Pork Wrap March 24

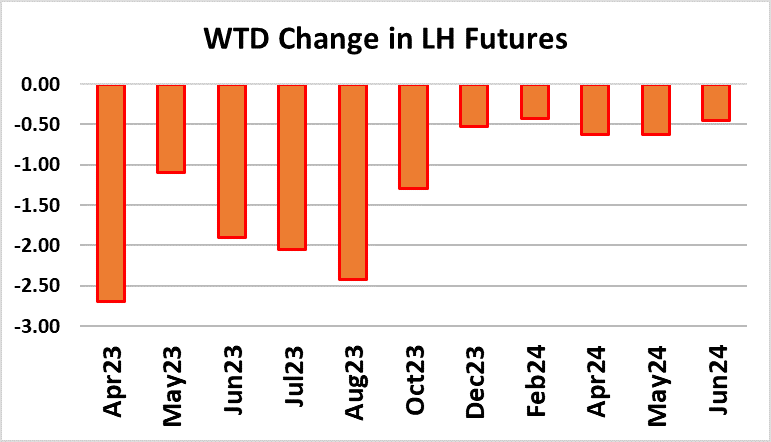

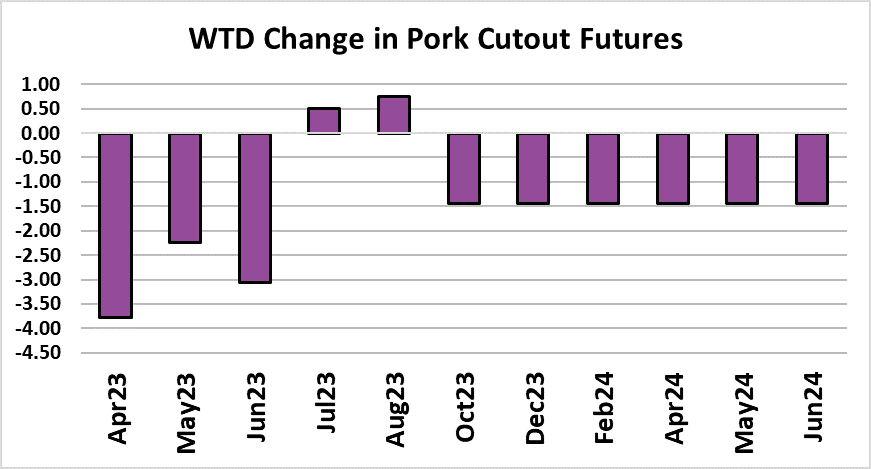

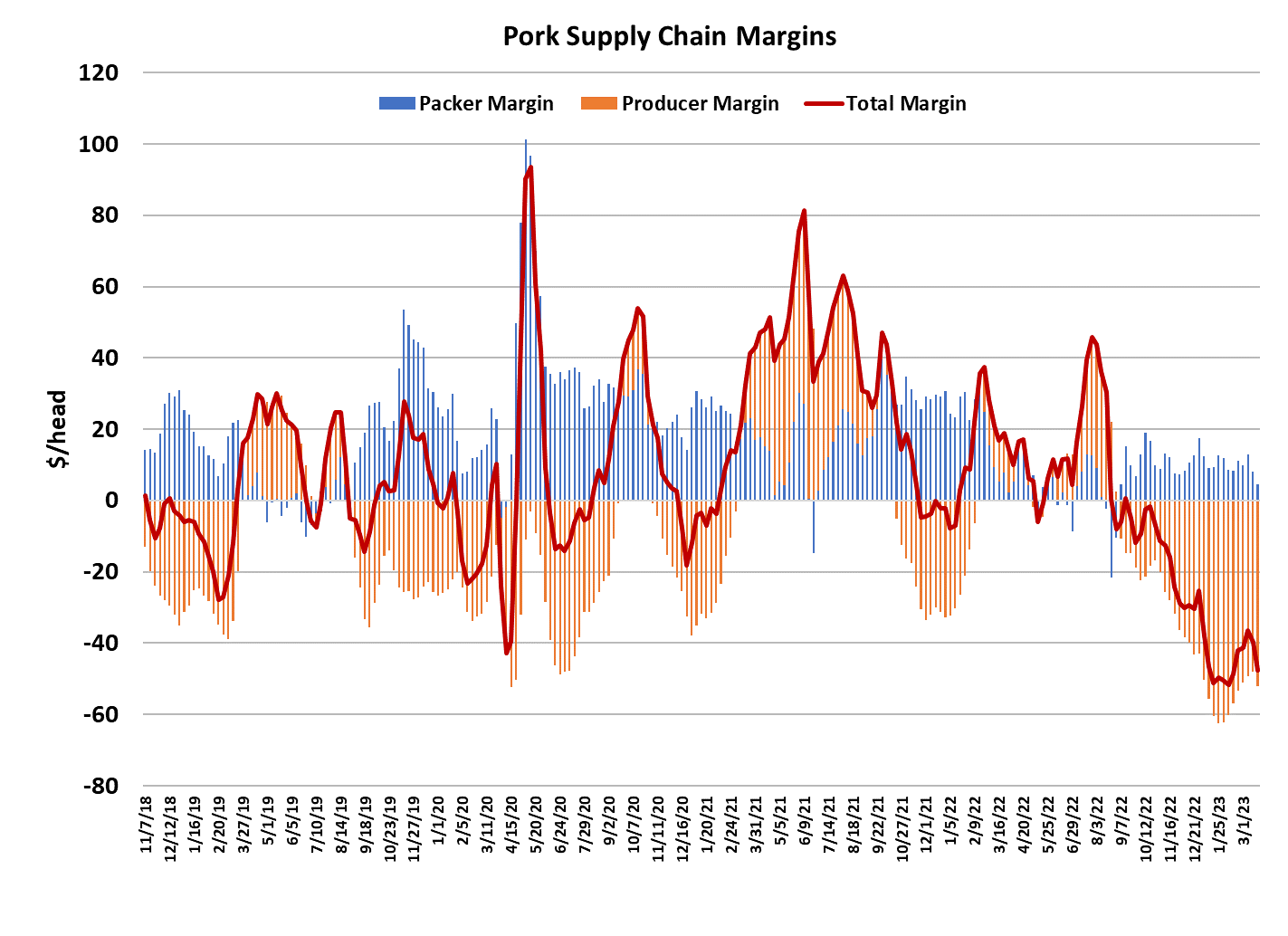

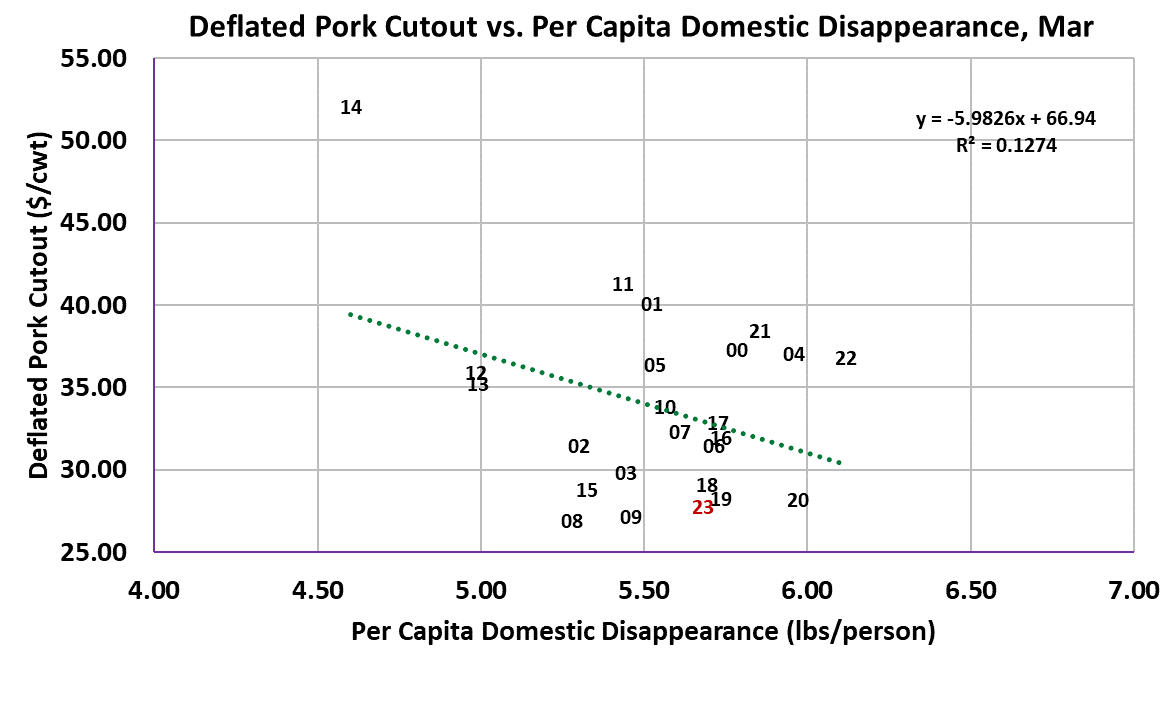

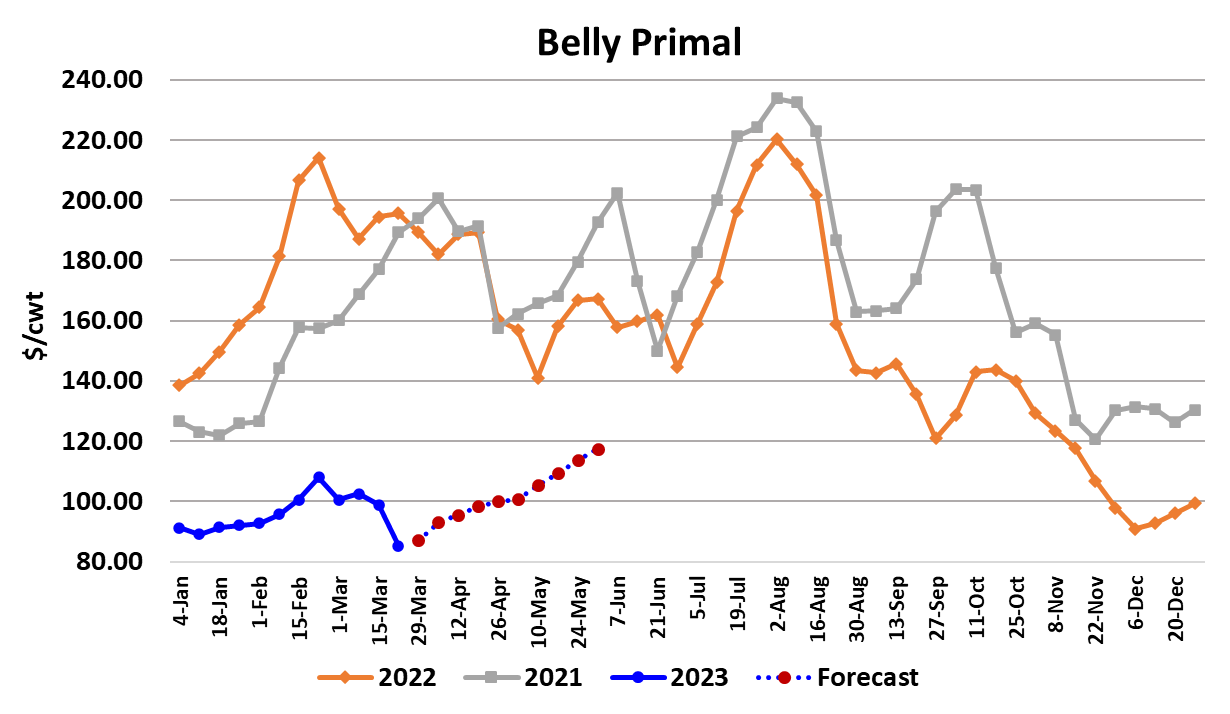

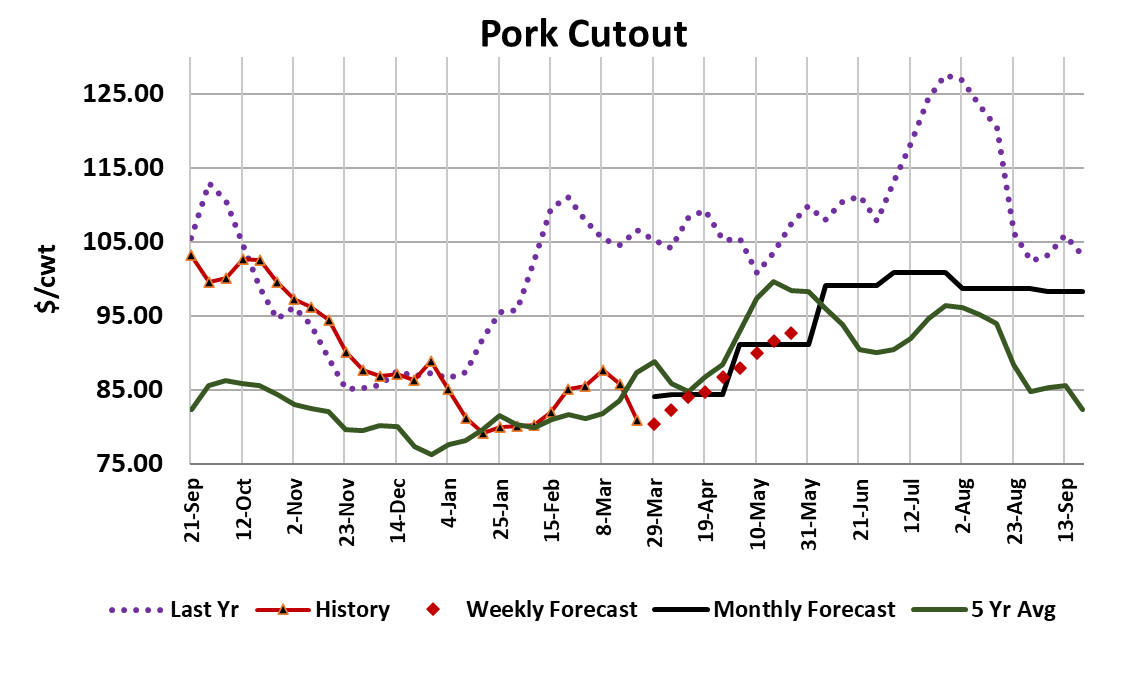

Late last week the pork cutout posted a sharp drop and, while it didn’t drop much further this week, it didn’t go up any either. As a result, the pork cutout was down $4.92/cwt on a weekly average basis. The week the cutout averaged $80.97/cwt and when it was at that level back in early February, the LHI was printing close to $74/cwt. This week, the LHI averaged just a little below $78, so that raises the question as to whether or not we can expect to see further softening in the LHI if the cutout stays mired around $80 like it did for so much of January and February. Hog supplies seem relatively abundant for this time of year and that suggests that packers won’t have much trouble pressuring cash hog prices lower if the cutout remains on the defensive. This week packer margins only averaged about $4/head, down from $8/head the previous week. That is simply a result of the cutout dropping hard without a commiserate decline in cash hog prices. The NDD negotiated market was down only $0.75 to $77.08/cwt this week. Look for packers to put more pressure on the cash hog market next week in order to improve their margin. Bellies and hams were largely responsible for the decline in the cutout this week, but the retail primals were also a little lower. Towards the end of the week, ham prices began to stabilize, but didn’t show much inclination to advance. The bellies just seem to get weaker by the day. USDA released the results of their cold storage survey this week and it showed that the amount of bellies in cold storage as of the end of February increased 1.4% from the January number. Currently, bellies in cold storage are up almost 42% YOY. I think that goes a long way to explaining why belly prices haven’t been able to get any traction this year. Hams in cold storage increased 8.3% from the end of January to the end of February and that happened while prices were generally increasing. However, total ham inventories are 35% below the five-year average, so it seems like inventories are not playing a big role in the recent price decline on hams. I suspect that the ham weakness is a result of processors winding down their Easter ham production and thus just needing less product around them as a result. I don’t foresee a lot more downside risk in either ham or belly pricing, but I feel more confident about the hams showing gains before the bellies do. The attached price chart on the pork cutout is interesting. We spent most of Jan and Feb with the cutout stuck at $80 and then for 4 weeks from mid-Feb to mid-March, the cutout traded right around $85. Now it is back down near $80. The forecast has the cutout steadily rising from here, but it has been a very long time since we’ve seen that kind of price pattern in this market. Each week, I seem to be lowering forecasts again and again because the cash market has under-performed. I wouldn’t be terribly surprised if it under-performs the forecast again in April and May. The combined margin chart continues to look dismal. After a brief rise, the combined margin is now tracking lower again and may be on its way to taking out the all-time low set just a few weeks ago. I see two potential bright spots that could turn this market around. The first is that spring is just around the corner and that could spur demand for grilling items like loins and smoker items like butts. The second is that weekly kills are likely to slowly shrink from this point forward. Perhaps with the help of both of those things working in tandem, the cutout can start to track higher like the forecast suggests. This week’s kill registered 2.46 million head, down from 2.49 million the week before. However, it looks like packers are scheduling a bigger Saturday kill next week than what we saw this week and that has the potential to take next week’s kill back over 2.5 million head. The attached chart indicates that, just like last quarter, the industry continues to over-kill USDA’s estimate of the pig crop. By now it is readily apparent that there have been more hogs on the ground than expected for a long time. There’s not much doubt that has contributed to the market’s woes so far in 2023. Next Thursday USDA will release another Hogs & Pigs report and I expect it will show that the breeding herd is up slightly YOY, but down slightly from what was reported last quarter. I’m calling the Dec/Feb pig crop up 1.8% and those are the hogs that will be slaughtered this summer. So yes, I expect this summer’s hog supply to be larger than last year (maybe a lot larger if these over-kills continue) and it is pretty clear that demand is way, way below last year’s level. The attached scatter diagram for March shows just how weak pork demand is currently. Only the 08/09 time period in the wake of the financial crisis saw softer demand. I can understand why futures traders finally took the summer futures down from over $100 to the low $90 area. Hog producers continue to lose money hand over fist, with this week’s margin estimated at -$52/head. Corn prices have firmed up a little lately, perhaps indicating that high production costs are going to be a continuing feature in this market over the next few months. I guess the best thing I can say about the hog and pork complex right now is that generally, it is always darkest right before the dawn. Perhaps seasonally smaller kills and spring grilling demand will bring the new dawn that this market so badly needs. There is reason to have hope, but not much reason to have confidence.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}