Pork Wrap May 10

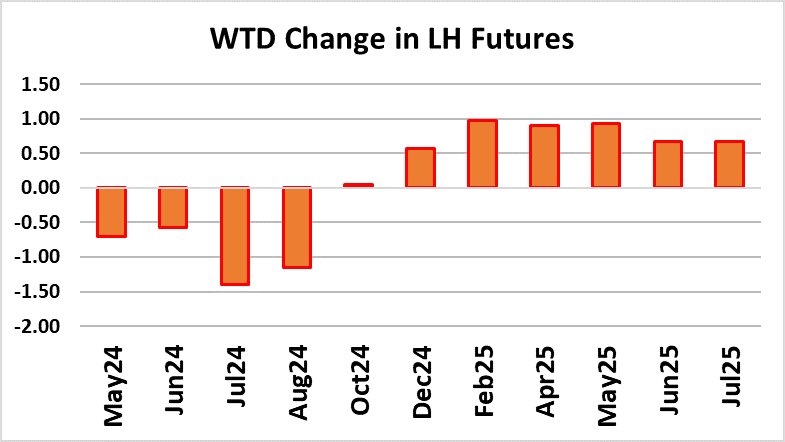

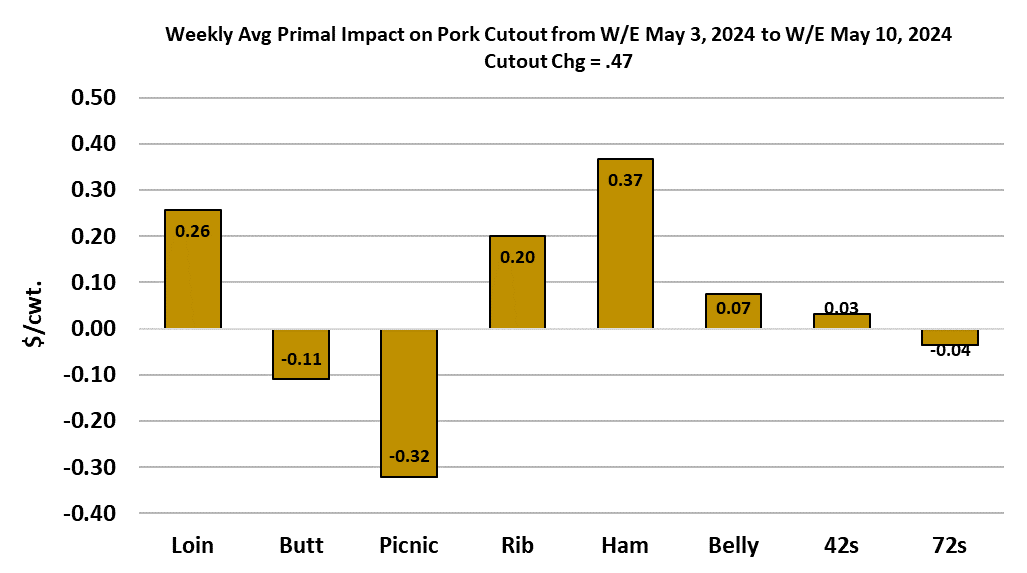

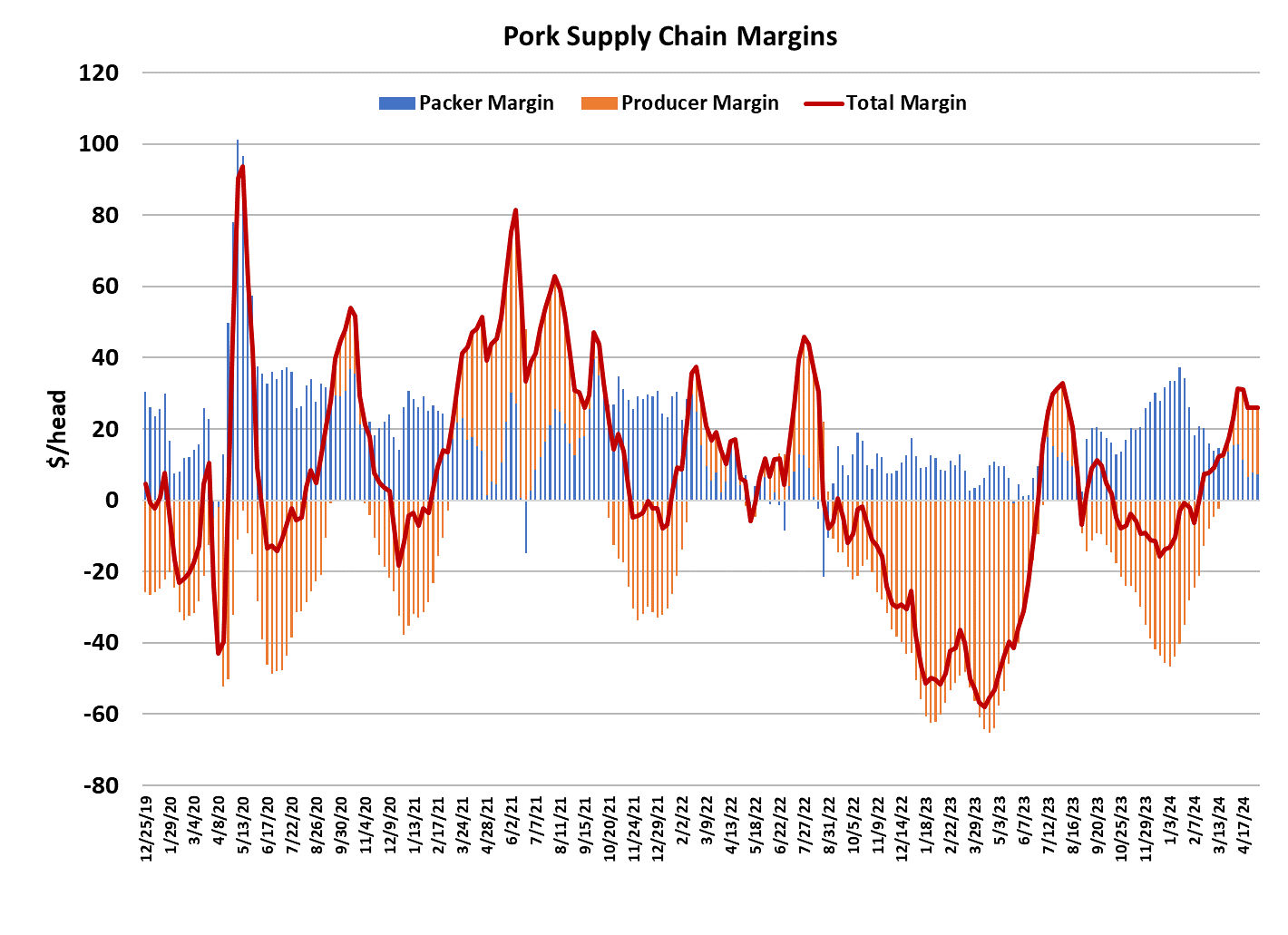

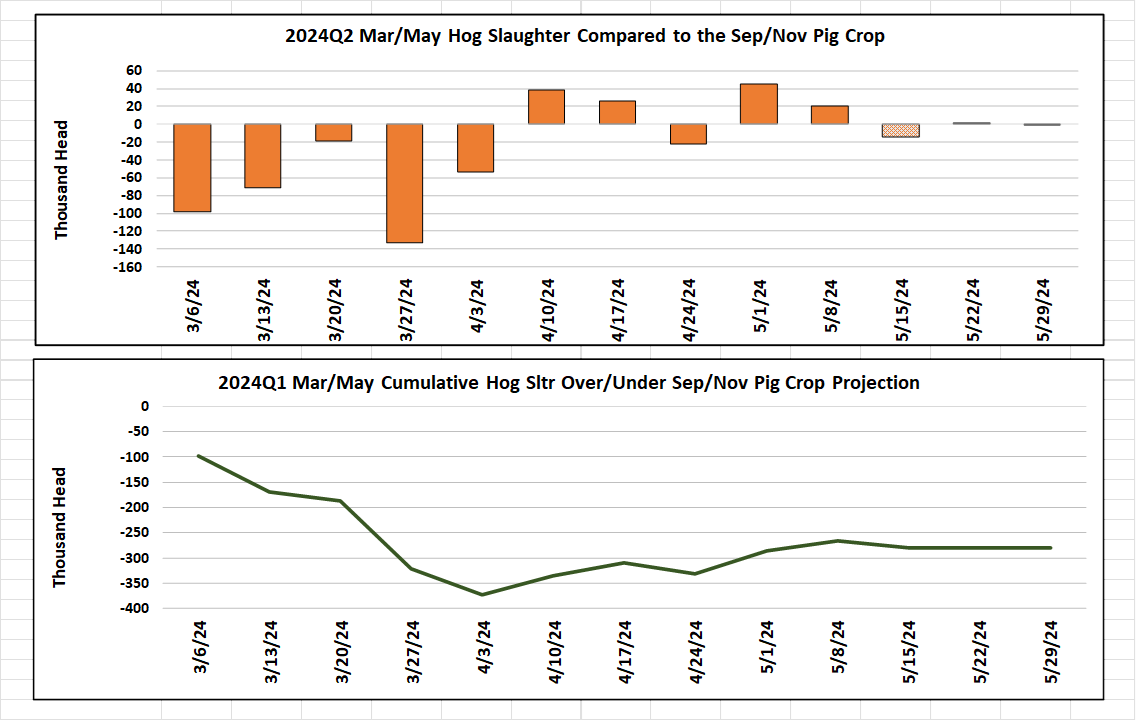

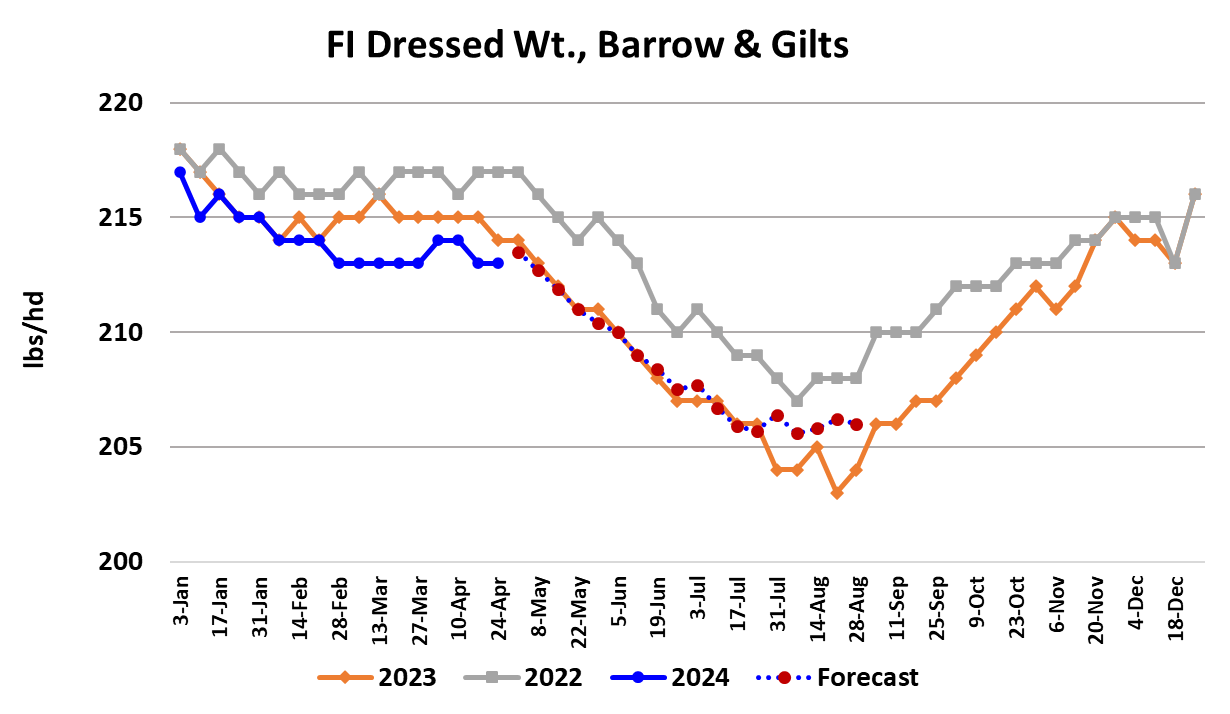

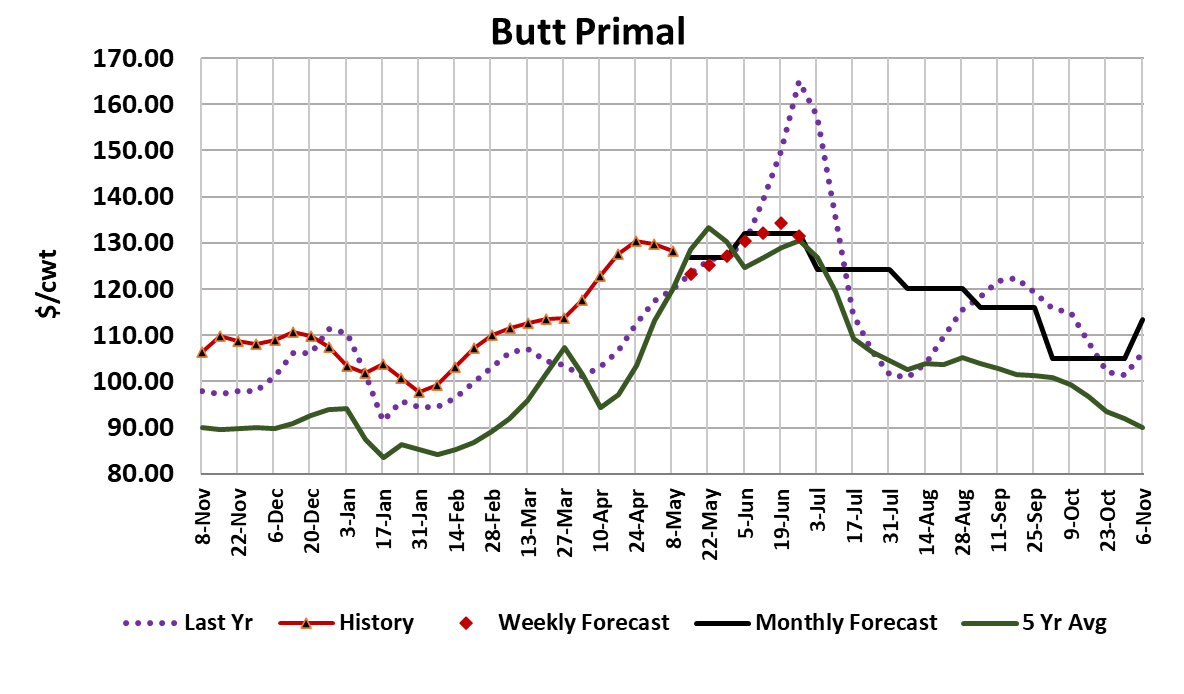

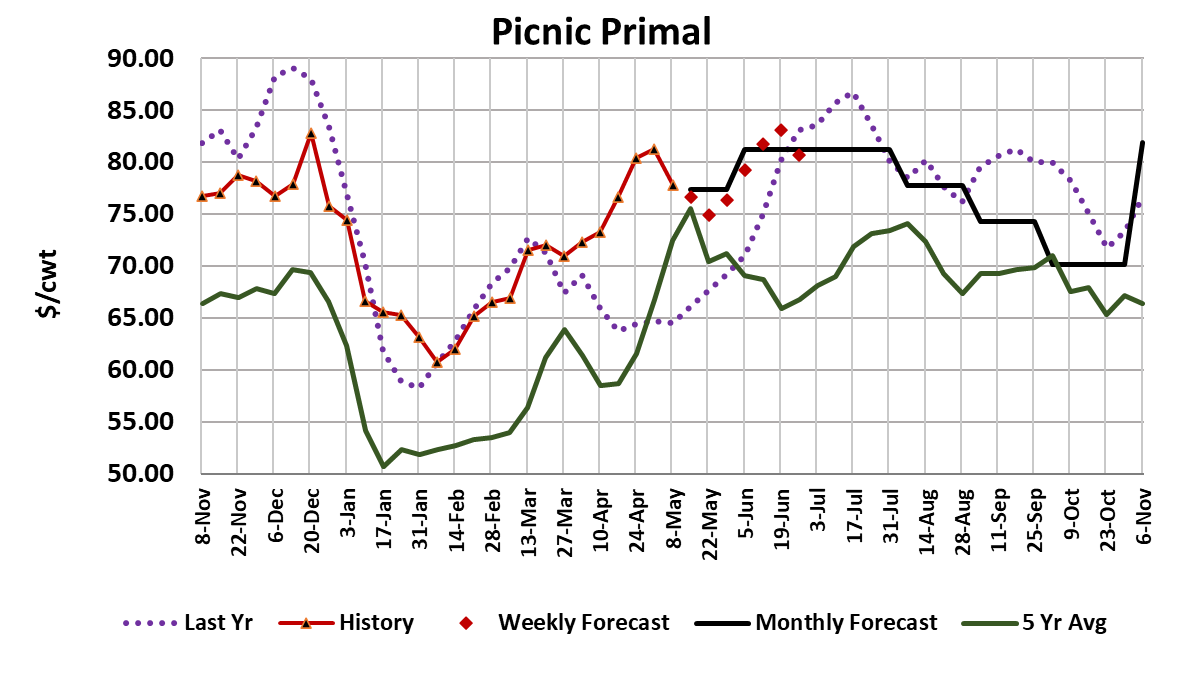

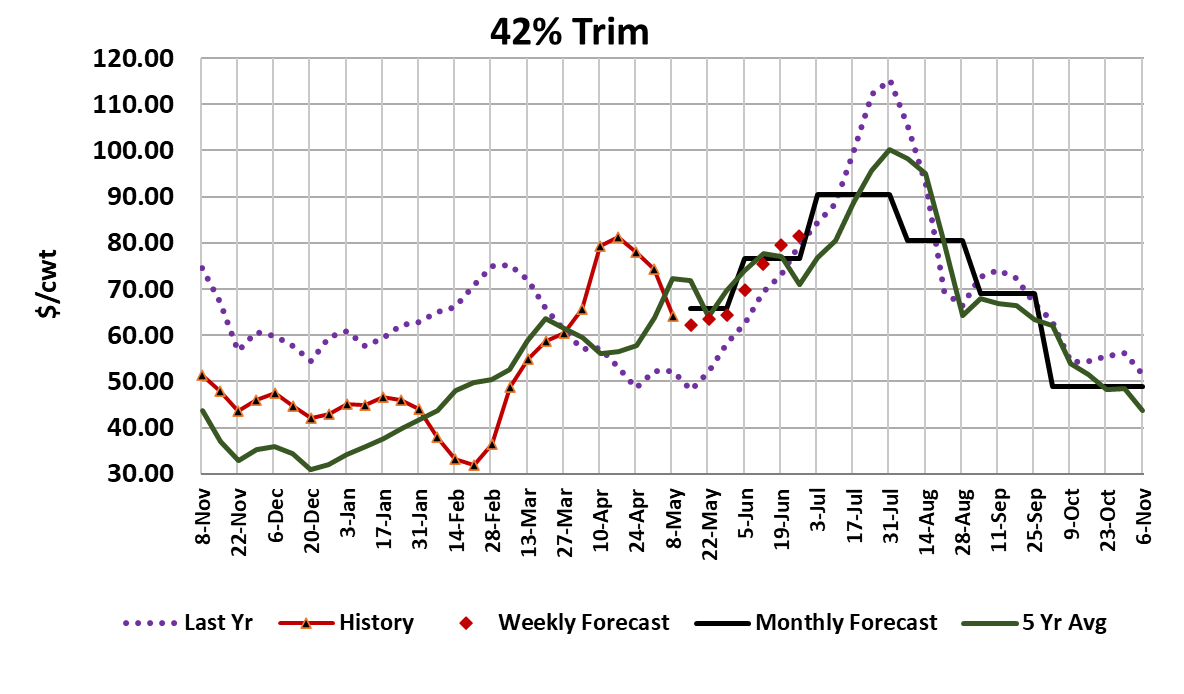

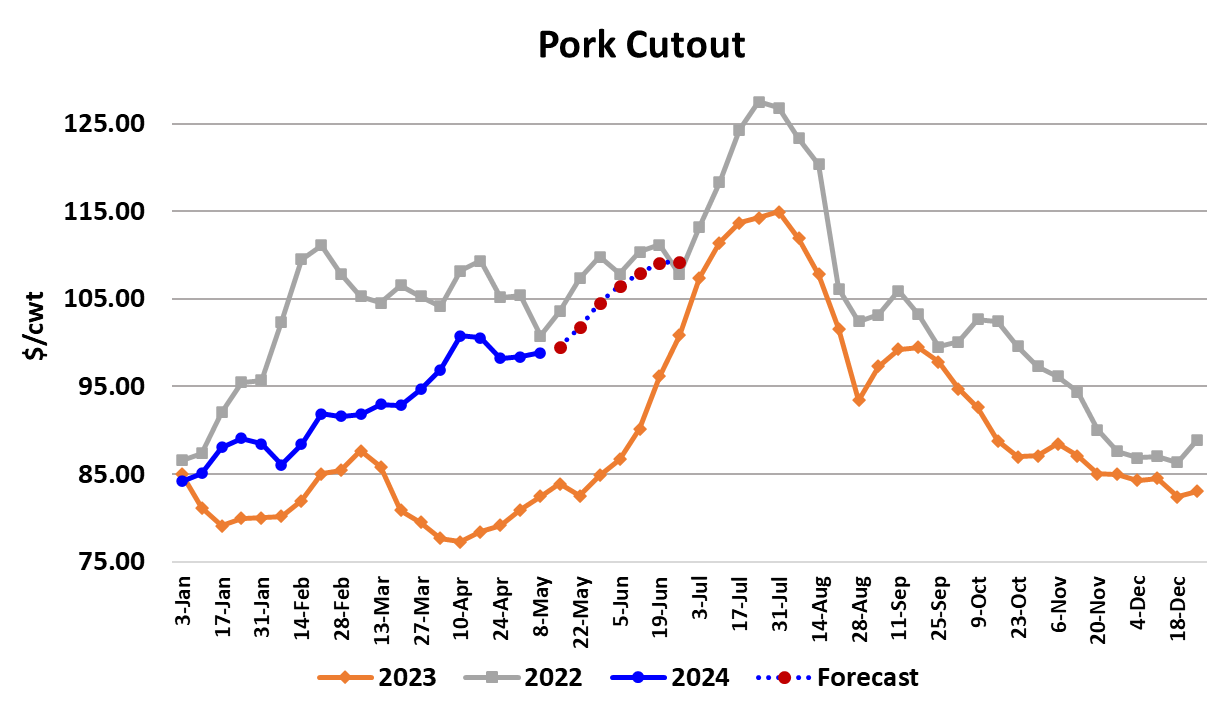

Prices across the hog and pork complex were virtually at a standstill again this week. The cutout moved up $0.47 to average $98.82 and the WCB negotiate market was a mere four cents higher on a weekly average basis. The lack of upward movement in prices during May is very unusual and it has frustrated the futures bulls who can normally count on cash prices advancing several dollars at this time of year. The best news for the bulls is that the hams appear to be turning higher now after three weeks of lower prints. Past price patterns suggest that the hams should continue to post gains at least through Memorial Day and maybe a bit longer. The bellies are still dead in the water however, as that primal only added $0.58 on a weekly average basis. As the kill shrinks in the coming weeks, it is reasonable to expect better price gains for the bellies and that, in combination with rising ham prices, will be the force needed to propel the cutout back over $100. The fundamental forecast has the cutout averaging in the $104-105 area for the week that contains Memorial Day, suggesting faster gains are on the way. However, not everything is rosy in pork land. The butts and picnics are both working lower now and that has removed some of the support that the retail items had been providing. I don’t expect either to remain on a long-term downward path, but for the next week or two they may be more of a hinderance to the cutout than a help. The trims are in the same boat, also working lower at present, but not expected to remain that way much longer. Packer margins were almost unchanged on the week, holding in the $7-8/head range. Packers seem to have a good handle on this market, as we note that when the cutout slows down, so does the price that packers pay in the negotiated hog market, thus helping to preserve their margin. Of course, as hog supplies shrink seasonally over the next couple of months, packers will have to compete harder for hogs and that is likely to put further pressure on their margins. Hogs should be a little more plentiful this summer compared to last, so packers may be able to make it through the summer without experiencing a negative margin. If negative margins do materialize, I wouldn’t expect it last more than a week or two. Producer margins remain healthy also, now close to +$19/head and the combined margin is sitting a little north of $25/head after moving sideways this week. It is easy to sense trader’s boredom with this stagnant market, but it is impossible to do much about it. I don’t think it is going to stay that way much longer as summer is usually good for some pricing fireworks. May LH futures will expire on Tuesday and appear to be gliding toward a settlement in the $91-91.50 range, which is only a hair higher than where the Apr contract expired. That’s just further proof that this market has been stagnant for the past month. Jun futures are carrying about a $7 premium to the cash index, which is certainly achievable at this time of year, but if the price stagnation lasts for much longer, traders will need to adjust that downward. The fundamental forecast has Jun expiring in the $98-99 range and Jul going off the board closer to $104. In order to get to those levels, some fairly strong gains in the cutout need to materialize along the way. The current projection for the summer top in the cutout is around $112. Obviously, that won’t happen unless the bellies get going and some of these soft retail items turn around. Right now, I’m pretty confident that both can be achieved, but nothing is ever certain when it comes to pricing in the future. On the supply side of the market, this week’s kill registered 2.39 million head, just 16k less than the week before. That was a little above what the pig crop implied, but the cumulative kill during the March/May quarter is still about 275,000 head less than what the Dec/Feb pig crop suggested. While the kill is declining seasonally as expected, hog weights have not yet started their descent. Barrow and gilt weights were reported steady at 213 pounds this week and it looks like next week they may print one pound higher. Still, the seasonal decline should be just around the corner, unless producers make a conscious decision to stretch out the feeding period, resulting in heavier-than-expected carcass weights. The weekly export data has looked a little softer recently, with reported volumes to Mexico now back below last year’s level. That is a little concerning, but these data are notoriously unreliable so it is probably best not to attach too much weight to that just yet. We have noticed some trading down within the beef category on the part of consumers and at some point they may choose to trade down further, substituting pork in the place of high priced beef. That could provide a much needed boost to pork demand, so it bears close watching. Next week, production should be a little smaller and demand should be a little stronger as we approach Memorial Day. Look for the cutout to add a dollar or two and likely some modest gains in the negotiated hog market. The Jun futures are vulnerable to some wild swings as it takes over the front month position when May expires.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}