Pork Wrap May 5

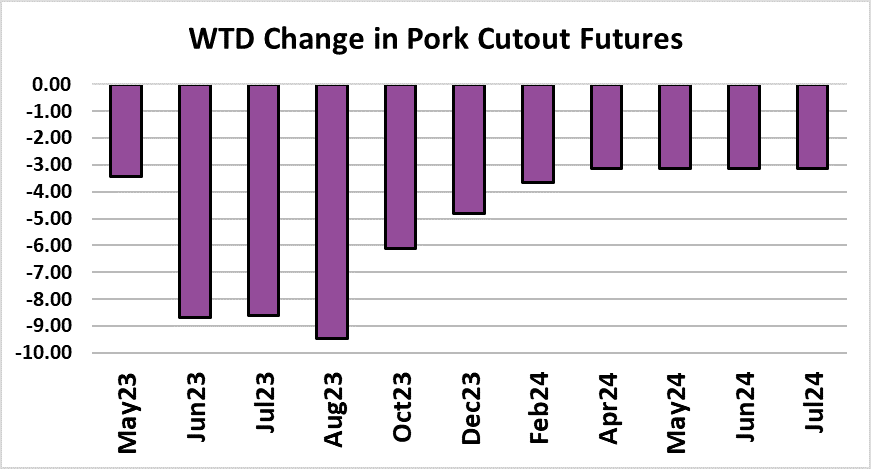

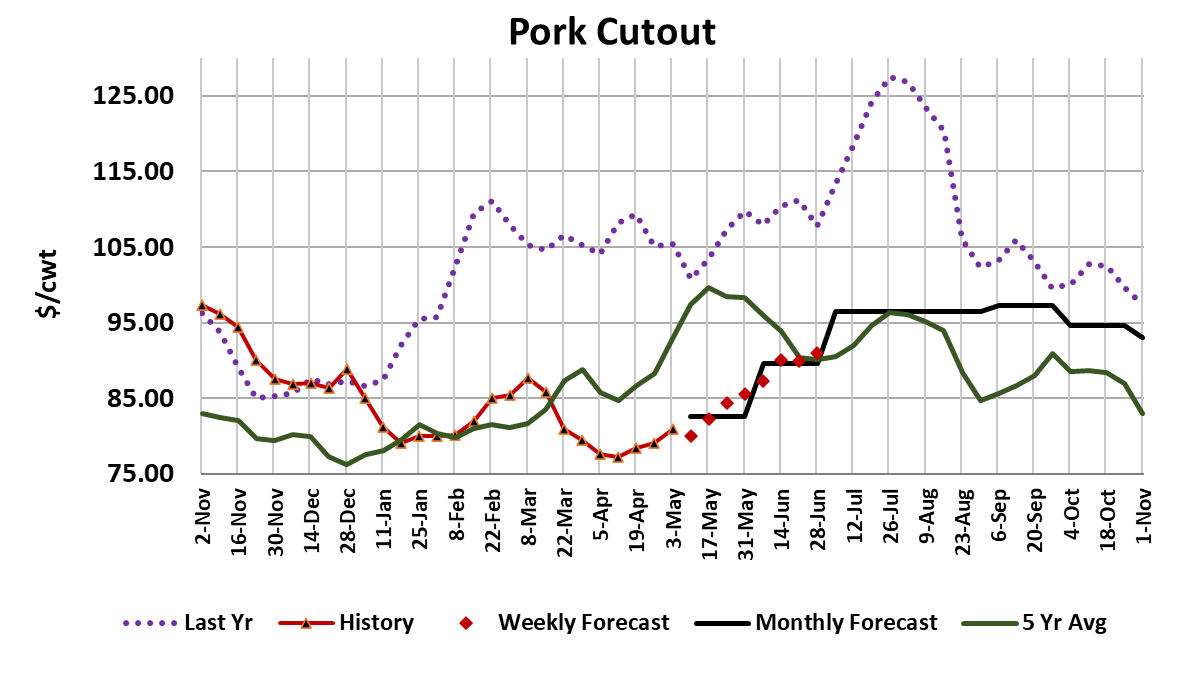

The pork cutout continued to

work slowly higher this week, up $1.80/cwt. on a weekly average basis.

Small week-on-week changes in the cutout have been a persistent feature of this

market since January. Today the futures bulls showed their

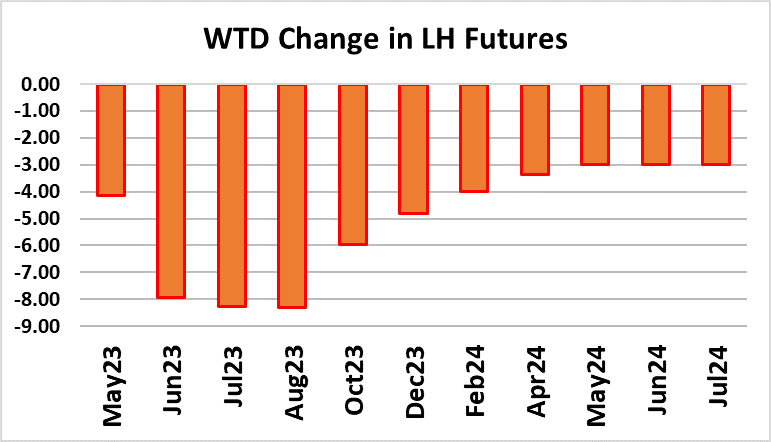

frustration with this slow motion pork market by trashing the entire futures

curve. They had been pricing the summer futures a good $10-12/cwt. over

the May contract, but with the cutout only inching upward a little every week,

it made traders question whether or not those big premiums are justified.

A big part of the problem is that we just haven’t seen much in the way of

seasonal reduction in kills. That is normally what drives prices quickly

higher in the late spring and early summer. This week’s slaughter came in

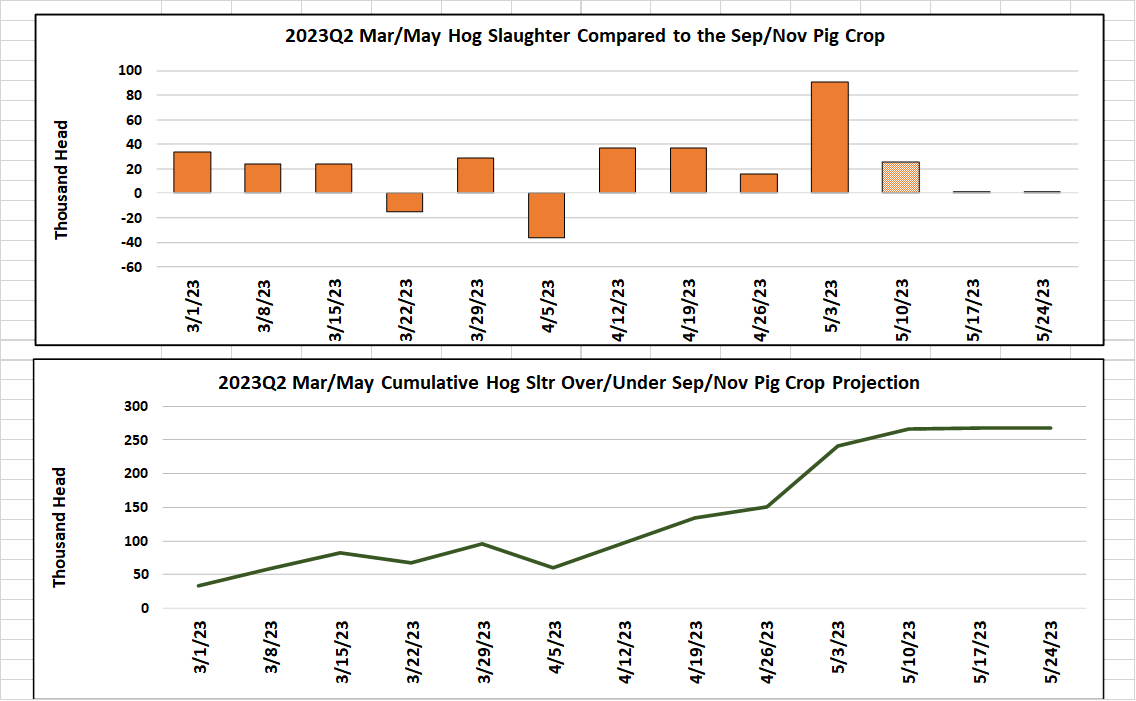

at 2.45 million head, some 60k more than last week. So, you can see the

problem. There are just more hogs than expected for this time of

year. Relative to the (revised) pig crop, this week’s over-kill amounted

to 90k head. The big kill means lots of pork that needs to clear the

market next week as futures participants will be eyeing the expiration of the

May contracts. The cash hog market performed better this week, with the

WCB cash market adding $3.17/cwt. on a weekly average basis and the NDD market

adding $3.33/cwt. However, the gains in the negotiated hog markets

stalled late in the week, which raises the risk that they might stall or even ease

a bit next week. It sure doesn’t look like we are running out of hogs, so

I don’t see a lot of reason for a big rally in the cash market. Most of

the strength seems to be originating in the WCB region, similar to what we saw

last summer and early fall. Tyson should have its Madison, Nebraska plant

back online within a week or so and it will be interesting to see how that

impacts the WCB negotiated market. The FI carcass weight data for

barrows and gilts was unchanged again this week, but soon it should start to

show weights declining seasonally. The DTDS weights are making it look

like producers have done a good job of moving hogs and thus keeping the

potential for a backlog relatively low. Warmer weather is on tap for the

Midwest in the next couple of weeks, so that should help weights get started

lower. The crux of the problem in the hog and pork complex right now is

that there are just too many hogs for the level of consumer pork demand.

Retailers are contributing to that problem by keeping retail pork prices

excessively high and grabbing a big share of what little margin is available in

the system, but that is their prerogative and if producers want to shift the

balance of power back in their direction, they need to really cut back on hog production.

That takes time to manifest as smaller pork production, but the longer they

wait to scale back, the longer the financial pain will persist. Maybe

some producers are thinking that summer will bail them out like it has the past

2 years, but that looks like a long shot at this point. Some may think

China is going to bail them out. Again, wishful thinking. On

Friday, sow prices were quoted close to $25/cwt. The last time they were

that low was back in September 2020, when producers were actively liquidating

sows in response to the pandemic shock that hit a few months before.

Perhaps these low prices are an early indication that producers are liquidating

once again, but so far we haven’t seen anything unusual in the sow slaughter

data. Sow slaughter seems to be tracking very close to where we would

expect it to be given the size of the breeding herd on March 1. A better

indication will come when we calculate the number of gilts retained as breeding

replacements from the data on USDA’s next Hogs & Pigs report (June

29th). It could be that producers are sending the usual

percentage of sows to slaughter but just not replacing them at the normal

rate. Time will tell, but clearly something needs to change.

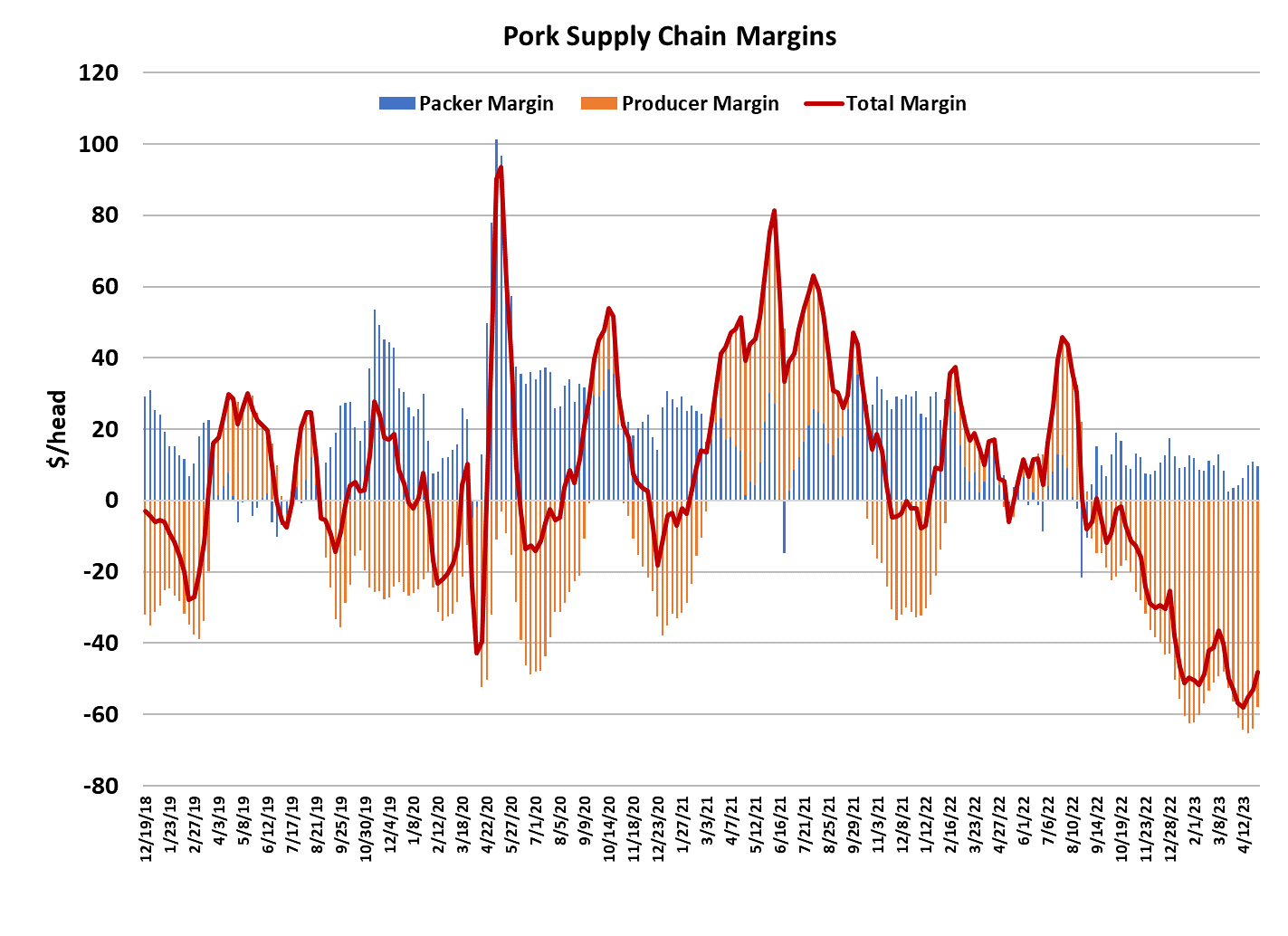

Producer margins this week were -$57/head. That is not what they have

come to expect in the month of May. Packer margins were just a tad under

+$10/head, which is actually pretty good for this time of year. The

relative abundance of hogs this spring has allowed packers to run at decent

capacity utilization without having to butcher each other in the cash hog

market. The combined margin continues to work slowly off of the record

low it posted a few weeks back, so I take that as a sign that demand is slowly

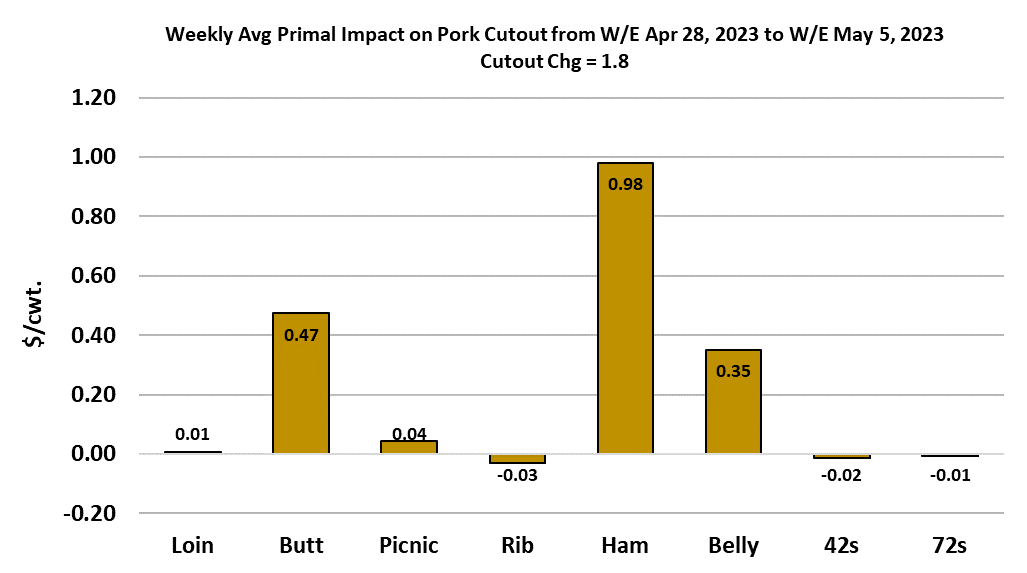

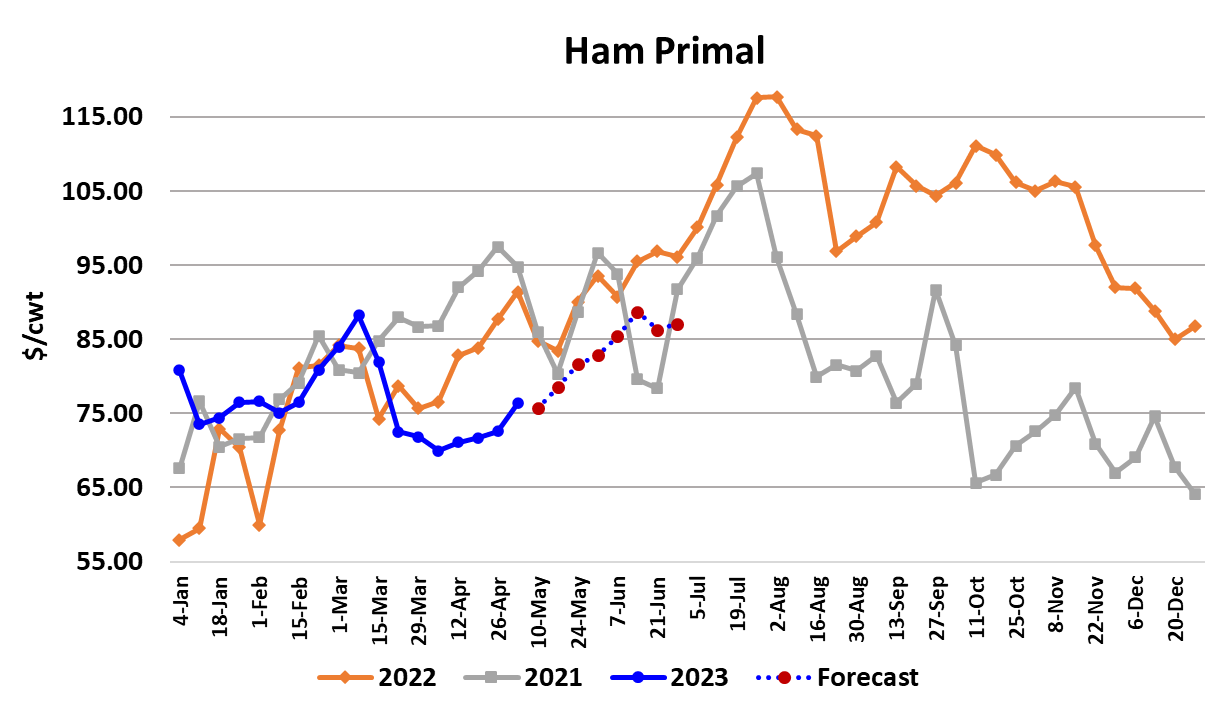

improving. This week, the hams were the biggest contributor to the gains

in the cutout. The normal seasonal pattern for hams points towards higher

prices at this time of year and I’ve built that into the forecast, but maybe a

bit too aggressively. Just watching the daily price action in the ham

market makes me think that they are about to catch and take a decent leg

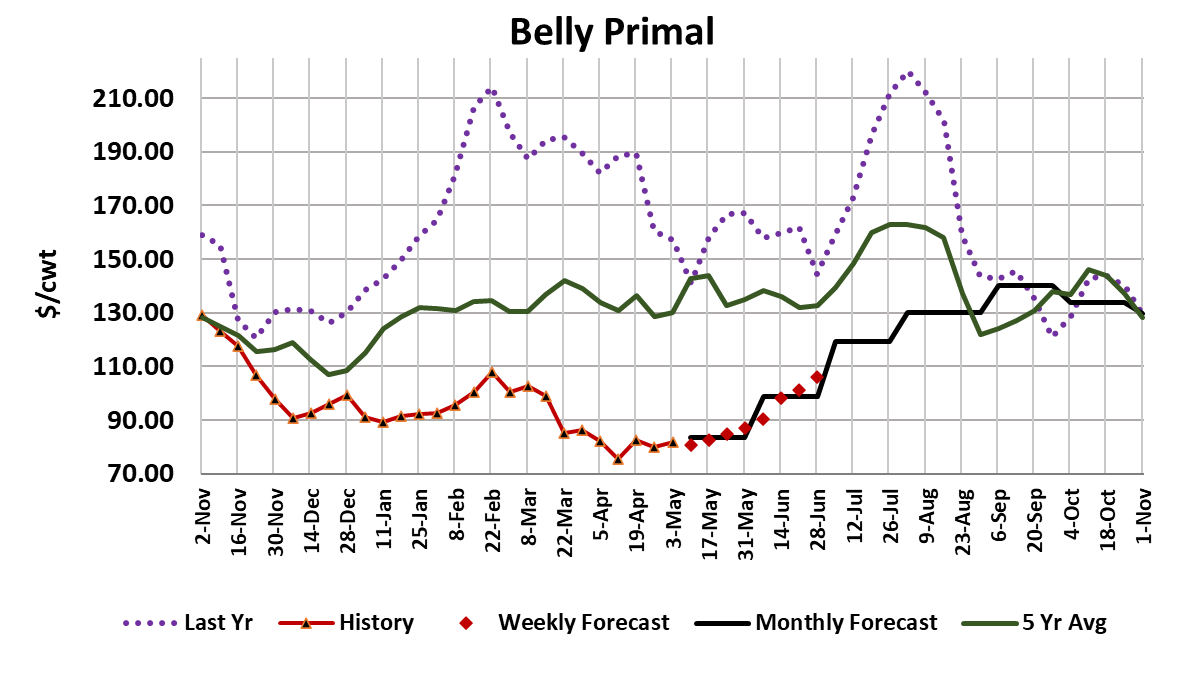

up. They certainly aren’t getting much assistance from the bellies.

Consumer demand for bacon seems pretty weak at present. Perhaps that will

change once schools let out for summer and families hit the road for vacation,

but large cold storage stocks of bellies will probably limit the upside

potential in early summer. The forecast has almost every primal

moving higher over the next few weeks, more based on the seasonal reduction in

supply rather than any big new surge in demand. Still, week after week I

find myself lowering forecasts because nothing is living up to

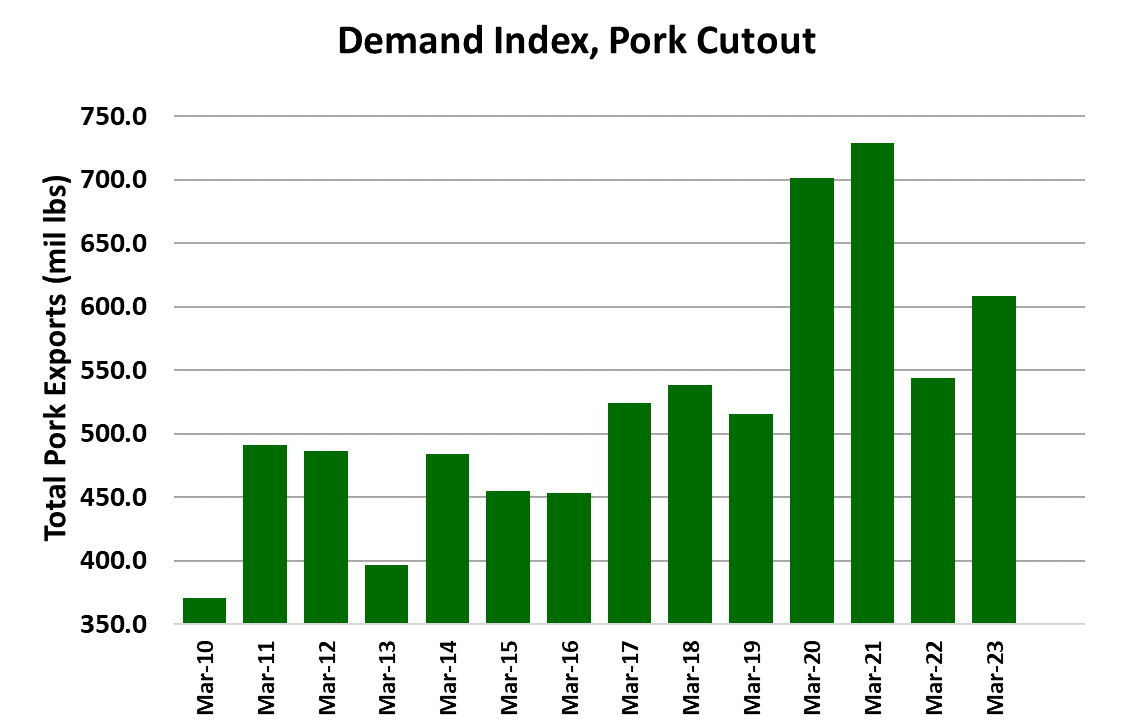

expectations. International trade is one area where there has been some

good news lately. Both new sales and shipments have looked strong in

recent weeks. Low pork pricing in the US is attracting attention from

overseas buyers. ERS released the official export numbers for March this

week and it showed an 11.8% YOY increase. That was a good bit stronger

than what I had been carrying, so made some pretty significant upward revisions

to the export forecasts for the rest of 2023 and into 2024. That change

raised the fair value for most of the futures contract months and thus makes

the deferred futures look even more undervalued this week compared to

last. This week the market returned to Earth after getting head-faked

last week by sudden advances in the negotiated hog market that made traders

believe that the summer rally was full-on. I suspect that traders will treat

future advances more cautiously.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}