Pork Wrap May 24

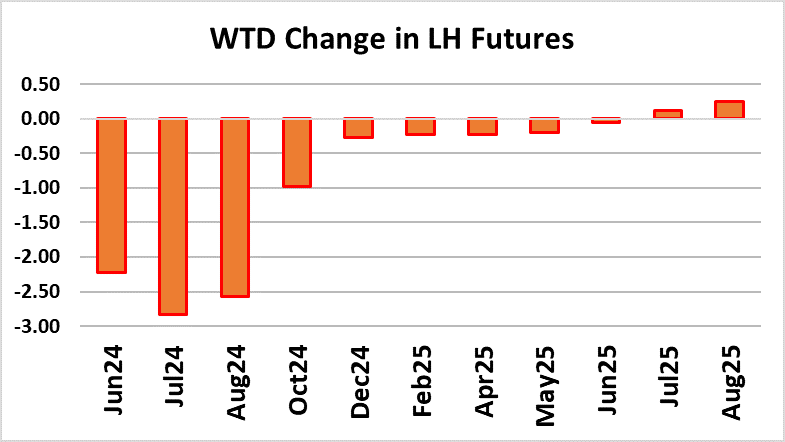

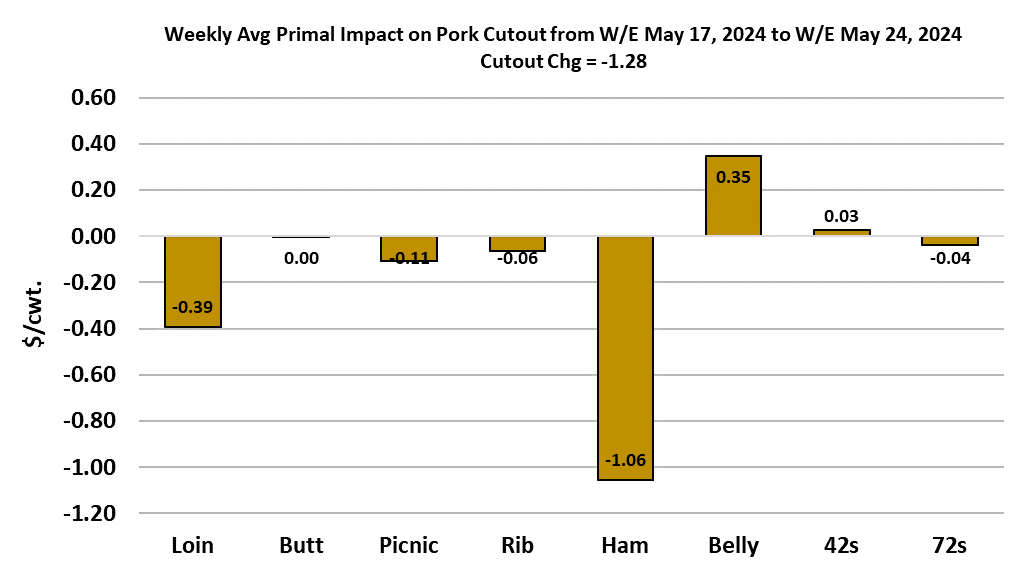

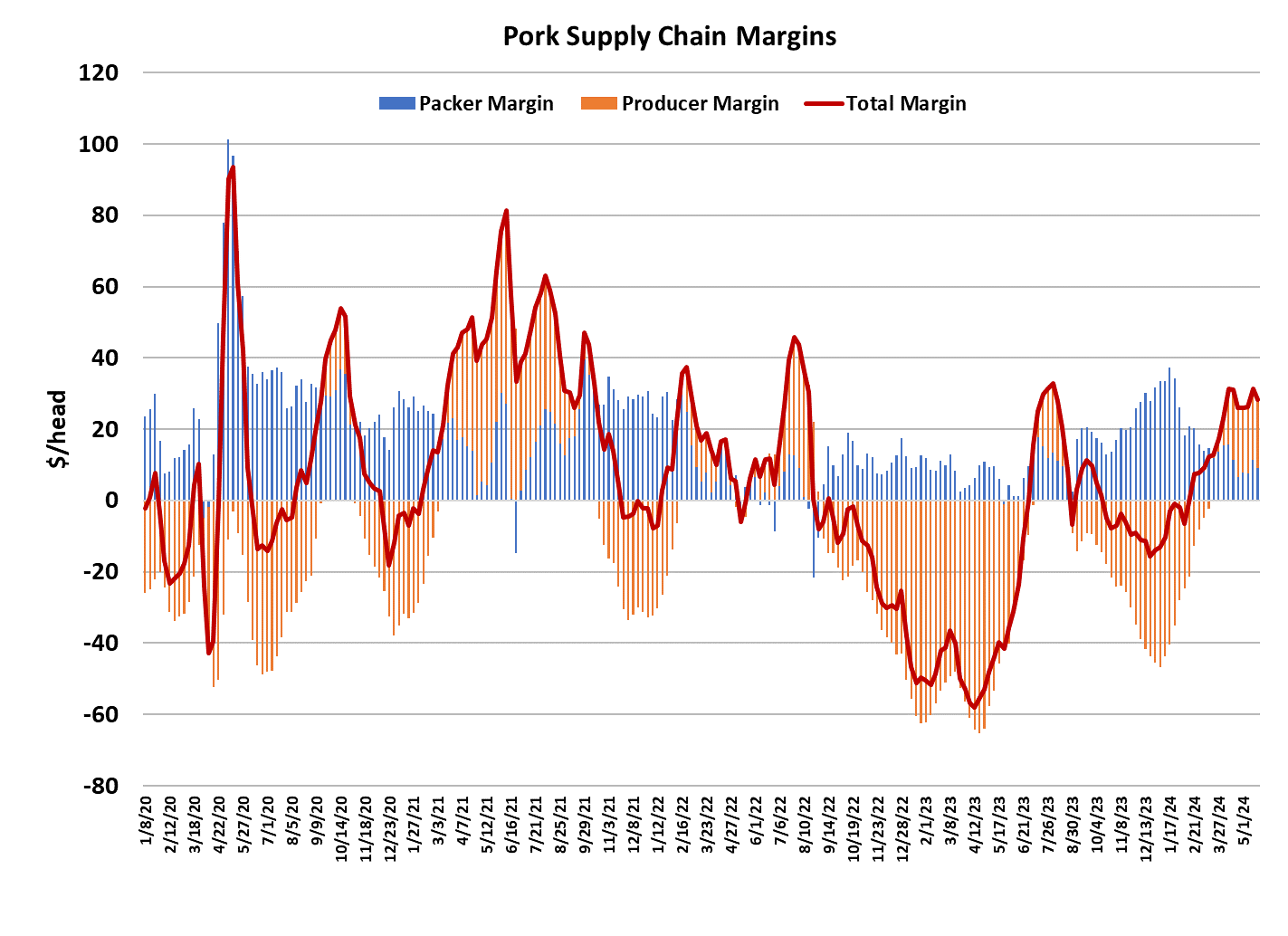

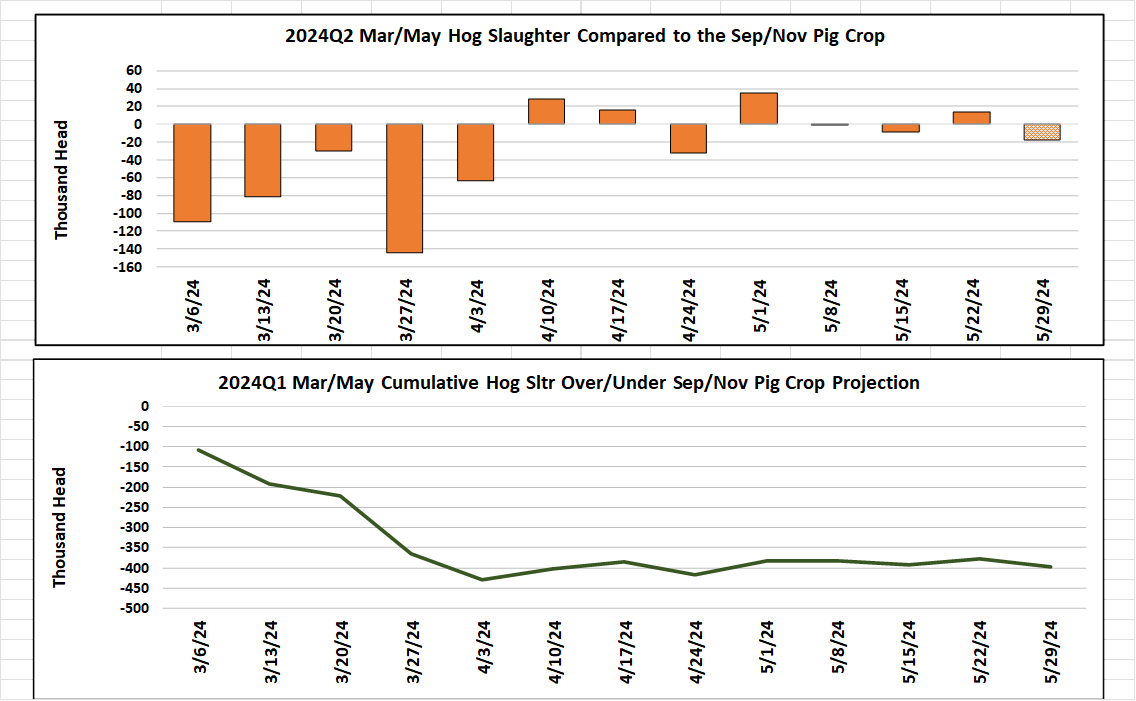

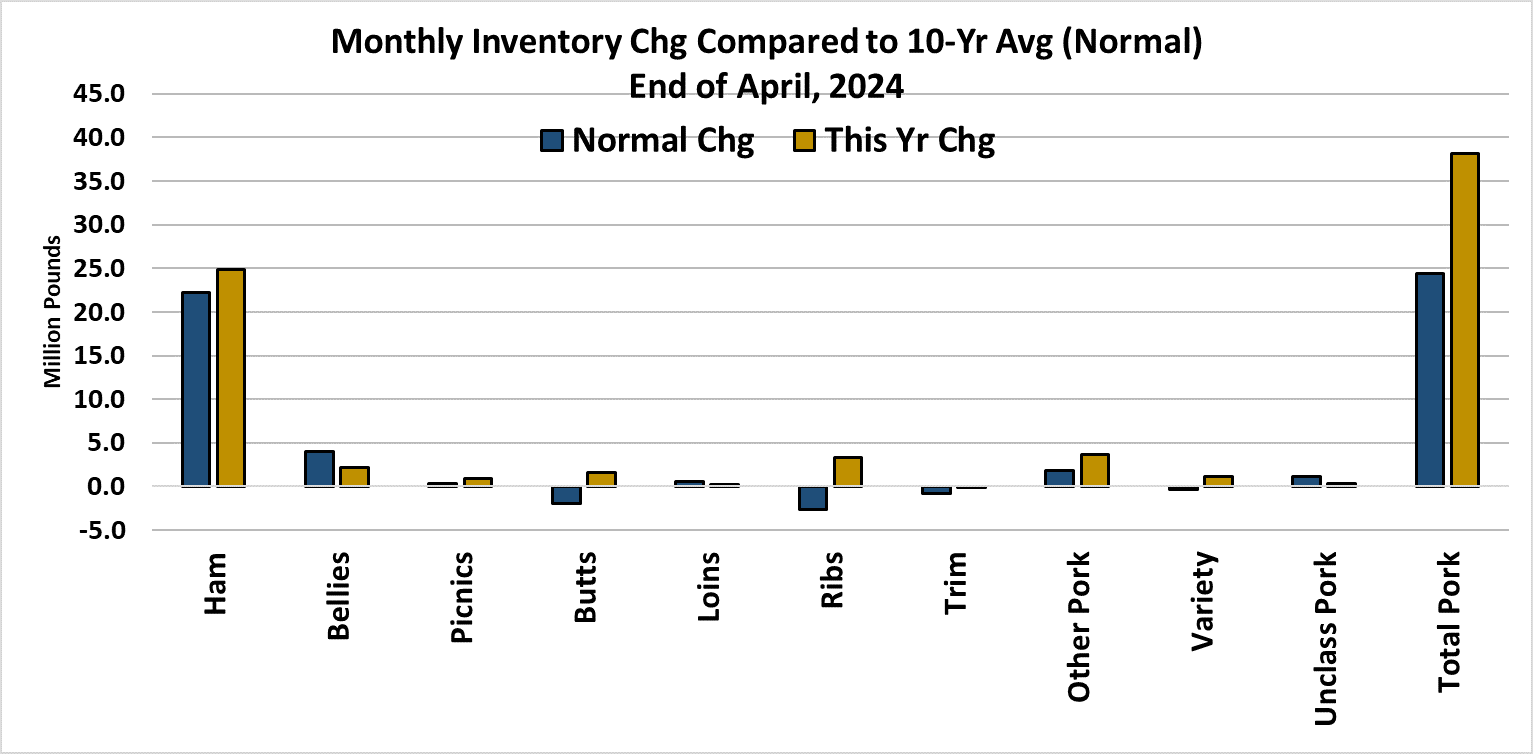

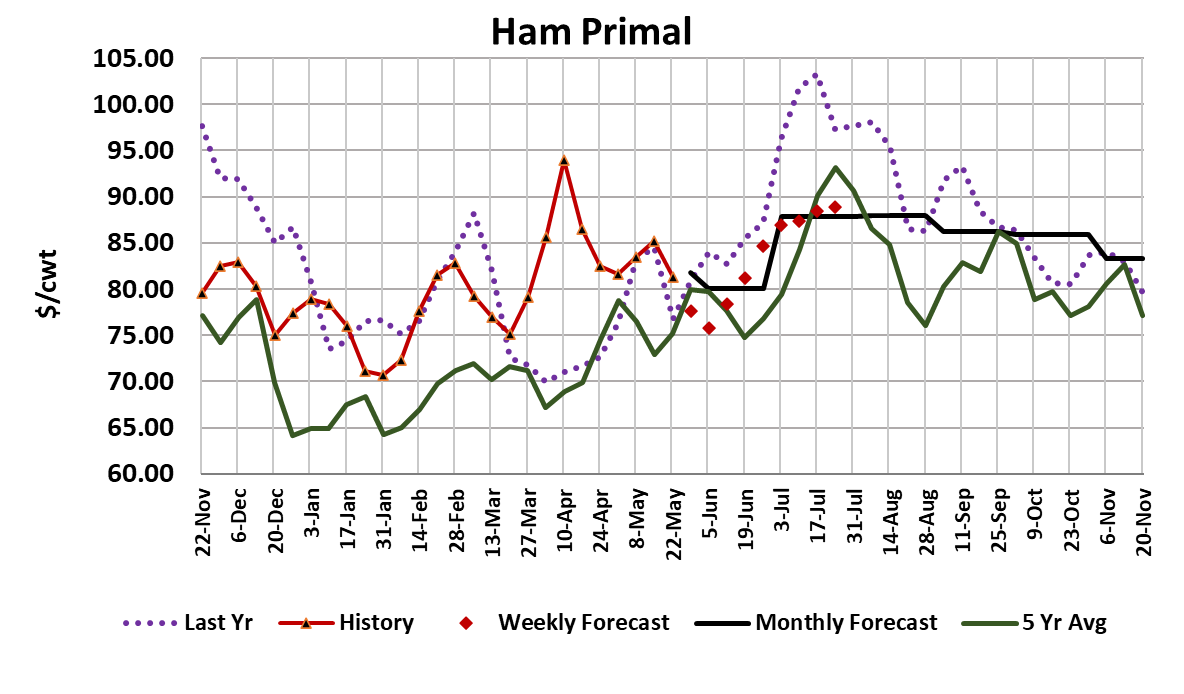

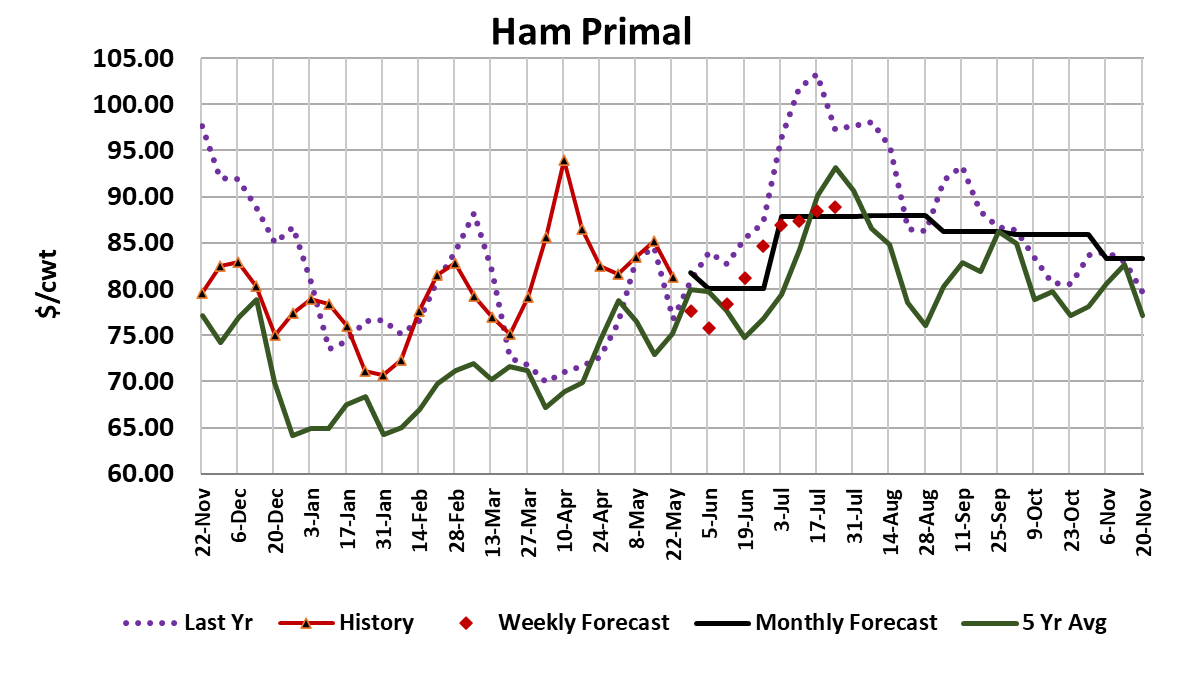

It is fairly typical for the pork market to be heating up in May as Memorial Day approaches, but this year seems to be different. The cutout actually declined this week, dropping $1.28/cwt. to average $100.07. The negotiated hog markets were softer too, with the WCB dropping $2.06 on its way to averaging $87.42. For those that are keeping track, the WCB market was trading near $92 back in early May. The slowdown at this time of year is odd but it doesn’t yet seem severe enough to label as a full-blown demand “air pocket”. Those are normally characterized by sharp price declines that can’t be accounted for by changes in pork availability. No, this seems to be more of a gentle easing in demand that is also being helped along by pork production failing to show much in the way of seasonal decline. Stay tuned however, because the potential for an air pocket is rising and would certainly catch participants off guard if it happens in June, which is normally one of the strongest pricing months of the year. The supply side is not helping the cause either. Over the past 10 years, excluding 2020, weekly pork production has posted an average decline of about 20 million pounds from the end of March to Memorial Day. This year however, production has been close to flat over that same period. Kills have come down slightly, but carcass weights have not, and that is keeping pork production from exhibiting its typical seasonal decline. Further, the weather in hog country has been relatively benign this spring and that may be what is keeping carcass weights from trending lower. This week’s kill came in at 2.37 million head, down from 2.4 million the week before, but most of that decline can be attributed to packers running light schedules on Friday and Saturday in recognition of the holiday weekend, not a lack of hogs. Next week will mark the final week of the March/May quarter and it looks like the industry has under-killed USDA’s estimate of the Sep/Nov pig crop by about 400,000 head. However, as the attached chart indicates, most of that under-killing happened early in the quarter and recent kills have been much closer to what was expected. The industry will be killing the Dec/Feb pig crop during the upcoming Jun/Aug quarter, and that was projected to be up 1.9% YOY. If that estimate is correct, then it is possible that we will see very little shrinkage in the weekly kill from this point forward. In other words, the push toward higher pricing this summer will need to come all from the demand side because there is little help on the way from the supply side. That is a scary thought to those that are used to seeing tight summer pork production generate triple digit cutouts and hog prices. Futures traders are trying to wrap their heads around this possibility at present and have pounded the summer contracts back into the mid-$90s after brushing up against $110 less than a month ago. In fact, the over the past 23 trading sessions the July contract has only seen four days where the price settled higher than the day before. That sounds more like November than May. How bad could it get? At the rate things are going now, traders would be wise to prepare for the possibility that the Jun contract expires lower than the May contract and we could soon see the nearby futures trading at little or no premium to the Lean Hog Index. Of course, next week’s holiday reduced kill could provide a temporary reprieve by limiting production, but my guess is that packers will generate weekly kills at or above 2.4 million head in early June to catch back up. The behavior of the primals this week just adds to the discouragement. Hams were by far the biggest drag on the cutout as they have now turned lower following a brief upturn in late April/early May. There could easily be another 2 weeks of lower ham pricing before they start to cycle higher again. Bellies helped the cutout a little, but the price prints near the end of the week were soft and make it look like bellies are not really going anywhere. Processing demand for raw materials like bellies and hams will be light next week due to the holiday. Even more concerning than the price action in the processing sector, is the fact that the retail items are now starting to struggle. The loin, butt, picnic and rib primals all averaged lower on the week, as did the trims. The losses weren’t big, but they were losses nonetheless. As I look across my trend model for the primals I have only the bellies and butts trending higher and everything else trending lower. That’s about 35% of the carcass where prices are headed higher and 65% where prices are working lower now. It is hard to be bullish in that environment. The combined margin has been wavering in a sideways pattern over the last few weeks and looks like it might be poised to break lower soon. The good news is that both packers and producers are realizing positive margins at present, with packer margins calculated at +$9/head and producer margins near +$19/head this week. If demand does start to weaken after the holiday, it will hit packer margins first and will then likely transition to producer margins a week or two later. Despite all of the negative fundamentals that seem to be emerging, I’m not yet ready to give up on at least a modest price rally this summer. The fundamental forecast has the cutout holding in the high $90s for a couple more weeks before it regains its footing and marches towards a top in the $108-110 range by mid-July. USDA provided the cold storage data for April today and it showed pork inventories building faster than normal for this time of year. The 10-year change in total pork inventories between March and April is +25 million pounds, but this year the increase was close to +38 million pounds. Fortunately, bellies were not one of the items that contributed to that big build. However, if we zoom out and look at the big picture, total pork in cold storage is still down 11.7% YOY, despite the fact that inventories grew 8.2% during April. I’d rate the cold storage situation as only mildly bearish at present, but it bears close watching because if demand stumbles this summer, it could leave the industry with large cold storage stocks heading into fall and winter just as production starts to increase and that would be very bearish indeed. Next week, expect the cutout to meander sideways as post-holiday fill-in business for the retail items could help to offset further weakness in the hams. As long as the cutout isn’t going anywhere, we shouldn’t expect much lift in the negotiated hog market either.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}