Pork Wrap March 9

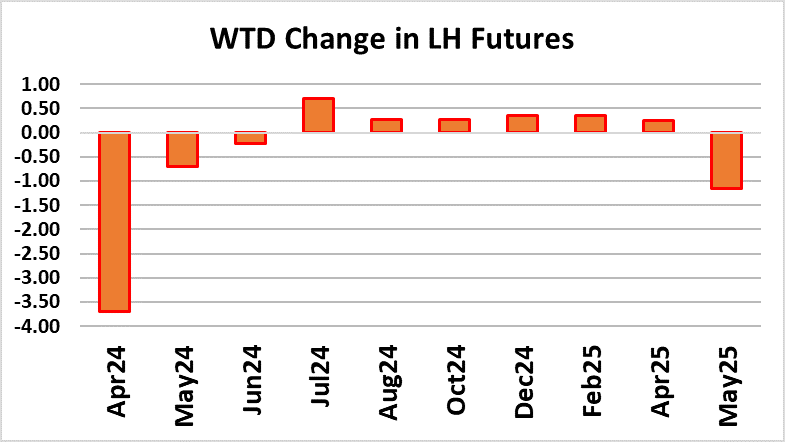

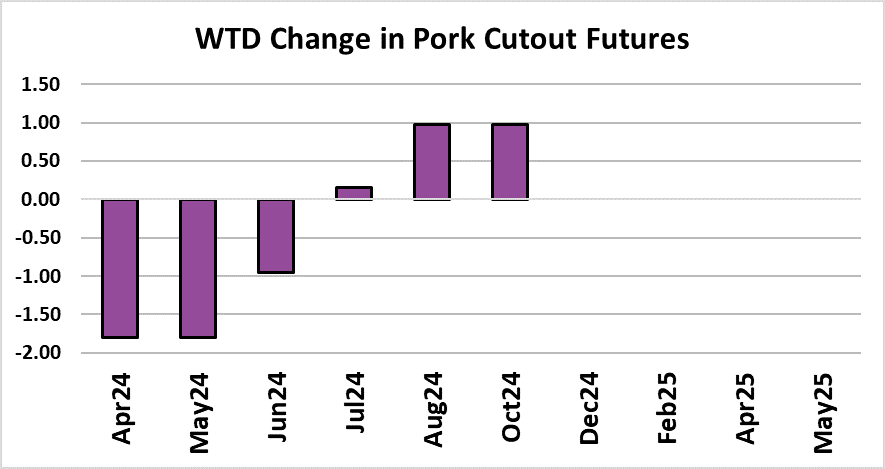

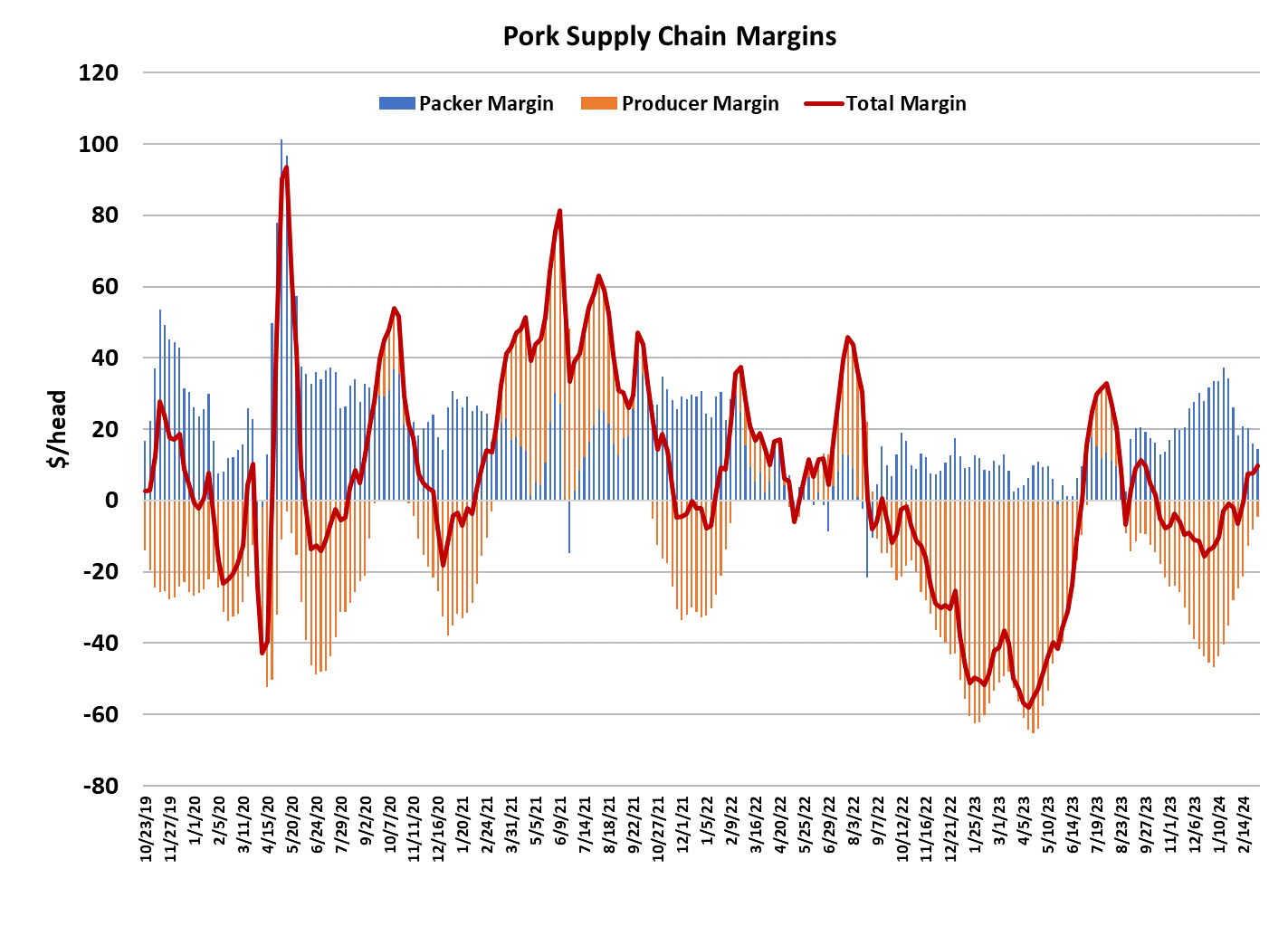

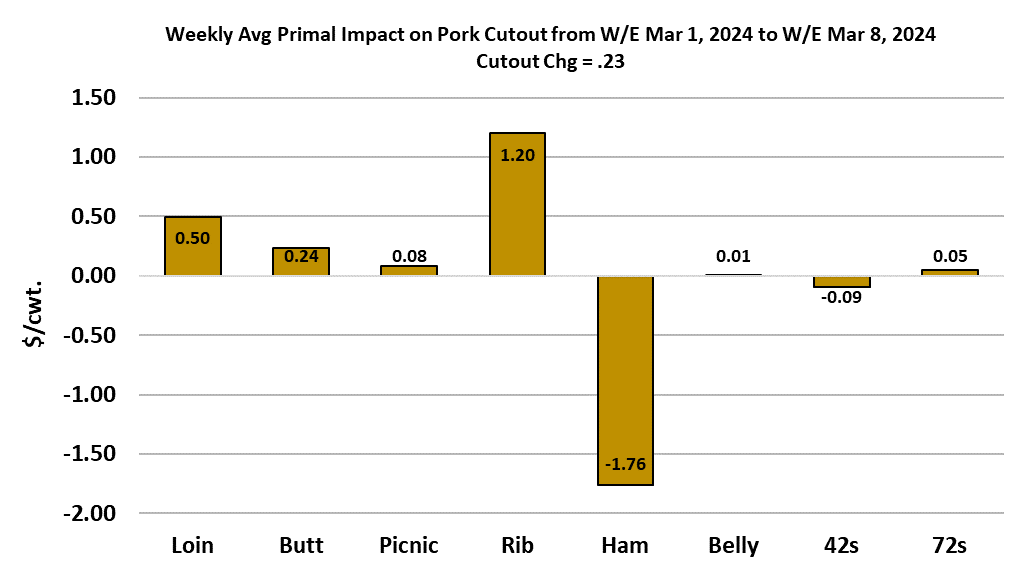

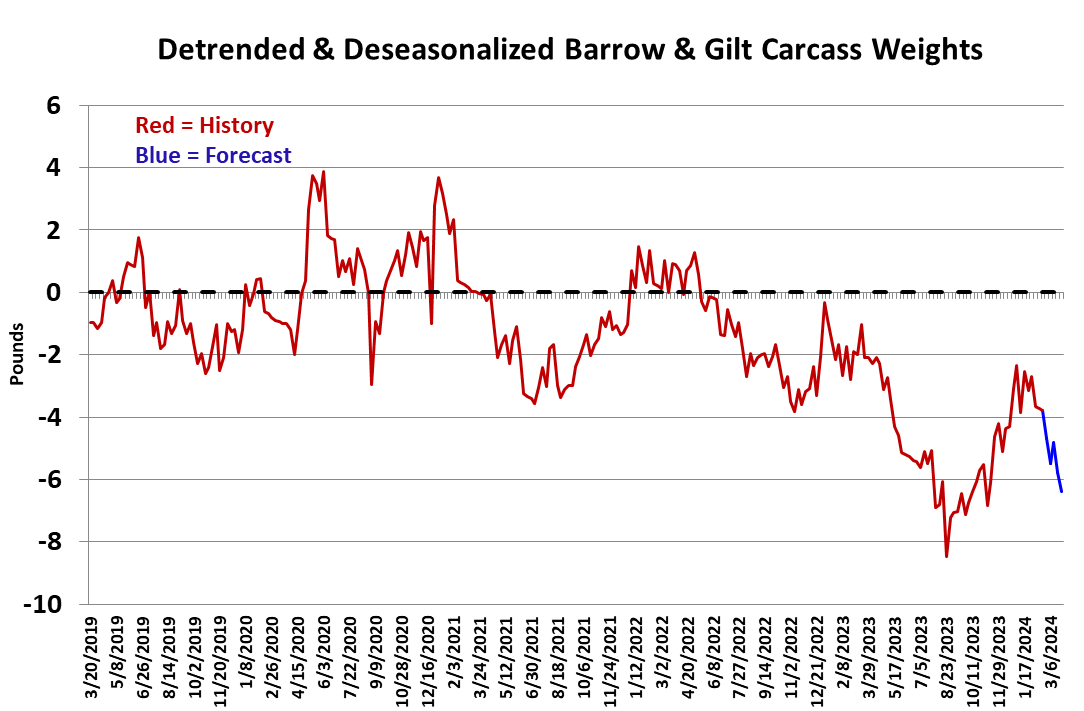

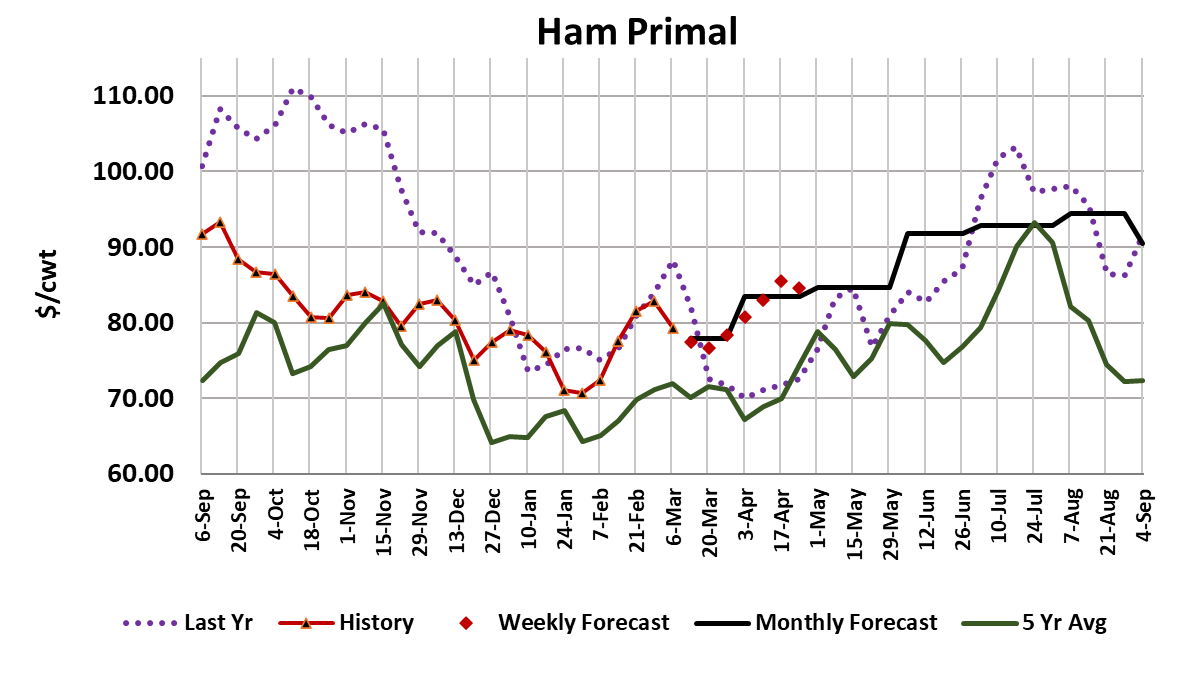

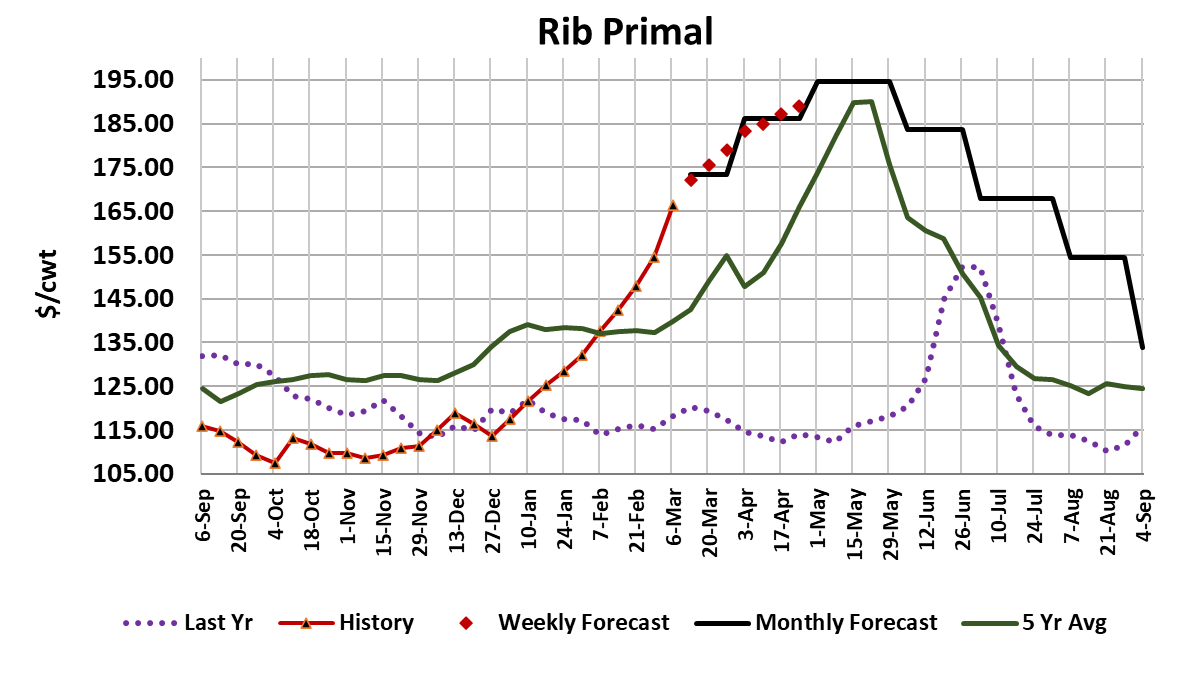

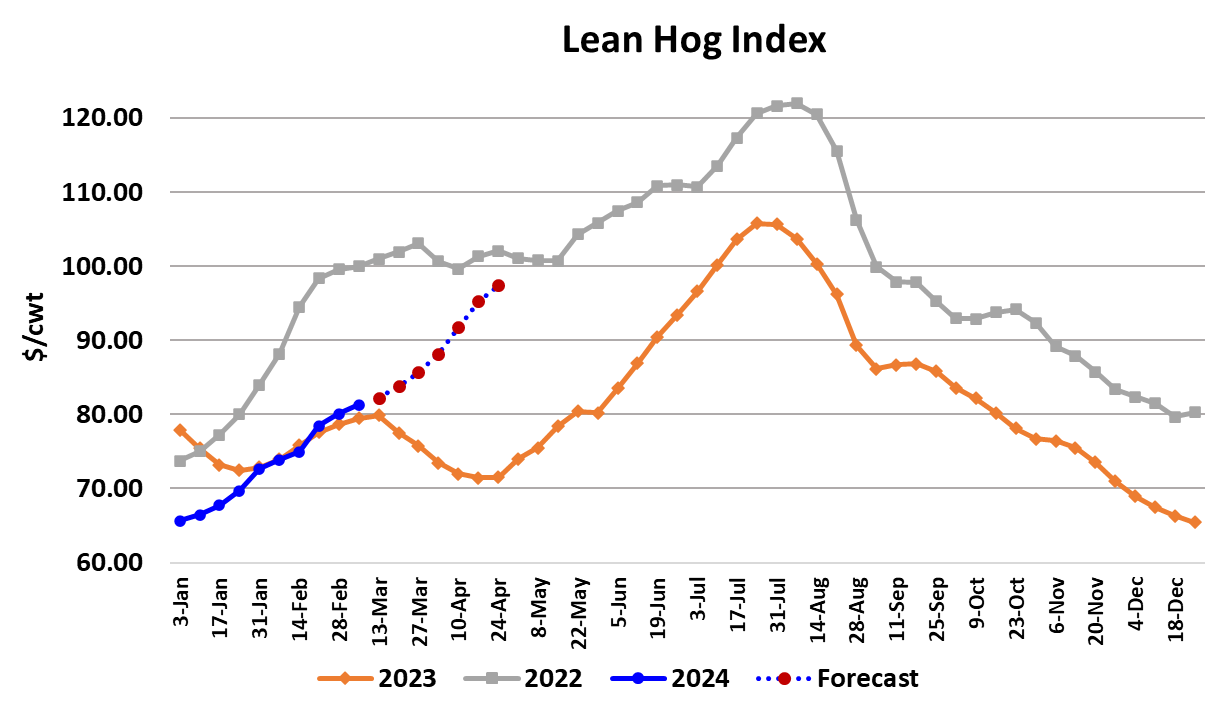

This was the second week in a row where gains in hog prices outpaced increases in the cutout. The cutout only added a paltry $0.23/cwt. on a weekly average basis while the NDD negotiated market was up $2.42. As a result, packer margins trended lower and now stand at just a little under $14/head. This week, the hams were the cutout’s “problem child”. I expressed concerns over the direction of the ham market last week and those concerns are still in place. True, this week’s lower pricing helped packers to move big volumes of ham, but I’m not convinced that will be enough to turn prices higher next week. The fundamental forecast has two more weeks of softer ham pricing dialed in before the market turns higher on the anticipation of post-Easter demand. Bellies were a non-event this week, as the primal value was virtually flat with the week before. Ribs are easily the star performer of the pork complex so far in 2024, moving higher in nearly a straight line since the beginning of the year. The problem is that ribs only contribute about 5% to the value of the cutout. The other retail items continue to grind slowly higher and there is no reason to think that won’t continue. In order to get big moves in the cutout we need to see big changes in either ham prices or belly prices, or both, and neither seems poised for a big move at the moment. As a result, the cutout forecast calls for 2-3 more weeks of tepid gains before the real price acceleration kicks in near the end of the month. This week marked the transition from the Dec/Feb quarter to the March/May quarter and, right on cue, the weekly kill dropped below what the pig crop implied for the first time in what seems like forever. For some reason, packers didn’t run several shifts this week and we ended up with a couple of daily kills down around 450k, rather than the more normal 480-490k. The size of the daily shortfall makes it look like one of the largest pork plants was down and if so, it was likely for mechanical issues, not a purposeful cutting of the kill for margin reasons. As a result, total slaughter this week tallied only 2.46 million head, down about 90,000 from the week before and 50,000 head under what the Sep/Nov pig crop implied. That could result in a little tightening of product availability early next week and thus temporarily benefiting the cutout. Barrow and gilt carcass weights were flat at 214 pounds for the third week in a row, in keeping with the general theme of sideways movement in weights during Q1. The DTDS weights remain at pretty low levels and are actually trending lower, so that suggests that hog producers are remaining current with their marketings. The fact that negotiated prices have been steadily rising also suggests that the production pipeline is flowing well. The next big data event on the hog calendar is the March 28th release of Hogs & Pigs, and I’m expecting it to show about a 2.5% YOY decline in the breeding herd as of March 1. Sow slaughter ran hot enough in the Dec/Feb quarter to support that type of reduction. However, before the bulls start to celebrate, I will point out that even with a smaller breeding herd, it is very likely that the Dec/Feb pig crop will be reported larger than last year due to big gains in productivity. I’m looking for USDA to report another strong YOY increase in the number of pigs saved per litter, that should more than offset the decline in the breeding herd. The data on January pork exports was made available today and it showed a 5.8% YOY increase. YOY increases have been reported in 13 of the last 14 months, so it is clear that the export market remains healthy. Next week, it seems reasonable to expect another small gain in the cutout and perhaps another $2-3 increase in negotiated hog prices. Hams pose the greatest risk to the cutout at the moment, so keep an eye on that market.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}