Pork Wrap March 31

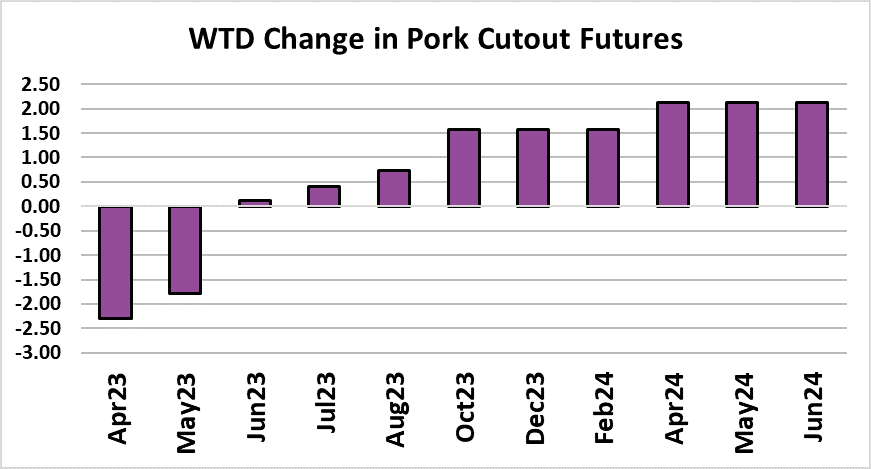

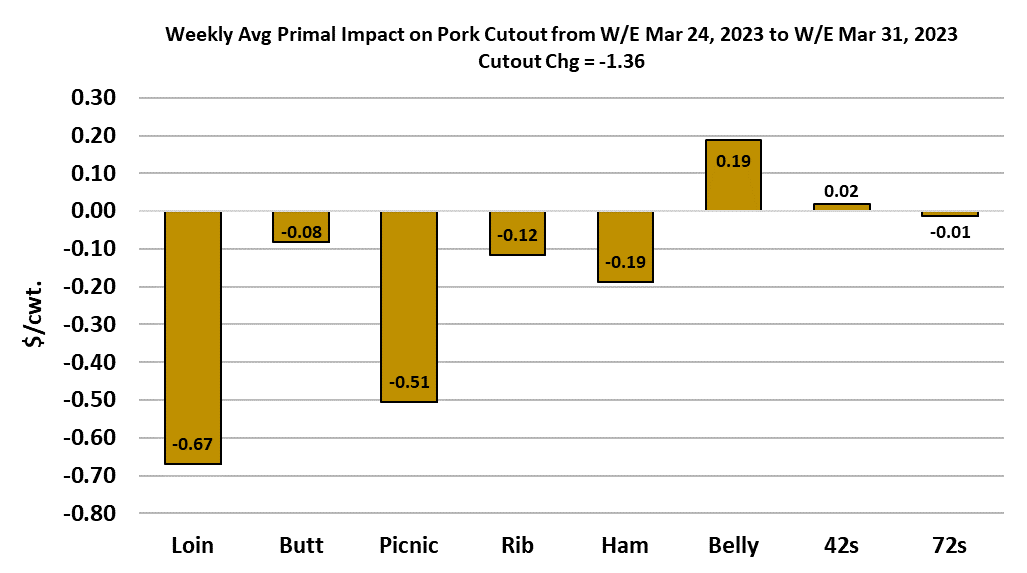

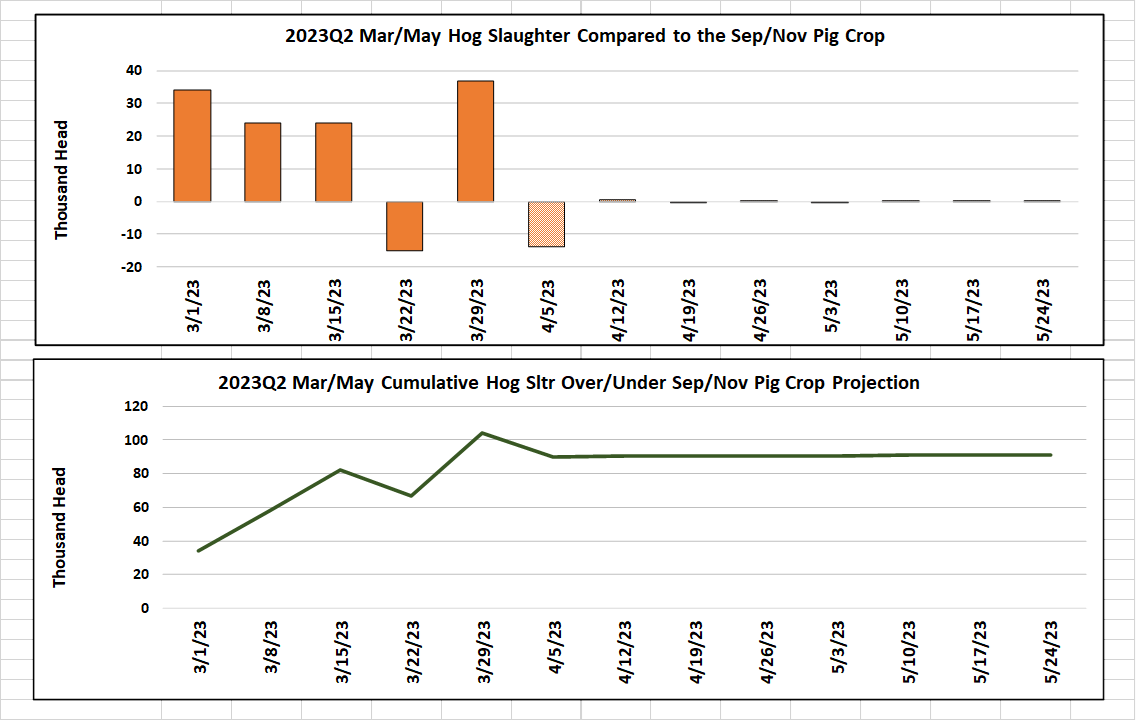

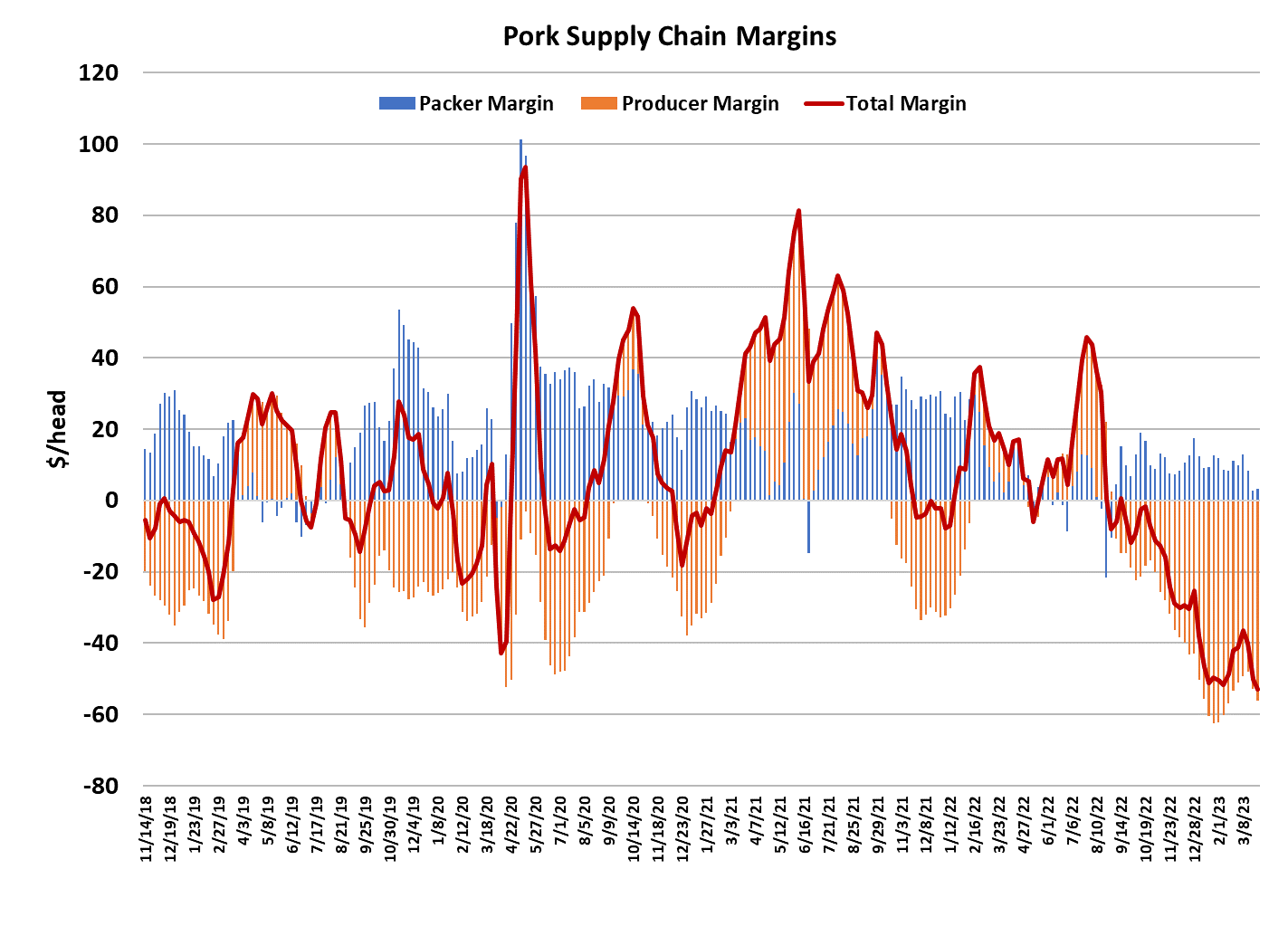

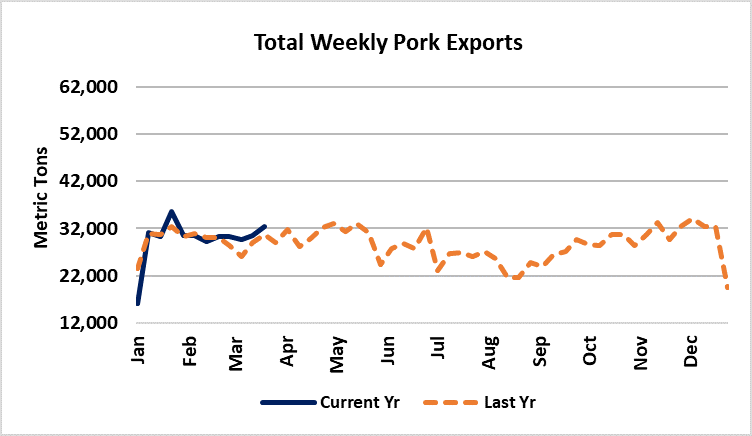

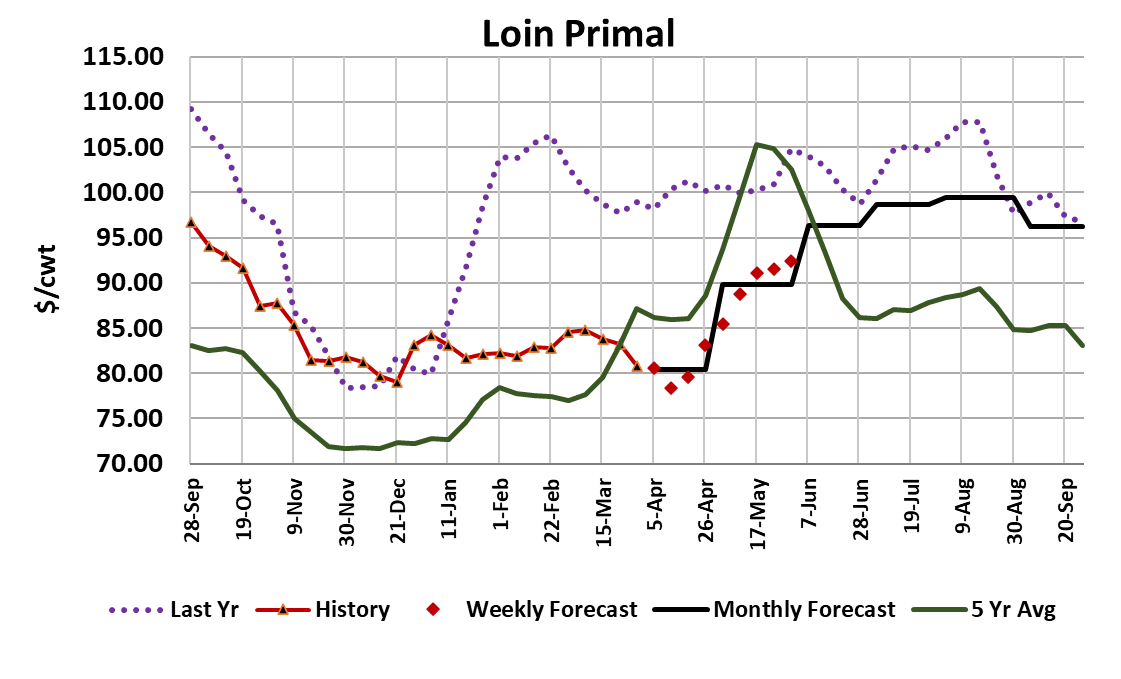

The soft undercurrent continued in the pork market this week. The cutout dropped $1.36/cwt. to average $79.51/cwt. for the week. There were two weeks in January where the cutout averaged just below $80, but other than that, the last time the cutout posted a weekly average this low was back in January, 2021. Observers sometimes forget that prior to the pandemic it wasn’t unusual to have a late-March cutout in the $70 and even $60s at times. So, I think the cutout is just reflecting a return to more normal markets in this post-pandemic environment. The concerning thing about this week’s decline in the cutout is that much of the weakness originated in the retail items. Loins and ribs were especially weak and butts are starting to look shaky also. We already knew there were problems with demand for the processing items, but if that is now spreading to the retail cuts, then there could be further cutout softness on the horizon. Ham prices are still in retreat and it is hard to imagine the cutout gaining traction as long as that feature is still in place. The belly primal averaged about a dollar higher than the week before, but that isn’t saying much. Last year at this time the belly primal was near $190. This week it averaged $86. Packers, frustrated by soft pork demand, are starting to push down on the cash hog market. The NDD negotiated market averaged $2.11/cwt. lower than last week. Packer margins, which were compressed by the sharp drop in the cutout the week before, expanded just a little to $3/head. Needless to say, producer margins are headed deeper into the red as hog prices fall. I calculate this week’s producer margin at -$56/head. The combined margin made a new all-time low this week. If it seems very dismal, it is. About the only ones enjoying this market are the futures bears. The Apr contract dropped over $2 this week and is now inside the two-week window until expiration. The failure of demand to firm at all in the past few weeks caused me to do a major downward revision in the price forecasts this week and I’m now looking for the cutout to spend a couple more weeks in the high $70s before shrinking production and improving demand lifts it back into the $80s. I see fair value for the Apr expiration near $73 and quite possibly lower. Perhaps the most remarkable thing about the hog and pork complex so far in 2023 has been the slow, methodical way in which prices have moved (mostly downward). Volatility in the cutout and hog pricing has been very low with very few big moves in any prices. Just a slow, steady drumbeat lower. The export trade has been very steady as well, holding close to last year in the weekly numbers and not showing much indication of wanting to improve or soften. There has been talk about a resurgence of ASF in China, but no one is in the mood to buy the hog futures based on that. We went through that exercise back in 2019 and, while exports and price levels in the US increased, they fell way short of the wildly bullish expectations that many market participants held. This time around, no one is speculating on China. It is more of a “show me” situation now. Next week will mark the end of Lent and grilling season is upon us now that April is here, so perhaps we might see some improvement in demand. However, the supply side of the market remains burdensome. This week’s kill was right at 2.5 million head, with over 100,000 scheduled to be slaughtered on Saturday. That weekly total was about 40k larger than last week, so packers are likely to start out next week with more pork to sell than they had this week. Next week’s slaughter should be down around 2.4 million head, owing to some lighter kills on Friday and Saturday ahead of Easter. That is a tiny piece of good news for the bulls. After Easter, we should see kills between 2.4 and 2.45 million head for a few weeks and by the time May arrives I’d expect to see weekly kills down around 2.35 million head. Barrow and gilt carcass weights were reported even with last year and seem to be in a normal sideways pattern right now. There are a lot of hogs out there, but because of their poor margins, producers have been working hard to keep pushing hogs out the door. So the weight data doesn’t suggest any backup in the production pipeline. We are still over-killing the pig crop, but astute readers may notice that this week the over-kill relative to the pig crop has gone way down. That is because USDA revised the Sep/Nov pig crop higher by 540k in this week’s Hogs and Pigs report. They also revised the summer 2022 pig crop up by 580k. We have known for some time that those pig crops were under-estimated and now USDA has finally corrected most of that. The report also told us that the breeding herd expanded slightly from last year, but was down modestly from the previous quarter. All of that was anticipated in my production forecasts, so it didn’t change much as far as future supply estimates go. The most important number in the report, the Dec/Feb pig crop, was estimated to be up 0.3% YOY. That was a little smaller than the increase I had built in, but given their recent track record on under-estimating pig crops, I’m not convinced that I was too far off. We will find out this summer when the industry starts to kill hogs born in Dec through Feb. In all, the H&P report didn’t contain many surprises and didn’t alter my forward supply picture much. Farrowing intentions for the next 2 quarters were reported to be relatively light and that could be an indication that poor profitability has producers thinking about scaling back their operations in the second half of the year. Clearly that needs to happen because producers are drowning in red ink at current production levels. Next week, expect more easing of the cutout and cash hog markets. Production should be down next week and that might lead to some modest price gains in the week after Easter, but that will come too late to help the Apr contract.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}