Pork Wrap May 27

Negotiated cash hog markets improved a little bit this week, with

the WCB up $1.46 and the National market quote up $0.86. The

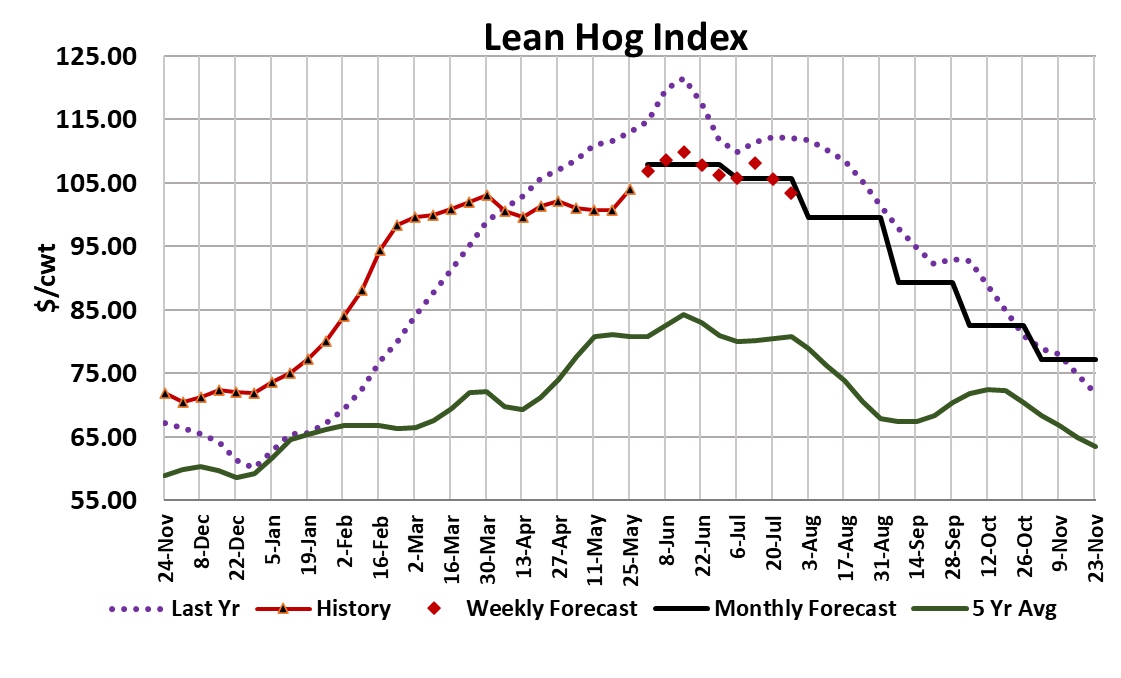

Lean Hog Index added $3.32 to average a hair over $104. Most

of that gain was due to the delay in the previous week’s stronger

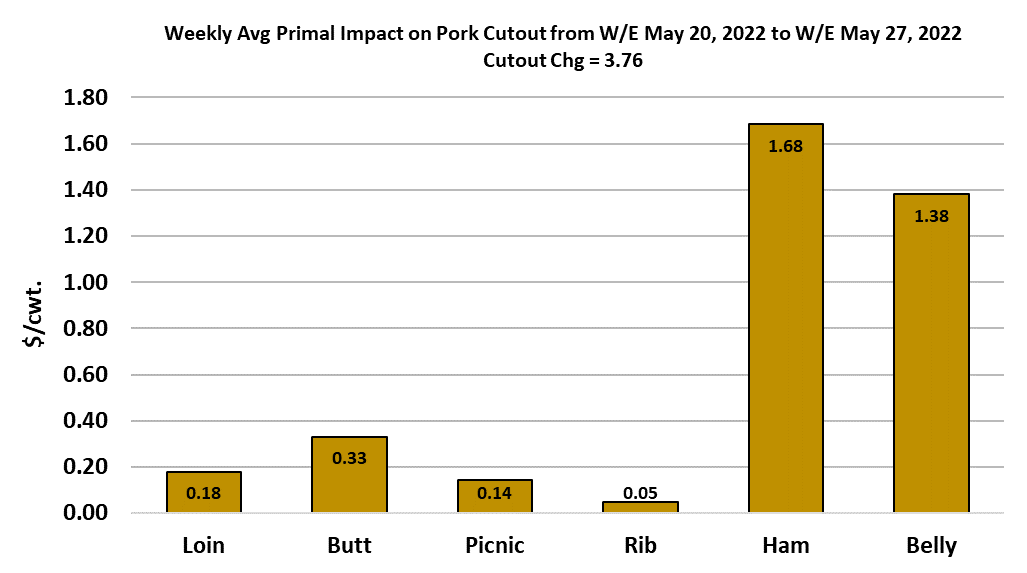

cutout and cash hog pricing flowing into the index. The cutout

continued on its upward trajectory, gaining $3.76 on the week.

Once again, it was the bellies and hams that provided the loin’s

share of the strength. Packer margins held almost steady at

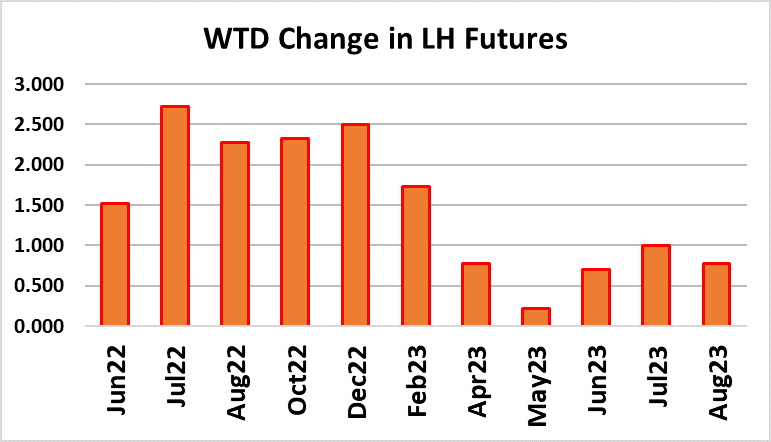

$4.84 per head. The futures market was higher across the board,

with the bigger gains coming in the Jul and Aug contracts. At one

point this week the Jun contract was trading close to $111.50,

which seemed a bit excessive given that the LHI at $104 and only

two weeks until expiration. Jun finished the week at $110.40 and

the question of whether or not the LHI can get there by expiration

will largely hinge on how the cutout performs in the next couple of

weeks.

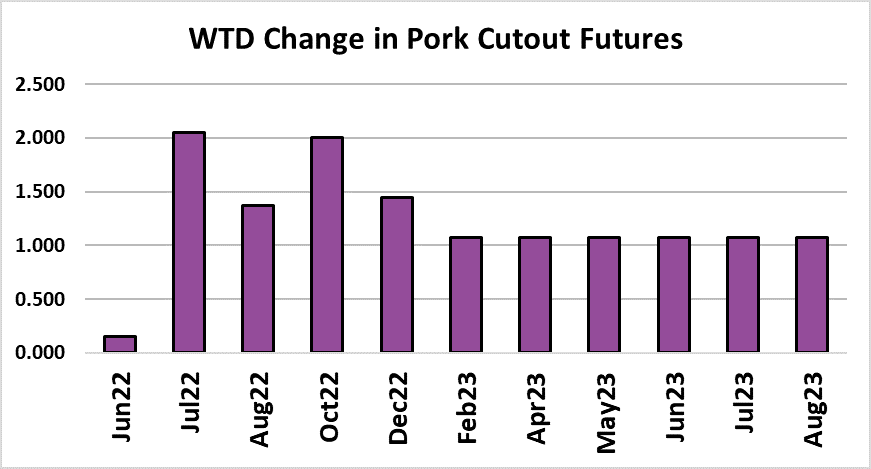

And, of course, how the cutout performs will depend on what the

bellies and hams do. My fundamental forecast has both primals

trading higher over the next couple of weeks, but not strongly

enough to take the cutout high enough to justify $110 on June. I

think that perhaps something closer to $108 is more likely. The

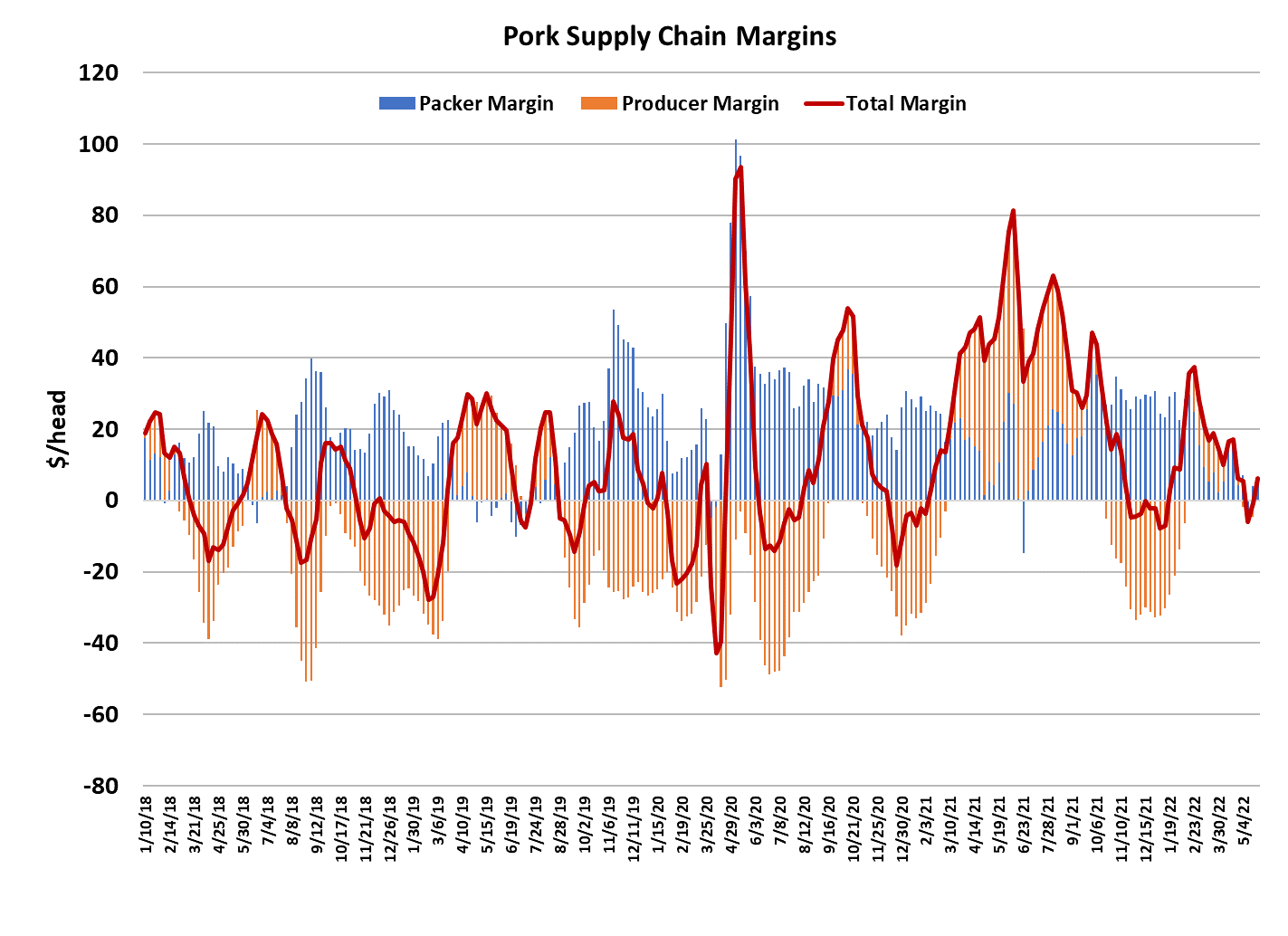

combined margin chart has been higher now for two weeks in a

row and so I’m going to take that as confirmation that a new

upcycle in demand is underway. This one may be short and isn’t

likely to get nearly as high as some of the upcycles we saw during

the pandemic years. Retailers will be restocking early next week

following the holiday weekend and that alone could boost the

cutout a little, depending upon how good their clearance is. Of

course, those retailers won’t be buying bellies and hams, which is

where the real action will be.

Processors will be snapping those up, dependent on how they

expect demand to play out over the next couple of months. All of

the normal demand headwinds remain in place: inflation, high

retail pork prices, post-pandemic spending shifts, etc. so I still

think the longer-term trend toward softer demand remains an

important market feature. It may not be very visible during June

since we are in a local demand upcycle and production will be

declining, but from mid-summer onward, I’d expect the softening

demand story to be back near center stage. This week’s

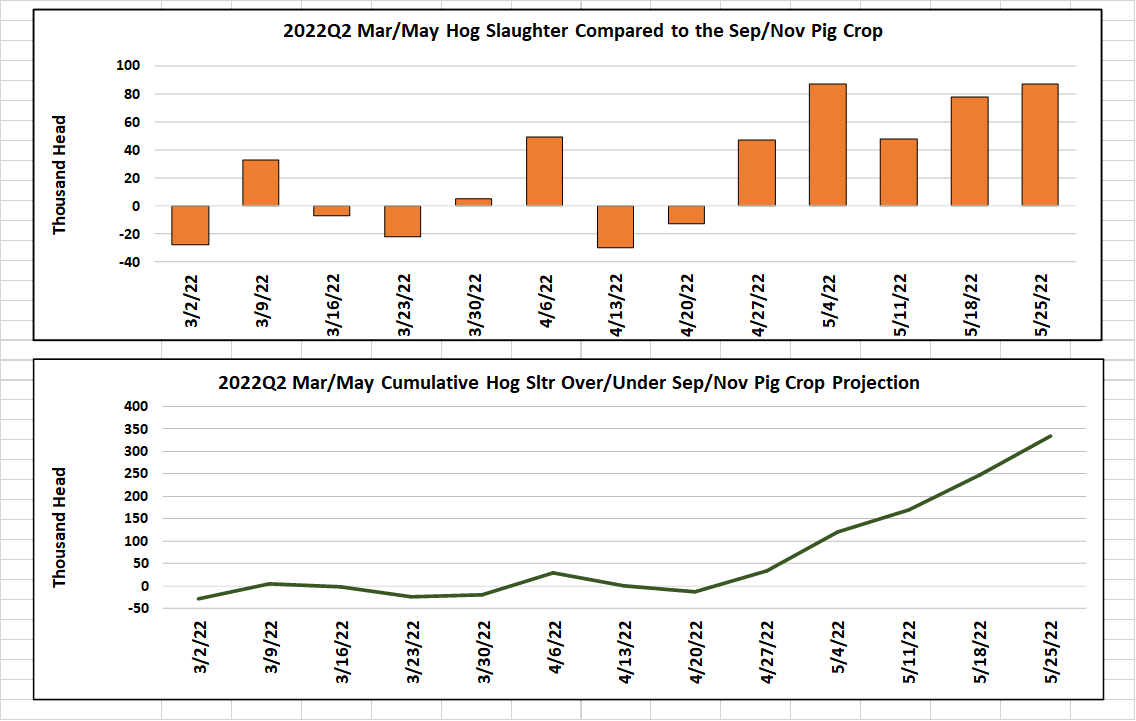

slaughter clocked in at 2.35 million head, just a little smaller than

last week’s strong number but still well above what the pig crop

implied. We have now completed the March/May quarter and it

looks like the industry over-killed USDA’s estimate of the Sep/Nov

pig crop by about 340,000 head.

Now the important question is whether or not those over-kills will

persist into the Jun/Aug quarter. That is when packers begin

working on the Dec/Feb pig crop, which USDA estimated to be

down 1% YOY. I’m projecting the Jun/Aug slaughter total to be

about 1.5% below last year, but I may be too low on that. Actual

pork availability might be slightly better than last year during the

quarter, depending on how the export market performs. The

weekly export data showed a nice uptick in shipments last week and

we saw China take the largest weekly total so far this year. I want to

see more confirmation of growing volumes into China though before

I’m ready to declare that Chinese interest in US pork is improving.

With all the lockdowns, port congestion and macroeconomic

softness that China is facing it doesn’t seem likely that they will

ramp up their imports of US pork materially from current levels.

Mexico seems a better bet as a growth market for exports this year.

This is the time of year when the focus is largely on the supply side

of the hog market. Everyone knows that hog supplies tighten

between Memorial Day and Independence Day and there is also the

potential for exceedingly hot weather which can slow weight gains

and thus limit supply. The prior pig crop leads me to believe that the

smallest non-holiday kill this year will be close to 2.25 million head.

That is really only about 100,000 head smaller than this week’s kill,

so the impact of smaller animal numbers on the kill is probably only

modest at this point. The weather/weight impact on production

remains to be seen, but so far this year temperatures in the Midwest

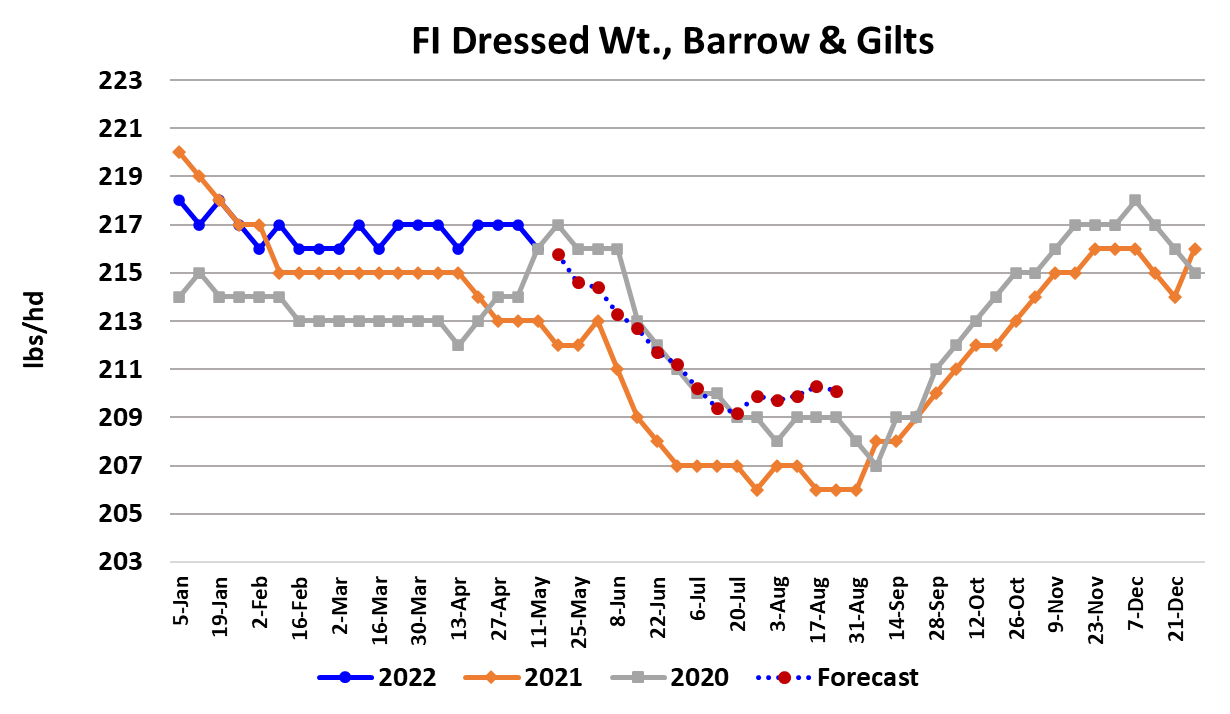

have been relatively mild. Barrow and gilt carcass weights were

reported down one pound this week to 216 pounds, so it looks like

the normal seasonal decline in weights is now underway.

My expectation is that weights will decline toward a bottom in the

209-210 pound range sometime in early-to-mid July. Futures

traders seems to have curbed their enthusiasm a bit. No longer is

there danger of them running the summer contracts up to $125 just

because the cutout advances for a few days in a row. In fact, if I’m

right about $108 being an appropriate expiration value for June,

then that could have a chilling effect on the futures as Jun declines

heading toward expiration. Next week, watch the bellies and hams

as always—those are the big movers. Also keep an eye on the

projections for next Saturday’s kill because that will have a big

impact on how long the effect of the holiday persists in the market.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}