Pork Wrap May 17

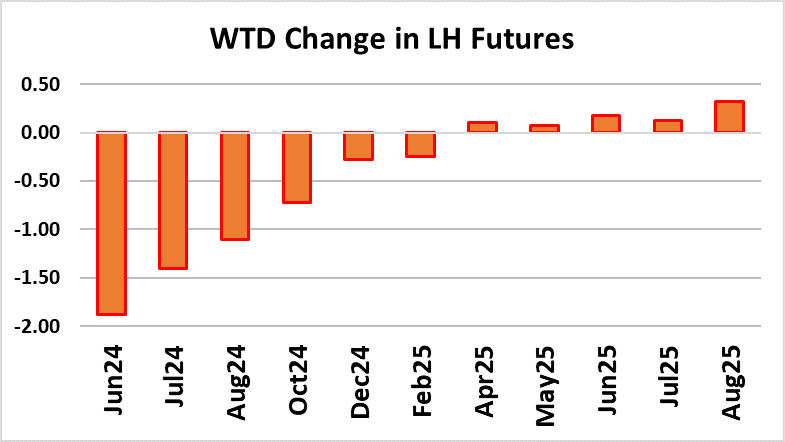

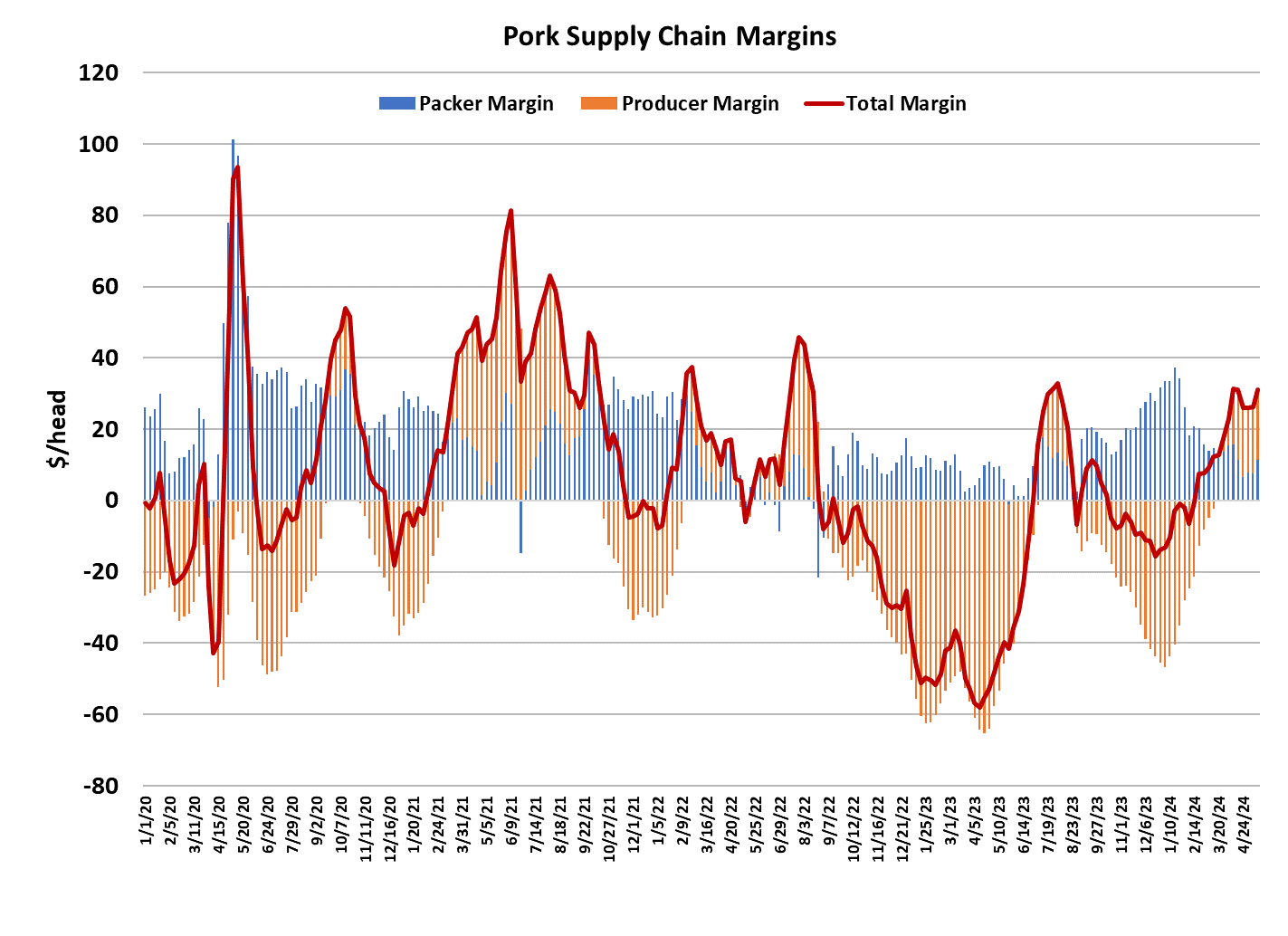

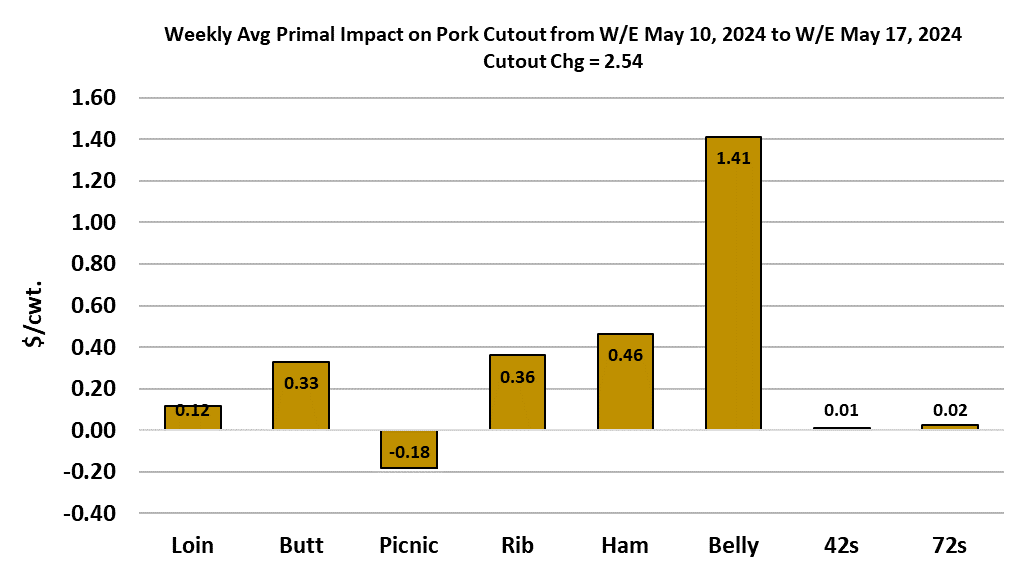

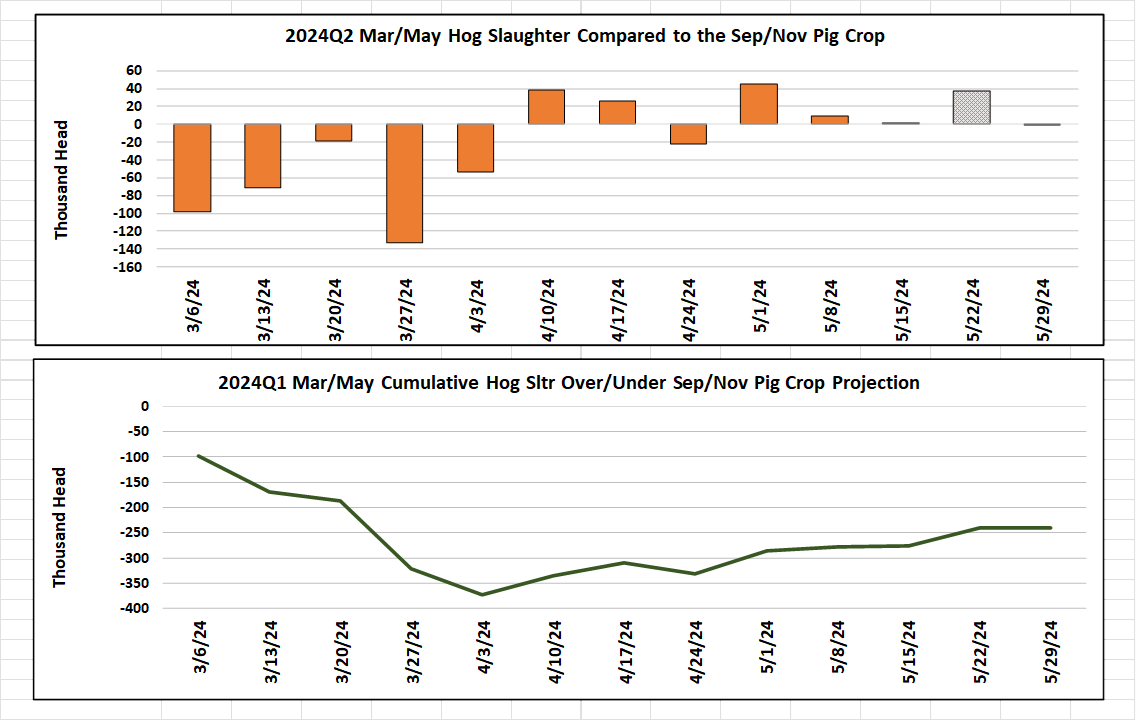

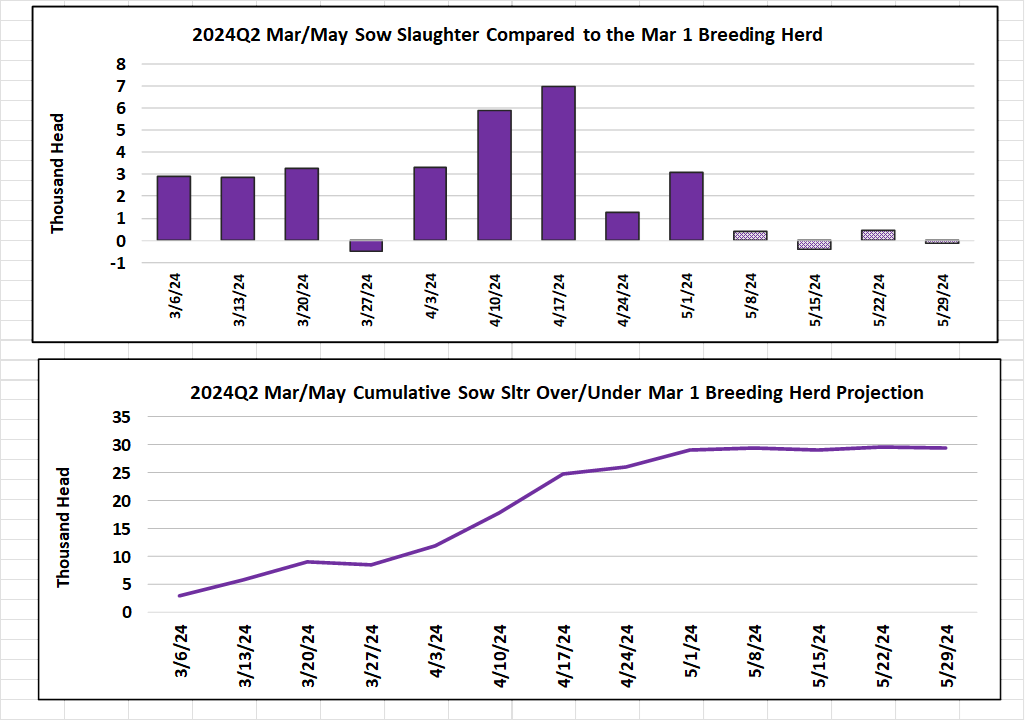

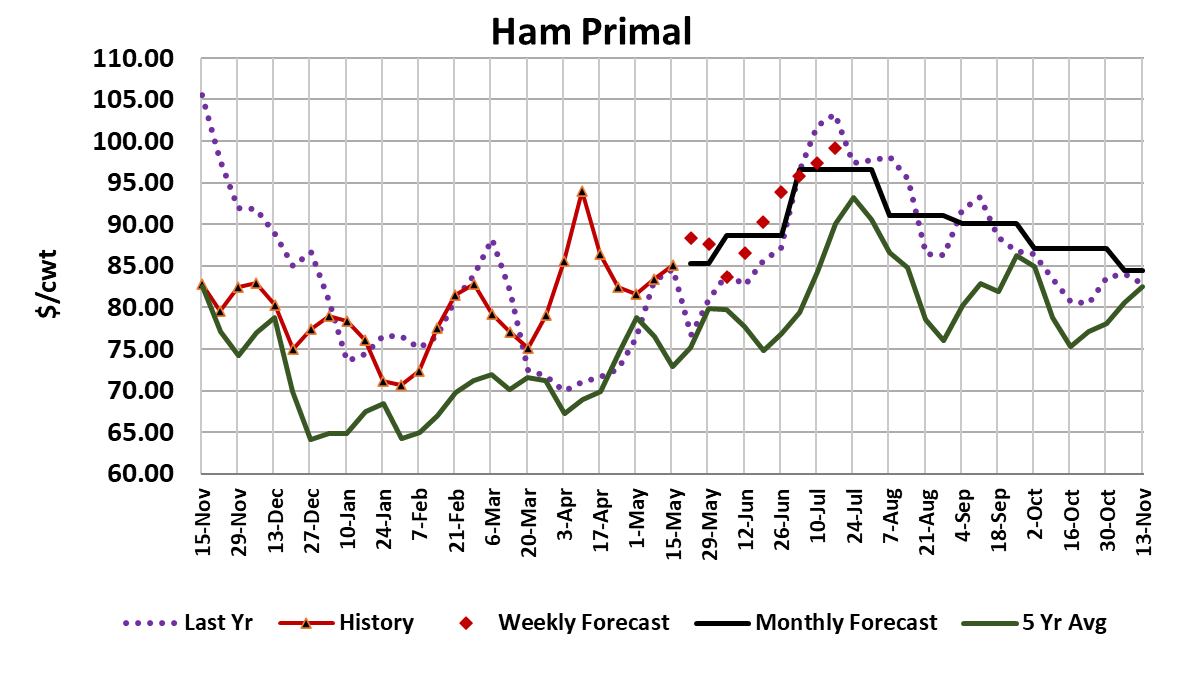

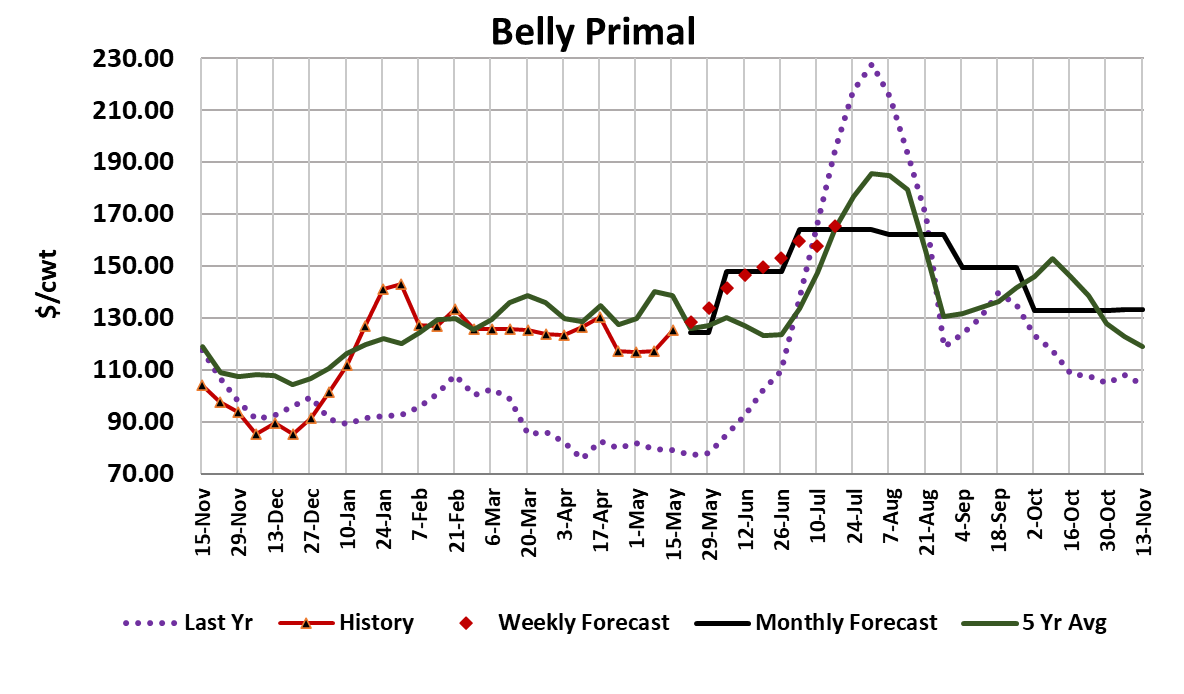

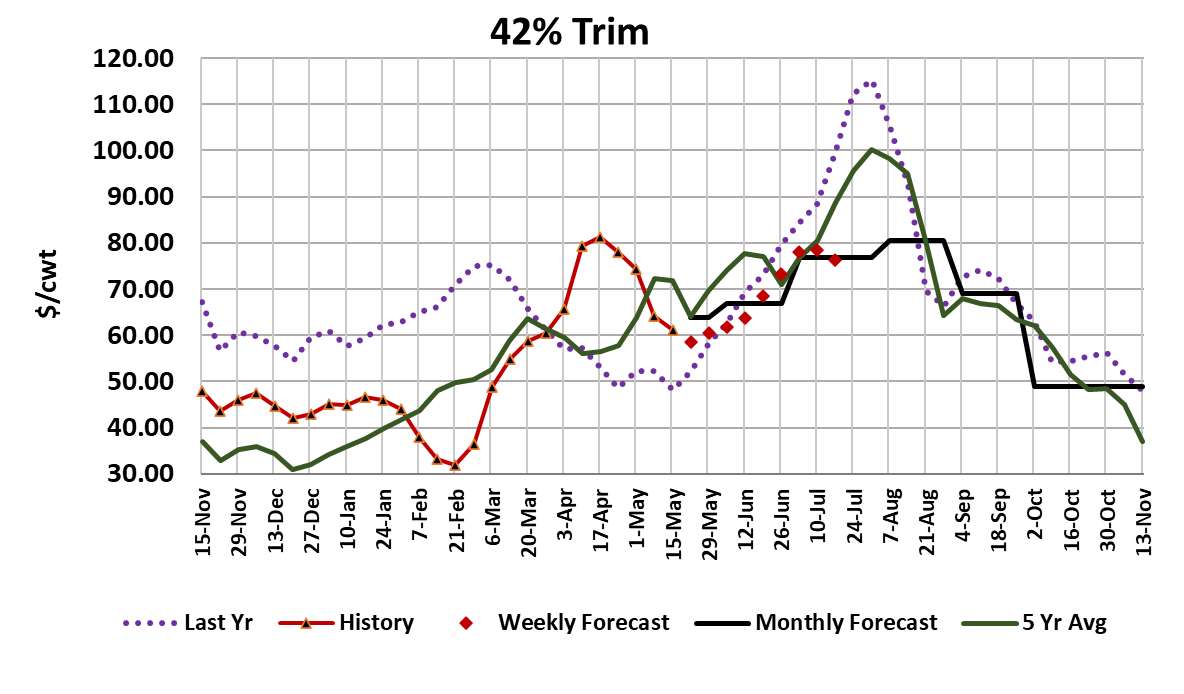

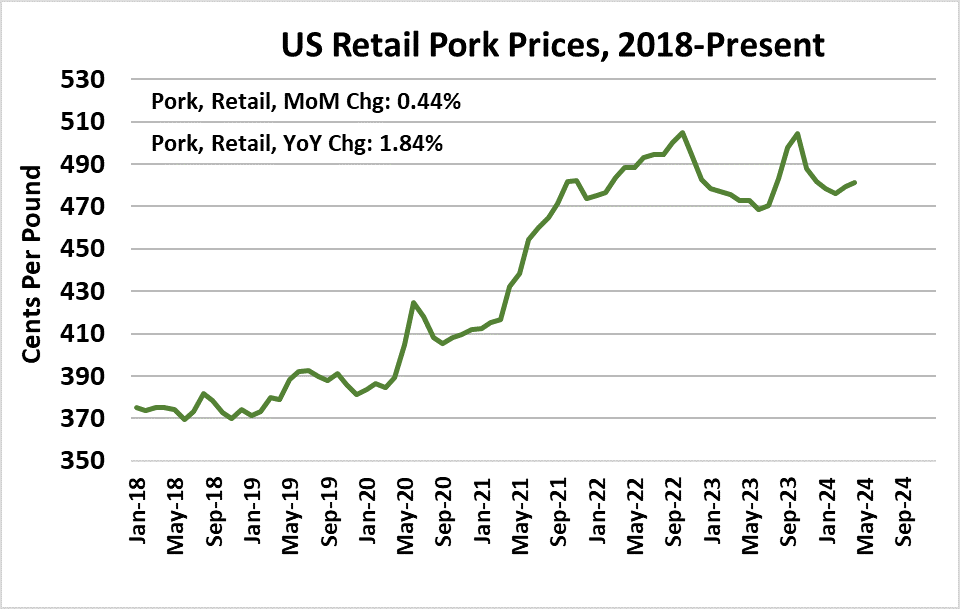

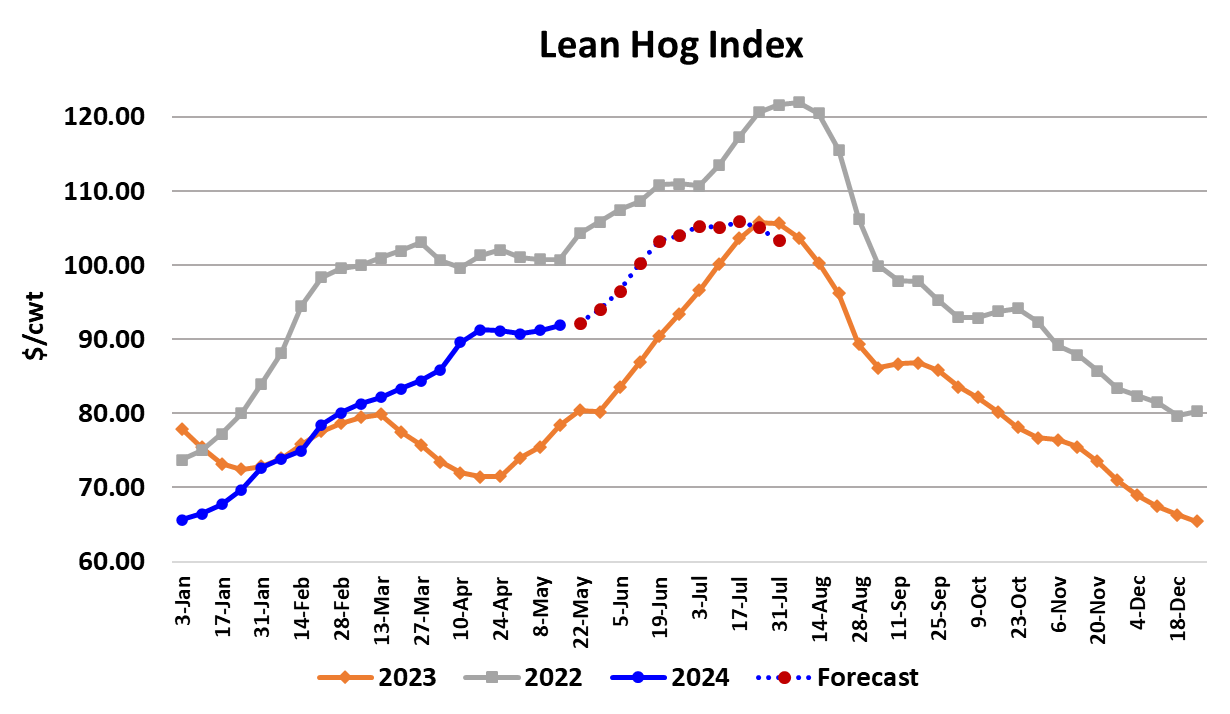

After three weeks, where it was stalled at $98, the pork cutout regained some upward momentum this week, averaging $101.35. That feat was accomplished largely due to gains in belly prices, although the hams also provided support. The surprising feature of this week’s market was that negotiated hog prices did not follow the cutout higher, and actually lost ground. Negotiated prices in the WCB region dropped $2.28 to average $89.48 for the week. With the cutout advancing and hog prices dropping, packer margins expanded and now sit close to +$11.50/head. In the previous three weeks, where the cutout was stalled, packer margins were mostly in the $6-8/head range, so this week’s events have lifted the near-term profitability prospects for packers. I’m expecting margins to remain in double digits for at least a couple more weeks before seasonal shrinkage in the availability of spot market hogs causes packer margins to turn south again. This week’s slaughter clocked in at 2.40 million head, about 25k larger than the week before, but very closely aligned with what the pig crop would have projected. With only two slaughter weeks left in the March/May quarter, it looks like the industry will under-kill USDA’s estimate of the Sep/Nov pig crop by about 300,000 head. Next week’s kill should be tempered by lighter-than-normal slaughter on Friday and Saturday as packers will cancel some shifts to give workers more time off over the holiday weekend. The following week, there will be zero slaughter on Monday, but packers should put in a relatively large Saturday harvest to help catch up. I’m forecasting total slaughter during Memorial Day week at 2.14 million head. After that, the industry will start working on the Dec/Feb pig crop, which was estimated to be 1.9% bigger than in the previous year, suggesting that weekly slaughter levels will also be larger than last year. The current forecast has slaughter during the first three weeks of June near 2.4 million head per week, not all that different from what we have experienced so far in May. Barrow and gilt carcass weights held steady at 213 pounds again this week and haven’t yet started their seasonal move lower. That doesn’t seem to be causing any problems since the de-trended and de-seasonalized weights are still at relatively low levels, suggesting that producers are staying current on their marketings. The weather in the hog growing regions has been relatively mild so far during May, so perhaps that helps to explain why weights are a little slow to start moving seasonally lower. The weather forecast for the next couple of weeks also looks pretty mild, so there is not much concern about weather-induced performance losses at present. Sow slaughter continues to run large relative to the reported level of the breeding herd on March 1, suggesting that producers are still making an effort to shrink the herd. Our next read on the size of the breeding herd will come on June 27 when USDA releases its quarterly Hogs and Pigs report. I focus on the hams and bellies every week because those two primals have the most potential to cause big changes in the cutout. This week the ham primal averaged about $1.70 higher than the week before but appeared to be running out of gas as the week progressed. The ham primal has been up for two weeks in a row could be nearing the point where it turns lower again for a couple of weeks. That would spell trouble for the cutout unless the belly primal steps up to fill the void. This week’s $8 advance in the belly primal was the first substantial gain in almost a month. We are at the point in the calendar where foodservice entities start preparing for increased sales due to the end of the school year and the beginning of vacation season, so belly demand should be strengthening. The danger is that belly buyers may have become complacent and short bought after months of mostly sideways pricing in the wholesale market and that could lead them to bid belly prices up rapidly as product availability tightens due to short kills around the holiday weekend. Last spring we saw a similar thing happen in early June that carried the belly market to a peak in July that was about three times the price level seen in May. One concerning feature of the market is that fat trim prices have been on the defensive for over a month now and may very soon move back below last year’s level. I still think they will eventually rally in summer as weights come down and kills shrink, but often the trims can be leading indicators for yet unrealized problems with demand in other parts of the carcass. Memorial Day should be good for pork demand with smoker items such as butts and ribs getting a high degree of ad space. If consumers really are feeling financial stress from inflation as many market observers have suggested, then maybe they will forgo the beef steak this year in favor of pork chops. Retail pork prices for April were released this week and they were up 0.4% from March and 1.8% stronger than last year. That makes sense given that wholesale pork prices, as measured by the cutout, are currently running about 20% stronger than last year. Futures traders are struggling with the slow pace of the cash markets for both hogs and pork. The May contract expired on Tuesday at $91.76, only about $1 higher than where the Apr contract expired. Traders have tried putting bigger premiums on the Jun contract, but the cash markets never seem to be moving fast enough to justify it, so it evaporates quickly. The Jun nearly touched $99 this week, but it was quickly reversed when the cutout failed to follow suit. As of Friday’s close, Jun is holding a little over $4 premium to the LHI and, while that seems rather small for a period of the year when prices are often escalating rapidly, the bulls have been burned enough times that they are understandably cautious now. The fundamental forecast has fair value for Jun close to $100, but that may prove to be too high unless the bellies can begin to post rapid gains. Next week, watch the hams because they could be on the verge of turning lower and that would be a headwind that the other primals might have a difficult time overcoming. Also, expect further modest gains in packer margins as the negotiated cash hog markets don’t currently seem to be able to keep up with advances in the cutout.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}