Pork Wrap May 3

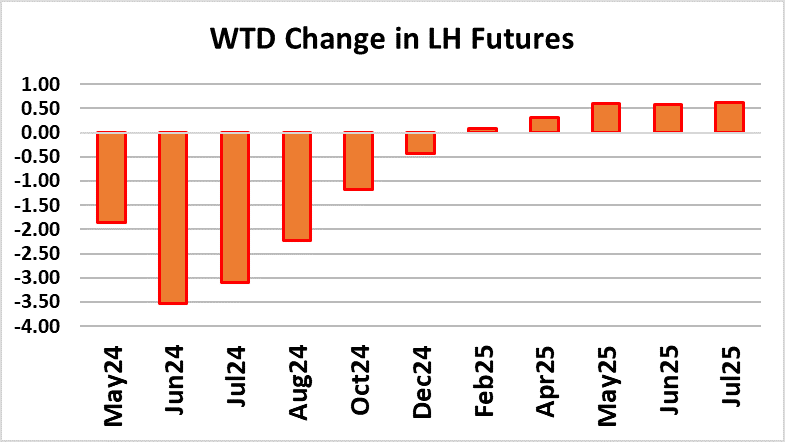

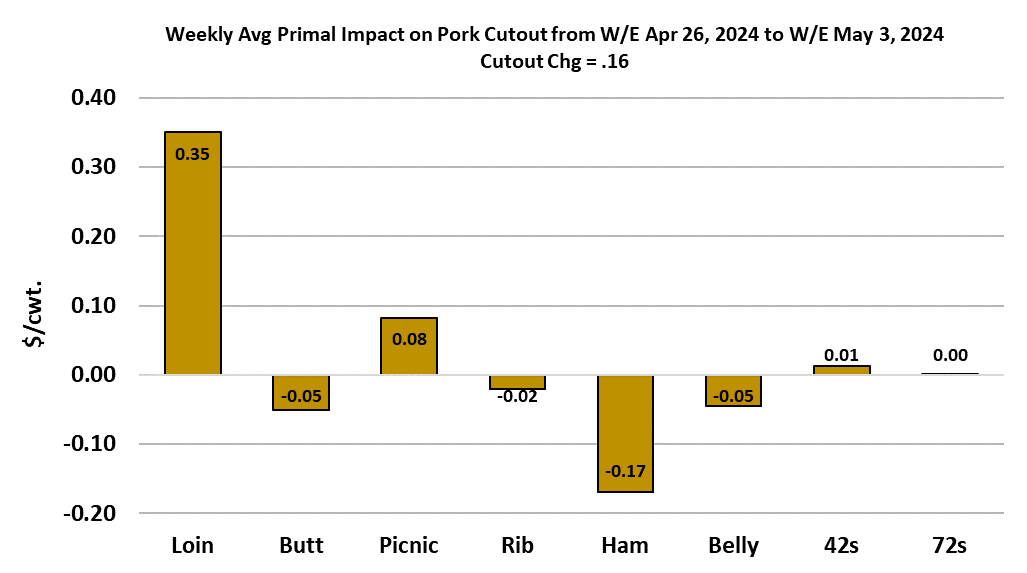

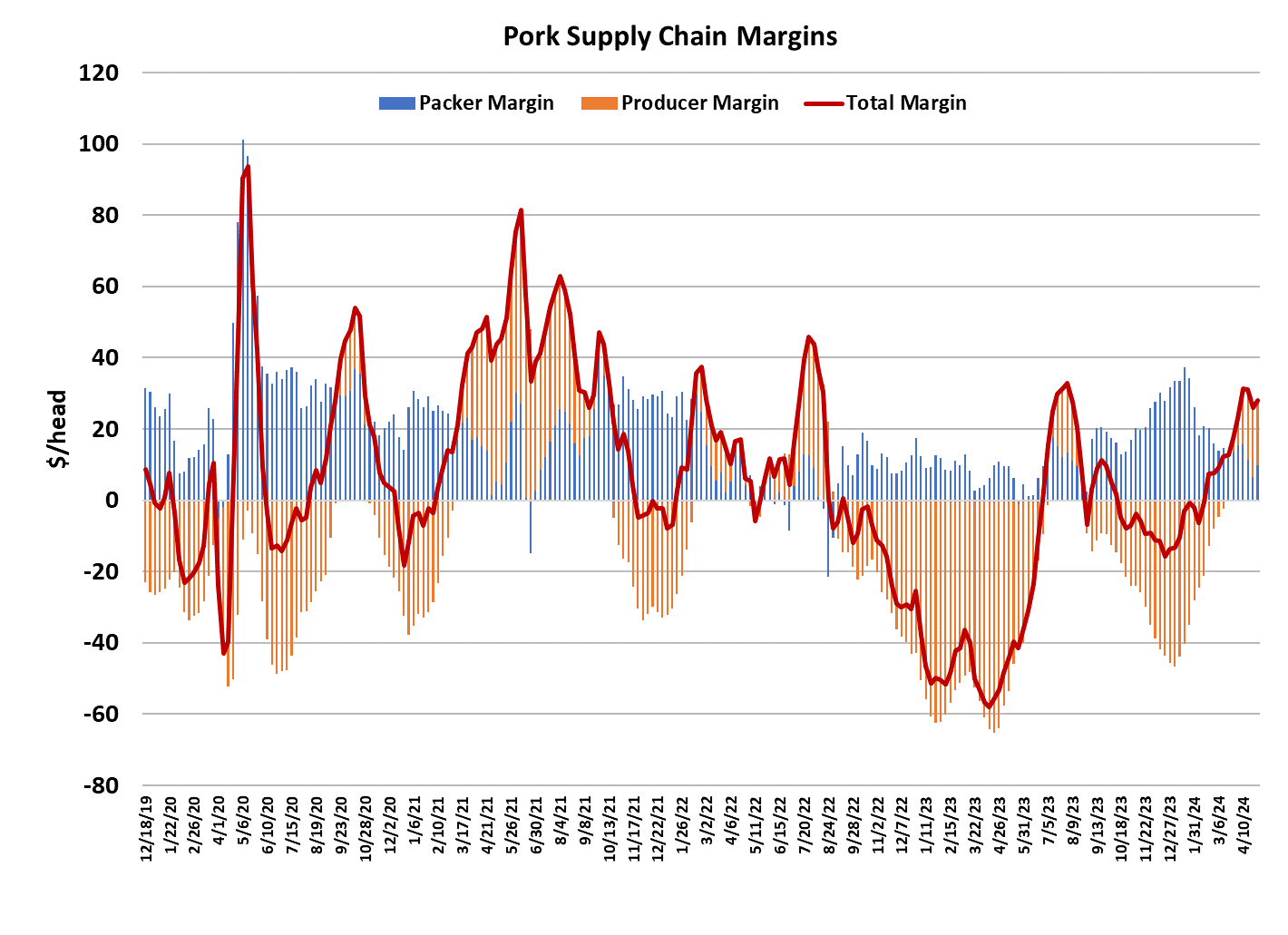

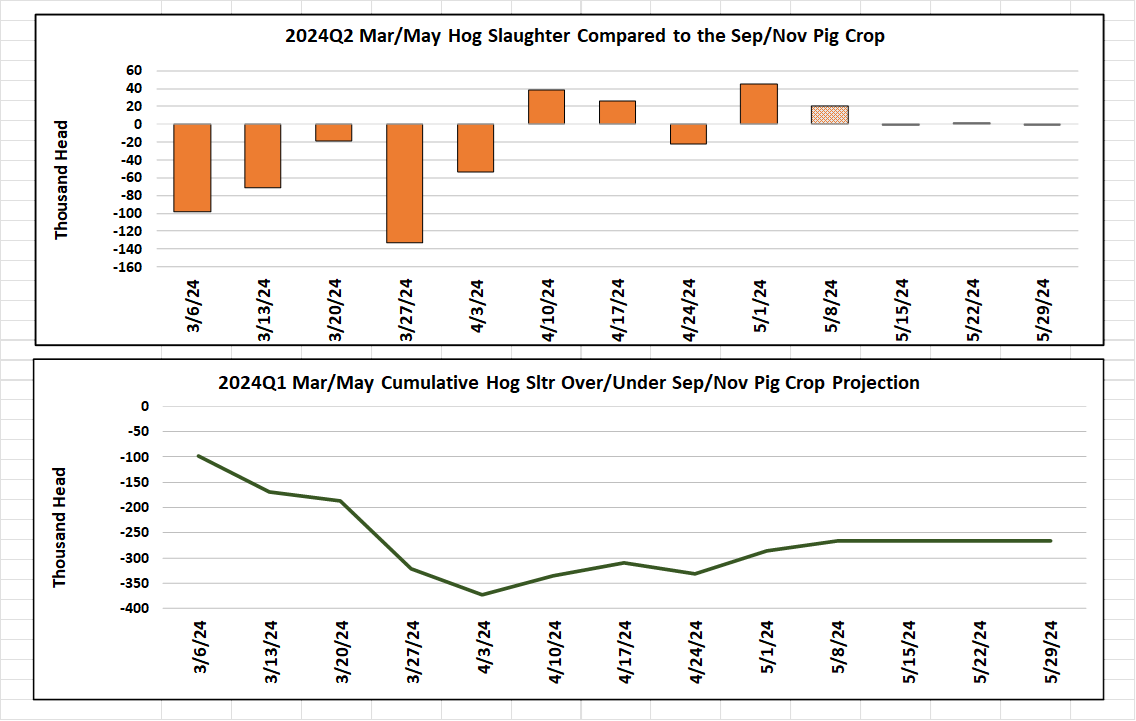

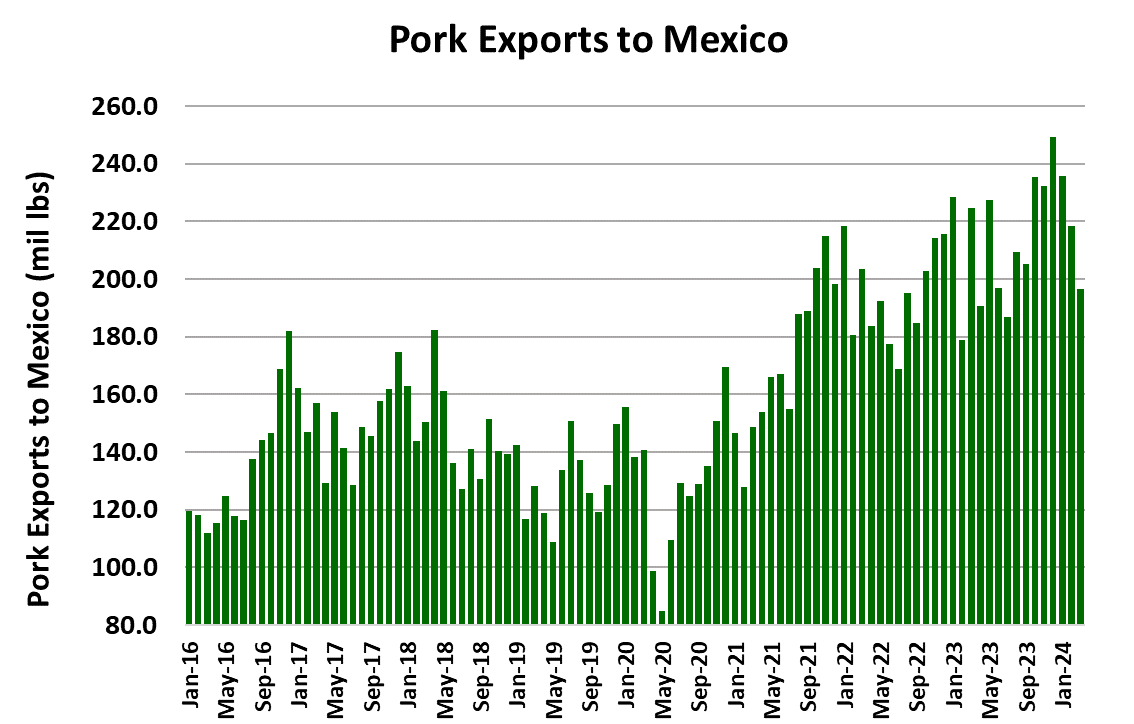

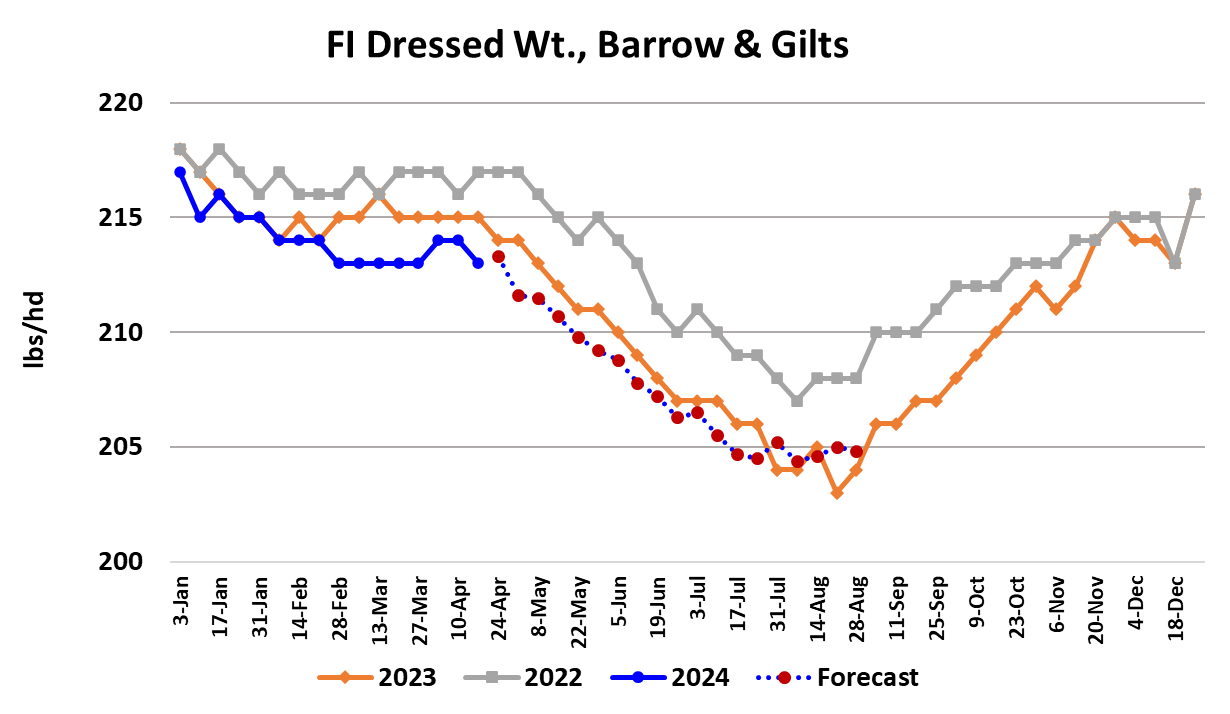

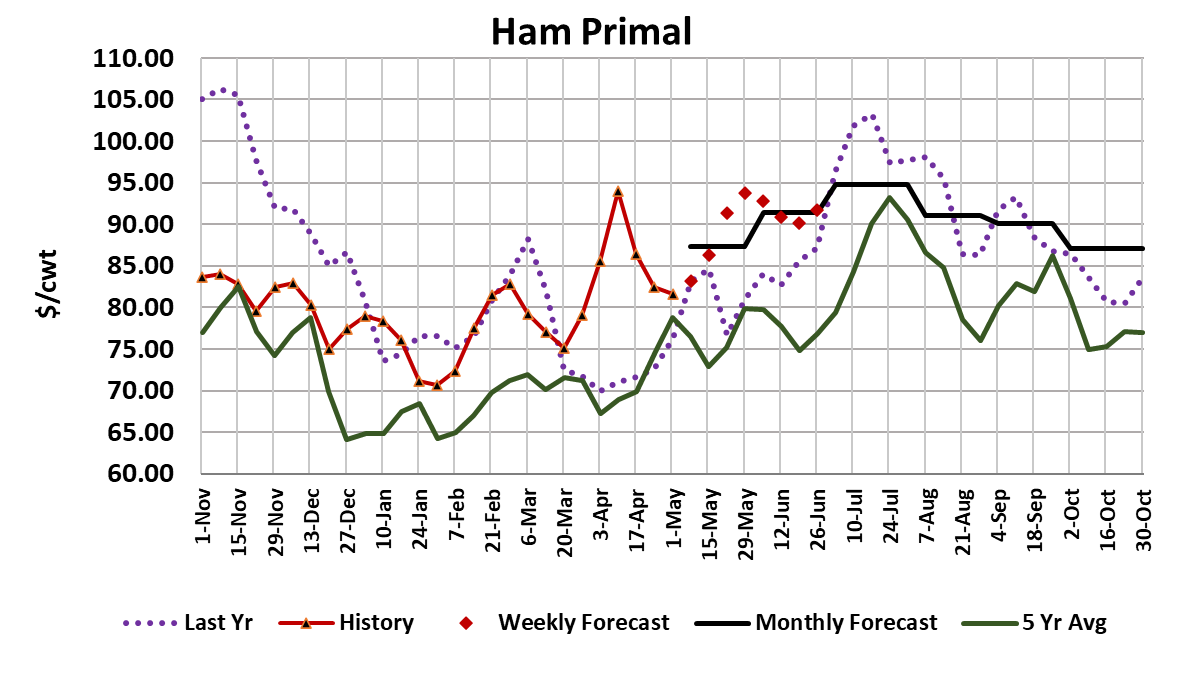

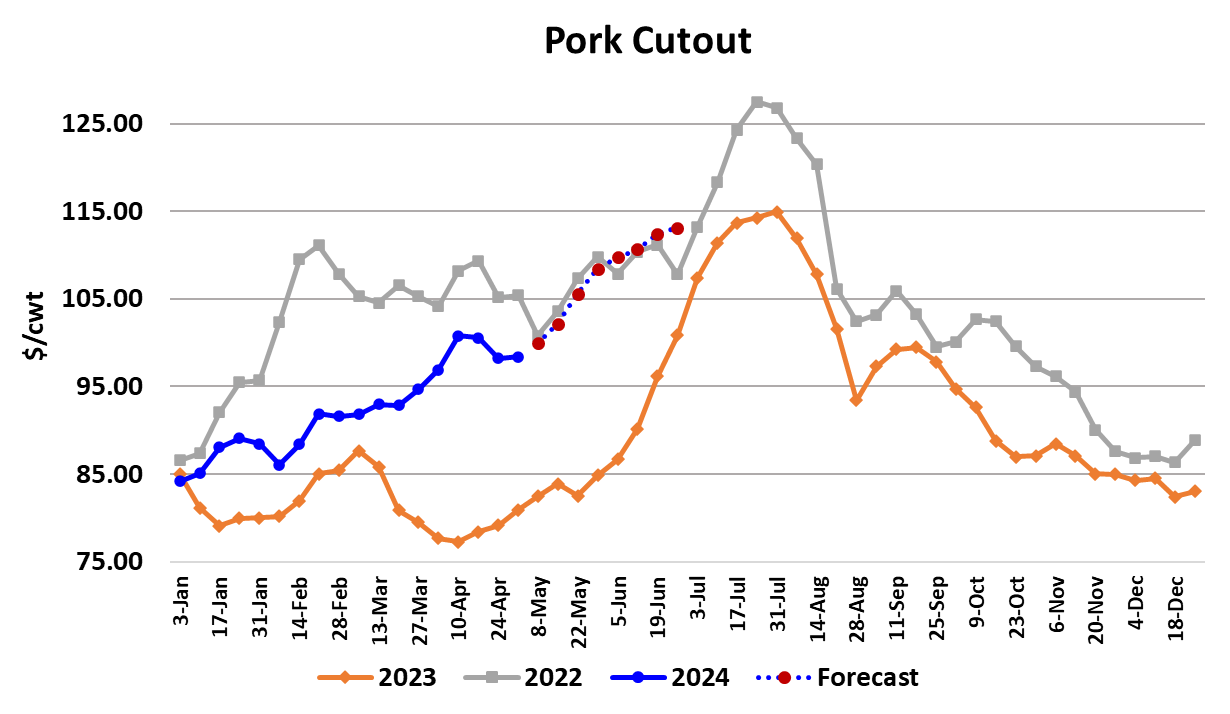

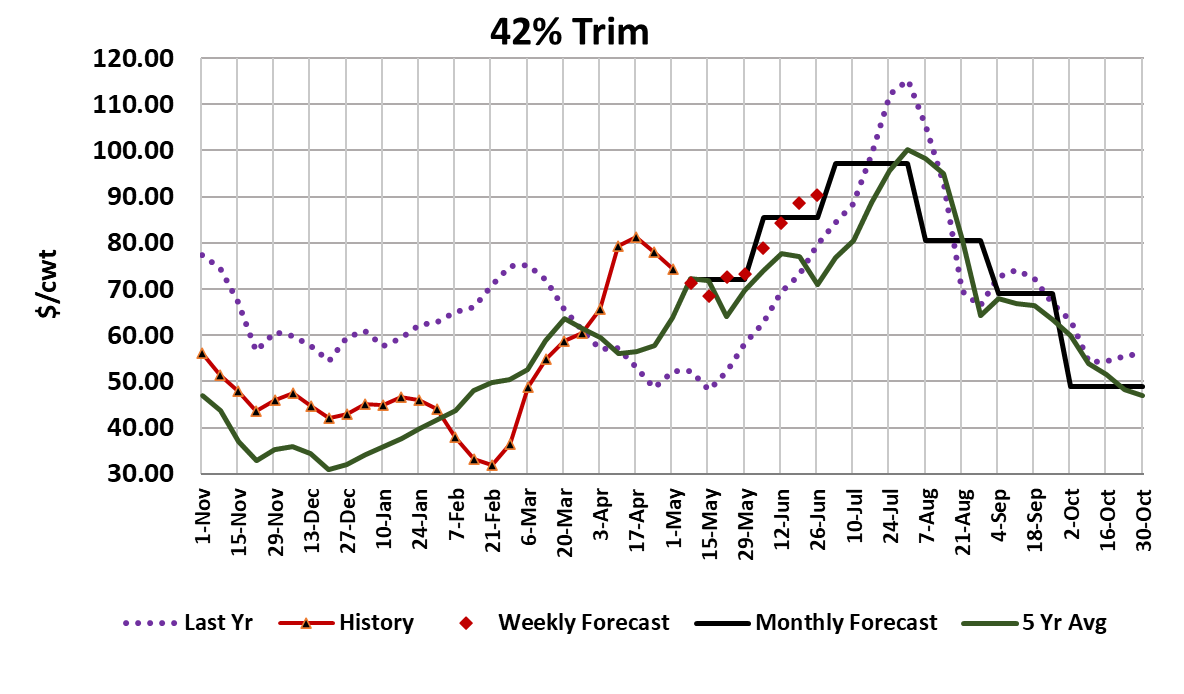

In contrast to the cattle market, the hog and pork complex was pretty boring this week. Negotiated hog prices barely moved, with the NDD averaging $90.97, up $0.42 from the week before. The cutout also barely moved, averaging $98.35, up a mere $0.16 from the week before. The LHI actually declined, losing $0.47 on the week. Needless to say, this steady-state market has caused futures traders to reset their expectations and this week we saw the summer futures lose $2-3, with the Jun contract finishing the week below $99. Less than two weeks ago it traded over $108. So, what is going on? Shouldn’t price levels be advancing seasonally? Yes they should, but there are a few things that are limiting the gains. The first, and probably most important, is that domestic demand seems to have eased a bit over the past couple of weeks, primarily demand for hams and bellies. That is probably temporary and we could see both improve some next week. The second thing is that kills haven’t come down very fast like they do in some years and thus the pork market seems to be amply supplied at the moment. This too will change as we get deeper into May and transition into June. Finally, we could be seeing a modest slowdown in export demand given how quickly the cutout escalated to $100 this spring. Weekly exports dipped below last year this week, driven primarily by softness in movement to Japan and Mexico. ERS released the official trade data for March today, and it showed only a 2.1% YOY increase, but that was comparing to a very big number last year. It seems like what was a very strong export environment during Q1 started to ease a bit in late April. For futures traders, trading the hog market is all about gauging the rate of change in cash prices. When the cutout and negotiated hog prices are rising rapidly, traders build big premiums into the nearby futures. When the cutout and hog markets go stagnant, like they have been for the past couple of weeks, those premiums get slashed. So, while the Jun contract below $99 seems pretty low at the moment, it could easily rocket higher if the cutout and negotiated markets come to life. One thing that could prompt that would be a good old fashioned heat wave that takes hog weights down quickly and encourages producers to slow marketings in order get hogs up to the ideal slaughter weight. A heat wave could materialize in May, but it is more likely to be a June or July event, so the bulls will need to wait a few weeks if that is what they are counting on. In the near term, the best hope for bulls lies in the ham market, which has declined three weeks in a row now and is probably poised to turn higher shortly. That would help the cutout to gain some much needed upward momentum. Bellies appear to be dead in the water and seem destined to repeat last year’s pattern where the summer rally didn’t get started until after Memorial Day. That will limit the upside potential in the cutout, but with just a little more help from the retail primals, we could see the cutout back in the $102-103 range within a couple of weeks. Once the bellies kick in, the gains in the cutout should come faster and the current forecast has the cutout reaching $113 by the beginning of July. If the cutout posts that kind of rally, we can be sure that hog producers will want their share and negotiated hog prices are likely to rise at an even faster pace than the cutout. If all of this talk of rising prices seems a little out of place in the current environment, it is, but we should never underestimate the ability of the hog and pork complex to catch fire in the summer. Clearly futures traders still respect that potential as they are pricing the Jun contract almost $7 over the May. It is looking like May might expire at par or only slightly higher than where the Apr contract went off of the board, which implies that the LHI didn’t hardly move for a whole month between Apr and May. To expect a $7 increase over the next 30 days shows that traders don’t think the market will remain stagnant for much longer. This week’s kill came in at 2.41 million head, about 27k larger than the week before. That was about a 45k larger than what the Sep/Nov pig crop implied. It still looks to me like that pig crop was back-end loaded and we are likely to continue to see small over-kills in the remaining four weeks of the March/May quarter. Overall however, slaughter during this quarter is running about 300k below what the pig crop implied, so there is a good chance that the Hogs & Pigs survey actually over-estimated pig births for a change. That is the good news, but the bad news is that the slaughter during the Jun/Aug quarter is likely to be 1-2% higher than last year. If the Dec/Feb pig crop estimate is correct, the smallest non-holiday weekly kill this summer might only be 2.3 million head—not too far off of what we saw this week. So, there might not be a lot more supply side reduction between now and the summer lows in harvest levels unless USDA badly over-estimated the pig crop or a big heat wave engulfs the Midwest and causes weights to plummet. All that said, I remember that things were looking pretty dismal last spring at about this time when the cutout was near $80, yet by late July we were looking at a cutout near $115. So, as I said before, never under-estimate the ability of the market to post a strong rally in summer. Packer margins are currently right at $10/head, which is relatively good for early May. I expect their margin to shrink down to $5/head by the middle of June and the could be a few weeks in July/August where their margin slips into the red. Producer margins are currently near +$18/head, way better than the -$58/head they had last year at this time. Right now, it just seems like the market is in waiting mode, waiting for something to break the logjam. The best candidate for that would be the hams, which should start to print higher within a week or so and that could be the catalyst to move the cutout back into triple digits and thus bring the futures out of the deep slump of recent days.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}