Pork Wrap May 20

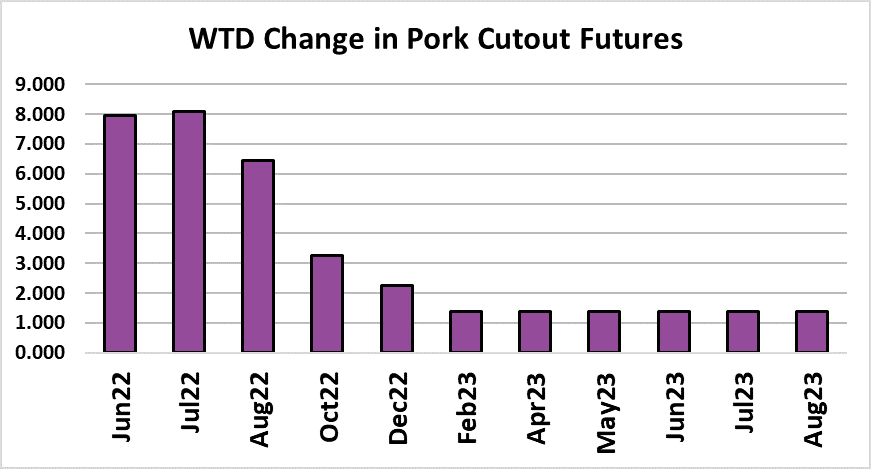

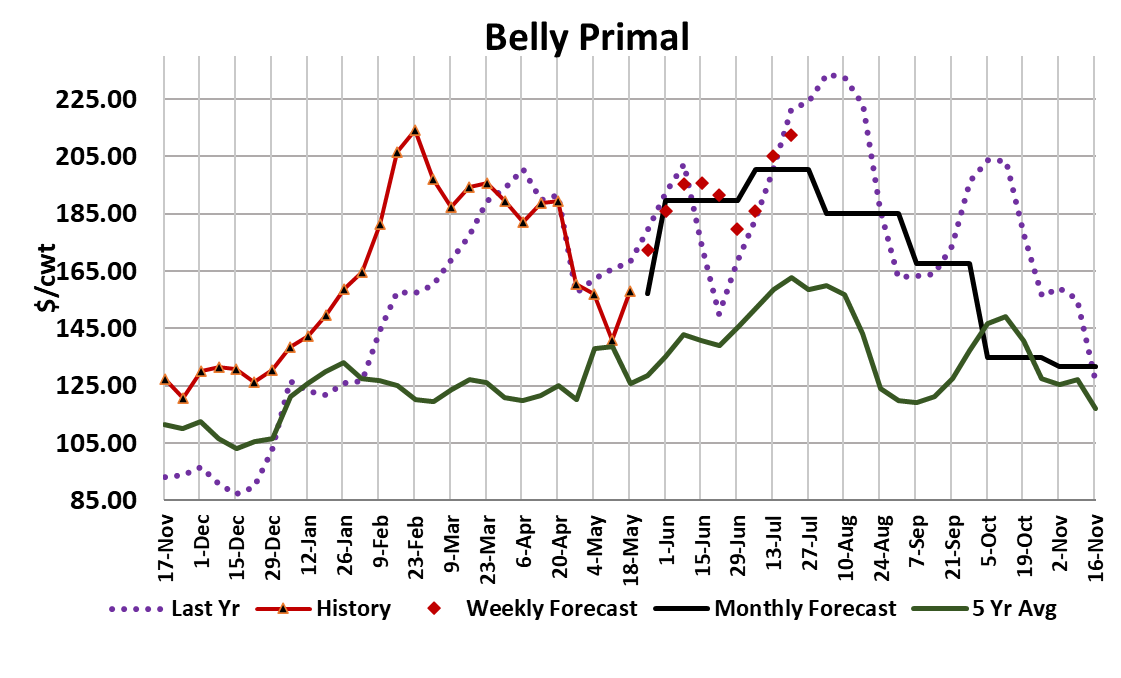

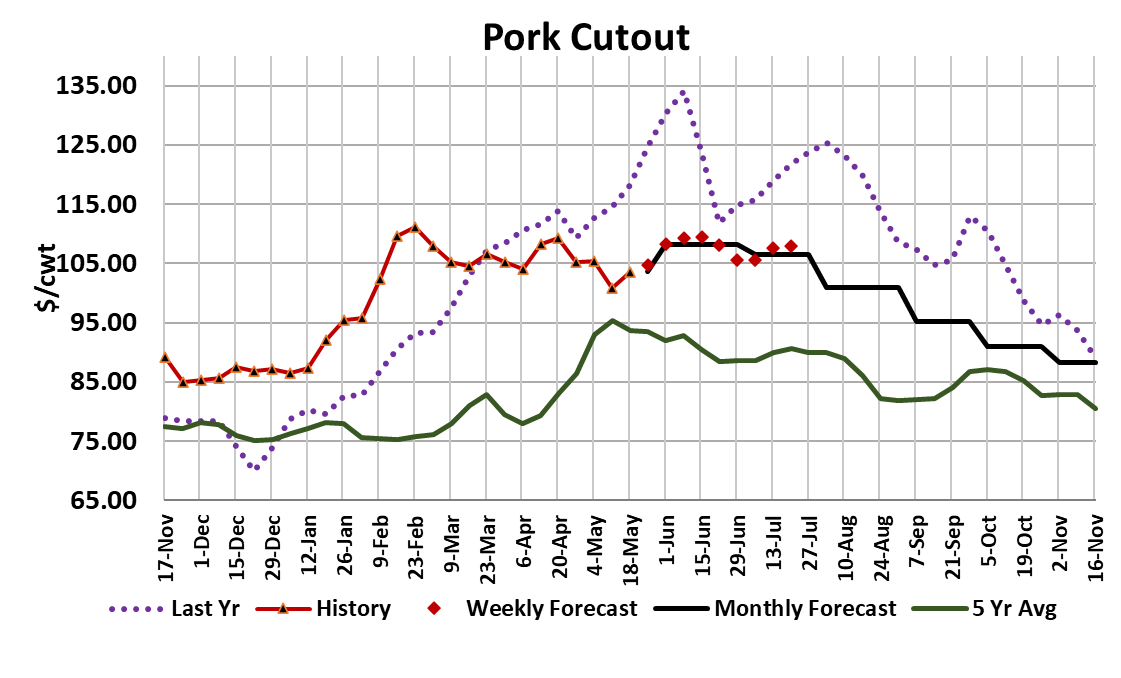

The pork cutout rebounded this week, gaining $2.80/cwt to average

$103.57. That is still a bit below the $106 average that has

characterized the pork market since the middle of February, but does

help erase some of the bearishness that was prevalent the week

before when the cutout dipped below $100 and thus enabled the May

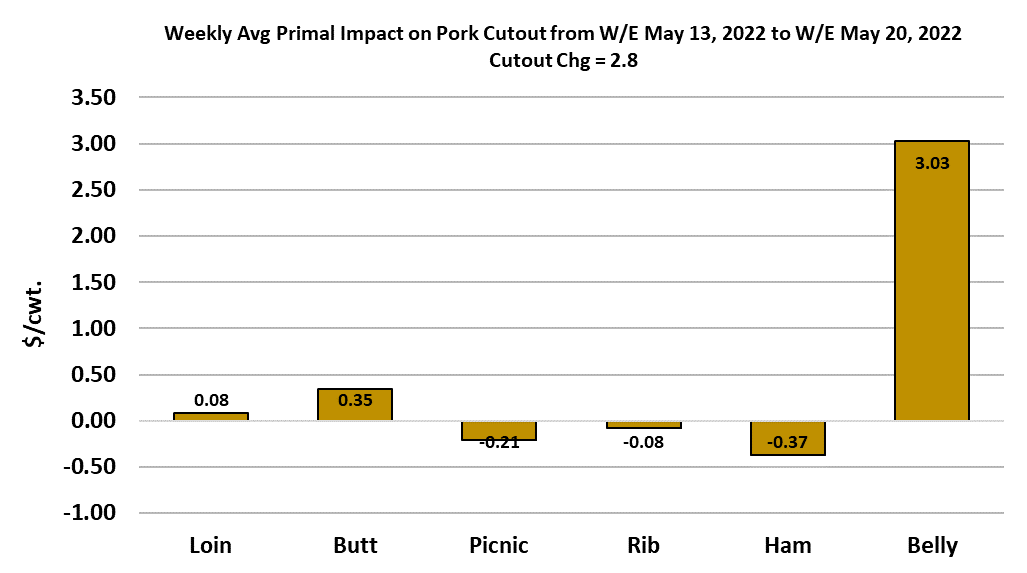

lean hog futures to expire near $100. The attached chart shows that it

was gains in belly pricing that were largely behind this week’s cutout

improvement. Hams also showed some price gains, but they started

the week with a couple of low prints, so the weekly average didn’t

reach the previous week’s level. All of the retail primals were rather

ho-hum—just churning along in a sideways pattern as they have been

for the past couple of months. It has really gotten to the point where

movement in the cutout is primarily dependent upon price changes in

either the bellies or the hams. Of course it won’t stay that way forever,

but right now that seems to be program. The negotiated hog market

moved higher this week, with the WCB adding $1.74/cwt on a weekly

average basis and the National negotiated market up $3.23/cwt.

Those gains, combined with the improvement in the cutout, helped to

break the LHI out of its downtrend and got it moving higher toward the

end of the week. Further gains in the Index are expected next week as

the negotiated improvements flow fully into the calculation. If the

cutout and the cash hog market were to remain where they were at the

end of this week then the LHI should move into the $104-105 range.

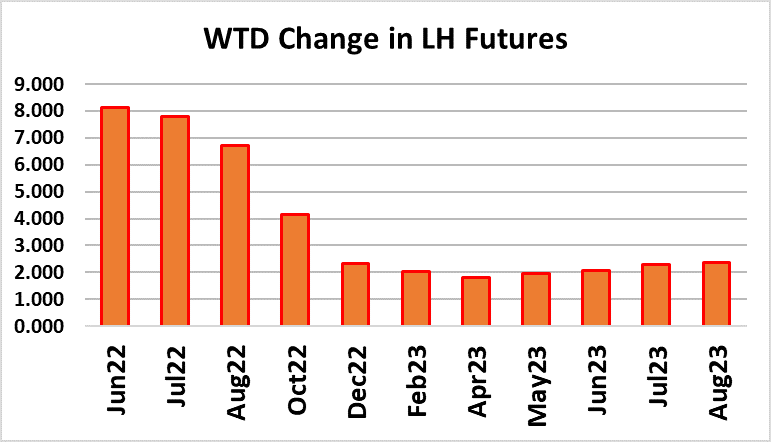

Of course, futures traders got excited about the cash market

improvements and added $8 back on the Jun and Jul contracts after

taking almost $6 off of the Jul contract the week before. This is

characteristic of a directionless market, where traders simply react to

the day-to-day movements in the cash market fundamentals. Right

now it looks to traders like the market is going up, but in reality it is

probably just coming back toward that $106 average cutout that has

been the norm for so long. In order to reach the $109 value that

traders put on the Jun contract today, the cutout is going to need to

break out of its trading range and move above $110.

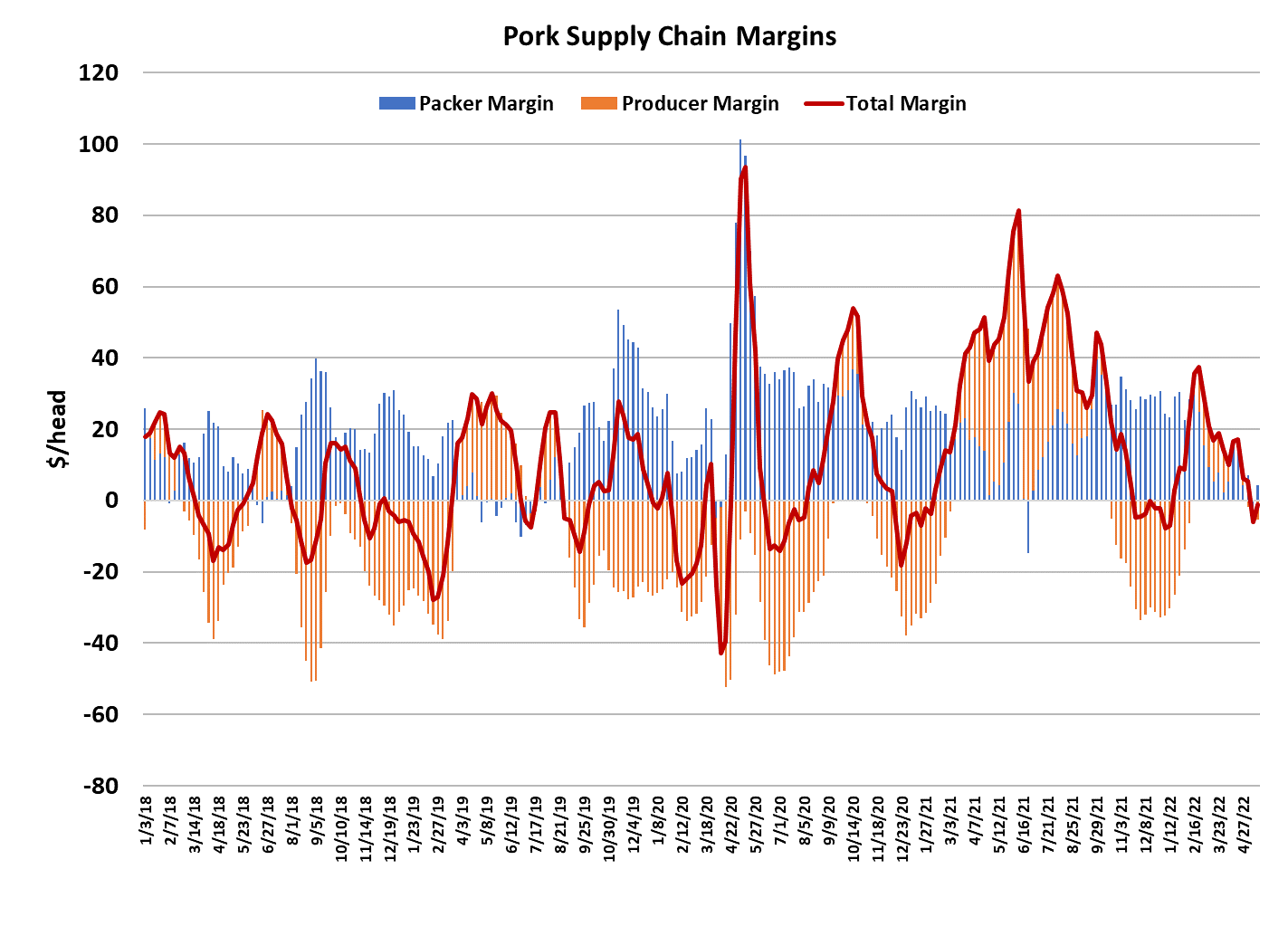

The combined margin moved a little higher this week and although it

looks like it might have bottomed just below the zero line, I want to see

how next week’s data comes in before declaring that demand has

moved back into an upcycle. All of the last-minute buying for Memorial

Day is now behind us, but that was probably more important for the

retail primals than for the processing items. If both the hams and

bellies can move higher together, then that would be a powerful force

that could take the cutout several dollars higher next week. However,

even if demand is beginning a new upcycle, I suspect that it won’t be a

very long one or a very robust one given all of the demand-defeating

elements of the macroeconomy right now. Inflation, high energy prices

and a declining stock market should all work to temper pork demand in

the longer run.

Normally at this time of year, I would be pointing to shrinking pork

supplies as a supportive factor for hog and pork prices, but we actually

saw the kill increase this week to 2.41 million head. That is very similar

to the kill levels we saw back in March. It may be that packers are

anticipating doing a very small Saturday kill next weekend (Memorial

Day weekend) and thus are trying to build some inventory to

compensate. In any regard, it will be interesting to see if that puts

pressure on the pork market next week. This week’s kill was about

70,000 head greater than what the Sep/Nov pig crop implied and marks

the fourth week in a row where the industry has overkilled the pig crop.

That seems to suggest that there are plenty of market-ready hogs out

there, but the rise in negotiated prices this week suggests otherwise.

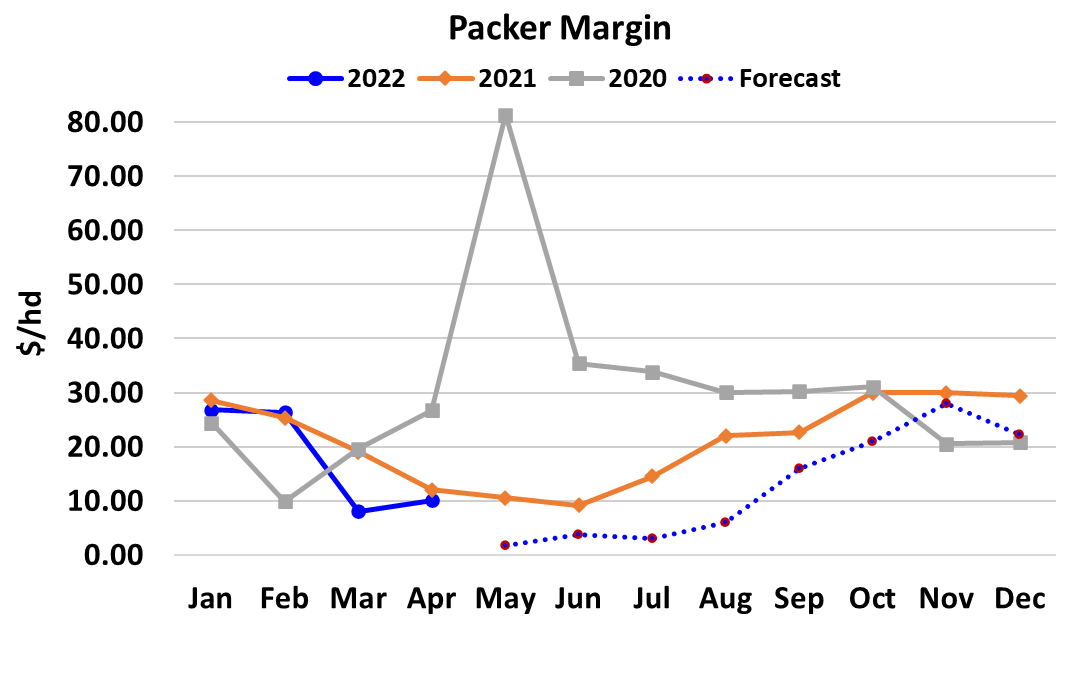

Packer margins improved this week to about $4/head after being -$2/

head last week. I suspect that packers are going to struggle with

margin problems for the next couple of months.

Recall that the industry added several large packing plants back in

2018-19 in anticipation of growing export demand and a bigger hog

herd. Well, now export demand is in decline and high input costs

are causing producers to shrink the hog herd. If plants want to run

at a reasonable capacity utilization rate, they may be forced to chase

hogs this summer and that could have a detrimental impact on

margins. If they have to chase hogs while demand is declining, that

would be particularly bad for their profitability. Hopefully, demand is

going to turn higher soon and a stronger cutout this summer will

leave packers more room to pay up for hogs. It doesn’t look like the

export market is going to bail them out this summer. China is still

dis-interested in S pork and that could get worse as COVID

lockdowns and port congestion continue. There is a good possibility

that China’s economy is going to slump throughout the balance of

2022 and that wouldn’t be good for US pork exports. Producers

are still struggling to turn a profit, despite the triple-digit cutout and

hog pricing.

High input costs have now pushed their breakevens close to $103/

cwt. That could lead to further reductions in the breeding herd and

smaller supplies down the road. We get another look at the breeding

herd when USDA releases the next edition of Hogs and Pigs on June

29. Corn futures pulled back a bit this week, but given that the crop

is not even fully planted, I don’t expect traders to let it decline a lot more

from here. As long as there is war in Ukraine and oil prices are in triple

digits, it is a good bet that corn will remain above $7/bushel and could

go as high as $9-10/bushel under the right circumstances. Next

week, watch the cutout to see how it is going to respond to this week’s

larger-than-expected production. If we do see further increases, that

will likely add to the bullishness in the nearby futures and most

likely will push it well above what it is capable of achieving before

the Jun contract expires in three weeks.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}