Pork Wrap May 19

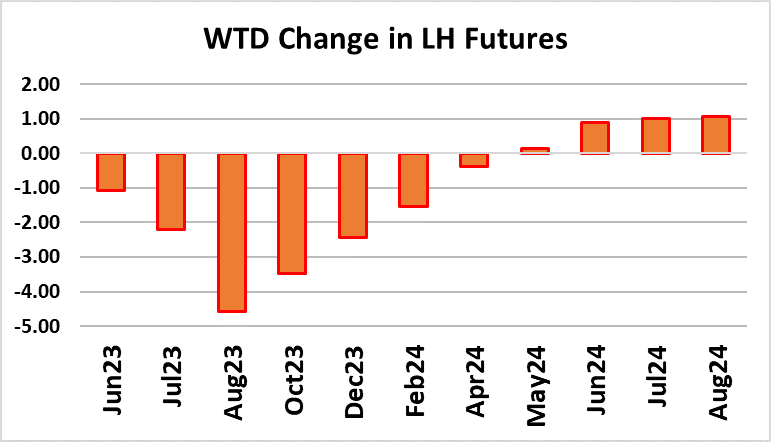

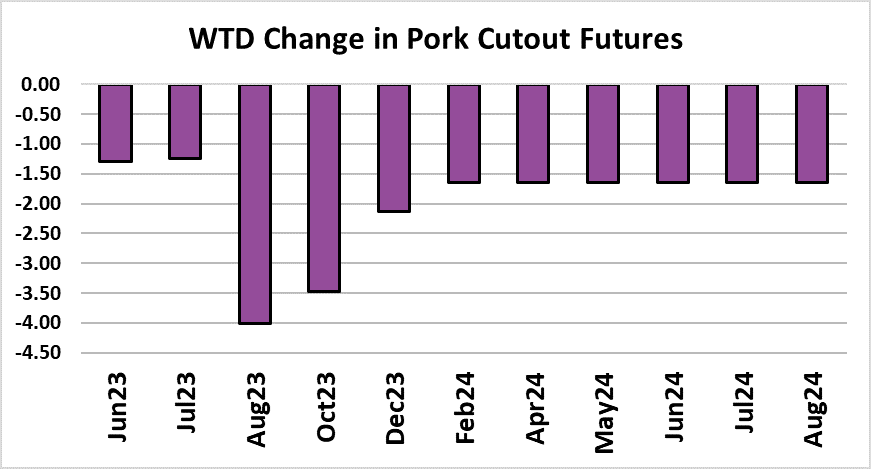

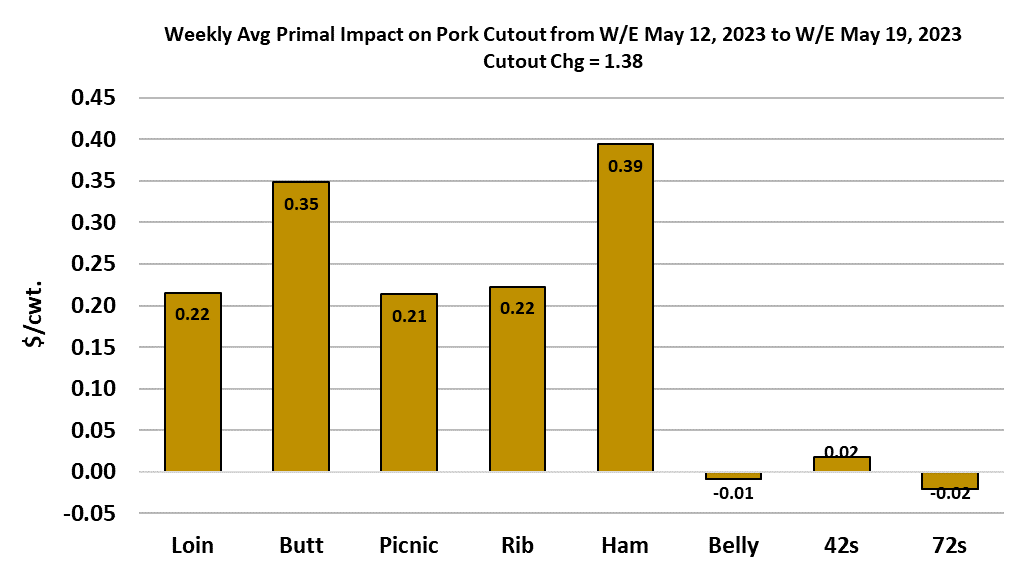

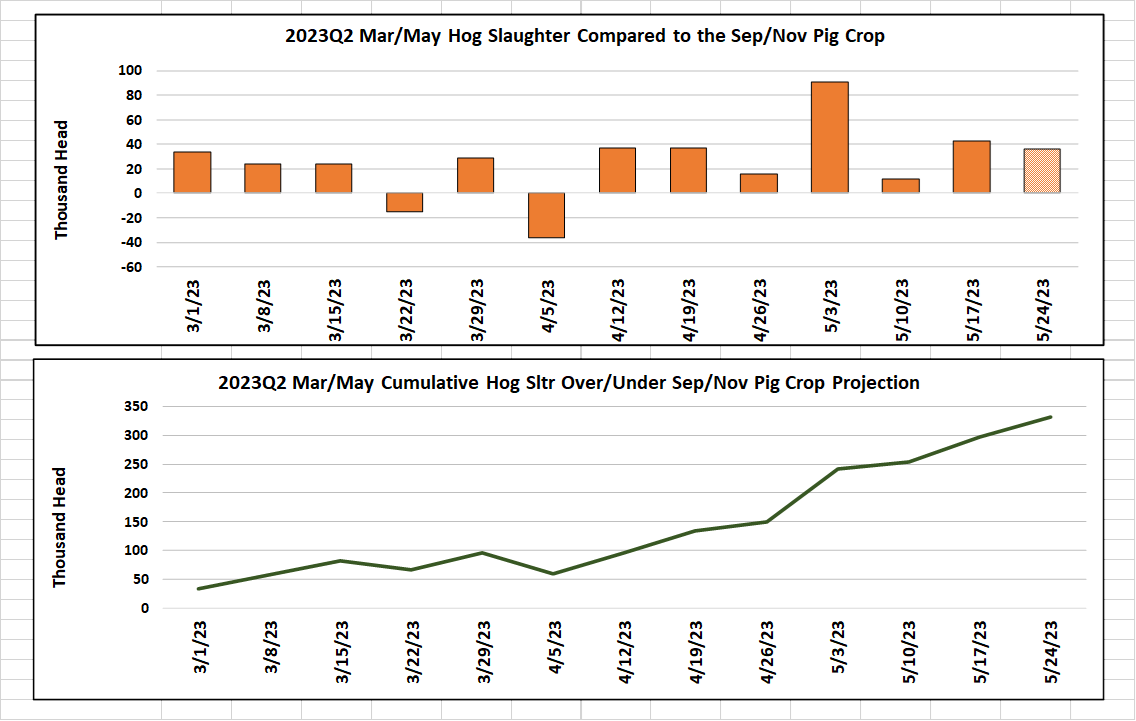

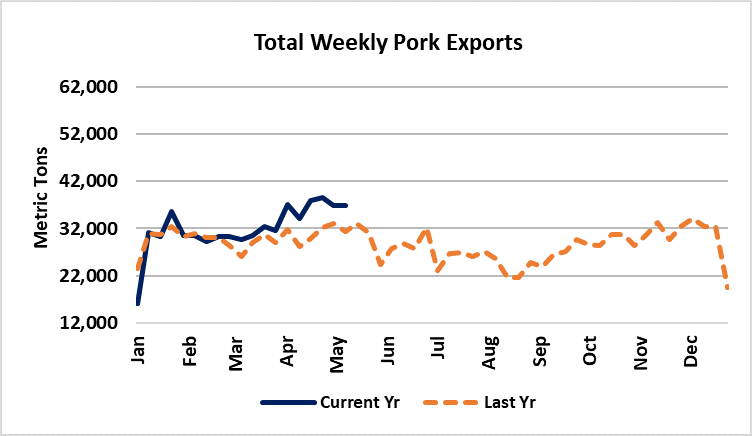

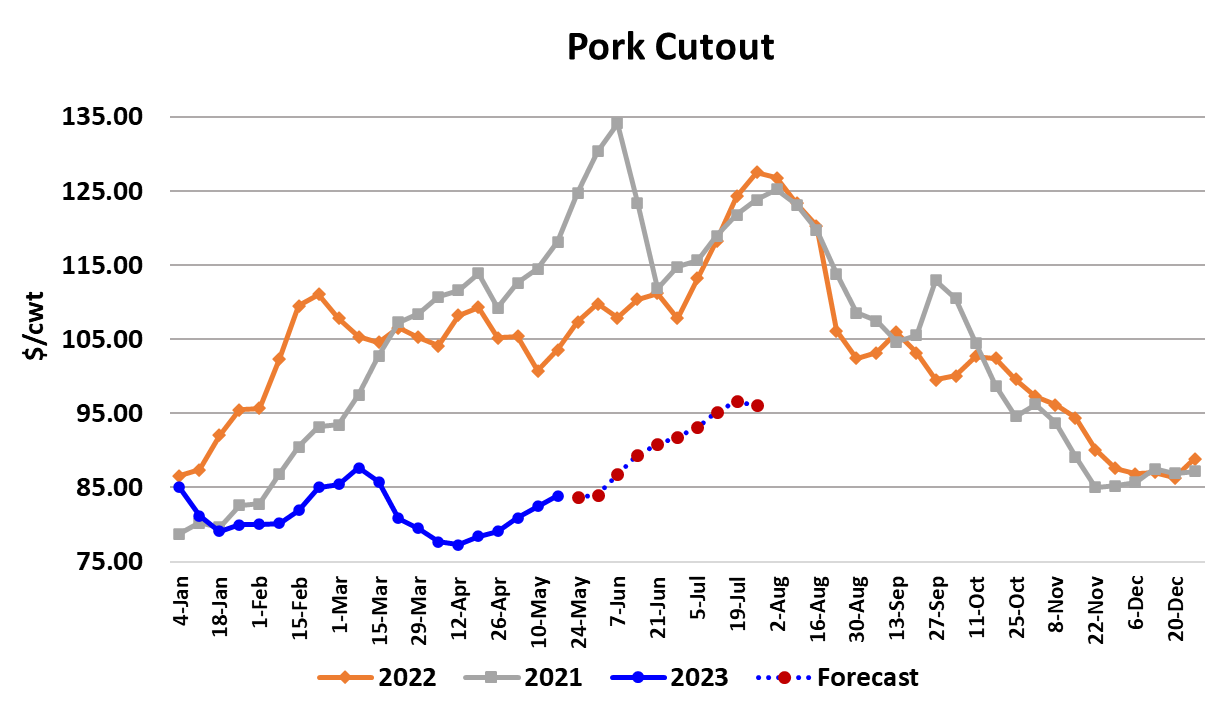

For the fifth week in a row, the pork cutout was up just a little over a dollar, averaging $83.86/cwt. The slow, steady climb in the cutout represents some very modest demand improvement and slowly declining pork production. But the pace of price improvement has been glacial and that is very unusual at this time of year when it is common for prices to move higher at a much faster clip. The futures market expressed its disappointment this week by taking $4 off of the Aug contract and over $2 off of the July this week. Cash hog prices, on the other hand, made solid gains, with the WCB negotiated market averaging $7.25/cwt. higher on the week. Hog supplies have dipped to the point where packers are having to compete a little harder to round out their weekly kill schedules, particularly in the WCB region. One or more packers seems to come into that market during the middle of the week and purchase larger-than-normal volumes at higher-than-prevailing prices. It is the same pattern that we saw last summer and early fall when hog supplies were tighter. It is an interesting phenomenon and often it gets the futures excited to see the cash hog price jump several dollars on a Tuesday or Wednesday, but by the end of the week, some of the gains have been given back. This week was a little different in that there wasn’t much retreat in the WCB price toward the end of the week. In any case, packer margins are getting compressed as cash hog prices rise faster than the cutout. I calculate this week’s packer margin at a little below $7/head, down about $3 from last week. The margin is likely to get worse next week once all of this week’s gains in the negotiated markets become impounded in the Lean Hog Index. That is, unless packers can find a way to move the cutout upward more than they have recently. One of the problems that packers face is that ham demand seems to be running out of steam. Hams have been the primary pillar of support in the cutout over the past couple of weeks, but this week we saw the 23/27 lb. ham quotes turn lower, even though the ham primal was up slightly on a weekly average basis. This bears watching. The cutout is getting a little more help from the retail primals, with all of those up modestly on the week. Trim pricing is still very soft, however. I think a big part of the problem here is that we just haven’t seen the kind of kill reductions that normally happen at this time of year. This week’s kill came in at 2.41 million head, up 40k from the week before. Here we are in the third week of May and kills are still above 2.4 million head! You can see from the attached chart that we are still over-killing the Sep/Nov pig crop and if my forecast for next week’s kill is close, then for the March/May quarter as a whole, the industry may over-kill by about 320,000 head. That is after USDA revised the Sep/Nov pig crop downward in the March Hogs & Pigs report. So it turns out that the initial estimate on the Sep/Nov pig crop was way understated. Should we expect more of the same in the upcoming Jun/Aug quarter? Possibly. That doesn’t bode well for producer margins this summer. Next week, the kill will be curtailed a bit by packers reducing Saturday shifts on Memorial Day weekend. I’m expecting a kill in the 2.32 million head area. After that, slaughter during the holiday week might only be 1.85 million head. So, there should be some supply tightening just around the corner and maybe that will help move pork prices higher at a little faster pace. Assuming no serious over-killing of the summer pig crop, I’d look for the lowest non-holiday weekly slaughter to come in around 2.28 million head in late June or early July. By the time we reach the end of August however, weekly kills should be back close to 2.5 million head again. The window opportunity is small, but just ahead, for hog producers to improve their margin situation. The rise in cash hog prices this week helped, and I calculate producer margins at -$47/head this week. The forecast currently has producer margins moving as high as the negative low single digits during July, but no positive margins at all. It is a long year indeed for hog producers when the summer doesn’t bring any positive margins. Fortunately for them, corn futures have been coming down at a fairly rapid pace and if that continues they will get some relief on the cost side of their profit equation. They cannot, however, fix what is wrong with pork demand. They are at the mercy of retailers and consumers on that one. All they can really do there is liquidate breeding stock and thus curtail production to the point where it better equates with the new, weaker demand environment that has emerged in 2023. Export markets could provide a bit of a lifeline and we have seen international interest in US pork pick up in recent weeks. The US has some of the cheapest pork in the world right now and savvy foreign buyers are beginning to take advantage of that. A new variant of ASF is spreading in China and there has been some speculation that at some point China will need to greatly increase its pork imports. I’m not sure that dangling that carrot is enough to keep US producers from liquidating, partly because the last ASF crisis in China didn’t yield near the benefit to US producers that some were expecting. Hog weights are now in their normal seasonal downtrend and there is much warmer weather coming to the Midwest in the next couple of weeks, so that should also help to limit production somewhat. After several months of repeated underperformance in the cash markets, futures traders are not very interested in being long in this market environment. We now have every contract on the board trading below what my fundamental analysis would say is fair value, but the bulls have had their nose bloodied so many times that they are just ready to trade something else. Next week, watch those hams for signs of further softening, because that is a big risk to the cutout, and watch the negotiated hog markets for another mid-week price surge.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}