Pork Wrap March 25

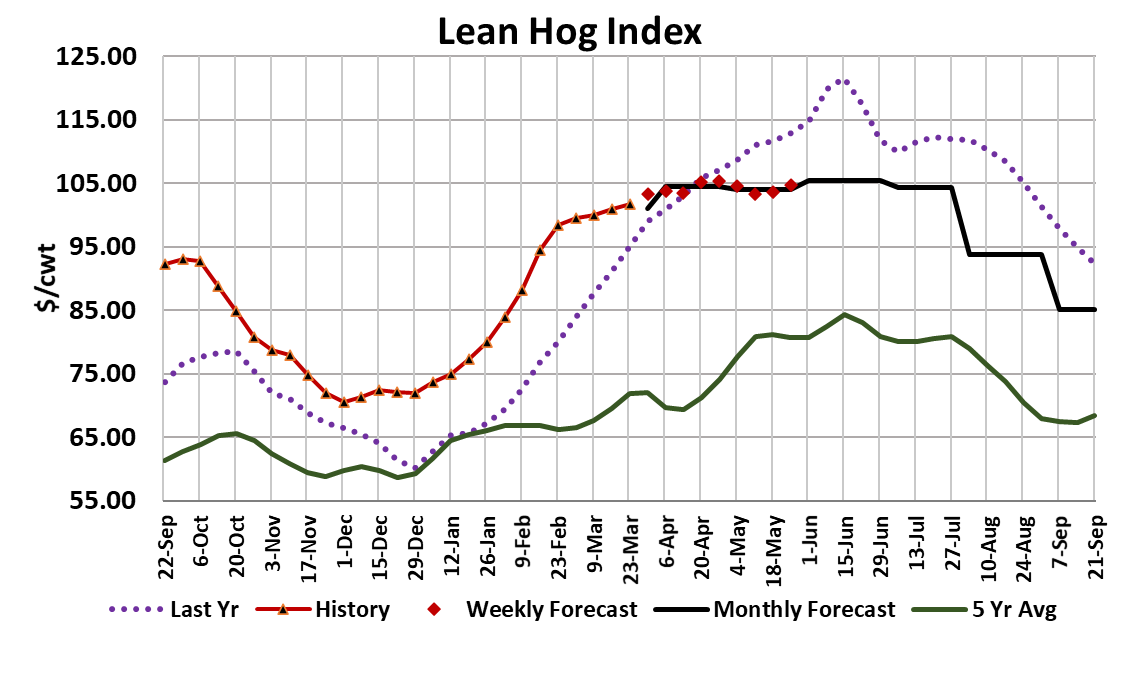

The bulls in the hog market had been frustrated in recent weeks by

softer cutouts and mostly sideways LHI. However, when the cutout

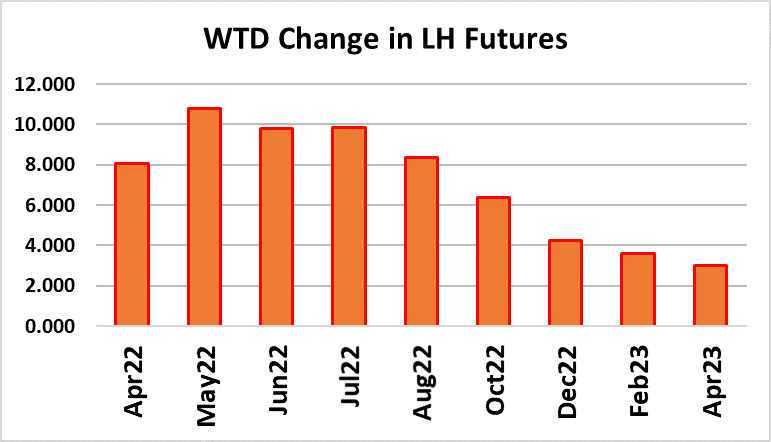

showed a modest amount of strength this week, the bulls exploded

onto the scene, forcing the Jun contract up almost $10/cwt. That

really seems like an excessive reaction in a week where the cutout

only gained $1.95 and the WCB negotiated market was flat with the

week before. I chalk it up to pent-up bullish enthusiasm. Now comes

the hard part. The market has to live up to the high expectations that

futures traders have set for it. We have been waiting for the pork

demand cycle to turn higher and it may have accomplished that this

week. The combined margin is showing a slight uptick, but we have

seen those before and then the combined margin continued lower.

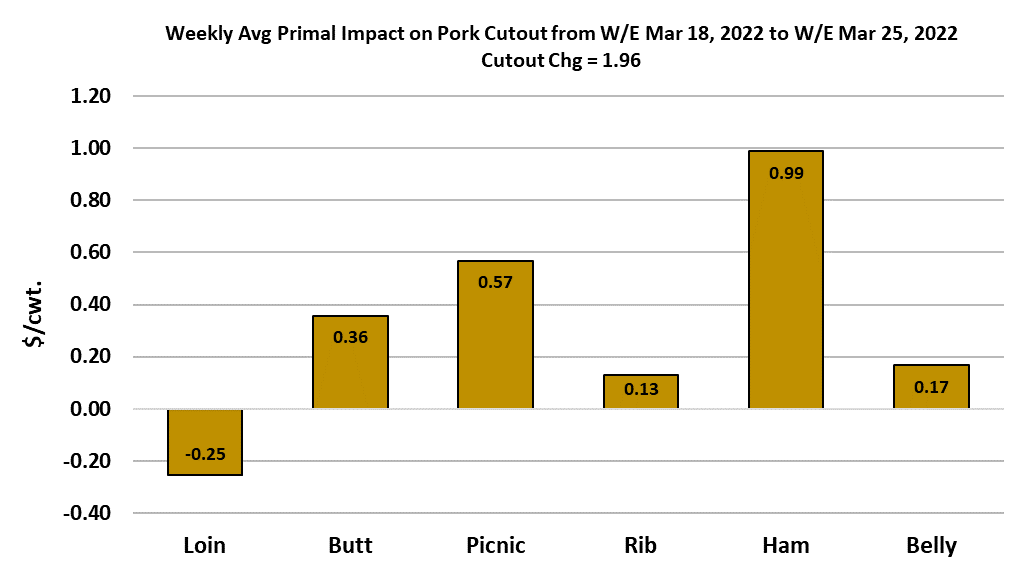

The gain in the cutout this week was driven by stronger ham pricing,

with a little help from the butts and picnics.

There were a couple of points during the week where the bellies

looked like they were about to surge higher and perhaps that is part of

what stoked the futures so much today. However, those all turned

out to be false signals generated by light volumes. The up-move in

ham prices is definitely real however, and it could be driven by

stronger export business to Mexico. By now, all of the Easter hams

for US retailers have been bought and processed, so I doubt that it is

stronger domestic demand that has been moving ham prices higher.

We are definitely seeing more boneless hams in the mix these days

and that has the effect of raising the ham primal value. I have to

surmise that packers are seeing labor availability improve. That is

important for sure, but prices for bone-in hams have also been

moving higher recently and when we combine the two effects, the

result is stronger ham primal values. I’m a little surprised that loins

haven’t performed better since that is a retail favorite for grilling

season.

Perhaps we are just not far along enough in the calendar for that to

occur. It is also possible that the modest upward turn in the cutout

this week has its origins in smaller pork production rather than any

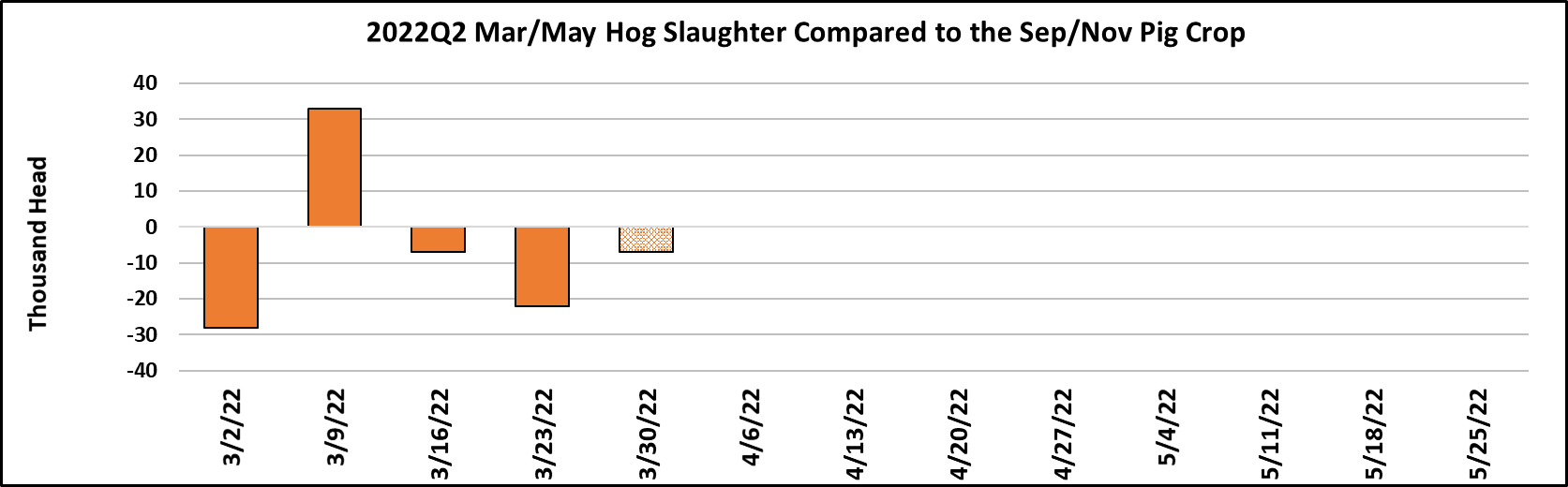

significant demand strength. Kills are working seasonally lower now

and this week’s total came in at 2.42 million head, about 10k less than

the week before and about 20k less than what the Sep/Nov pig crop

implied. That is not a very big deviation from the pig crop, so for now

I’m assuming that USDA was pretty close in its estimate. There has

been a lot of speculation about disease problems limiting the supply

of hogs, but if that were the case I would expect to see kills coming in

way below the pig crop estimate and so far that hasn’t happened.

We will get a clearer picture on Wednesday when USDA releases its

next issue of Hogs and Pigs.

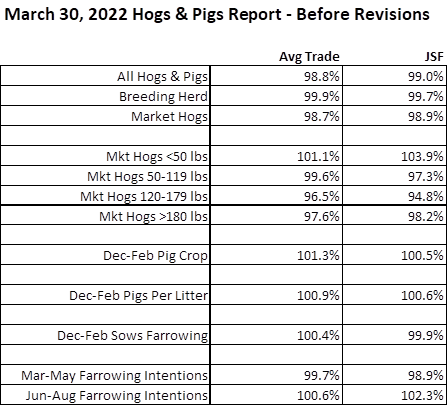

I’ve included a table here that provides the average trade estimate

for the important numbers in that report along with the JSF

projections. Expectations are for the total herd and breeding herd to

be down only slightly from last year, with a modest gain in the pig

crop due to productivity improvements. If there are more disease

problems than normal, then I would expect it to show up in a weak

pigs-saved-per-litter number and perhaps smaller than expected

farrowings. I think that the biggest risk heading into this report is

that it will show more contraction in the herd than the average trade

or JSF’s forecast. If that happens, it could be like throwing gasoline

on a fire in the futures because the summer contracts have been

exceedingly bullish and a smaller-than-expected pig crop would

have the effect of confirming the bulls’ bias.

If it goes the other way and supplies are reported larger than

expected, I suspect it won’t have near the same effect to the

downside. The bulls in the market seem to be pretty resolute right

now. They honestly believe that hog supplies are going to be very

tight this summer and no amount of USDA data will convince them

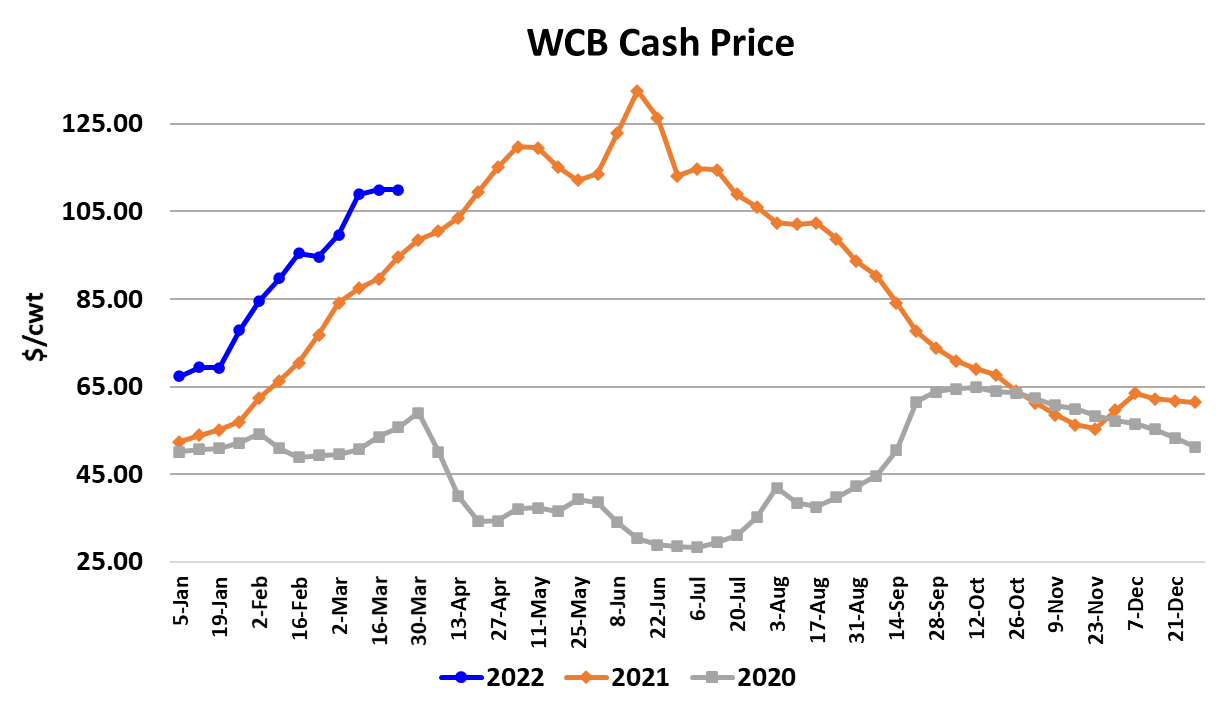

otherwise. It is interesting that the WCB negotiated price seems to

have stalled out around $110/cwt for the past couple of weeks.

Perhaps packers have adjusted their slaughter expectations

downward to better fit available supplies. This week the WCB cash

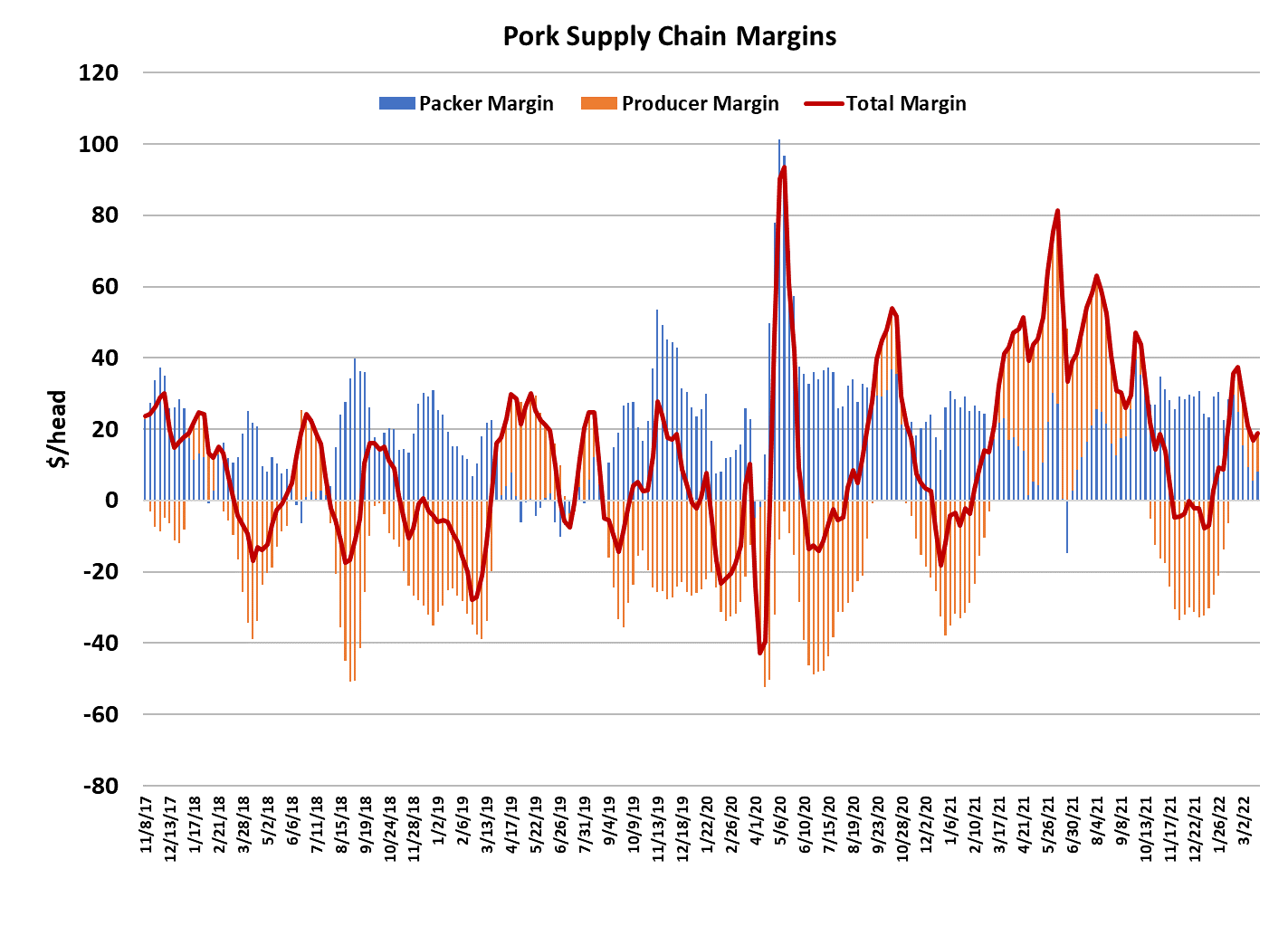

hog price was more than $3 higher than the cutout. That is a very

unusual occurrence, but it does point toward very small packer

margins. I have this week’s margin at $8/head, with risk that it

shrinks even more if the cutout struggles to hold on to the small gain

it made this week. Producer margins are larger than packer

margins, which is also a very rare occurrence. This week’s

producer margin was about $11/head.

Prior to 2020, it wasn’t unusual to see producers $10-20/head in the

red during March. Last year, producer margins averaged a little

over +$8/head—their best margin since 2014. I don’t think they will

be able to build on that this year with corn prices so high and

demand likely to fade from last year’s level. More likely, the

average margin for 2022 will be below zero and perhaps by a

substantial amount. That makes the decision not to expand the

herd look very smart in the current environment. Next week, we will

be watching for confirmation that the demand cycle has turned

higher and a stronger cutout would be the first clue. Futures traders

have already placed their bets that the upcycle has begun. There

could be a rather strong negative reaction if that turns out not to be

the case.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}