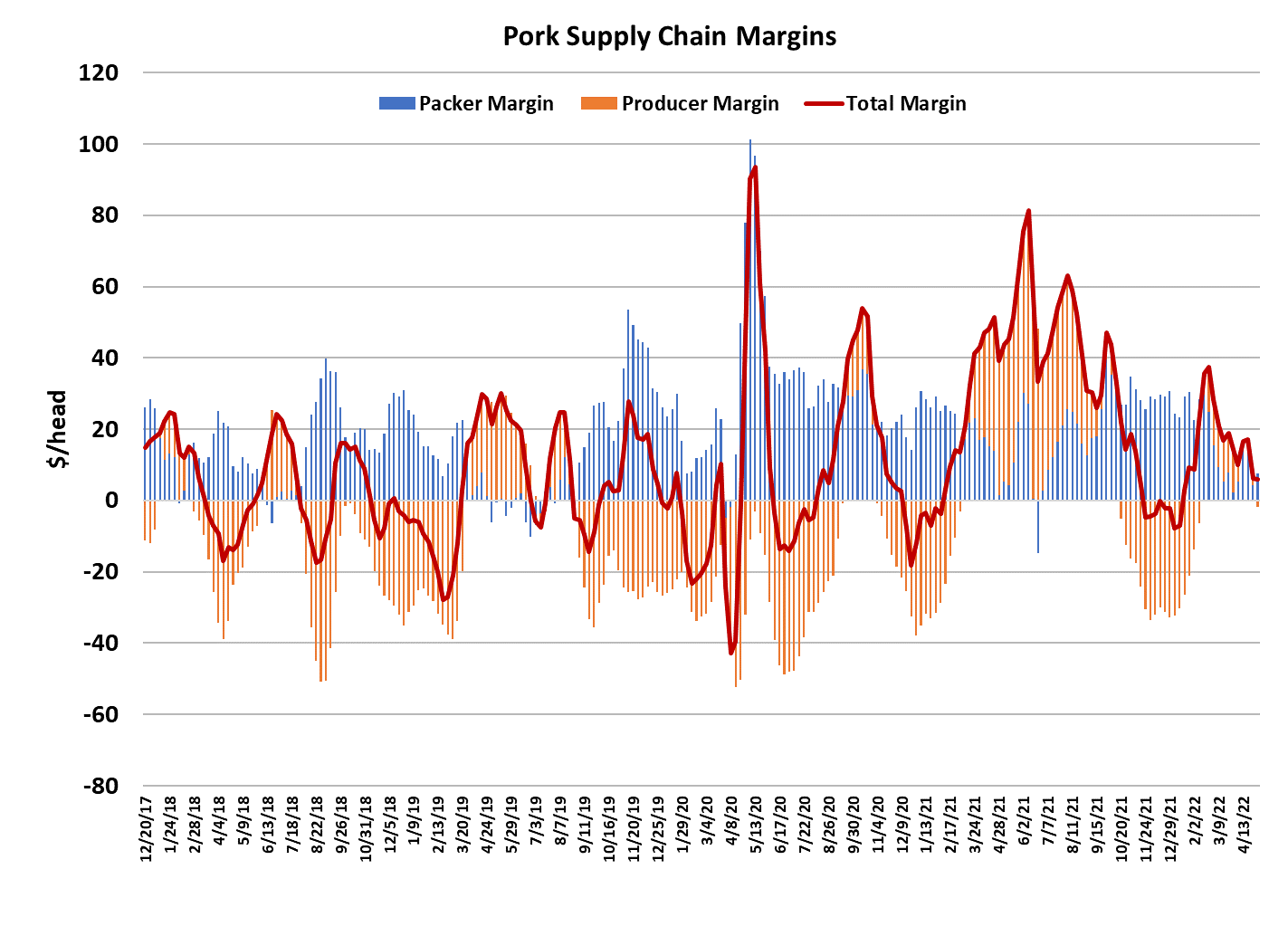

prices are very high. I calculate this week’s packer margin at about $7/

head, which is up a little from last week and pretty typical for this time of

year.

I’m looking for some further erosion packer margins as we move into

summer, but not expecting them to go negative for any length of time.

With the hog supply looking a little larger than expected, I think the LHI

could continue to drift a little lower and so we might see May expiration

very close to $100. If you recall, April expired at $99.98. It is pretty

unusual not to see any gain in the index between April and May

expirations and I take that as a sign that demand has eroded somewhat in

recent weeks. Right now, I’m looking for Jun expiration around $108, but

it could be several dollars lower than that depending on how

demand plays out. June expiring below April or May would be super

unusual, but I think the odds of that happening are better this year than

any year prior (excluding 2020, of course). Next week, watch the

bellies for signs that the bottom is in and the hams for topping action.

The hog and pork complex seems a bit boring right now, but when that

happens it is usually just the calm before a coming storm.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}