Pork Wrap March 3

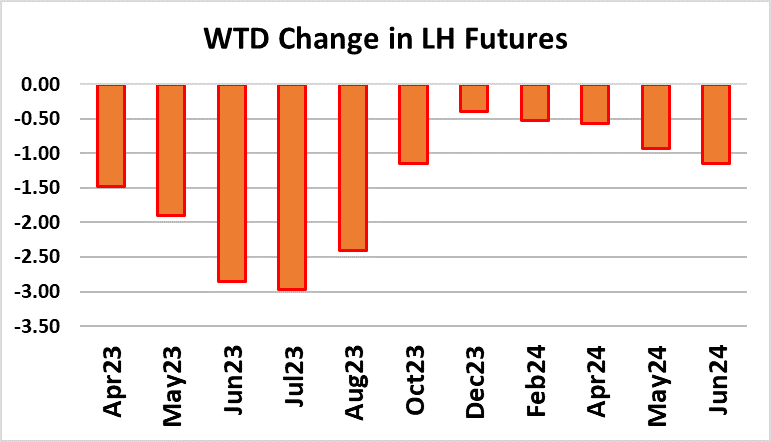

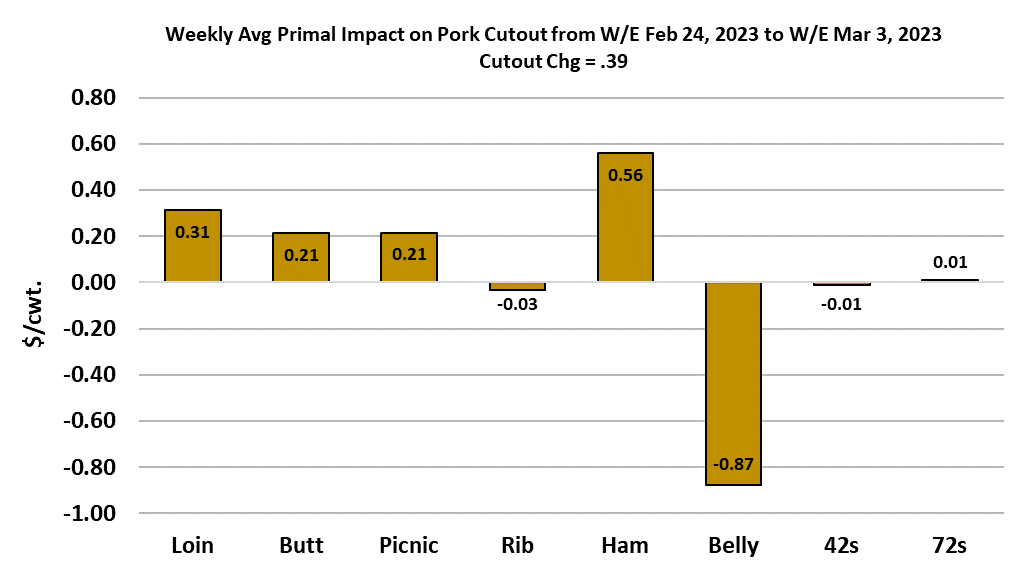

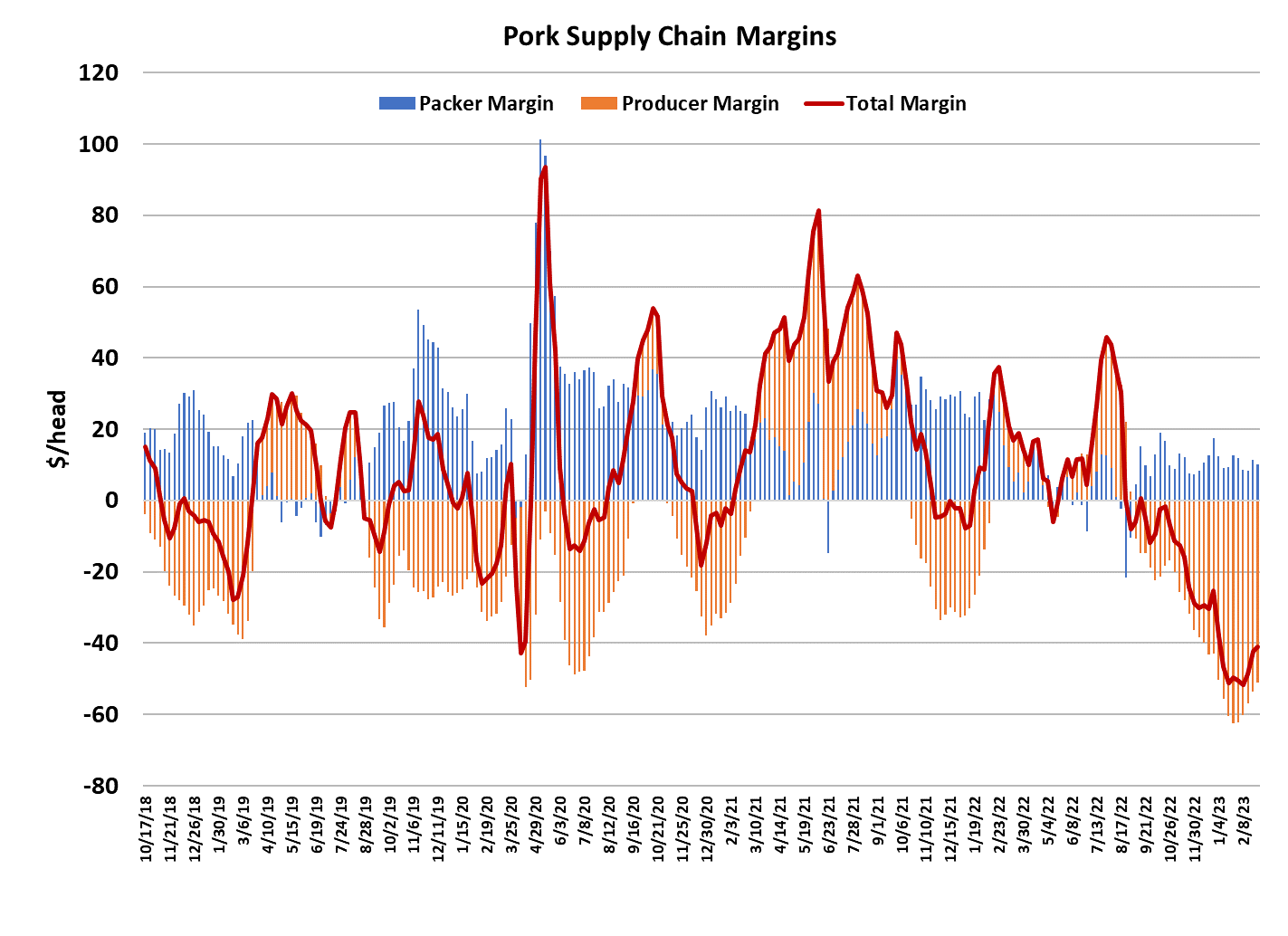

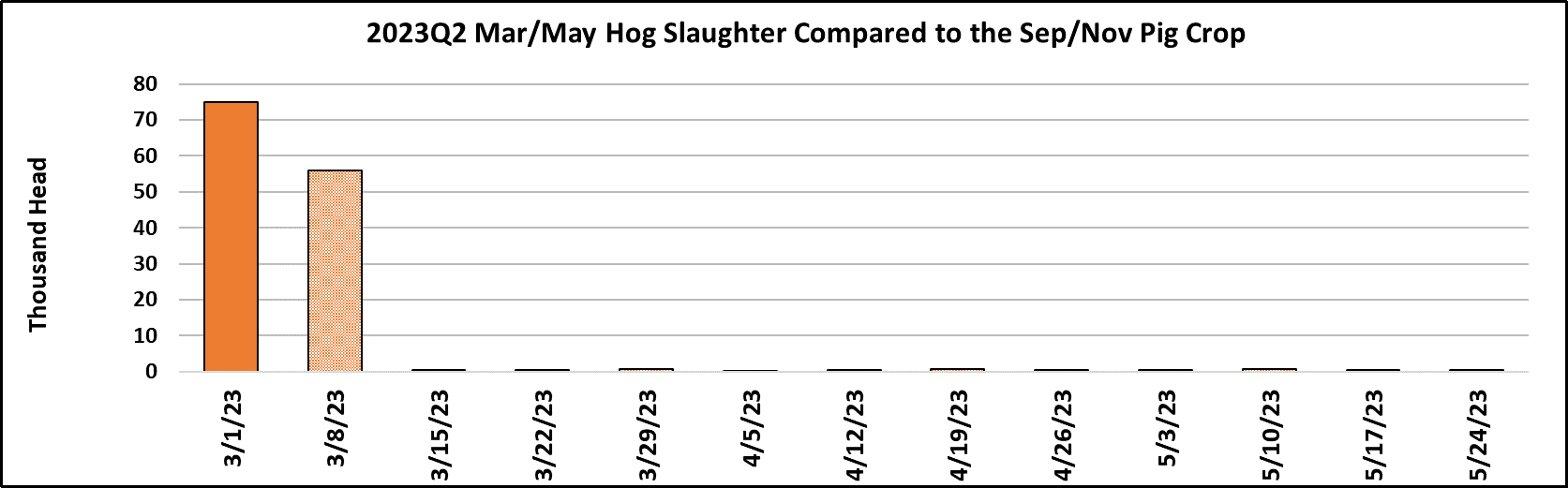

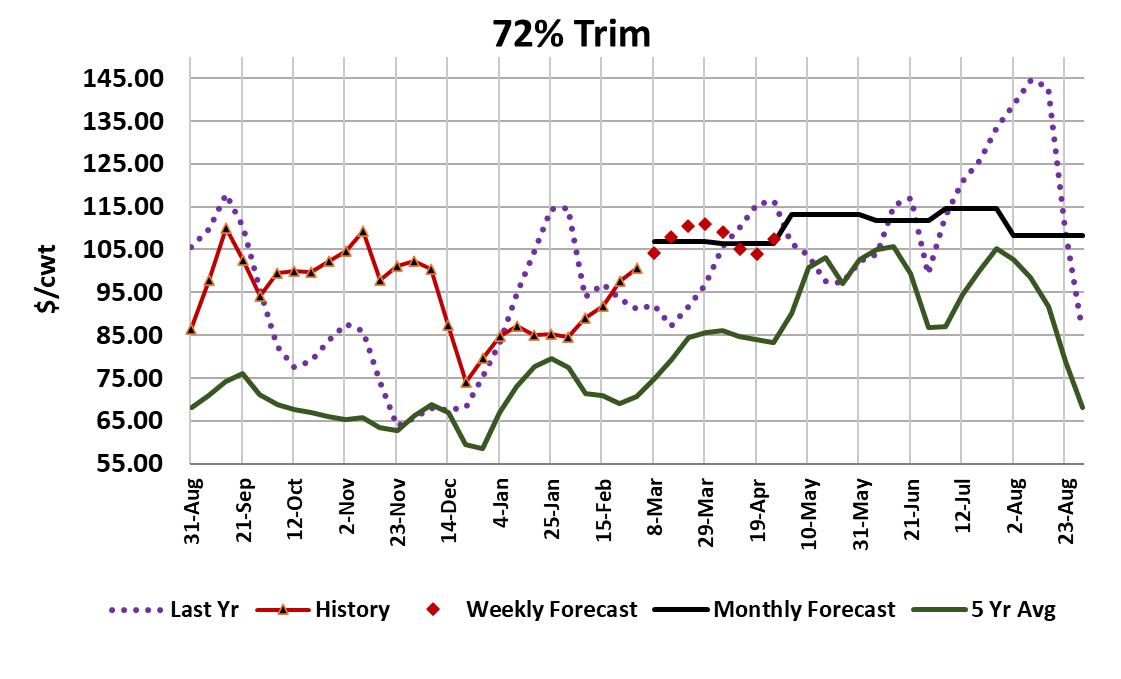

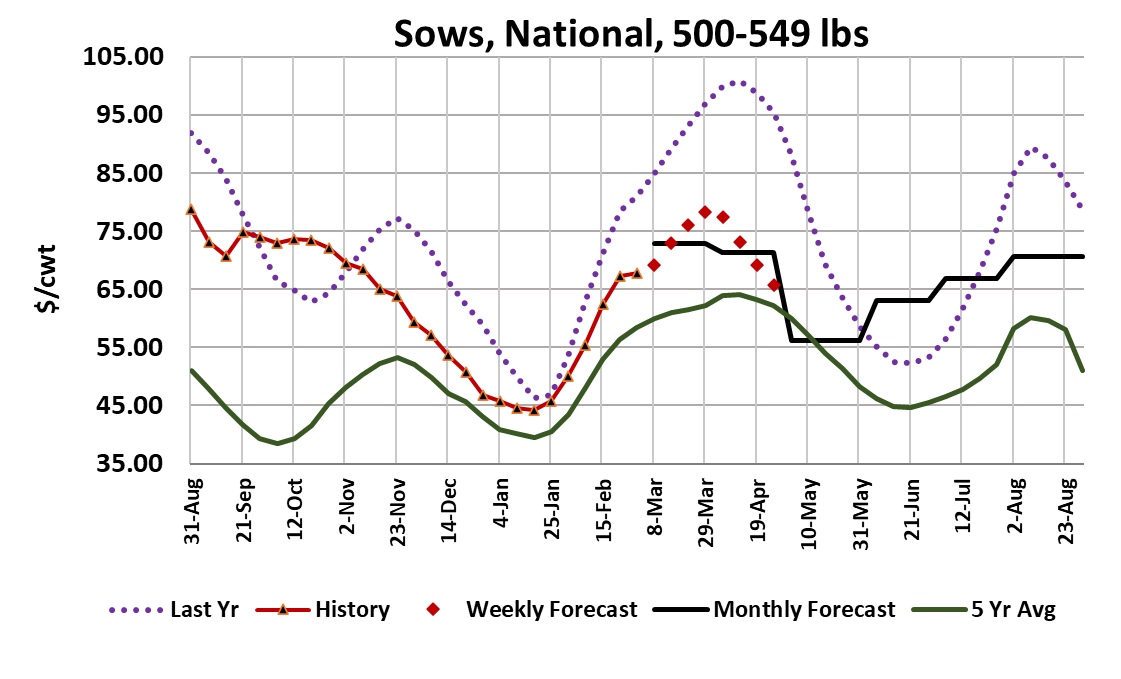

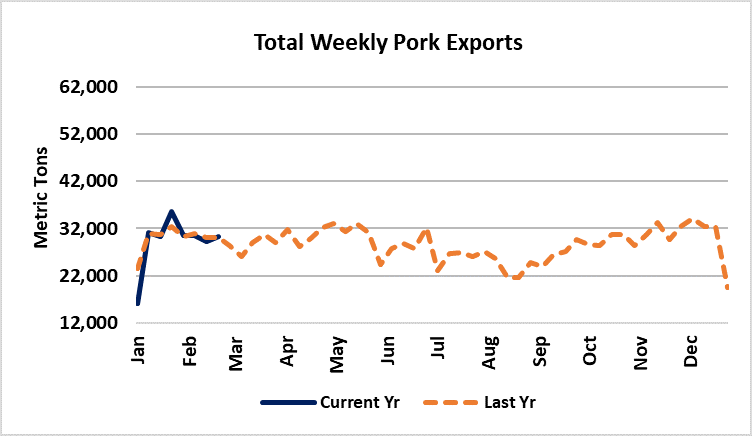

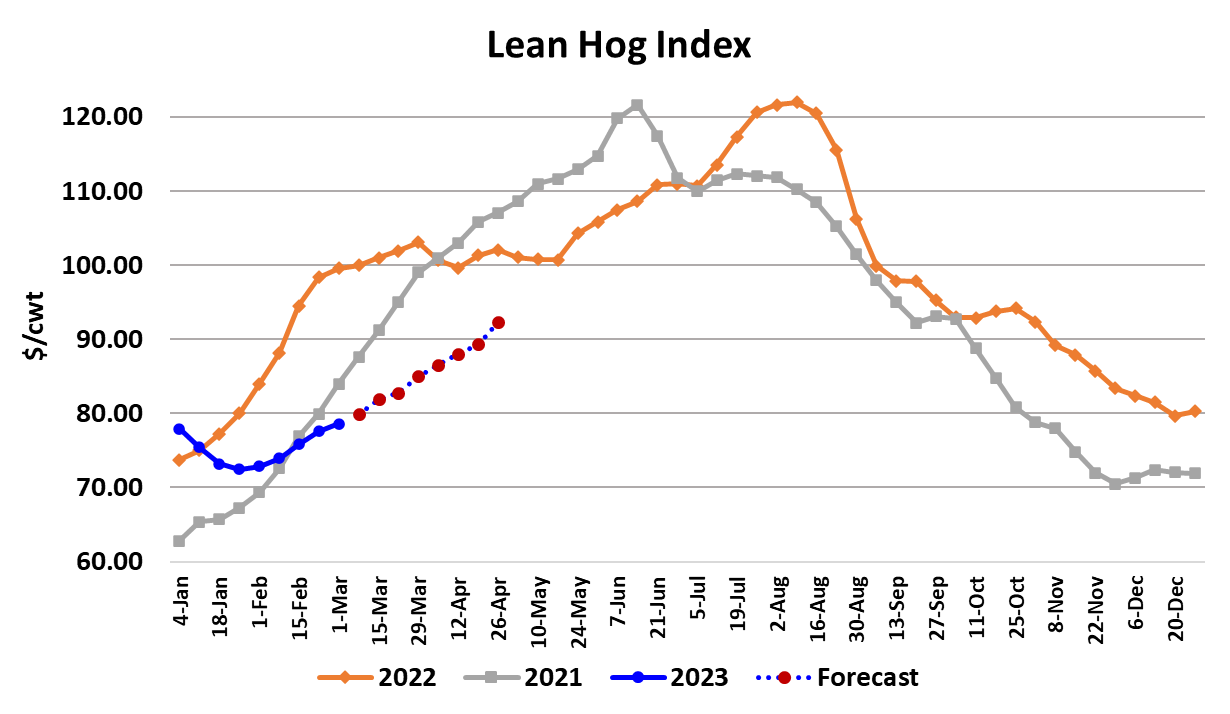

After last week’s solid move higher in the cutout, this week it was back to the same-ole, same-ole with the cutout only adding a measly $0.39/cwt on the week. It was a similar situation in the negotiated hog markets where the WCB gained $0.32/cwt and the NDD was up $0.61/cwt. Packers got caught up on the kill after weather curtailed the previous week’s harvest. This week’s slaughter registered 2.52 million head and was the biggest weekly kill since the first week in February. It was also about 70k larger than what the pig crop projected. We are now working on the Sep/Nov pig crop and, just like the previous quarter, kills continue to come in larger than anticipated. Carcass weights bumped a pound higher in this week’s FI data release, so that isn’t helping the supply picture either. If these bigger-than-expected kills persist, it will likely add to an already-large cold storage inventory and thus limit price gains this summer. Futures traders are obviously growing weary of the big kills and the inability of price levels to move significantly higher. Nearby Apr lost $1.50/cwt on the week and the summer contracts lost closer to $3. Pork buyers have grown accustomed to ample pork availability since October, so what is really needed to jump start this market is for kills to start shrinking seasonally. That might not happen right away, but by the end of March I would expect to see weekly kills closer to 2.4 million head per week. By that time, carcass weights should also be working seasonally lower. The current forecast has the LHI at April expiration near $87/cwt., but that might turn out to be too high if kills continue to run large. This week, it was the belly primal holding the cutout down while all of the other primals pushed a little higher. The last time we had belly stocks this large during Q1 was in 2020, and while the onset of the pandemic muddied the data somewhat, the bellies never really got much traction until near the end of summer. If that repeats again this year, it will be a tough year for the bulls in the hog market. I do think that demand is currently in an upcycle and the combined margin confirms this, but the rate of gain in that indicator slowed a lot this week. Perhaps warmer weather and the arrival of spring in a couple of weeks will boost demand. It is also possible that we could see retailers lean more heavily on pork in the next couple of months as they start to shy away from the very expensive beef market. The loss of the pandemic-inspired supplemental food stamp benefits by millions of lower-income Americans at the end of February could drive more demand away from beef and towards pork. So, there are reasons to be hopeful for pork demand this spring. However, the negatives on the supply side such as bigger-than-expected kills and large cold storage stocks don’t require hope—we can see them right now in real time. They say a bird in the hand is better than two in the bush, and right now what we have in our hands is a pretty negative supply-side picture. Hams are offering perhaps the most encouragement right now. That primal has added $10/cwt over the past three weeks and seasonally tends to continue higher into the summer. Easter falls on April 9 this year so processors are starting to run out of time to get hams processed, packaged in and in the stores for Easter features. However, as summer approaches, hams usually get a demand boost from processors preparing deli and sandwich items. The trims have also performed well, with the 72s now above last year and trending higher. One thing to keep an eye on is sow pricing, which has also been in an uptrend, but this week the gains really slowed. Since trims and sow meat often go into the same products, one can affect the other and it is starting look like sow prices might be making a top well below last year and well below the fundamental forecast. Export demand hasn’t been much to write home about so far in Q1, so I’m not particularly hopeful that the export markets will bail the industry out this year. The weekly data have exports holding very close to last year. Given that the cutout is about $25 below last year, this is an indication that export demand is down. Mexico has the potential to import a lot of US pork because their internal pork prices are well above those in the US, but so far the data hasn’t revealed bigger volumes heading south. China is covered up in domestic pork right now and prices are low, so I don’t think the Chinese will be siphoning off a lot of additional US pork this year. Hog producers remain in a big financial bind, with cash-to-cash margins this week estimated to be more than $50/head in the red. We will get a fresh Hogs and Pigs report on March 30 and I think producers are going to report a smaller breeding herd than they did in the previous quarter. High corn prices combined with soft pork demand are crushing producers and sending a signal for them to scale back. Packer margins this week were just under $10/head, which isn’t great, but at least margins are positive. If hog supplies had come in closer to what USDA projected, then I think packer margins would be smaller and producer margins less negative here in Q1. Packers and retailers have been the main beneficiaries of bigger-than-expected Q1 hog numbers. That storyline might well extend deep into Q2 also. Next week, watch the daily kills and negotiated pricing for any sign the hog supply is starting to tighten up. My current forecast is for the kill to come in right around 2.5 million again next week and that would be around 50k more than the pig crop implied.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}