Pork Wrap May 28

It was more of the same this week in the hog and pork complex—pork

prices rising and hog prices falling. The WCB negotiated cash hog price

fell a little over $3 on a weekly average basis, while the pork cutout

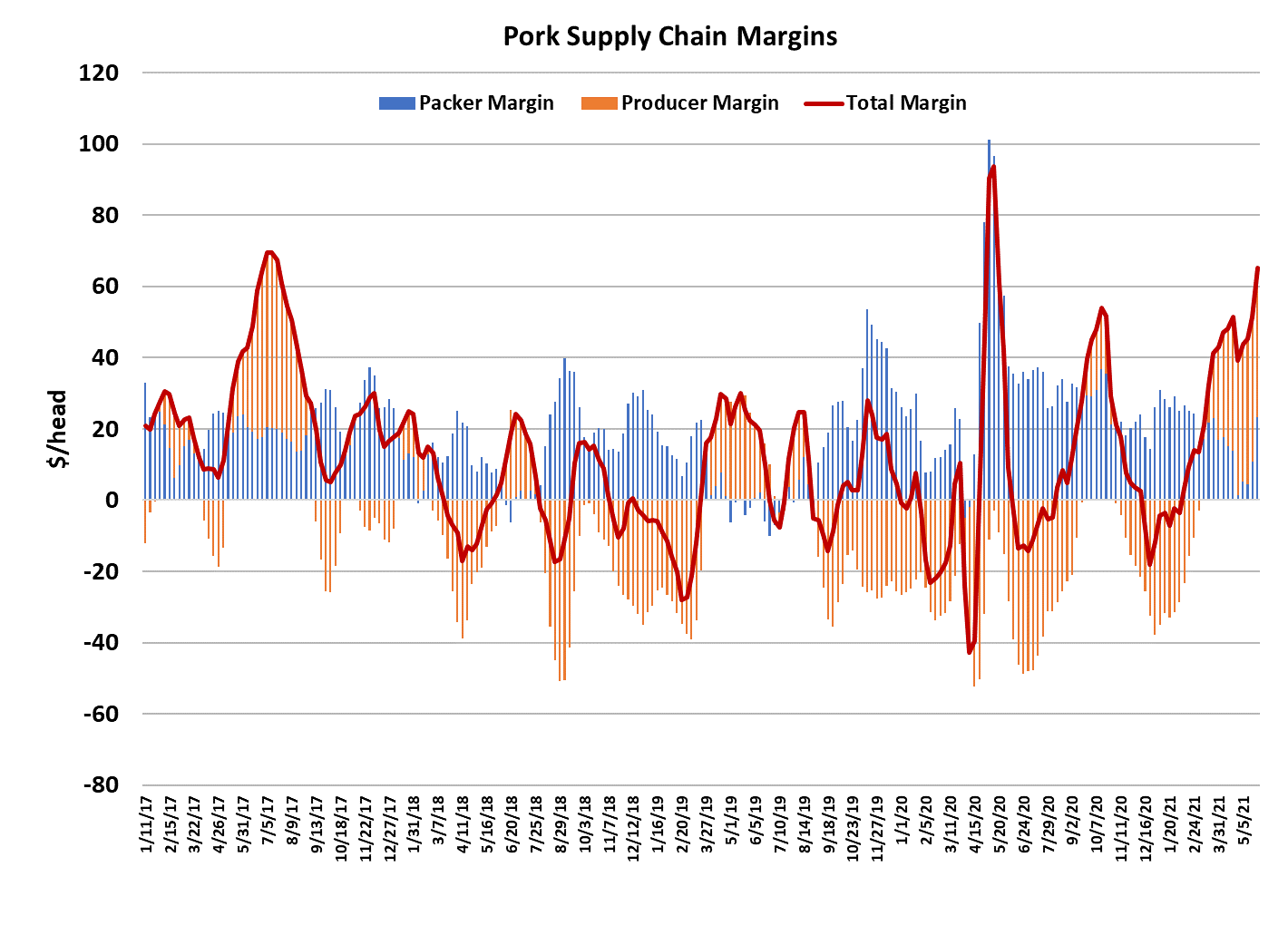

added $6.59. That means packer margins, which had already been on

the rise, shot higher. I calculate them at just over $22/head. Those are

the kind of margins one would expect in the fall, not heading into June.

Is it possible that pork packers are having the same labor availability

issues as beef packers and just can’t push any more animals through

their plants? I don’t think so.

First of all, hog supplies are near their annual low, so packers should

have plenty of spare capacity. I do think that pork packers have the

same labor problems as beef packers, but they just are not on display the

same way they are in beef because hog supplies are seasonally low.

Labor issues will come to the forefront for pork packers this fall and early

winter when seasonally increasing supplies will require packers to run allout, including large Saturday kills. If the labor problems are still in play

come November, then we could easily see packer margins swell close to

triple digits, mostly on the backs of producers because the inability to get

hogs killed on schedule almost always results in a rapid decline in hog

prices. Hog producers would do well to hedge those fall and winter hogs

at the high levels the futures board is currently offering, simply to protect

against a big bottleneck in the packing plants.

So, if labor isn’t currently constraining the ability to get hogs killed, what

explains the exceptionally large margins here in late May? Well,

something is allowing packers to exert pressure on the negotiated hog

market. Maybe producers held hogs back, hoping for price peaks to

come later in the summer and now they have a pressing need to get

hogs marketed. However, hog weights, and in particular the DTDS,

don’t seem to indicate any backlog of hogs. Maybe packers have

changed something about the way they approach the negotiated market.

I’m not sure, but current margins leave plenty of room for them to start

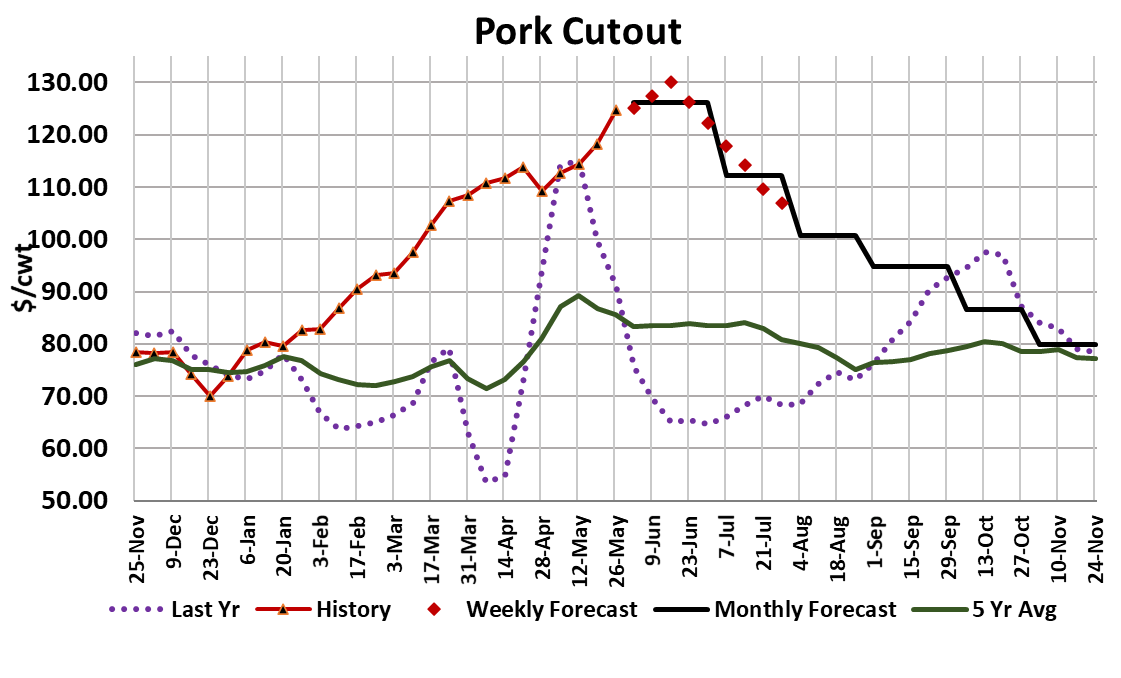

paying up for hogs again should they need to. The cutout doesn’t

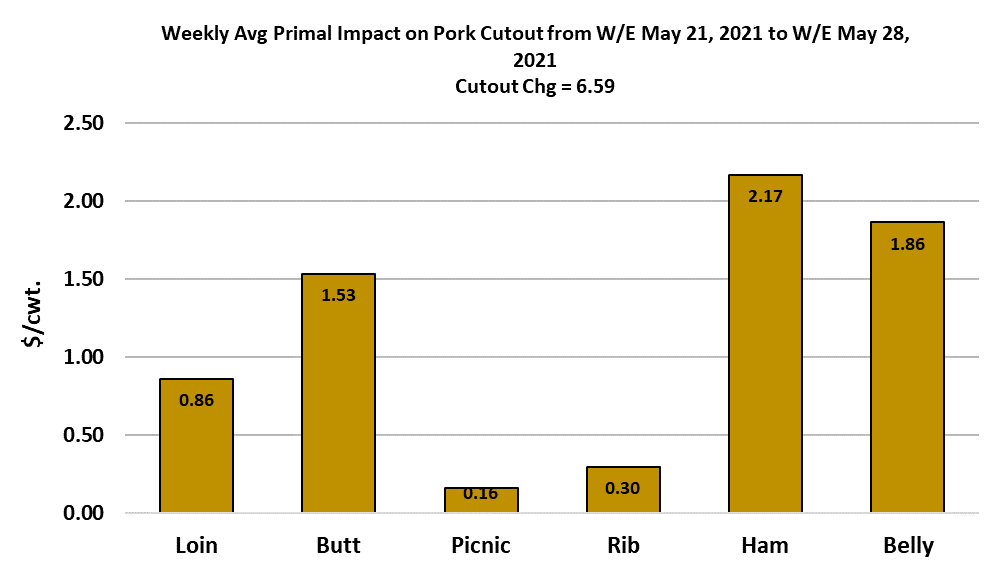

appear to be slowing down. The chart below shows that all primals

helped the cutout higher this week, but the hams in particular were a big

driver. Hams had been softening up until about 10 days ago, when they

started to work higher. Ham prices are high now, but not excessively so

like some of the other primals. Given that 72s averaged $126 this week,

it is possible that some users are buying hams to grind. Whatever the

cause, the move higher in hams greatly helped the cutout this week and

will likely continue to support it in the next couple of weeks.

Ribs finally showed some signs of easing late in the week, but I’m not

convinced that they won’t continue their move higher next week.

Demand is just phenomenal across the entire carcass. The combined

margin chart now makes it clear that the market gave us a big head fake

a few weeks back and has now exceeded the top made last October.

What will it take to cool off this red-hot pork market? I’d say that we

are unlikely to get much if any relief from high prices until supplies

start to expand again. That won’t happen until after Independence

Day, and even then the increases in weekly kills should be very

small until we get to the end of summer. So, we could be looking at

another month or more of rising pork prices. Given that the cutout

is currently in the $125-130 range, that means a $140+ cutout is

not out of the question at some point this summer.

The supply side remains well behaved. This week’s kill came in at

2.38 million head, slightly smaller than the week before. Next

week’s holiday-shortened kill may be closer to 2.2 million head.

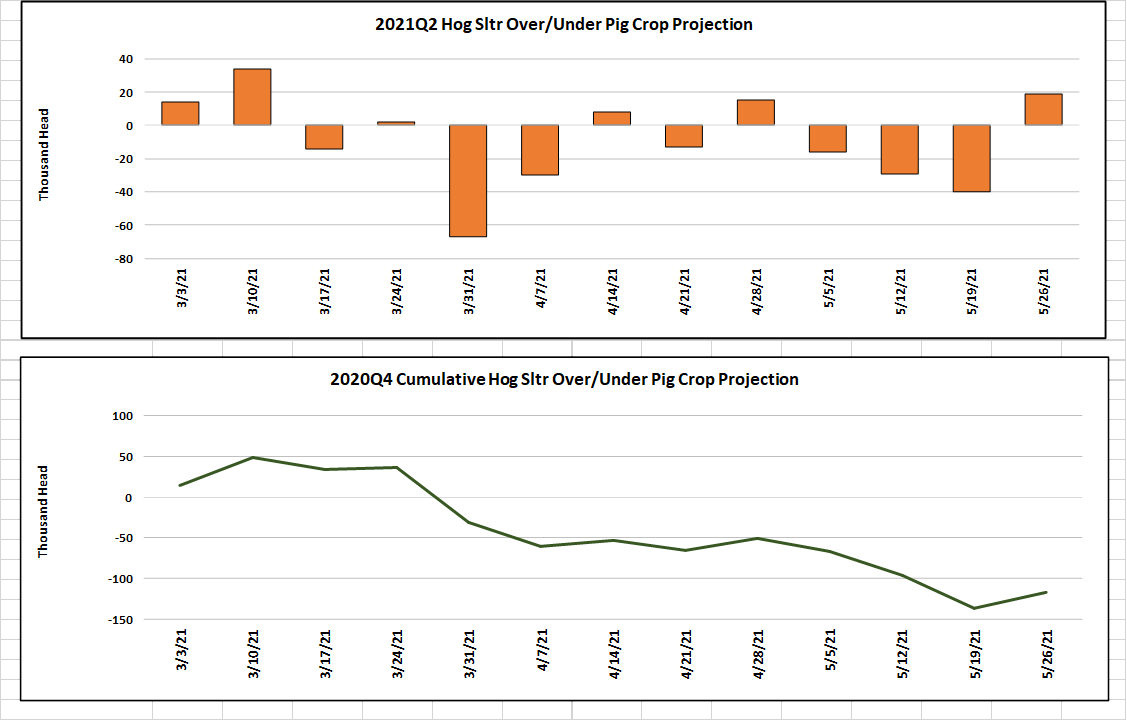

The pig crop over/under kill model shows that after 3 weeks of

slightly under killing the pig crop, packers actually over-killed a bit

this week. The second quarter (March/May) has come to a close

now and it appears that the industry under-killed USDA’s pig crop

estimate by only a little over 100k. That is not a very big miss. So,

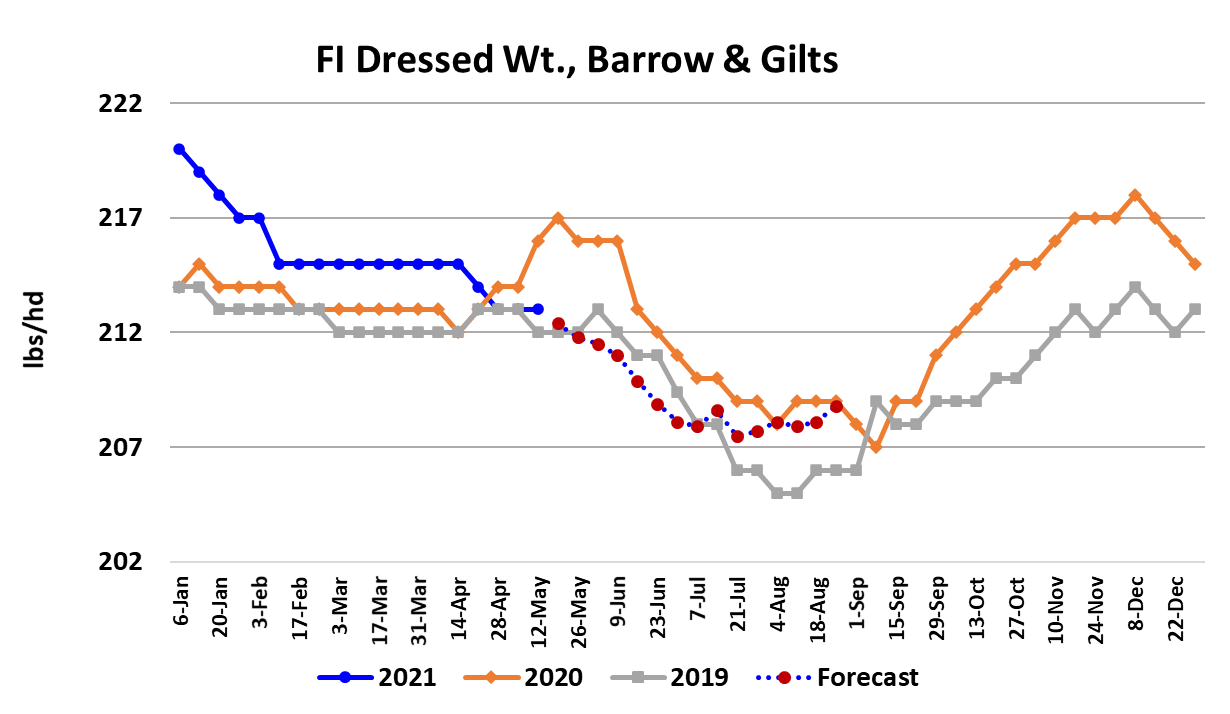

the pig crops are coming in as advertised. Weights are well

behaved also, now beginning their seasonal downtrend, with

barrow and gilt weights only one pound over their 2019 level.

The DTDS is at a relatively low level also, so there doesn’t appear

to be any problems with hogs backing up in the pipeline. It is really

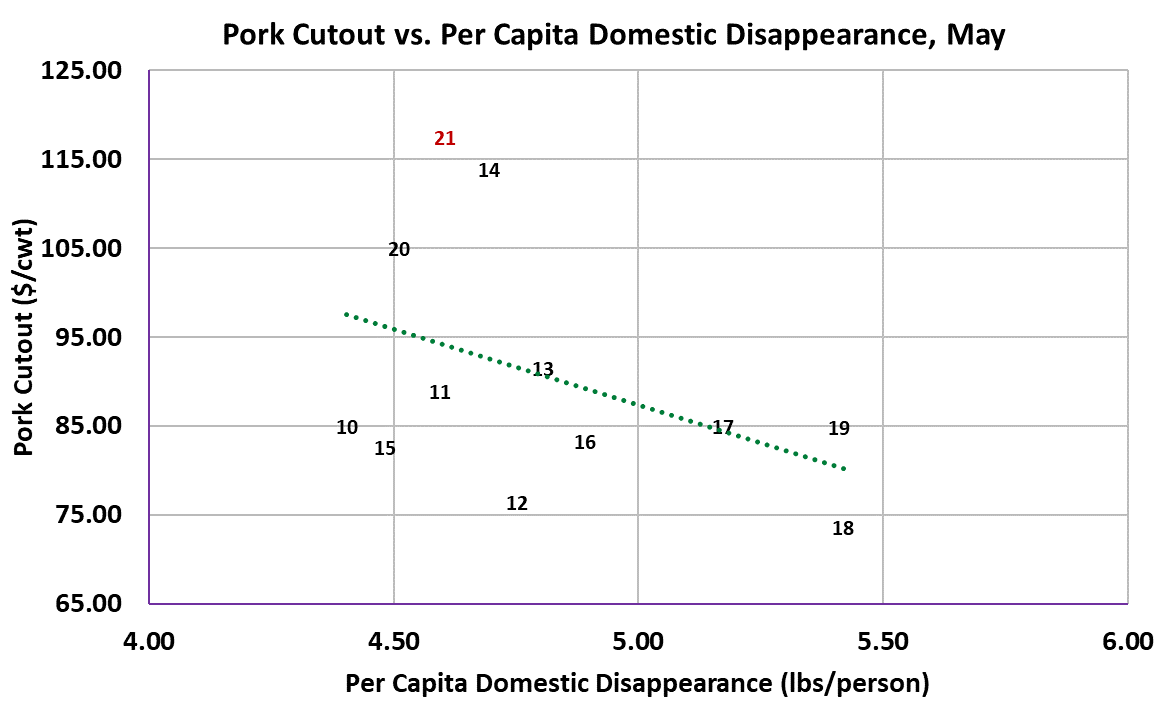

all about demand in the current market. The price-quantity scatter

diagram for May shows just how strong demand has been this

year. That scatter also points out that per-capita supplies are

small, pretty close to 2014 and 2020, which were both years in

which something abnormal was going on in the supply side. This

year, it is a reduction in the herd by producers that began a year

ago, combined with strong exports that is limiting per-capita

availability. Looking at that scatter, one can imagine a non-linear

demand curve where the slope gets very, very steep as the percapita quantity starts to approach 4.5 lbs. That shape probably

wasn’t appropriate back in 2010-2016, but it may be now.

The futures market continues to rise as the cutout and LHI rise, but

traders are very quick to punish the market if even the slightest hint

of a lower cutout appears. Markets like this need a steady flow of

positive news to keep rising and if that dries up for even a day or

two, the futures sell off. So far, those sell offs have been excellent

buying opportunities. For now, we just need to watch the primals

for any signs that demand weakness is creeping in, because the

supply trajectory is lower for the next 5-7 weeks, so price pressure,

should it develop, will almost certainly come from the demand side.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}