Pork Wrap May 13

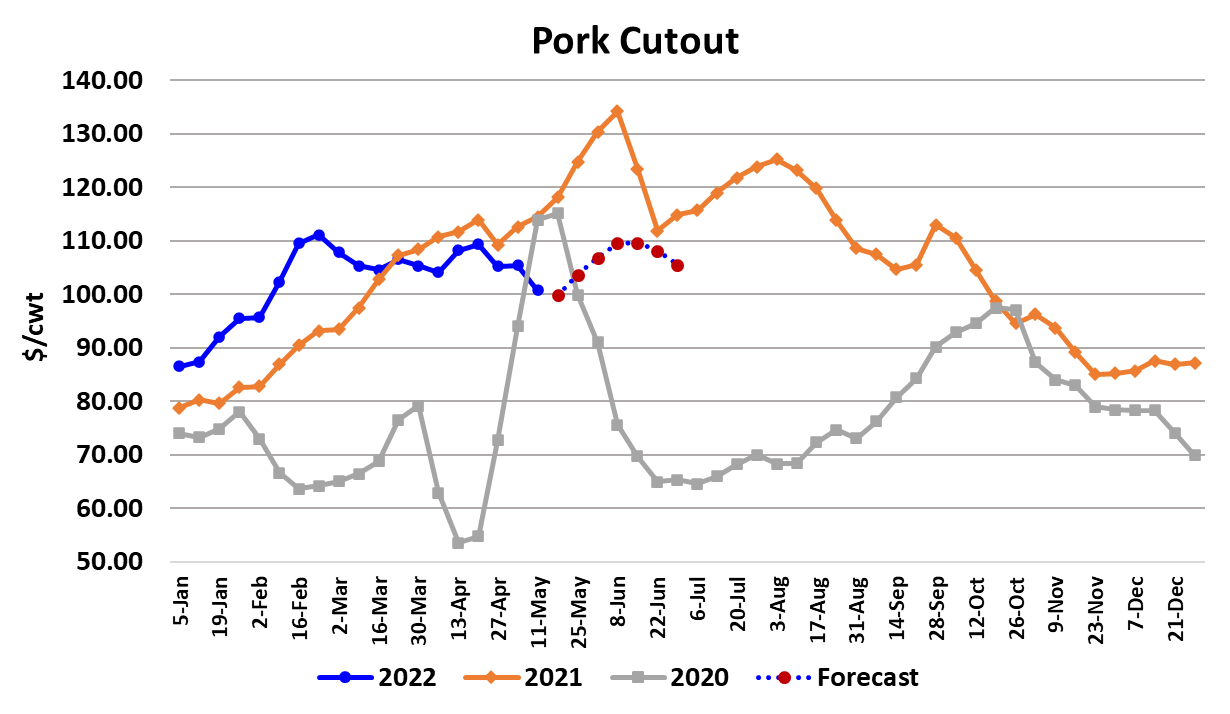

After months of being stuck at roughly $105, the pork cutout finally

moved lower this week, averaging $100.77. A downturn in ham

prices combined with already soft belly prices to take $4.62 off of the

cutout this week. While the cutout was moving lower, cash hog prices

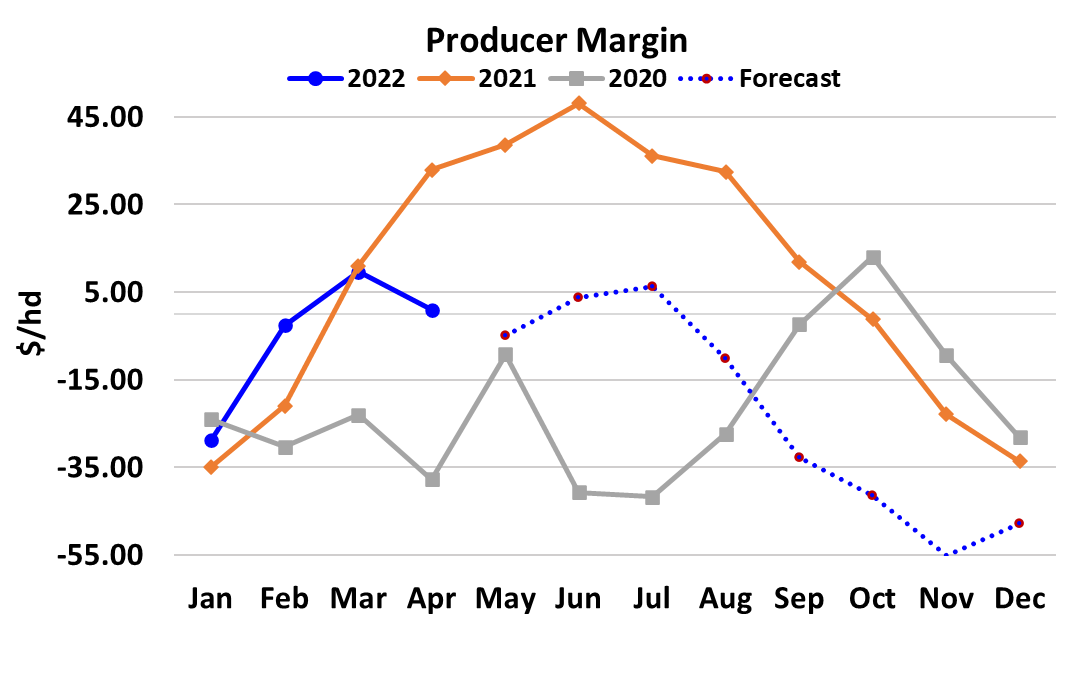

were moving higher. The WCB cash market added $2.42 this week

and the National market added $4.06. That was a bad combination

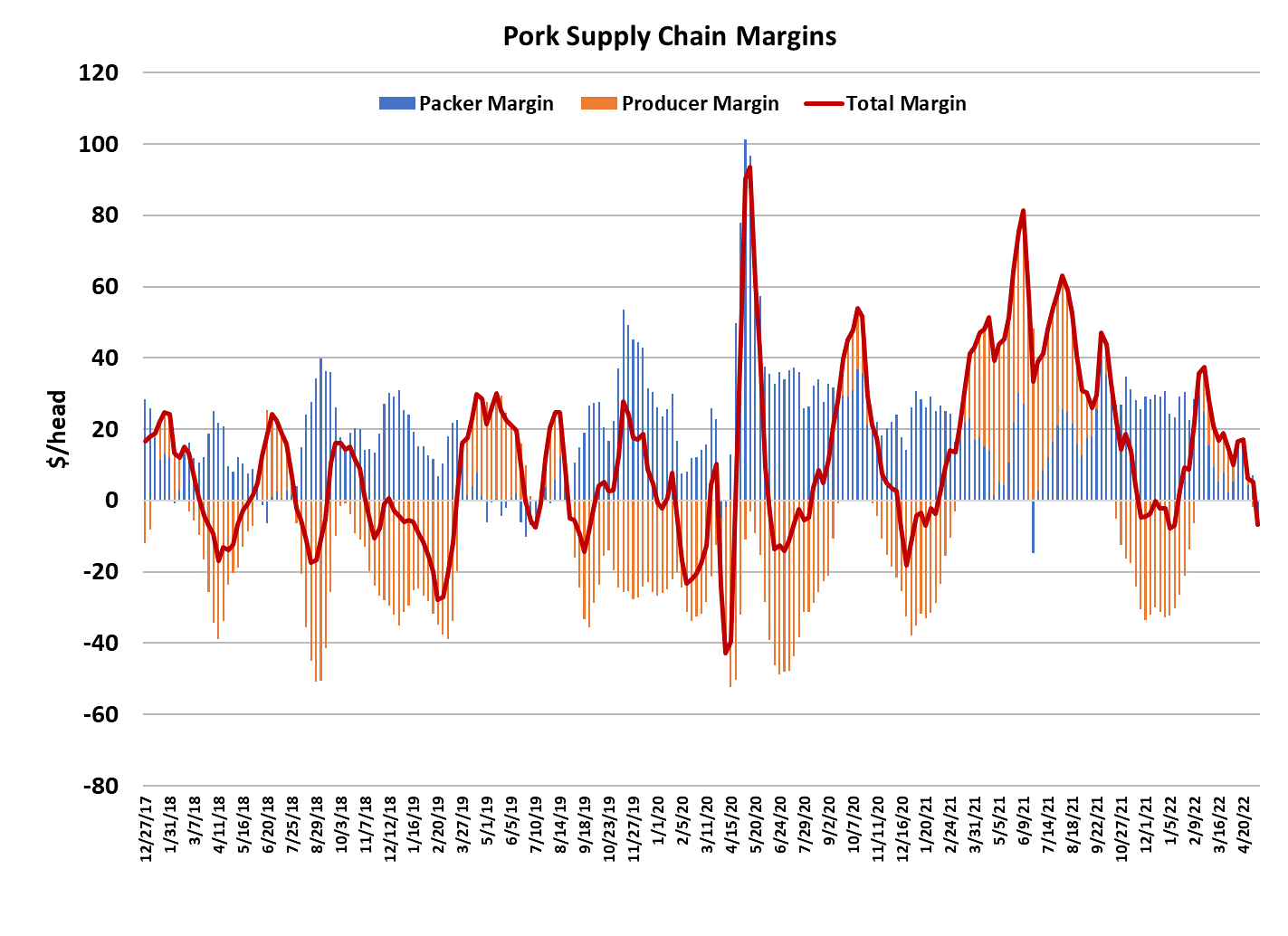

for packers and their margin dropped to -$2.70/head. That is the first

negative margin since last June when bellies collapsed and pushed

packer margins into the red for one week. Over the past three years,

there have been very few weeks where packers were running with

negative margins. My guess is that they will work quickly to try and

correct this problem before it gets any worse. They did reduce the kill

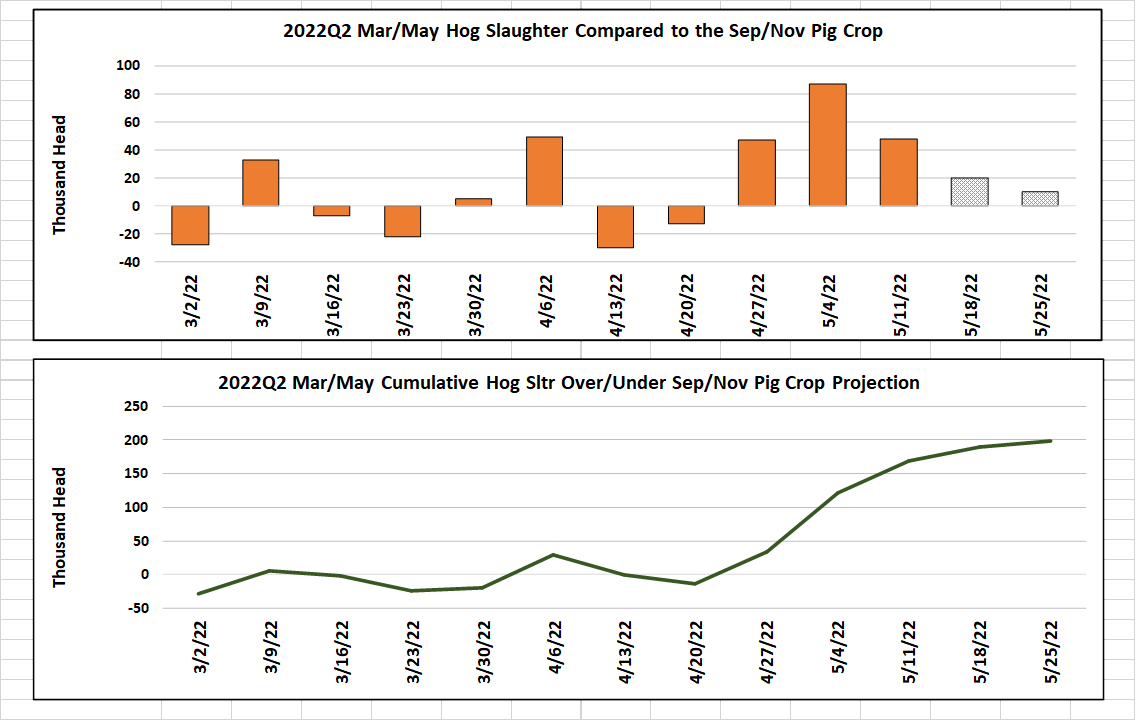

somewhat from last week’s rather large level, but even so it still

appears to be larger than what the pig crop implied. This week’s kill

was estimated at 2.38 million head, about 40k less than last week.

The attached chart indicates that was about 50k more than what was

expected. There are two weeks left in the March/May quarter and it

looks to me like the industry will over-kill the pig crop by about 200k.

That’s not a serious miss, but it could mean that kills during the

upcoming Jun/Aug quarter will also run a little larger than expected.

Barrow and gilt weights remain plateaued at 217 lbs and hopefully

they will start to move lower soon. There have been some very warm

temperatures in the Midwest recently and the forecast is calling for

warmer-than-normal weather next week, so perhaps that will be

enough to get weights started going lower. There will, of course, be a

short kill in the first week of June to account for the Memorial Day

holiday on May 30, but after that we should see weekly kills down

below 2.3 million head until the end of July. Kills should rise

seasonally in August and by the time the end of August arrives, we

could have slaughter levels back up to 2.5 million head per week.

I mentioned that packer margins were negative this week, but it is

important to note that producer margins were also negative by almost

$3 per head. That means the combined margin pushed into negative

territory this week for the first time since early in the year. The

combined margin is pretty close to where it bottomed last time, so

perhaps the demand softness has almost run its course for this cycle.

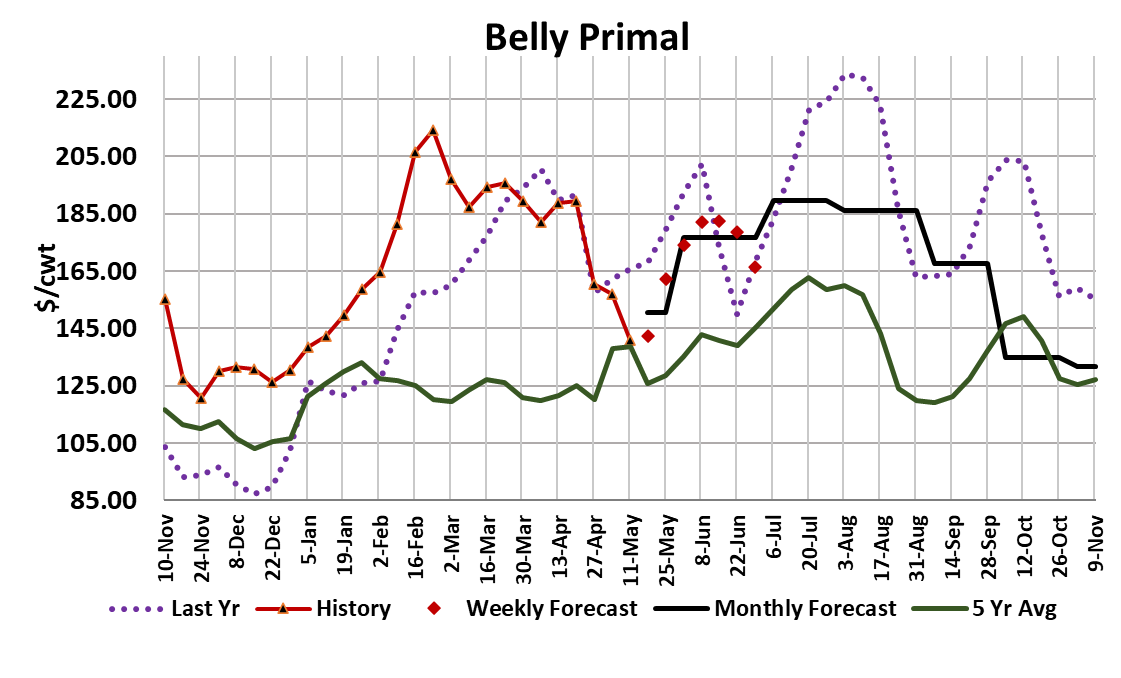

The main concern demand-wise is still the bellies and hams. Hams

clearly turned lower this week and the primal dropped almost $6/cwt.

Bellies also posted some soft numbers this week, although there was

an encouraging bounce in the primal on Friday. Hams I think will

continue lower next week. Bellies, I’m not so sure, but it is too early to

call them sharply higher. I want to see how they behave early next

week. The loins, butts and pics all seem to be trading relatively

steady and I’d guess that is likely to continue next week. The forecast

has the cutout just a tad lower next week and then moving back up

into the $105-110 range from Memorial Day onward.

To get to that forecast, I’m assuming that the downcycle in pork

demand is just about over and we will start to see seasonal

reductions in pork production soon. Both of those should be good

assumptions, but I’m more concerned about the demand side than

what will happen to supply. It is possible that the hams will continue

lower for longer than I imagine and thus keep the cutout depressed

for longer. Even futures traders are starting to grow wary of the pork

demand as they trimmed over $3 off of the Jun contract this week

and $5-6 off of the July and August contracts. By now, it is clear that

there is not a serious shortage of hogs that is going to cause price

levels to skyrocket this summer. I’m projecting the cutout to average

around $108-110 in June and July and the LHI getting back up to

perhaps the $105-107 area.

That’s not a huge gain from today’s levels and certainly well below

what traders were thinking this spring when they ran the Jun hog

futures up to $127. After running the futures up way too high and

then getting burned as the cash failed to live up to expectations, I’d

hope that futures traders will be more reserved this summer and

resist the urge to become wild-eyed bullish just because the cutout

moves up a few dollars. Further, there is the risk that packer’s

margin management efforts will be successful in pushing cash hog

prices down enough to offset a lot of the benefit to the LHI from a

stronger cutout. I think that the hog and pork complex will become

more bearish toward the middle of July because demand typically

sags after that and kills start to escalate. As a result, all of the

contracts from Aug onward look too rich relative to my take on the

fundamentals.

Export demand is still a lot softer than last year and with big imports

also, it is likely that pork availability this summer will be around 2%

larger than last year. If we throw in much softer demand than last

year, then there is no reason to think that price levels will get

anywhere near as high as they did last summer. Buyers would be

wise not to extend coverage too far into the future as things get

sorted out this summer. Corn prices remain very elevated and

producers are dealing with strong price inflation in a lot of other

inputs. That means breakevens will likely stay over $100/cwt for

much of the summer. Producer profitability is likely to be much worse

than what they have come to expect in the summer months and that

could lead to further reductions in the breeding herd later this year.

That is not necessarily bullish for price levels though, because

demand is expected to be working lower through the balance of 2022

also. Next week, watch the bellies for signs that the bottom is in and

also watch the hams because if the cutout moves lower, that will

likely be the primal that is to blame.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}