Pork Wrap March 5

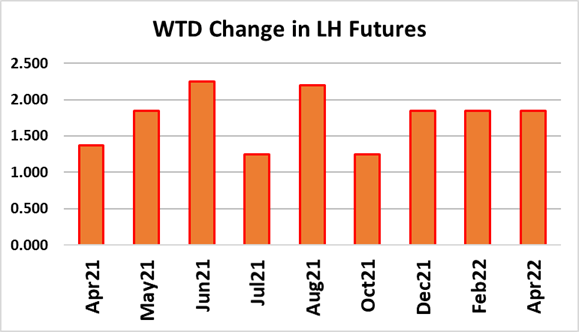

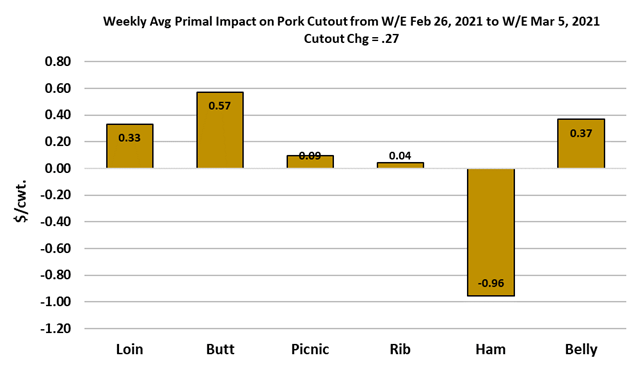

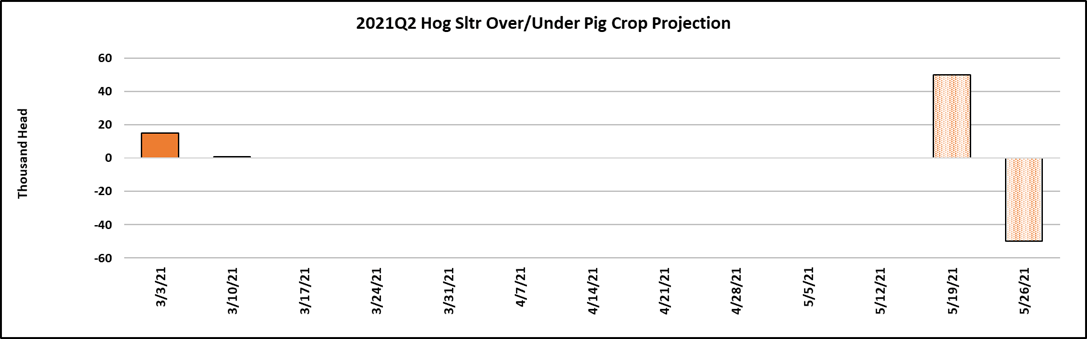

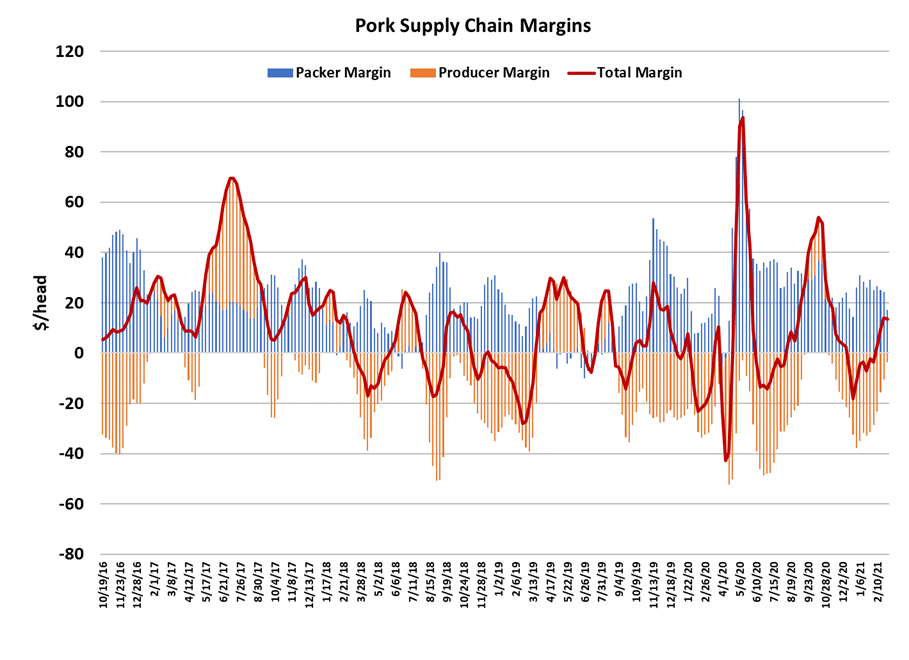

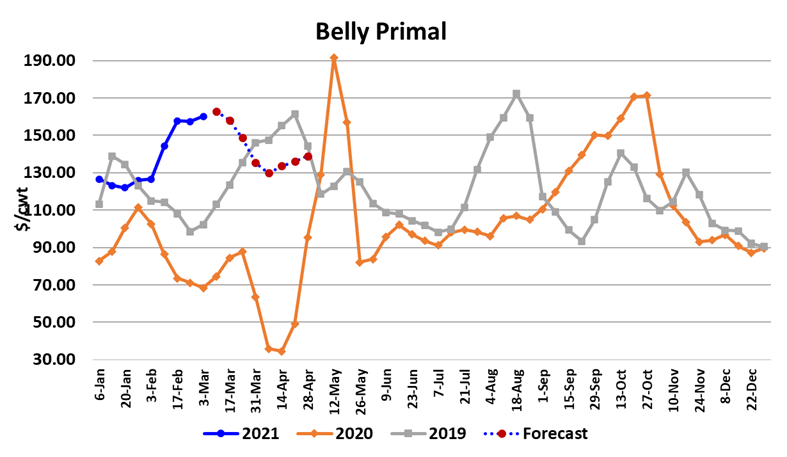

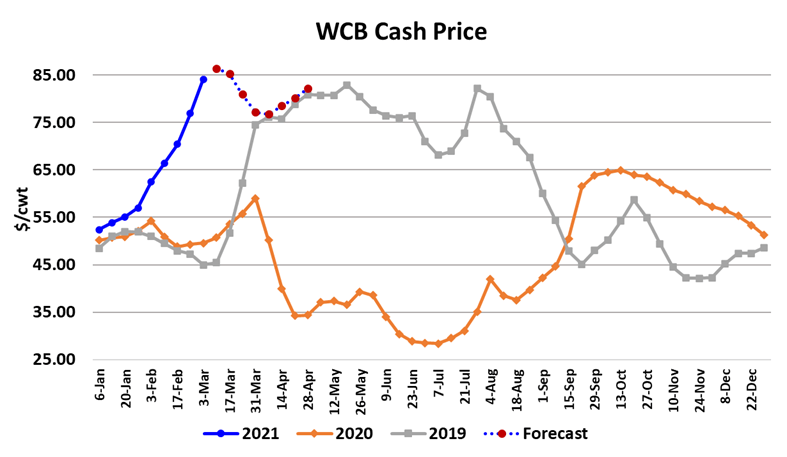

The cash hog market continued to impress this week, with the WCB negotiated market rising $7.22 on a weekly average basis and the NDD market up $6.44. Unfortunately for packers, the cutout didnft keep up, with the weekly average almost unchanged from the week before. That dealt a significant blow to packer margins which dropped $7 to $17/hd this week. The big mystery at this point is what is driving the cash hog markets higher so rapidly? The easy answer would be to say that hog supplies are tightening up significantly and packers are having to pay up in the negotiated markets to fill their kill schedules. There may be some truth to that, but it could also be that packer margins are just undergoing some overdue compression that is happening a little later than normal this year. Maybe both are true. There has been a lot of talk circulating about problems with PRRS this winter being worse than normal and that could be limiting supplies somewhat. But really, wefve seen kills throughout Q1 and now moving into Q2 that are very close to what the USDA-reported pig crops indicated. The chart below shows that this week, which was the first week that the industry was killing the Sep/Nov pig crop, the kill was only about 15k above the pig crop estimate. So, really close. We are not seeing anything in carcass weights that would suggest that packers have been pulling exceptionally hard on available supplies. Barrow and gilt weights this week were reported at 215 lbs, which was 2 pounds over last year. Preliminary data suggests that the next data release will continue to show weights stuck at 215. However, we did see packers scale back the Saturday kill significantly this week, down almost 80k from the week before. Perhaps they did that in order to keep cash hog prices from running even higher. We did see a $3 drop in the WCB market today, but Ifm not ready to say that the trend has turned and the negotiated markets are heading lower just yet. It is actually fairly normal for the Saturday kill to start dropping off substantially moving into March. As far as packer margins go, $17 in the first week of March is still pretty rich. So, maybe this all just a part of the normalization process that has been underway since covid disrupted this market nearly a year ago. Perhaps a more important question is why the cutout is still holding in the low-to-mid $90s with pork production this large. The hams and bellies have been exceptionally strong, and that gets most of the attention, but the other primals are also performing very well and that points to very robust retail pork demand. Now that slaughter levels and carcass weights are declining seasonally, if demand holds at this level, then it is quite possible that the cutout could take another leg up. The ham primal was the biggest drag on the cutout this week, dropping about $5, but is still at the highest level it has ever posted for this week, outside of 2014. Further, trim pricing is exceptionally high now, with the lean trim pushing over $100 this week. High trim markets put a floor under the hams because they can be ground up and substituted for trim. That could start to happen soon if trim gets much further ahead of the ham price. The belly primal is at its highest level ever for this week, even eclipsing 2014. With very low freezer stocks, more belly users are having to operate in the fresh market and that is probably helping to support the bellies and the freezer stock problem isnft going to go away anytime soon, so perhaps the bellies won’t come down soon either. Ifve mentioned before that this recent runup in the hog and pork markets feels a lot like what happened last October, but the difference this time is that it is happening in a shrinking supply environment rather than an expanding supply environment. That means it might last longer. To pour more fuel on the fire, this weekfs export report showed a big increase in new sales to China. There is talk of the ASF virus making a resurgence in China, so that bears watching. At this point, I’m not forecasting $100 cutouts, but I can’t totally rule that out either. More likely, the cutout will remain in the $90s for at least a couple more weeks before retreating back into the mid $80s around mid-April. Meanwhile, the deferred contracts keep marching higher, spurred on by high corn prices and the current cutout situation. There are those who believe that the industry over-corrected in scaling back the breeding herd last year in response to low prices caused by the pandemic. Ifm not in that camp yet, but do recognize that no one saw this type of demand strength coming and if they had, the industry likely wouldn’t have downsized as much. We will learn over the next few weeks if this is just a temporary bubble in prices or something longer lasting that will require herd expansion to solve.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}