Pork Wrap May 12

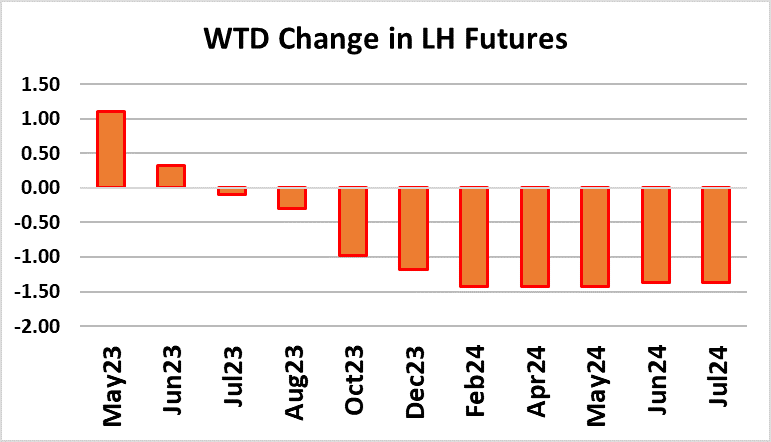

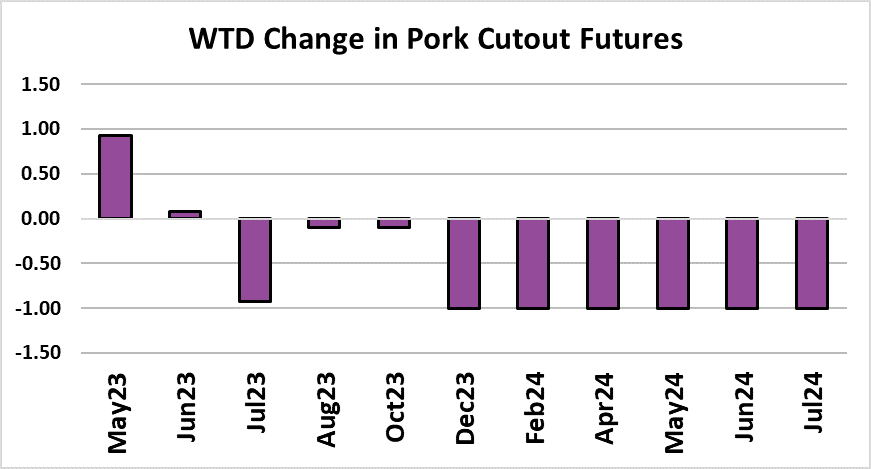

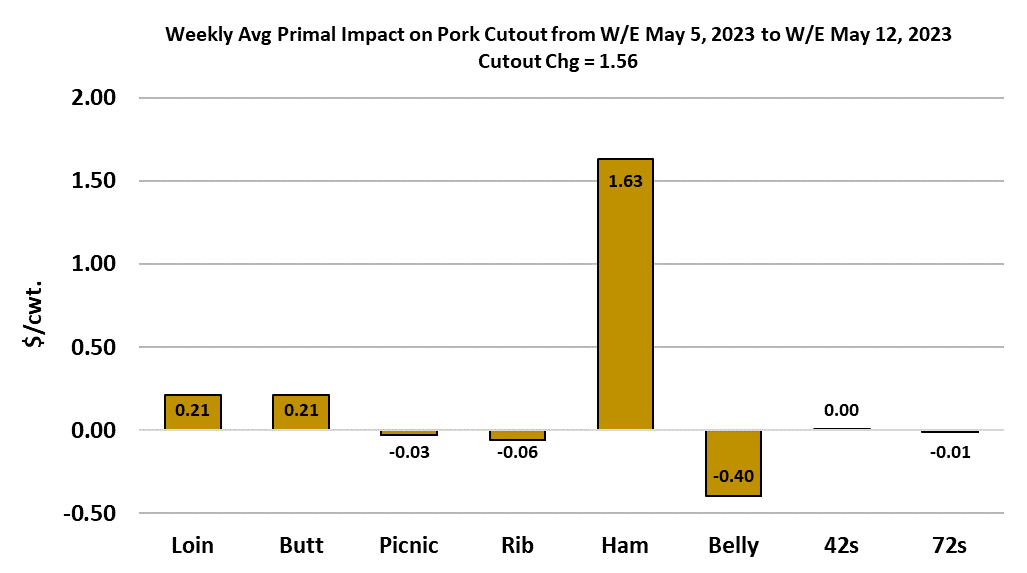

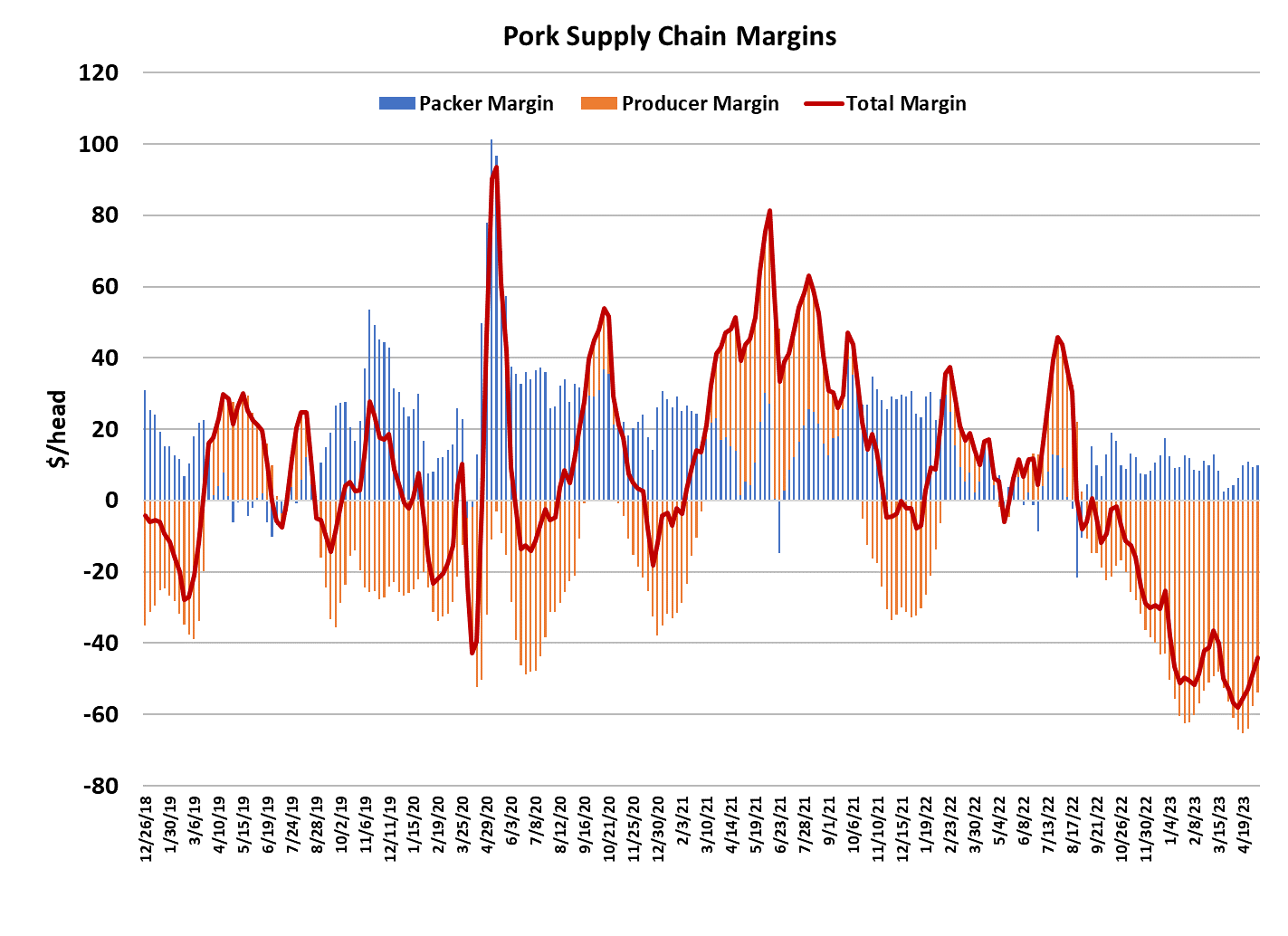

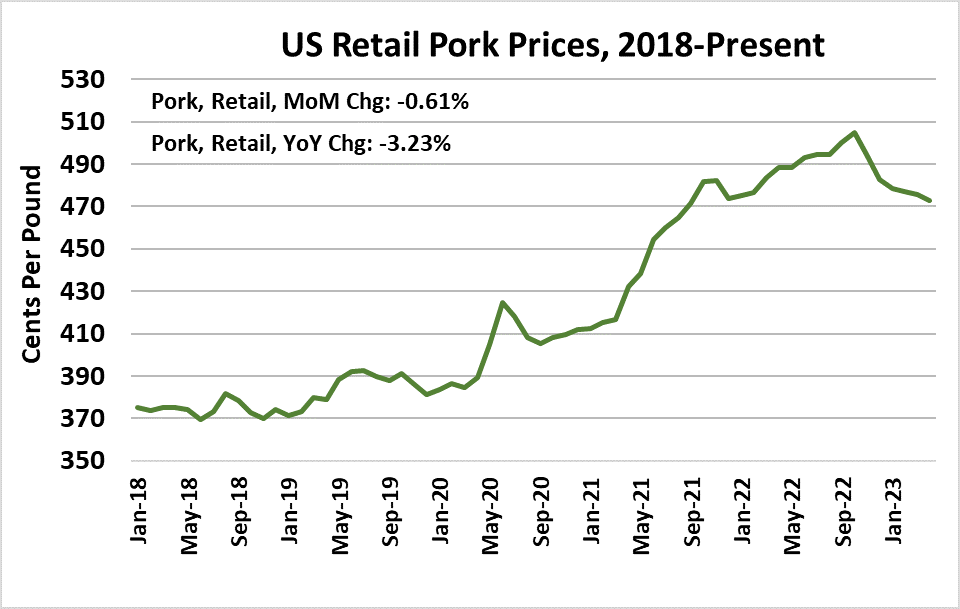

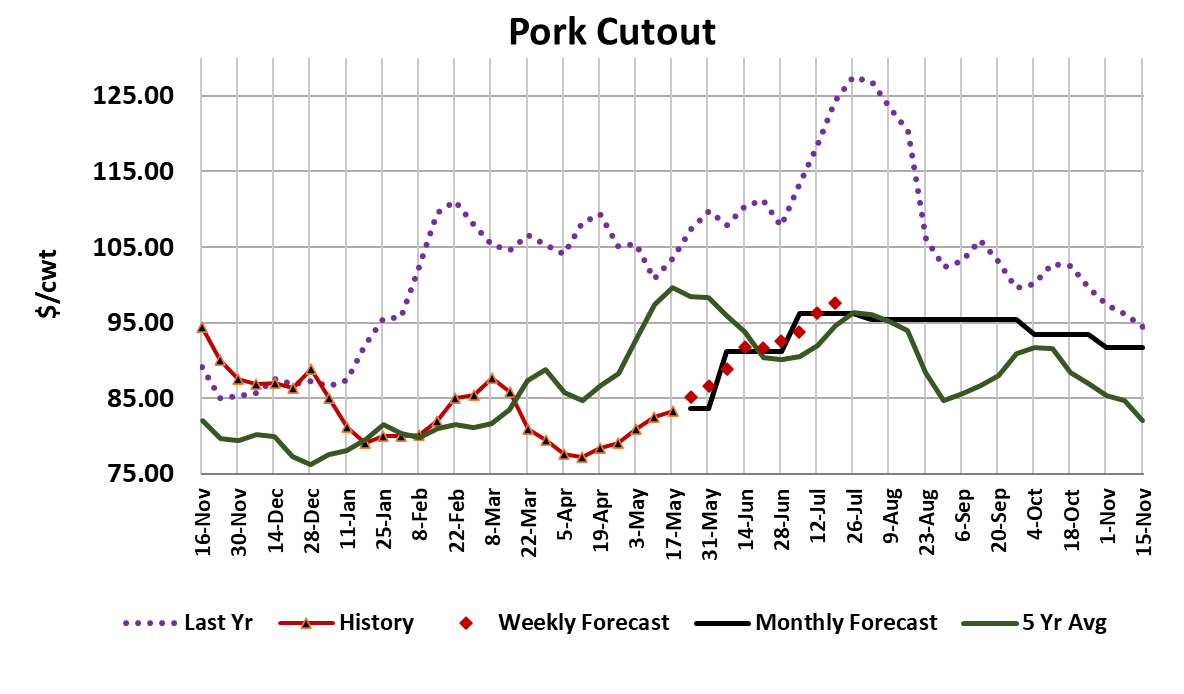

The pork cutout continued to work its way slowly higher, gaining $1.56/cwt. to average $82.48 for the week. Almost all of that gain was driven by a strong showing in the ham complex. Bellies still have yet to waken from their 2023 slumber, but the forecast has them moving gradually higher as production shrinks moving into summer. The retail primals remain uninspiring and the trim complex continues to look very soft for this time of year. So, right now, pork is basically a ham story, where the ham primal has added over $10/cwt. in the past two weeks after a long spell of trading sideways. Hams have benefitted from having low cold storage stocks relative to the other pork items and that has probably been a big factor in their recent success. Overall pork demand remains very weak. The attached demand scatter shows pork demand during May very near the low level it hit back in the recession year of 2009. The combined margin is moving slowly higher, so it is reasonable to conclude that we are getting some small improvements in demand, but it has a long way to go before it will be considered “normal” again. The cash hog markets were also higher this week, with the WCB gaining $2.60/cwt. on a weekly average basis and maintaining about a $2.50/cwt. premium to the NDD price. Hog supplies are now in the process of contracting seasonally, so we should see fairly steady gains in cash hog prices well into July. Last year, we saw packer competition for small summer hog supplies drive their margins into the red at times during June and July and that could be the case again this year because I suspect that packers will have more difficulty raising the cutout this summer compared to last due to demand deterioration. Packer margins this week registered about $10/head, but by Memorial Day I expect that will be cut in half. Producer margins improved a little also, but are still more than $50/head in negative territory. So far, sow slaughter hasn’t indicated that producers are downsizing their breeding herds, but sow prices fell to $24/cwt. this week, which is extremely low for this time of year. The only other time that sow prices were this low in mid-May was in 2020 during the onset of the covid crisis and that preceded a very sharp drop in the breeding herd over the next 2 quarters. Producer margins were in the red back then too, but not nearly to the degree that we have seen this spring. That seems to make a good case for some reductions in the breeding herd this summer and fall and that is exactly what is needed to bring profitability back to the production segment of the supply chain. My supply forecasts anticipate shrinkage in the herd over the next few quarters and that is why the deferred futures are showing well under-priced. The May futures expired on Friday at a bit over $76/cwt., which was up about $5/cwt. from where the Apr contract expired last month. Jun is currently building in another $7-8 advance over the next 30 days. That seems do-able, but will probably require the bellies to exhibit better demand than they have so far this year. I continue to have to revise price forecasts lower due to near-term under-performance, with the one exception being hams, which are now starting to outperform the forecast. 23/27 hams printed over $91/cwt. on Friday afternoon. Two weeks ago they were trading in the low $70s. This week’s kill registered 2.38 million head, down about 72k from the week before. At this point in the calendar, kills should continue to shrink a little each week until they bottom near 2.27 million head, not counting holiday weeks. That should happen in late June. Slaughter during the summer months of June, July and August should run about 1% stronger than last year, if USDA’s estimate of the Dec/Feb pig crop is accurate. Carcass weights may run a little below last year however, and that would bring overall pork production down to the point where it is similar to last year’s level. On the other hand, demand is obviously not on par with last summer’s strong showing and that is likely to be what keeps pork prices well below last summer. USDA reported that retail pork prices during April were down 0.6% from March and are now 3.2% below last year. It is encouraging that retail pork prices are coming down, but the rate of decline has been very slow and doesn’t yet seem to be spurring any renewed buying interest on the part of consumers. Further, retailers know that summer means higher wholesale pork prices and thus we might see them resist taking retail prices down much more over the next couple of prints. The export business is one area that looks promising for pork. The weekly data have been showing strong YOY increases in total pork exports and a lot of that has been driven by countries that fall into the “Other” category. Japan also seems to have renewed interest in US pork after a fairly weak showing earlier this year. Low US pork prices are clearly getting the attention of international buyers. Next week should look a lot like this week in the pork complex: moderate gains in both the cutout and cash hog prices along with modest reductions in both slaughter levels and carcass weights. Keep an eye on both the bellies and hams. Bellies need to come to life and hams are at risk of stalling after posting strong gains in recent weeks.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}