Pork Wrap May 31

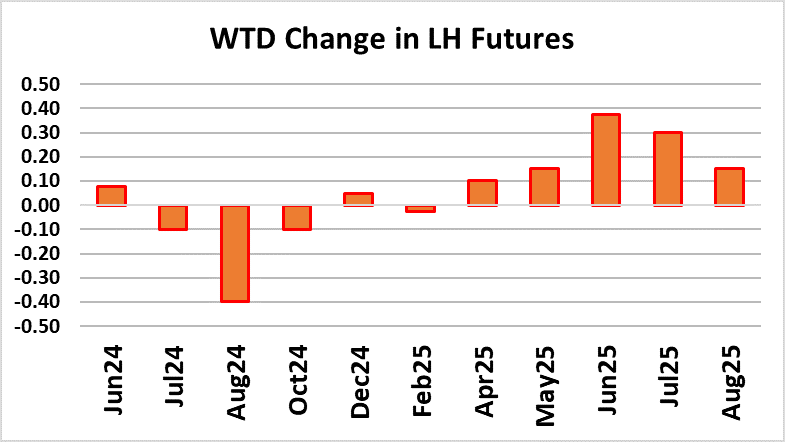

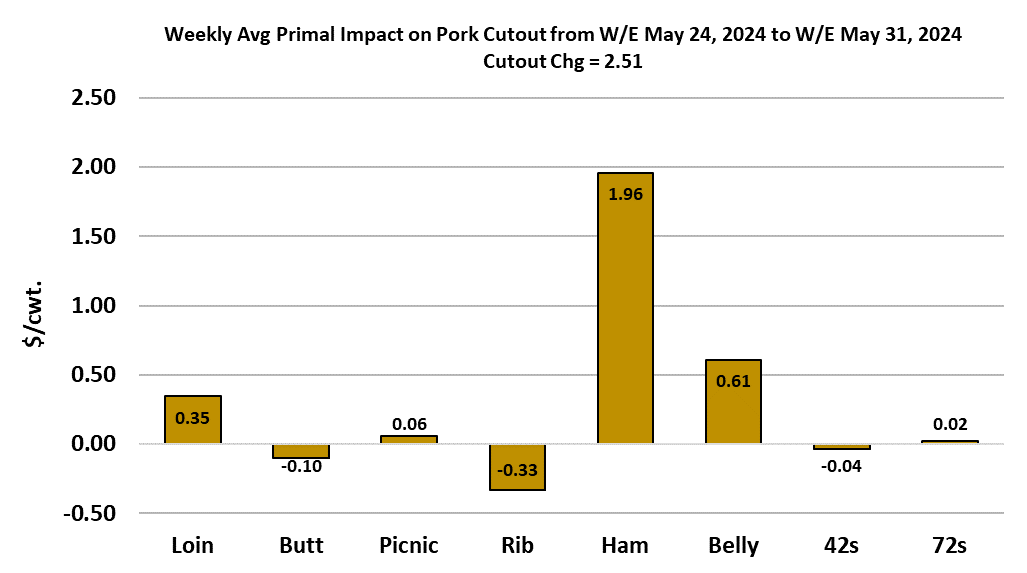

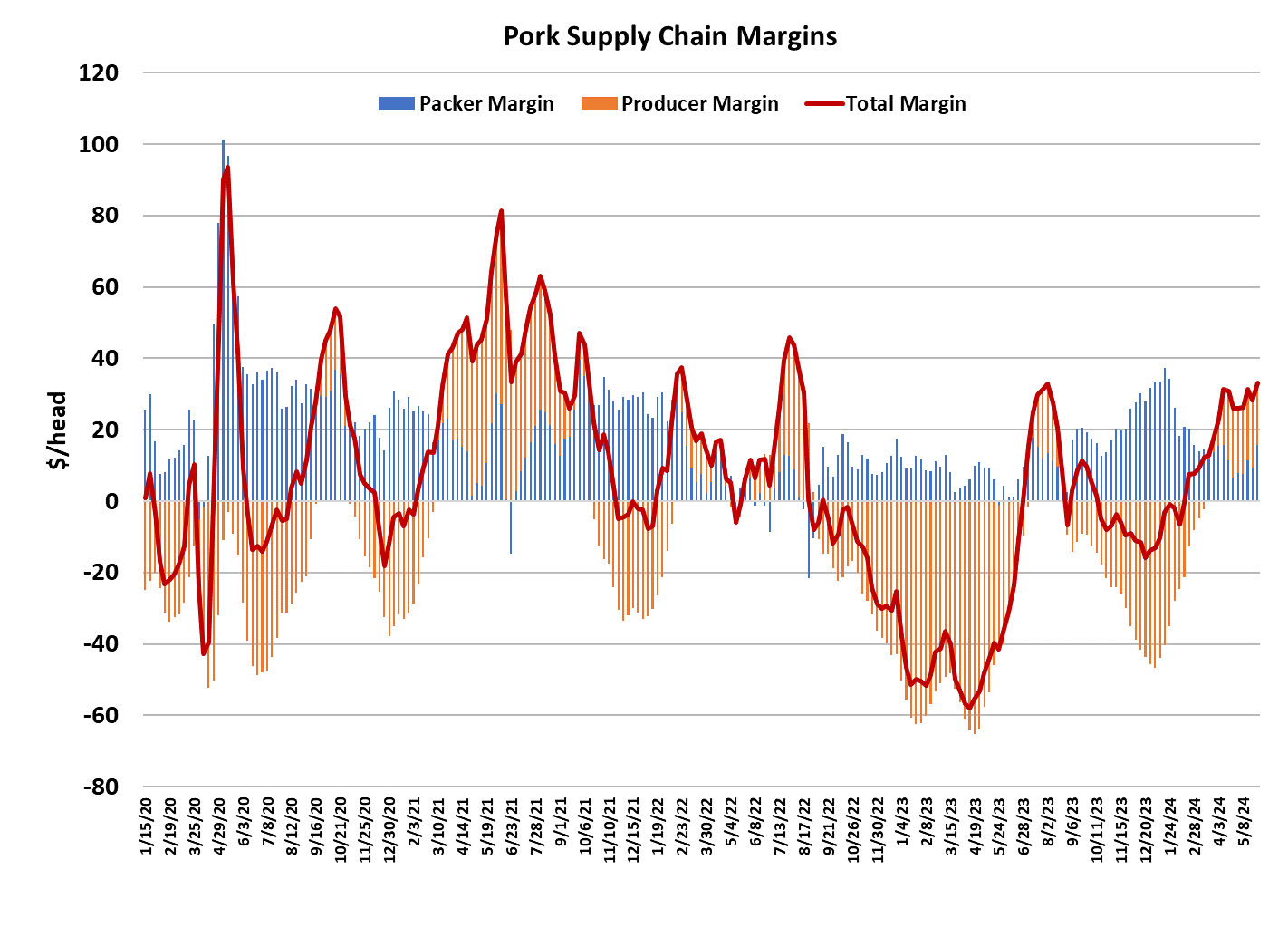

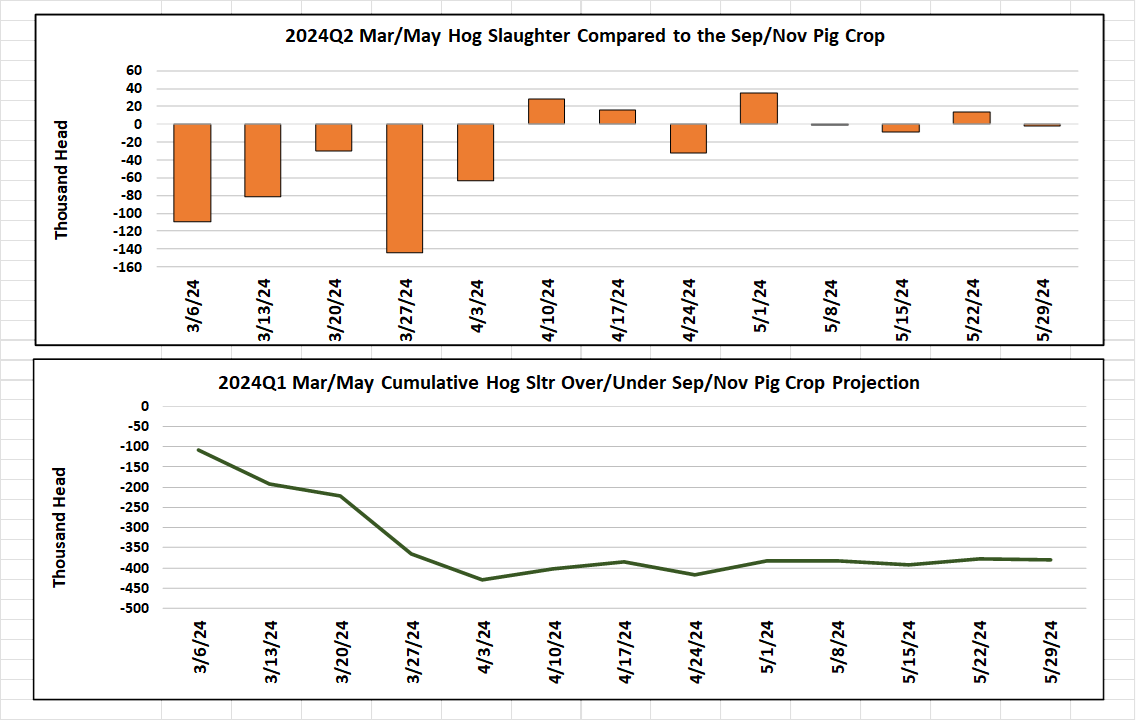

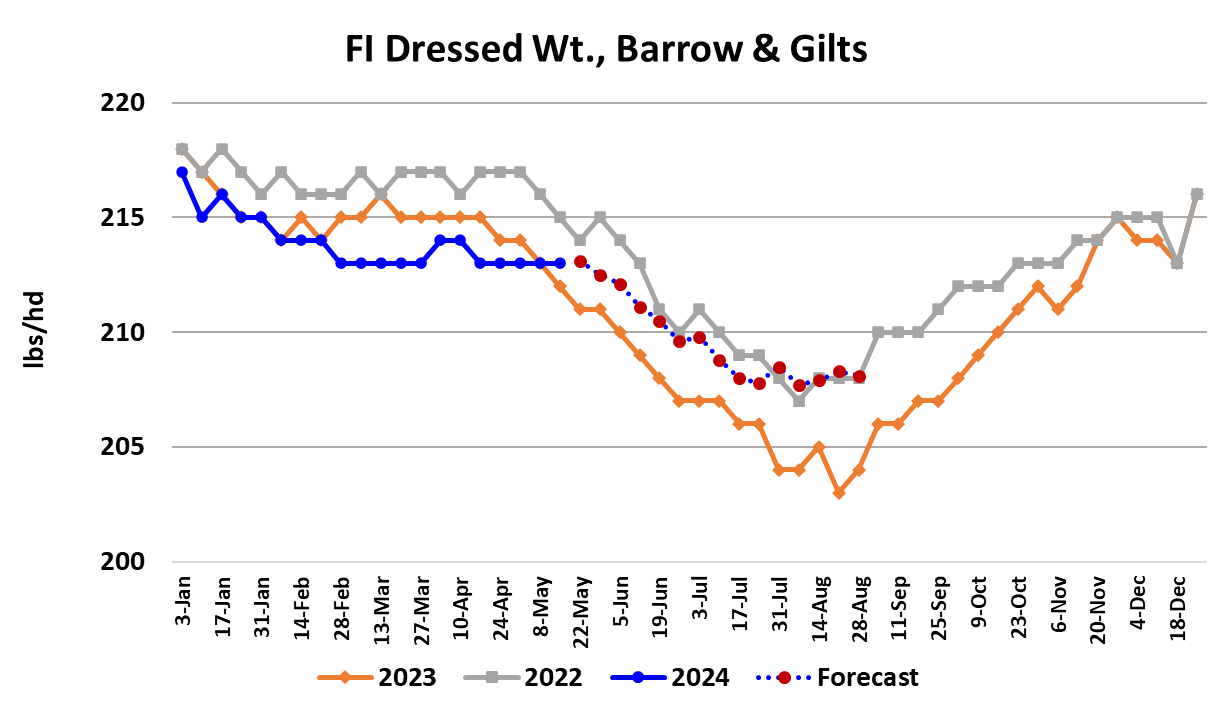

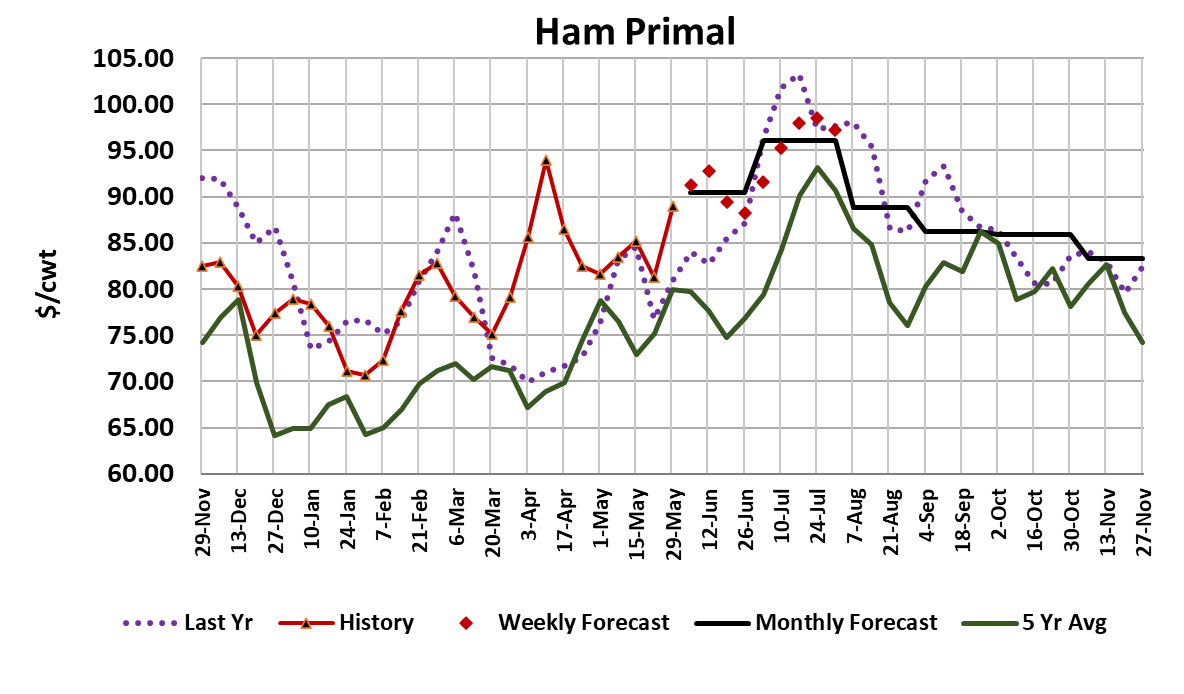

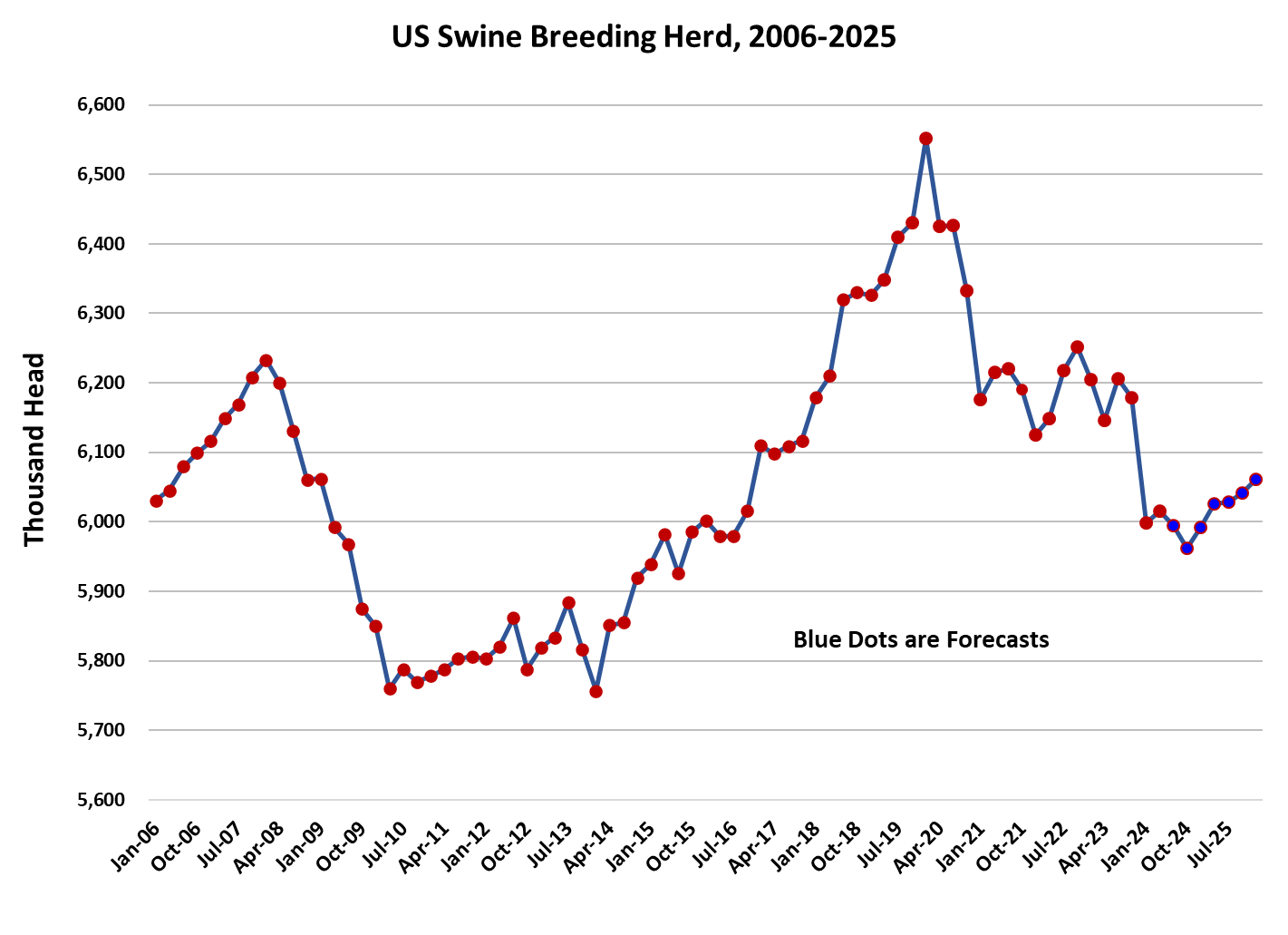

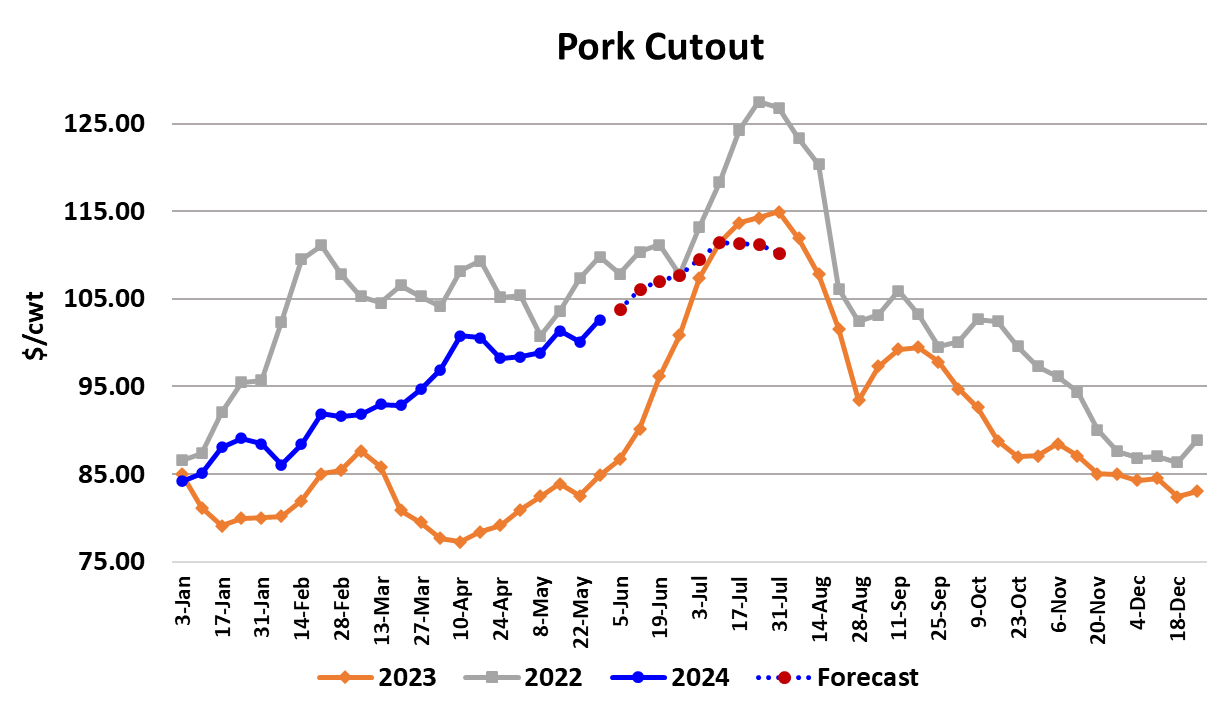

Cash hog prices were dead in the water this week as the NDD market only added $0.31 on its way to averaging $87.79 for the week. The cutout, however, showed some signs of life gaining $2.51 to average $102.59. The upward movement in the cutout was driven primarily by the hams and, to a lesser degree, the bellies. The ham move was impressive, up nearly $9 on the primal, and a bit of a surprise since the primal only posted one lower week before moving higher again. The increase was large enough that I don’t think it was primarily driven by the short kill, but rather by stronger ham demand. The other piece of good news is that the bellies are finally starting to work higher after a long sideways stretch. The belly primal gained $4 this week and appears poised to keep tracking higher as we move through June. The upward movement in the cutout breathed new life into the futures, with the Jun contract finally posting a couple of up days after a long string of red ones. However, as encouraging as the cutout was this week, there are still concerns about the number of hogs poised to come to slaughter and what that means for the negotiated markets in the next few weeks. Packer margins swelled to nearly $16/head this week due to the fact that the hog market didn’t move in conjunction with the cutout’s gains. That is generally a sign of strong packer leverage caused by more hogs than expected. This week’s holiday shortened kill came in at 2.16 million head, but slaughter is projected to rebound back above 2.4 million head next week. Going forward, if USDA’s estimate of the Dec/Feb pig crop was correct, it is unlikely that the non-holiday weekly kill totals will get much below 2.35 million head per week during June and July. In August, weekly kills could reach 2.55 million head according to the pig crop. That means that there is not likely to be much further reduction in slaughter levels to push prices higher, so demand will be forced to carry the cutout higher if it is to advance. The relative abundance of hogs on the ground this summer should also keep packers in a strong position when fleshing out their kill schedules with hogs picked up in the negotiated market. As a result, I’ve adjust packer margins upward for the balance of the summer and really doubt that we will see any weeks where packer margins go negative. Of course, it is always possible that a heat wave could descend on the Midwest, driving hog weights lower and thus providing more help from the supply side than currently envisioned. However, the weather forecast for the next couple of weeks looks rather mild so that isn’t an immediate concern. In fact, hog weights are starting to get a little concerning themselves because they haven’t yet shown any signs of making the normal seasonal trek lower. The FI barrow and gilt weights reported this week were steady once again and we are several week past the point where weights should have started easing. Perhaps hog producers are following the example of cattle producers and making animals heavier because the cost of feed is so much lower than it has been in the past couple of years. In any case, if weights don’t start declining soon, that is going to raise alarm bells about larger-than-expected production this summer and thus lower-than-expected pricing. Near the end of June, USDA will provide us with the results of another Hogs & Pigs survey and my early pass through the numbers suggests that the total swine herd could come in 1-2% larger than last year and the March/May pig crop could be close to 1% bigger than last year. I’m afraid futures traders might react very negatively to increases of that magnitude after all of the talk about needing to shrink the herd. Interestingly, I look for the breeding herd to be down 3-4% YOY, but strong increases in productivity (pigs per litter, in particular) has kept the number of market hogs strong even though the breeding herd has been shrinking. So, we need to add the possibility of an unfriendly Hogs & Pigs report to our list of concerning factors in this market. At the moment, hog producers might not share similar concerns because their margins are close to $18/head and have been in the black since the middle of March. That might cause them to let up on the brakes with respect to their herd reduction efforts. Perhaps the best prospect for better pricing in the hog and pork complex comes from the demand side of the market. Demand readings this spring, while better than last spring, are well below historical norms and if demand can move back toward average levels later this year, that would do a lot to offset the impact of big hog supplies. I’ve got demand during the second half of 2024 modestly higher than in 2023, but still about 4% below the long run average and it leads to a average cutout across Q3 and Q4 that is 4-5% stronger than last year. If 2025 brings even better demand improvement, but still below the long-run average, and coupled with continued production restraint on the part of producers, that could easily lead to a situation where the cutout is over $100 for two-thirds of the year. None of that requires any heroic assumptions, just that producers keep some semblance of discipline with respect to herd size and demand keeps working back toward “normal” levels. Next week, look for further strength in the hams and bellies to keep the cutout moving higher, but don’t be surprised if the negotiated hog market continues to languish.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}