Pork Wrap May 14

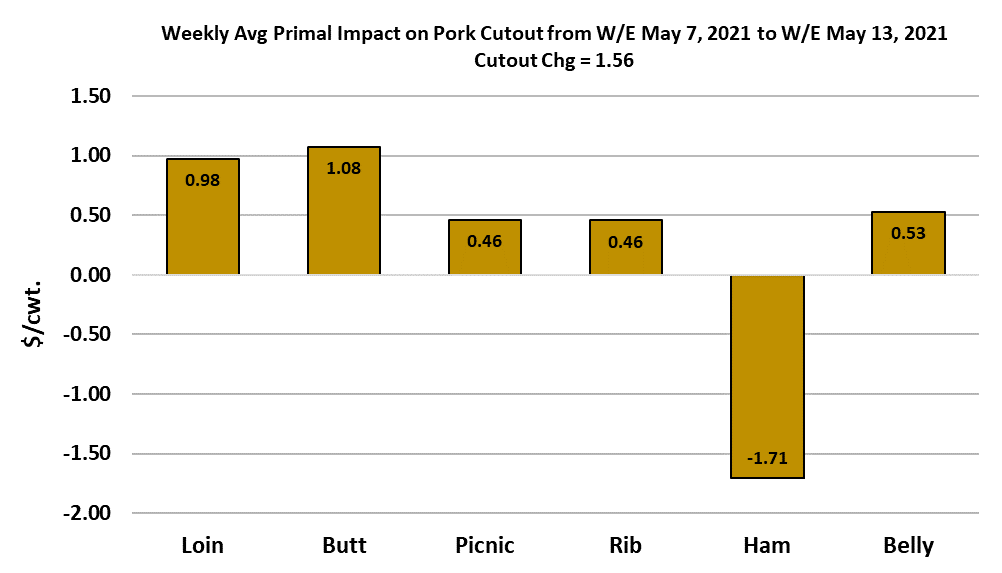

The pork cutout inched a little higher this week, adding $1.56 on a

weekly average basis. In the cash hog market, the WCB

negotiateds added only $0.33/cwt, while the LHI was up $2.25.

The bigger gain the LHI compared to the negotiated market reflects

some catching up that the LHI needed to do following last week’s

strong rally in the negotiated market.

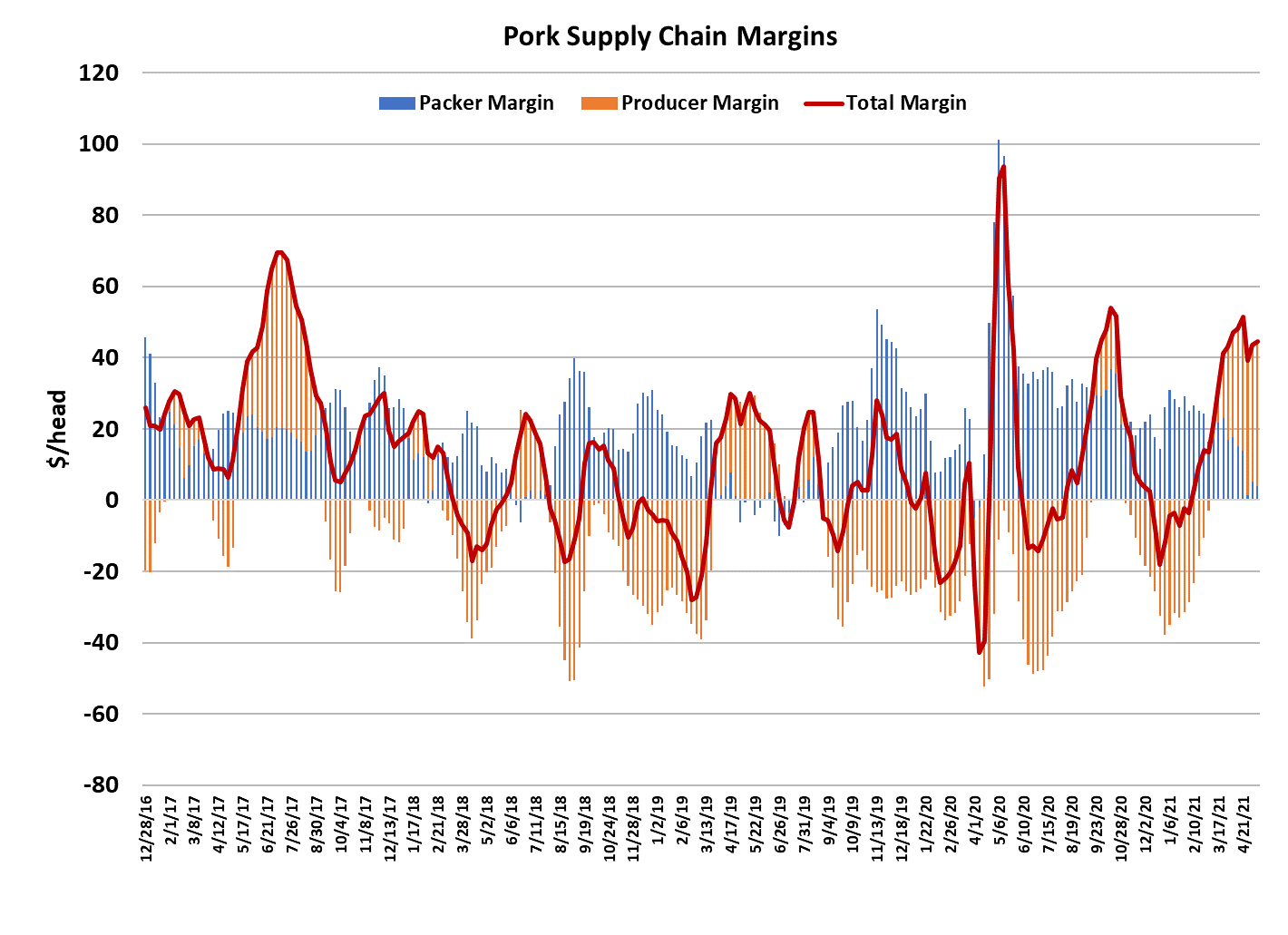

Packer margins moved about a dollar lower, now close to $4/head.

Last week, packers did very little in terms of a Saturday kill and I

suspect they may do even less this week. They are having

difficultly staffing plants and margins are not great anyway, so why

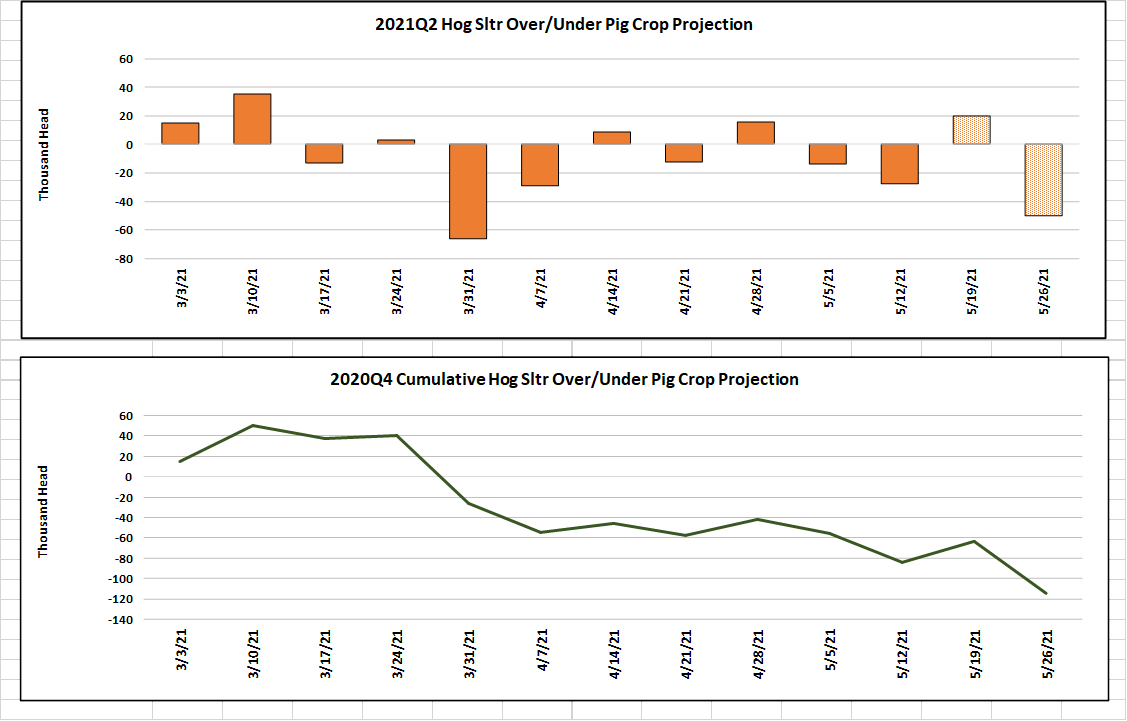

not let the Saturday kill go to almost nothing. By my estimate, this

week’s kill should come in very near 2.4 million head, which is not

all that different from last week’s total. It is however, about 30k

below what the pig crop implied. So, with two weeks to go in this

pig crop quarter, the kill is running 80k below the pig crop and that

may slip another 20k between now and the end of the month. So,

hog slaughter is beginning to tighten down seasonally.

Carcass weights are also starting their seasonal descent. This

week’s weight data showed a 1 pound drop in barrow and gilt

weights and the IA/S. MN liveweight data suggested the FI weights

will print lower again next week. The DTDS weight is now

registering -3, which is very low and an indicator that hog

producers are current on their marketings. Thus, I don’t really see

any surprises on the supply side of the market. Negotiated hog

prices have slipped off of their highs by about $3 in recent days

and that may indicate that a near-term top has been made in the

negotiated market. However, it is certainly conceivable that cash

hog prices resume their march upward as hog supplies tighten

further in June and July.

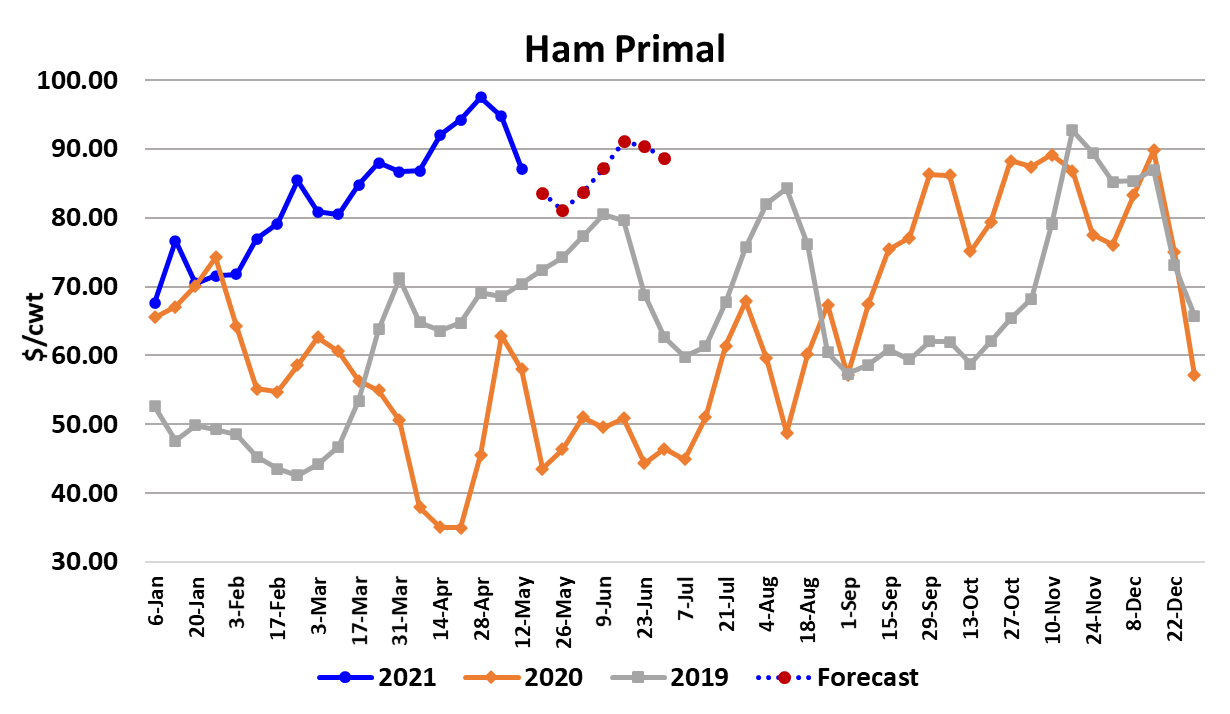

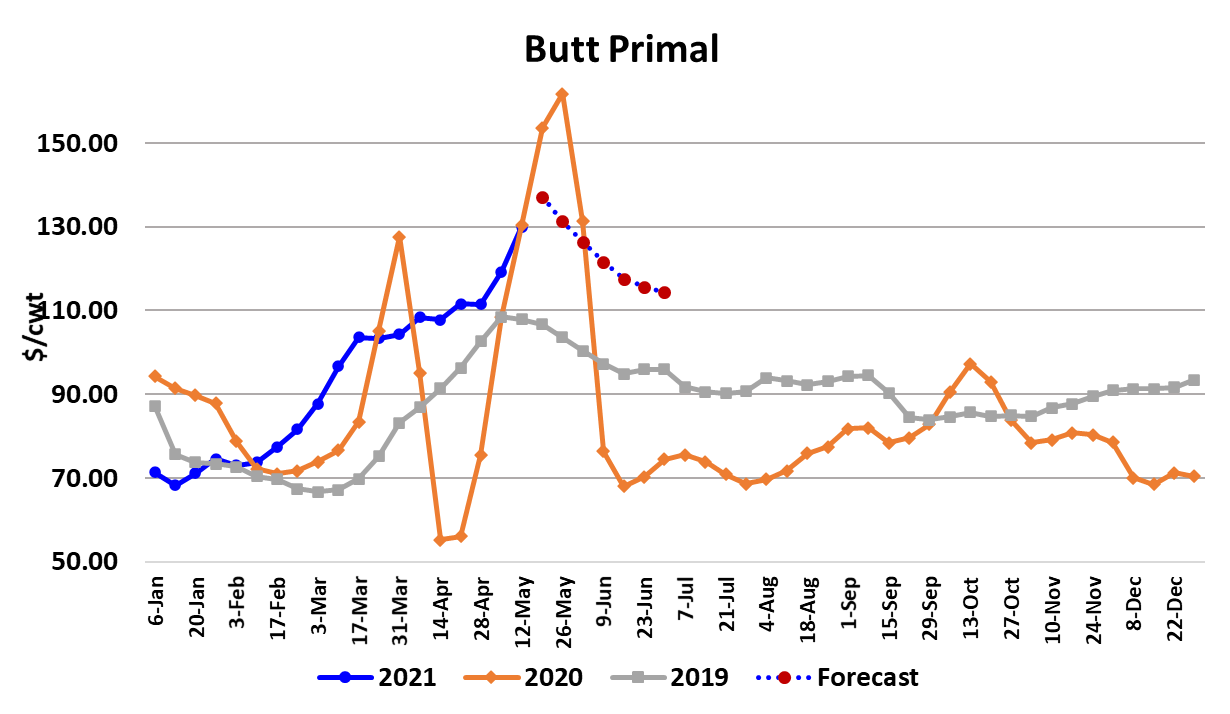

On the demand side of the market, we are seeing very strong

demand for the retail cuts—loins, butts, ribs. The weak sister in the

cutout is the ham primal, which has dropped $10 over the past two

weeks. The combined margin chart made a goofy little bend higher

this week, so I’d say that we are still inconclusive as to whether or

not the current strong demand cycle is nearing its end. Even bellies

managed a modest gain this week, up about $3.50. We are really

close to the point where the Memorial Day buying dries up and I

suspect that the retail cuts will start to ease lower once that point is

passed.

That means that the cutout could soon start moving south,

although I don’t expect that it will do so at a strong clip. Instead,

I’d look for a $1-2 drop in the cutout, on average, each week

between now and the end of June. That would still leave the

cutout somewhere in the $105-110 range moving into the first

week of July.

I’m expecting packer margins to work lower from here and turn

modestly negative in June. In the context of the LHI, the lower

cutout is bearish, but the smaller margin is bullish and those just

about wash each other out so that the LHI remains in the

$108-111 range through May and for most of June. Grain

markets came crashing down near the end of the week and that

took some of the air out of the deferred hog futures. However,

grain futures are at that point in the calendar when volatility is

near its annual high, so I think we can expect to see many more

wild swings, both up and down, in the corn and soybean markets.

That will move the deferred hog futures up and down as well.

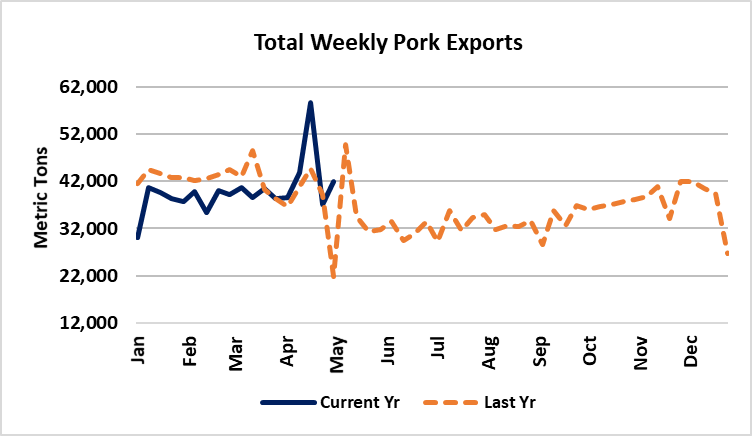

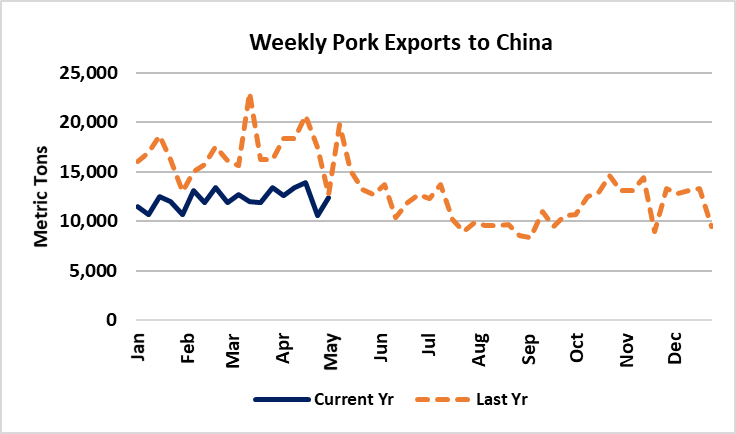

Export markets also seem to be stuck in a sideways pattern, with

reported shipments running around 40k MT per week, outside of

the weeks where reporting anomalies cause spikes. Even

shipments to China remain in the same sideways pattern they

have been in for most of 2021. It is actually pretty impressive that

international demand has been able to hold steady in the face of

rising US pork prices this spring. That may be an indication that

this strong demand environment is not limited to just the US, but

is part of the fundamentals in many other countries. Next week,

watch the hams for signs of further deterioration and be prepared

for a topping in the retail cut markets.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}