Pork Wrap March 29

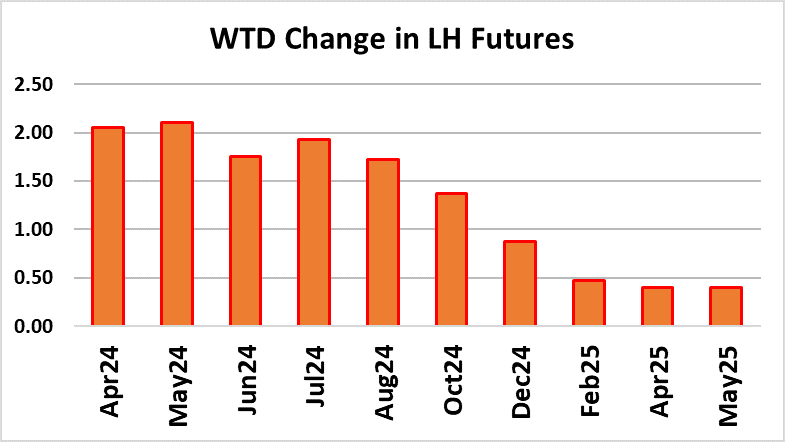

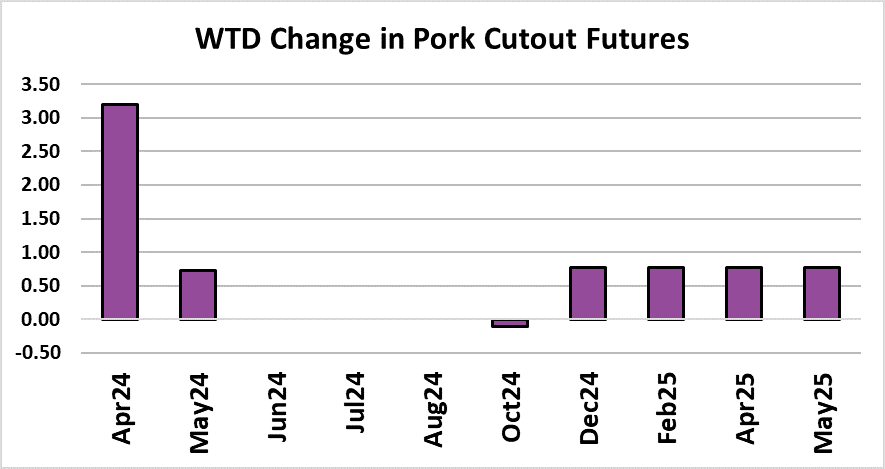

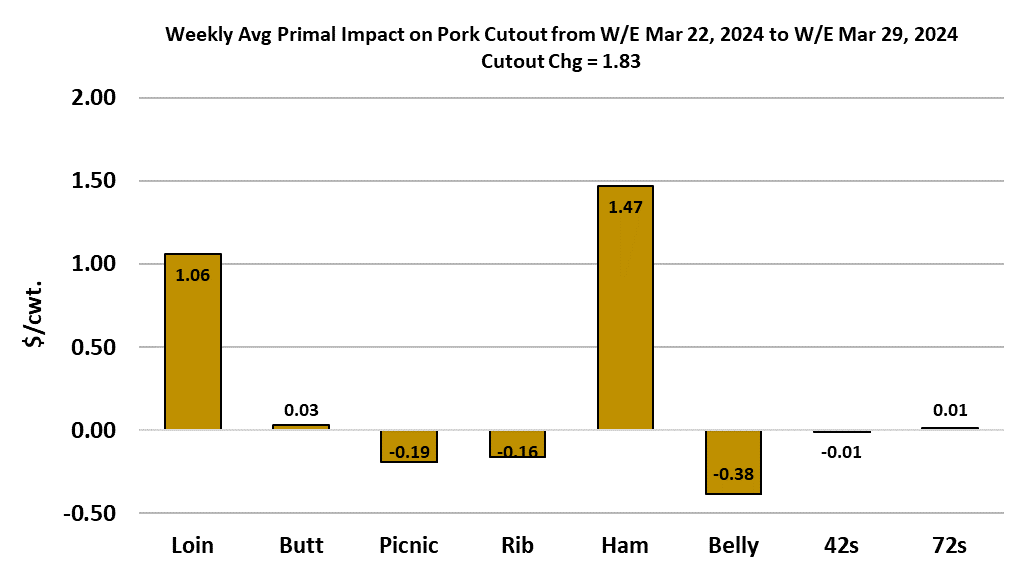

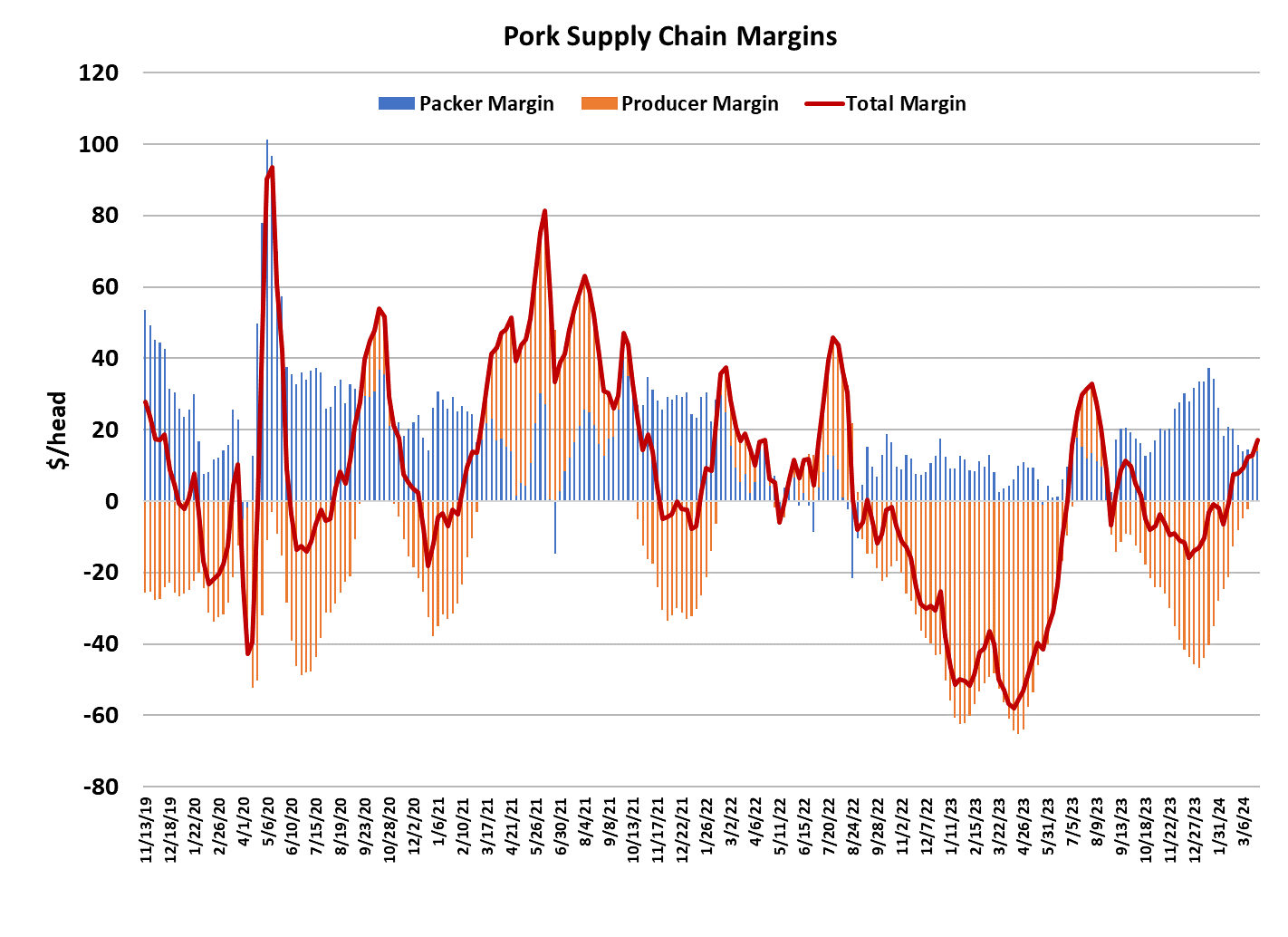

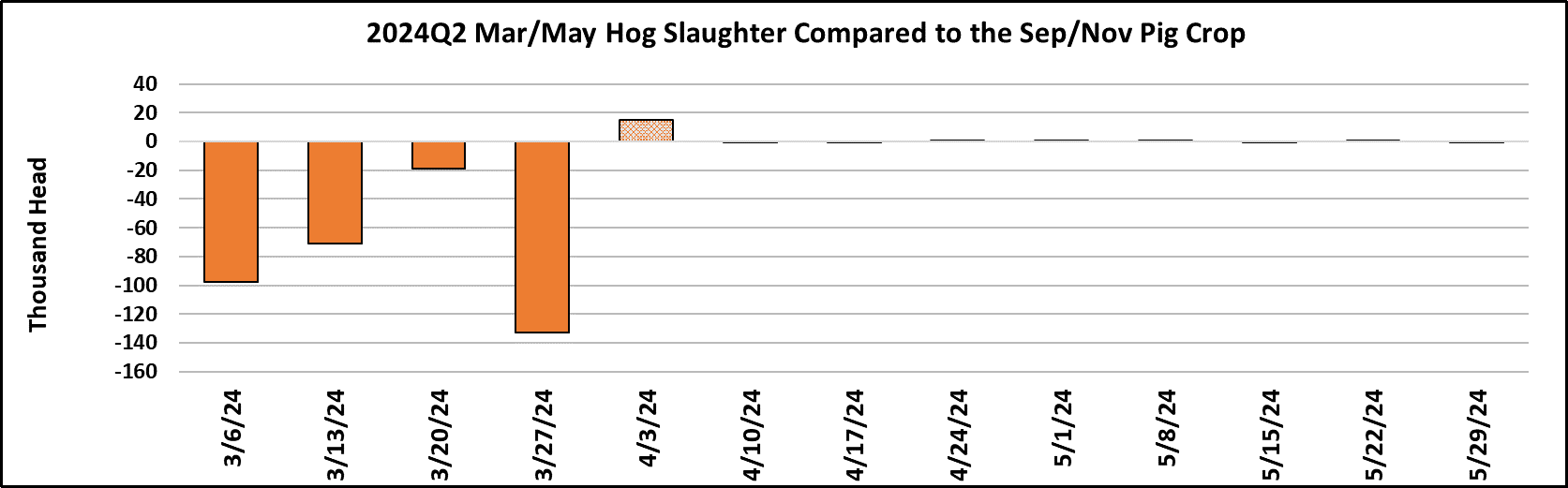

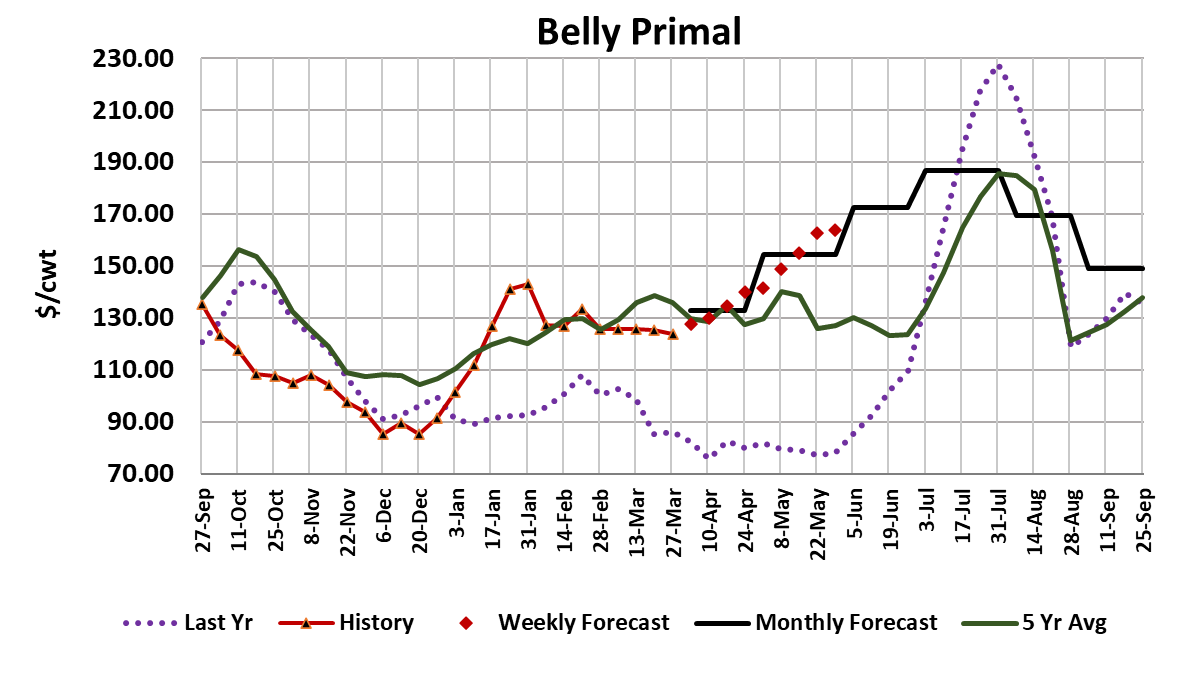

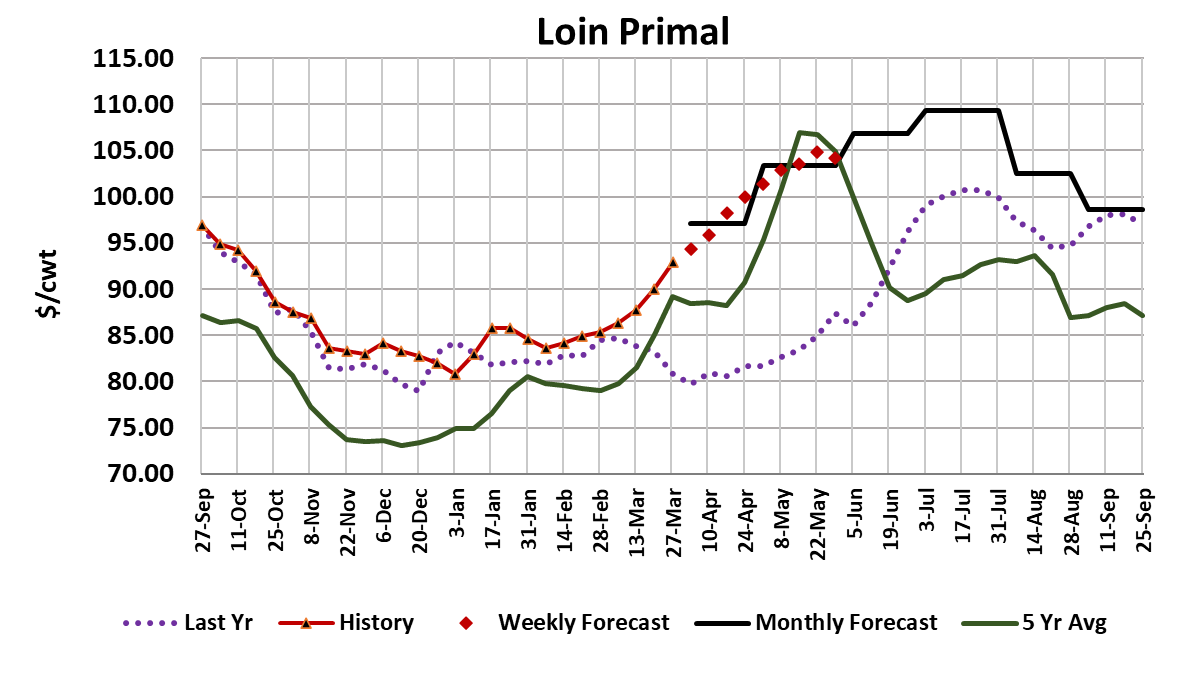

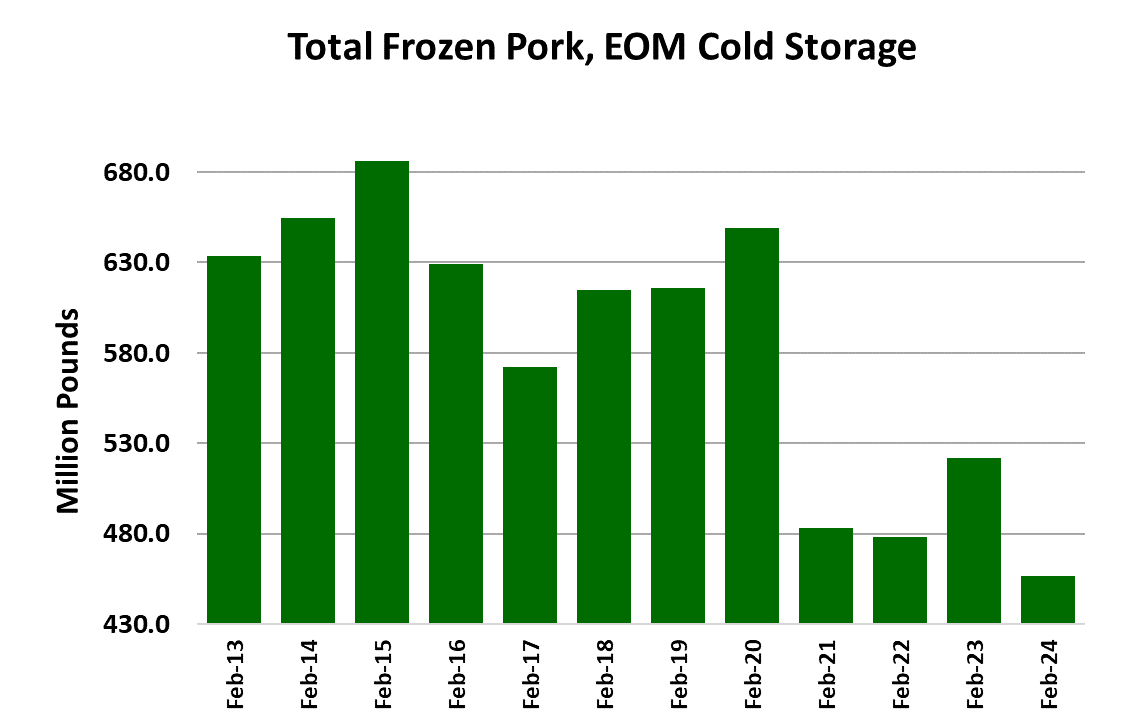

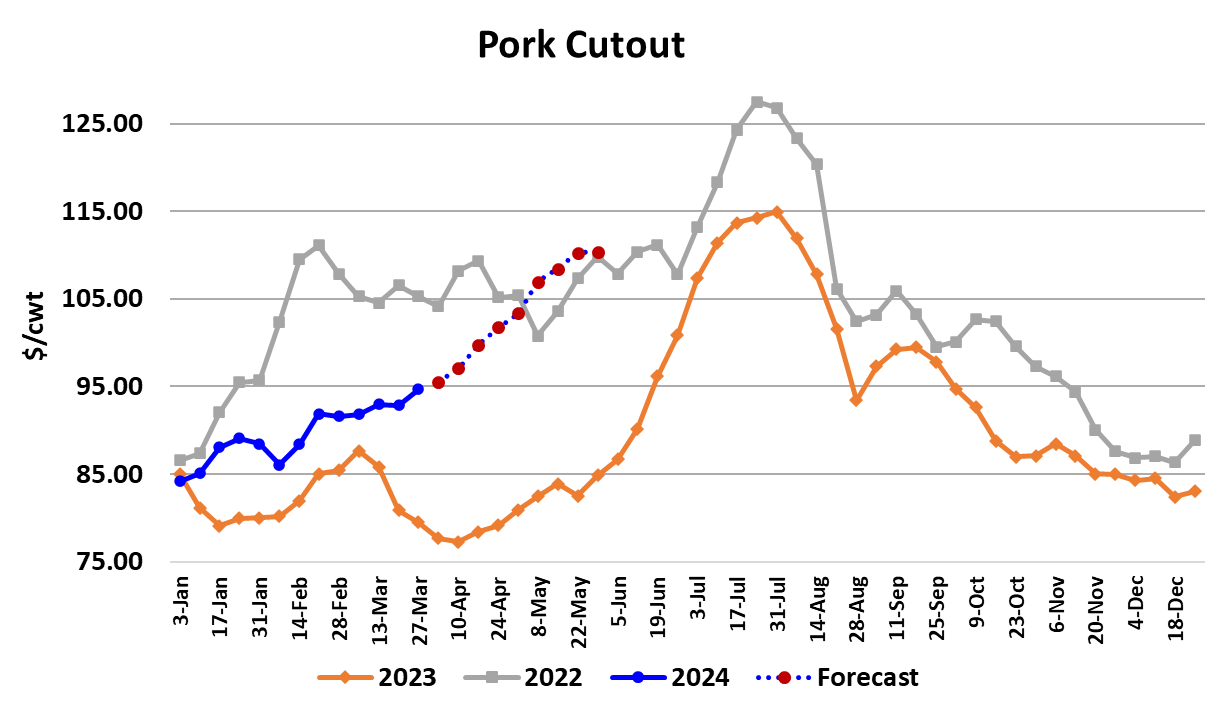

The pork cutout gained a little more traction this week, increasing $1.83/cwt. to average $94.66 for the week. Negotiated cash hog prices were more sluggish, with the WCB only gaining $0.10 on a weekly average basis. That helped add a couple of dollars back on packer margins, which now stand at just under $14/head. That’s a substantial improvement over the past couple of years where margins were averaging under $5/head in the last week of March. As long as we are talking about improvements, we should consider producer margins which this week are around +3/head. Last year in the last week of March they were -$61/head. Clearly, things much better in the production sector this spring. In the pork markets, the notable event this week was improving ham pricing. The primal added almost $4 on a weekly average basis and appears poised to make further gains next week. That is great news for the bulls, but it would be even better news if the bellies weren’t pulling the cutout in the opposite direction. The belly primal slipped a couple of bucks this week and the print on Friday was particularly ugly. I’ve had to scale back my near-term belly forecasts, resigning myself to the idea that this is probably going to be a slow spring for bellies. I still hold high hopes for summer, with the primal expected to reach $190 at some point in July, but right now with the primal sitting at $123, that looks a long way off. Bellies have a reputation for highly volatile pricing, but for the past two months the primal hasn’t deviated much from the $125 level, except for a brief trip to $130 in third week of February caused by light volume. Long periods of flat pricing are uncharacteristic of bellies and it makes me wonder if perhaps something has changed in the cash market. The other unsung hero of the cutout has been the loins, which make up a little over a quarter of the cutout value, and have been quietly doing the yeoman’s work helping the cutout to grind higher. The price trajectory there has steepened in recent weeks and the primal appears on track to reach the low $100s before Memorial Day. I guess if I were to summarize the current state of the cutout, I’d say the hams look promising, the bellies are disappointing and all of the other items are doing well in their supporting roles. That gives me confidence that the cutout will remain on an upward path and should be trading in the upper $90s two weeks from now when the Apr futures expire. As of today, my target for Apr expiration is in the $87-88 range, but the futures have so far been reluctant to go there for any length of time. They may be even more reluctant on Monday when traders will get their first opportunity to react to Thursday’s Hogs & Pigs report. USDA reported a 2.1% decline in the breeding herd, but the consensus was looking for something closer to a 3% decline. That is modestly bearish, but what is even more bearish is the finding that the number of pigs saved per litter jumped to a 4.6% YOY gain, while analysts were only expecting a 3.3% increase. So once again, gains in productivity have more than outweighed the progress that producers were making in reducing their breeding stock. The end result was that the Dec/Feb pig crop posted a 1.9% increase and those are hogs that will be slaughtered in the upcoming Jun/Aug quarter, so buyers should find pork availability this summer a little better than originally thought. When I incorporated all of USDA’s numbers in place of the forecasts I had been carrying pre-report, it knocked the forecast for the July cutout down from $125 to $118. Since then, I’ve dialed back summer demand expectations somewhat and now project the July cutout to average closer to $116. I have the LHI topping averaging close to $111 in July and while that is down from earlier projections, it is still more than $7 over where the Jul futures finished the week. My guess is that traders will come out selling pretty vigorously on Monday, particularly in the summer and fall contracts. If Apr gets caught in the crossfire and moves lower, it could prove a good buying opportunity. There is some concern that recent margin improvements in the production sector will cause producers to curtail their plans for reducing the breeding herd. With productivity running this strong, that could end up creating another margin disaster for them later this year and in early 2025. If anything, Thursday’s H&P report should be telling them they need to cull harder and deeper in order to offset strong productivity. USDA provided a cold storage report that was moderately bullish this week, showing cold storage stocks at the end of February down 12.5% YOY. During the month of February, USDA reported a net drawdown in cold storage inventories of about 7 million pounds, when normally the industry is still building stocks during February. The 10-year average change in cold storage stocks between the end of Jan and the end of Feb is +37 million pounds. Thinner cold storage holdings heading into spring improves the odds that the cutout will remain on its upward trajectory and raises the risks of stronger-than-expected pricing this summer. The weather over much of the US this Easter weekend will be very mild and that bodes well for the start of grilling season as the calendar turns to April. Next week look for another couple dollars higher in the cutout and negotiated hog prices, but be prepared for a volatile start to futures trading on Monday.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}