Pork Wrap May 26

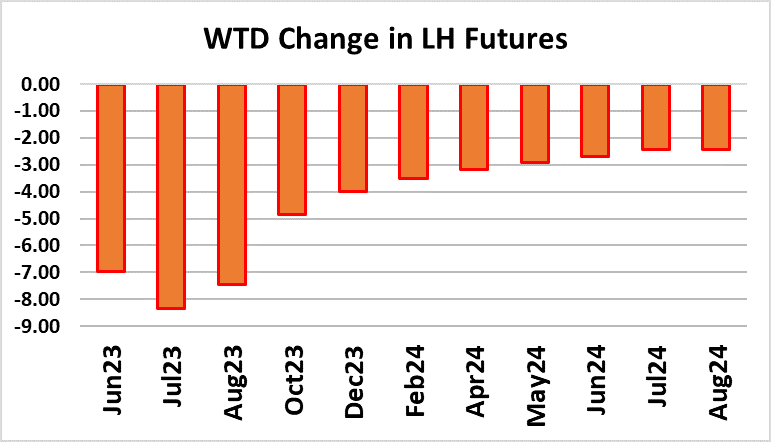

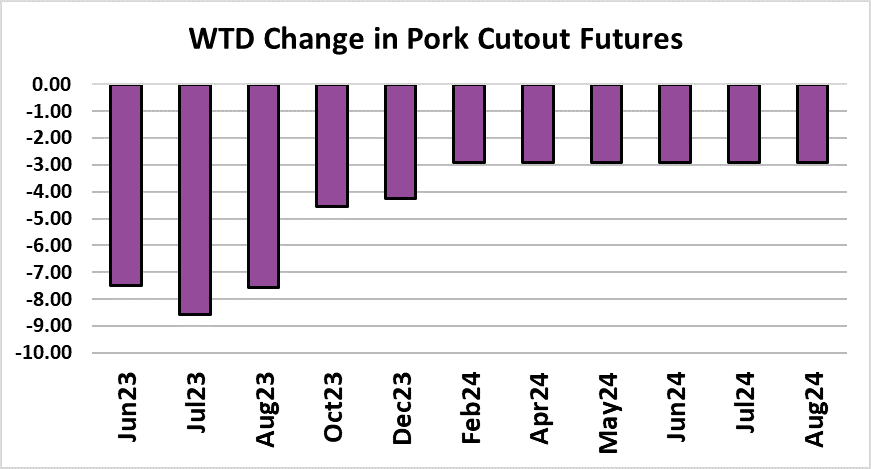

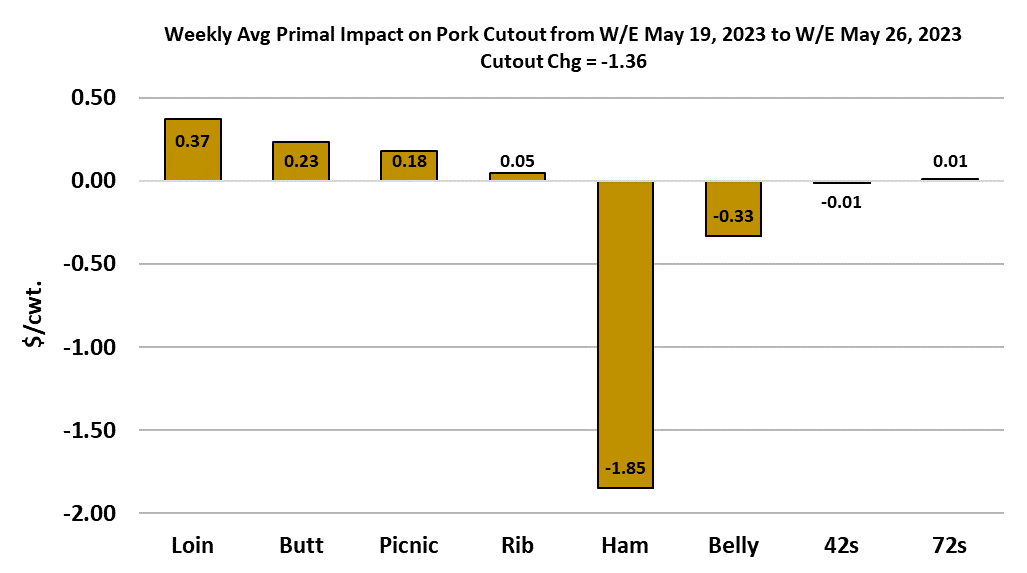

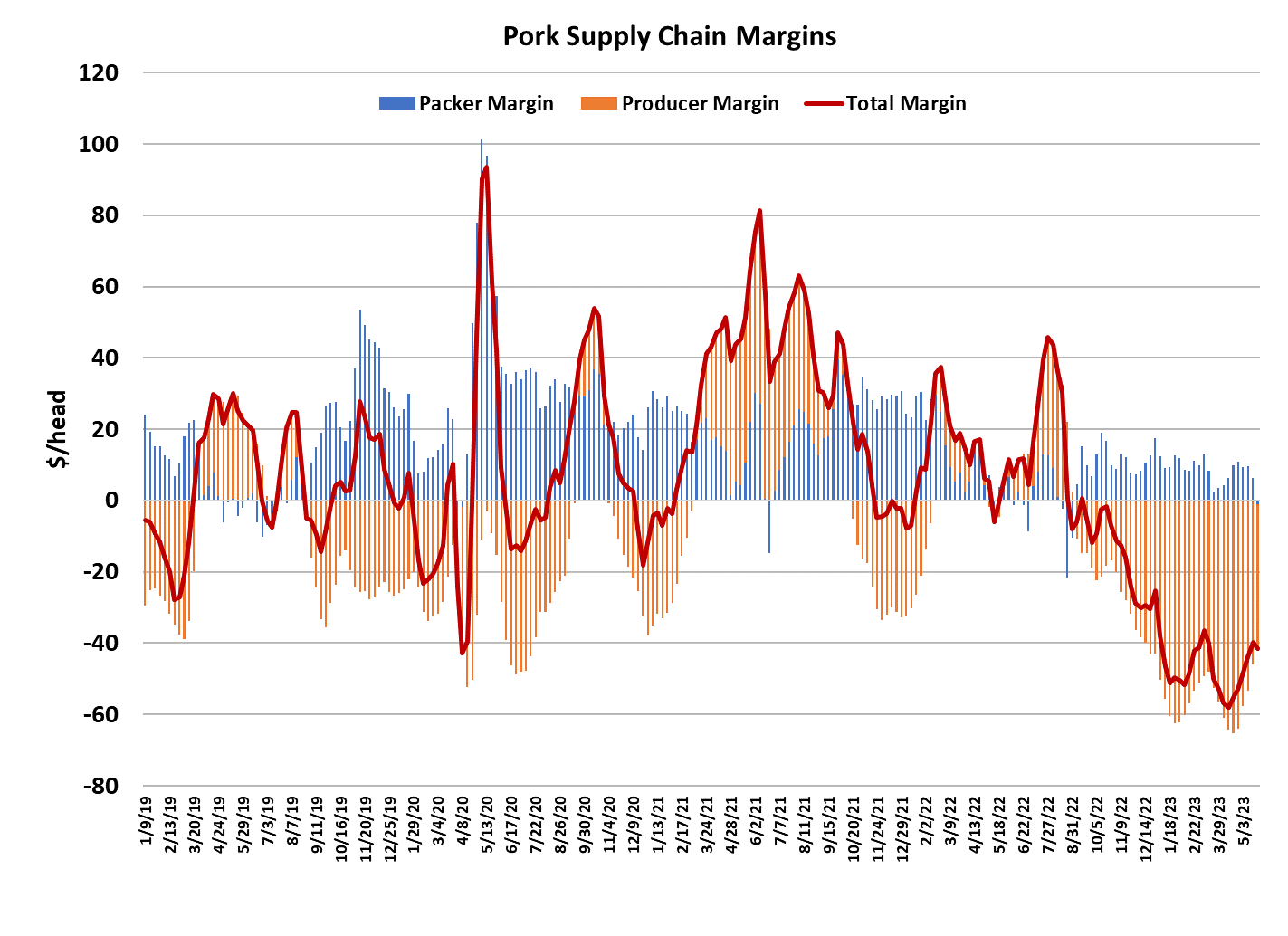

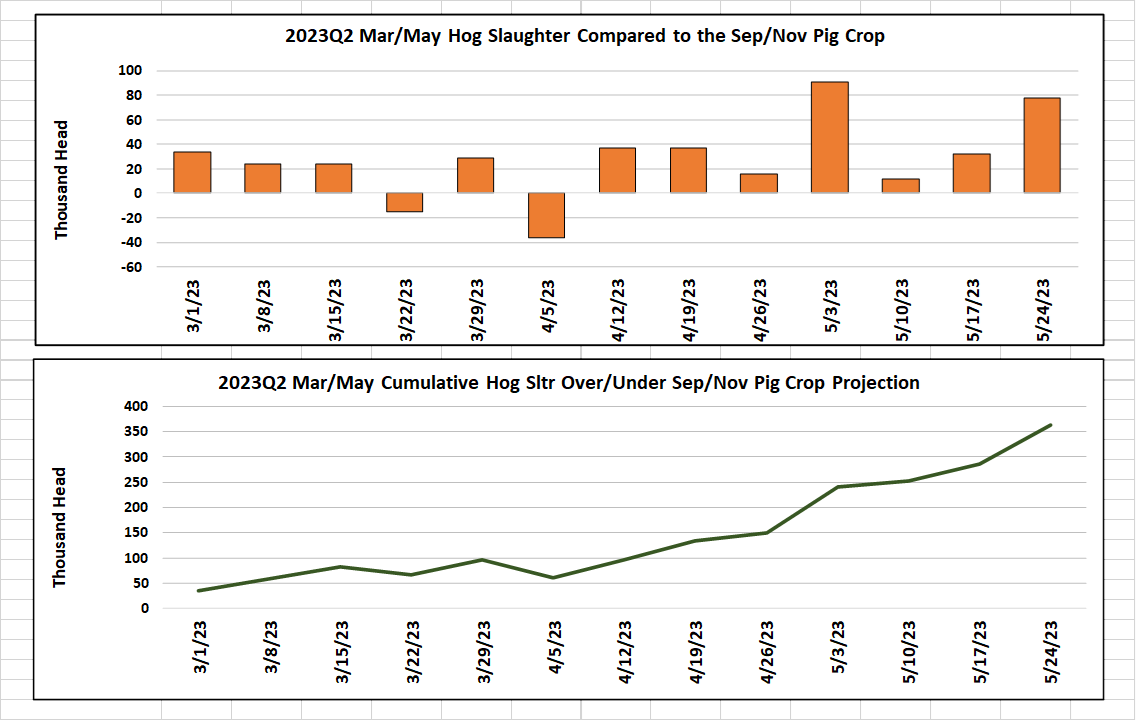

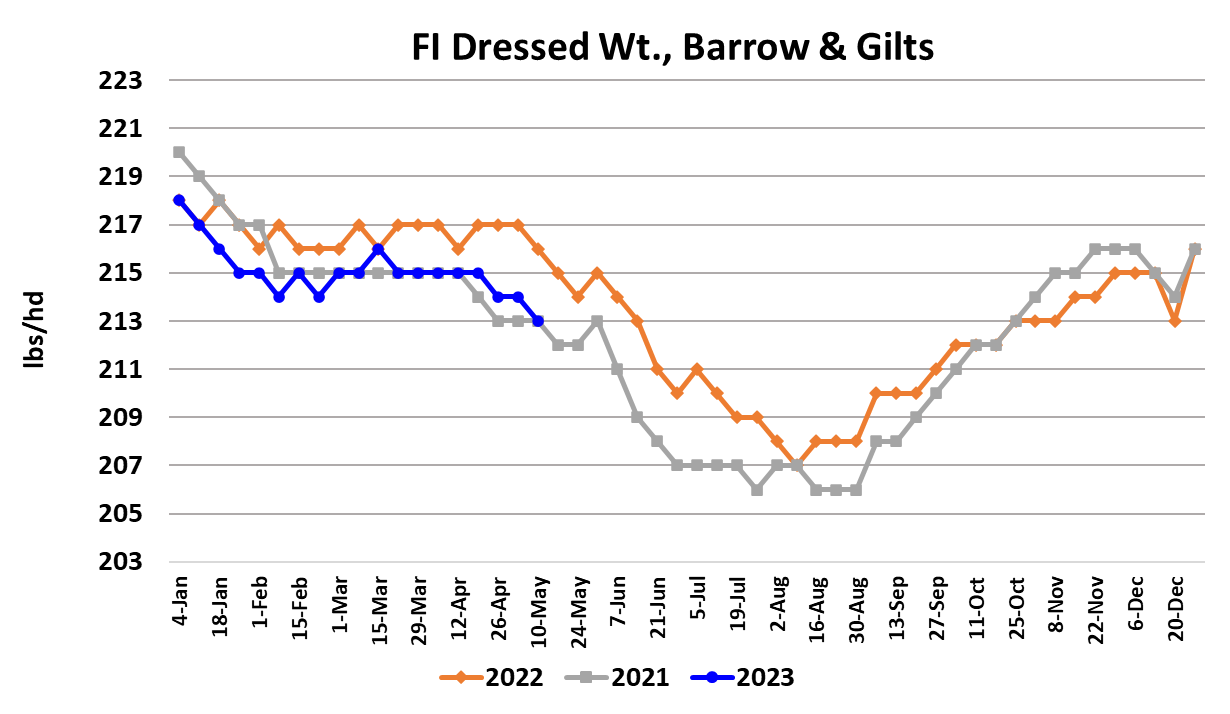

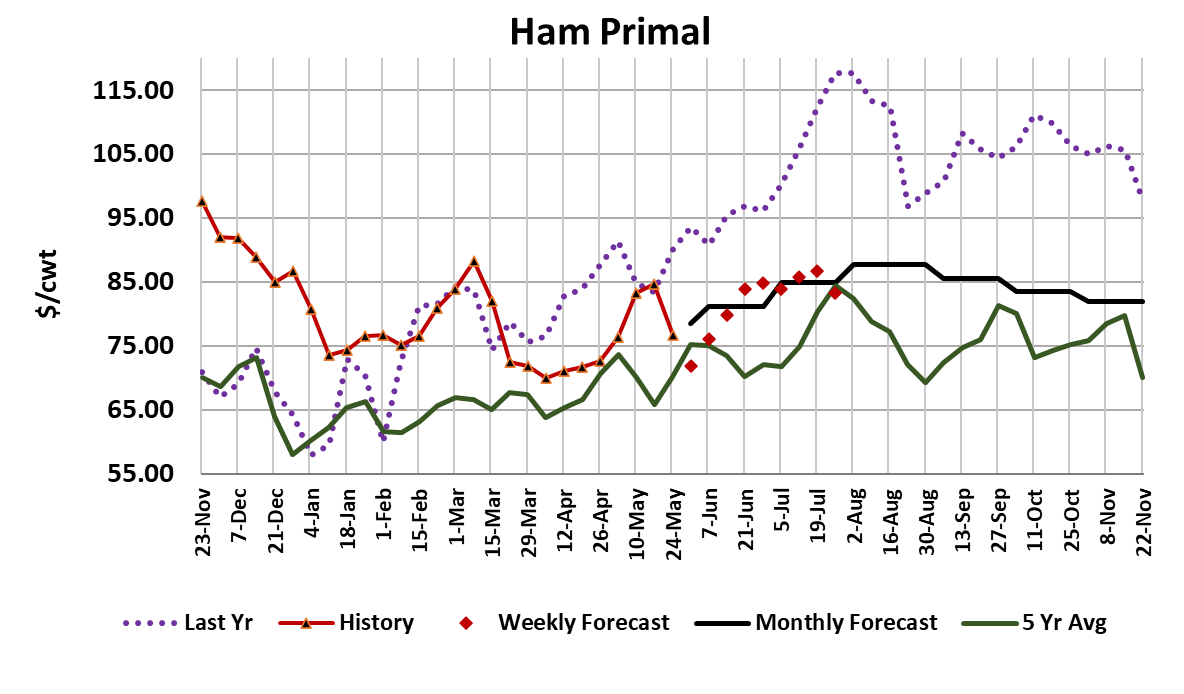

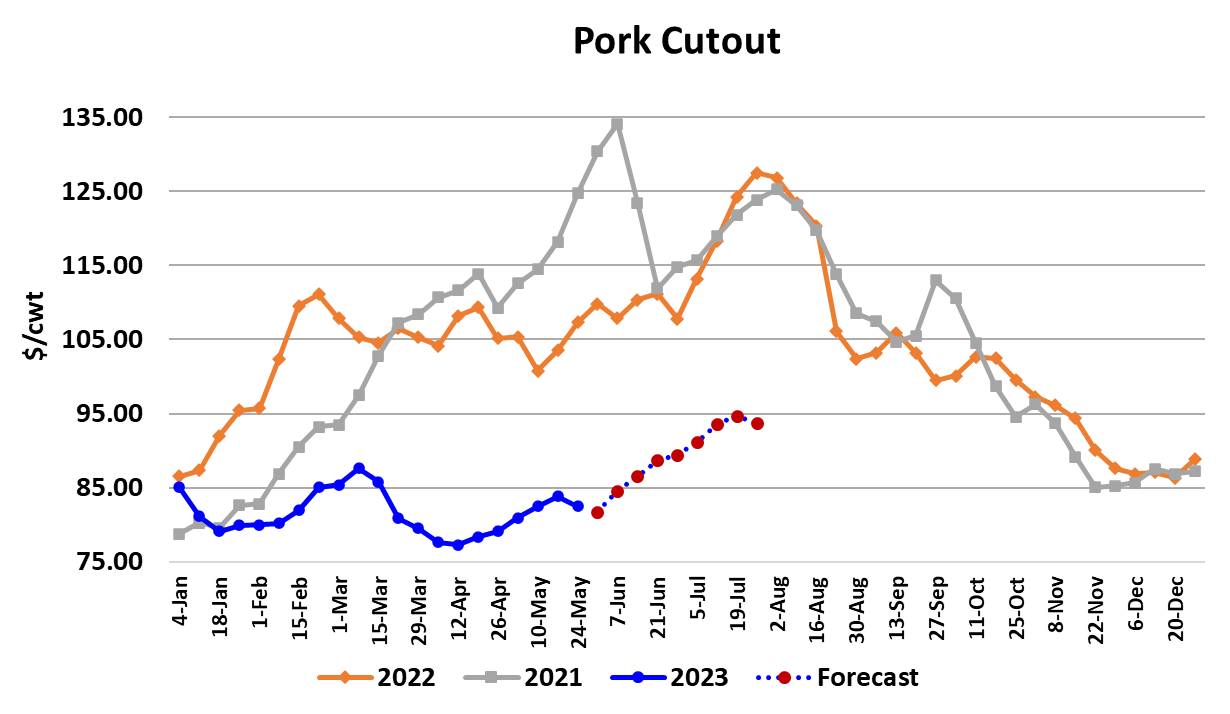

For the first time in six weeks, the pork cutout failed to advance. The cutout averaged $82.51/cwt. this week, down $1.36 from last week’s average. If that seems like a small thing, it probably is, but futures traders took it very seriously and pummeled the entire curve this week. Friday-to-Friday, the July contract lost $8.57/cwt. Last week all of the summer futures contracts were premium to the LHI and by the end of this week, they were all significantly discount to the index. What in the world brought about such a violent reaction to such a small price change in the cutout? Traders have probably been ruminating on the Supreme Court’s Prop 12 decision since it was issued a couple of weeks ago and may have taken this week’s price softening as an indication of far worse things to come due to the implementation of Prop 12 by California on July 2. That is the best explanation I can come up with. In reality, all that happened this week was that the processing items, hams and bellies, saw price declines ahead of Memorial Day weekend. The retail primals all traded higher. It wouldn’t be unusual for ham processors or bacon slicers to have less interest in purchasing raw materials the week before a holiday, so those price declines may have been perfectly rational and they may get at least partially reversed next week when processing plants re-open after the holiday. For several week now, ham prices have been the only part of the cutout moving in any significant way. All of the other primals have either been flat (bellies) or inching seasonally higher (retail primals). For a while hams were moving higher and that lifted the cutout from the high $70s to the low $80s. Now suddenly, the hams have a bad week and the futures traders act like it is the end of the world. There are a lot of reasons to be optimistic about the cutout, not the least of which is a reduced Saturday kill this week and a holiday-shortened kill next week. Further, the calendar is now turning to June, which usually sees available hog supplies tighten up significantly and carcass weights post some of the largest declines of the year. Granted, the pork complex hasn’t performed well at all this year, but it has been in the process of slowly working higher. No one was expecting the LHI to break into triple digits this summer, but it wouldn’t be unreasonable to expect it to continue plodding a little higher each week until supplies start to expand again near the end of July. This week’s market action seems like a huge over-reaction to a relatively minor, and possibly short-lived, problem with the hams. And, because this pessimism permeated the entire futures curve, all of the contract on the board now look really underpriced relative to the fundamental forecast. Cash hog prices were also a little lower this week, probably as a result of packers pushing back due to the big gains in the last couple of weeks, but I certainly don’t think that negotiated hog prices have topped for the year. That is more likely to be a July event. The NDD negotiated market averaged $0.72/cwt. below last week. That is not a crisis either. Packers only slaughtered 20k hogs on Saturday since it is Memorial Day weekend, and that brought the weekly total to 2.37 million head. Next week, look for the holiday-reduced kill to be below 2.0 million head. This week’s kill was, once again, larger than what the (revised) Sep/Nov pig crop implied and now that the March/May quarter is complete, I calculate that the industry overkilled the pig crop by about 360,000 head. Keeping in mind that back in March USDA revised the Sep/Nov pig crop upward by 540k, that means that USDA’s survey underestimated that pig crop by a whopping 900k. Hopefully, USDA will do a post-mortem investigation into what caused the survey to miss so badly and maybe they can make corrections so that it doesn’t happen again. In any case, next week we will start working on the Dec/Feb pig crop, which USDA estimated to be up 0.3% YOY. Of course, if they underestimated that pig crop by 900k again, then we will be looking at a 3.2% YOY increase in the hog supply this summer. Now that is something that would be worrisome. Hopefully, the survey is close to accurate and we won’t be swimming in hogs this summer. FI barrow and gilt weights declined another pound this week and it is clear that the seasonal trend lower has commenced. The DTDS weights are at very low levels historically, suggesting that producers have done a good job of marketing on schedule and there is little risk of a backup in the production pipeline. Packer margins took a hit this week, dropping from +$6/head last week to -$1/head this week, but slightly negative margins at Memorial Day are fairly typical. With hog supplies trending seasonally lower, there is very little risk that packers will try to protect their margins by cutting the kill. If anything, they will fight a little harder with each other for the shrinking pool of uncommitted hogs in the next few weeks and that should be supportive to negotiated hog prices. The now familiar pattern of strong negotiated prices coming out of the WCB on Tuesday and Wednesday repeated again this week and will likely be a regular feature of the market for most of the summer. I see packer margins ranging a few dollars either side of zero at least through July. The combined margin ticked a little lower this week, as the downward change in packer margins slightly outweighed a modest improvement in producer margins. I’d see this as just a little pre-holiday blip and not the start of a new downcycle in demand. Of course, hams and bellies will have to do better in the coming weeks if a new downcycle is to be avoided. The weekly export data has looked pretty good in recent weeks. It has been a long time since international buyers have seen price levels this attractive heading into summer. I expect that exports will continue to perform fairly well, at least through the summer. Prop 12 seems to be the elephant in the room, but I don’t really think it is going to be much of a market disruptor in the short-run. California has stated that all fresh pork entering the state after July 2 must be Prop 12 compliant, but I don’t think they have a very well defined process for checking compliance. A producer may have 5 sow barns and one of them is outfitted with Prop 12 compliant sow stalls. When his pork gets shipped to California, how will they know which barn the piglets were born in? I suspect that pork will continue to flow as normal into California this summer and there is even a chance that California might recognize that they aren’t ready to police this thing and thus delay the official implementation. On the surface, Prop 12 seems scary and relatively bearish for the market, but I think that, as with most things, reality won’t be nearly as bad as what traders are imagining now. Next week, look for the cutout to move higher as pork users reload after the holiday and find less availability due to the short kill. Keep a close eye on the hams because if they start to move higher again, then all of this week’s panic will have been for naught.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}