Pork Wrap March 22

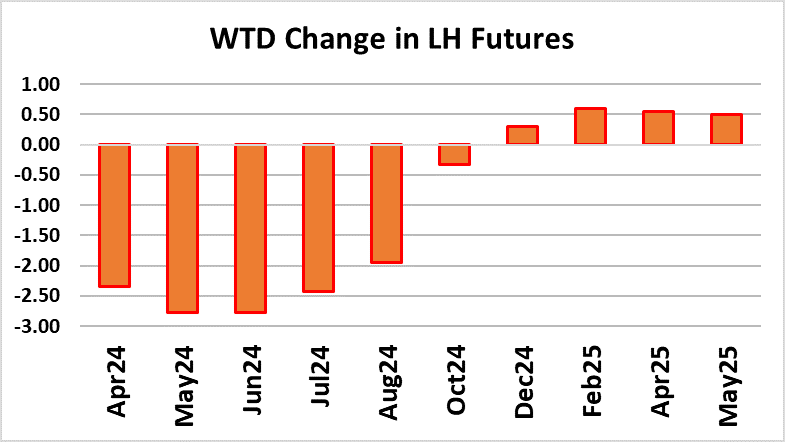

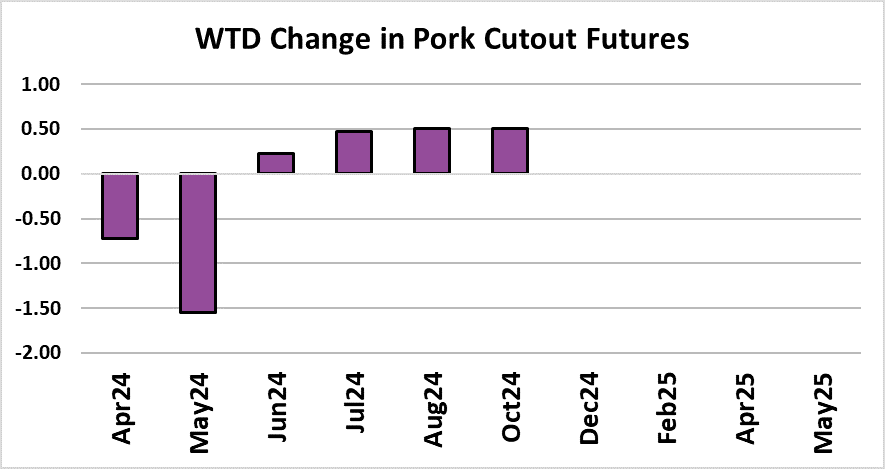

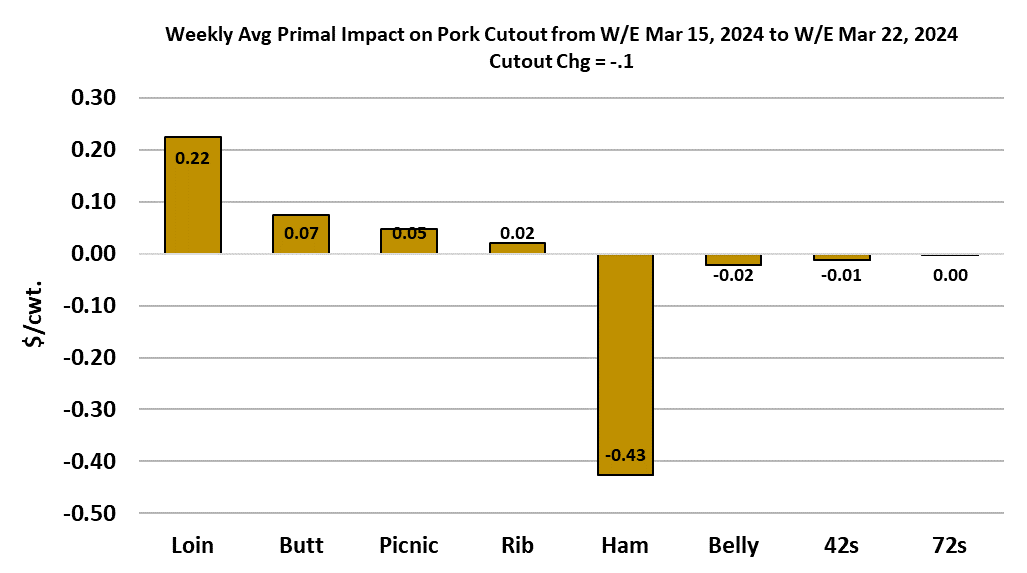

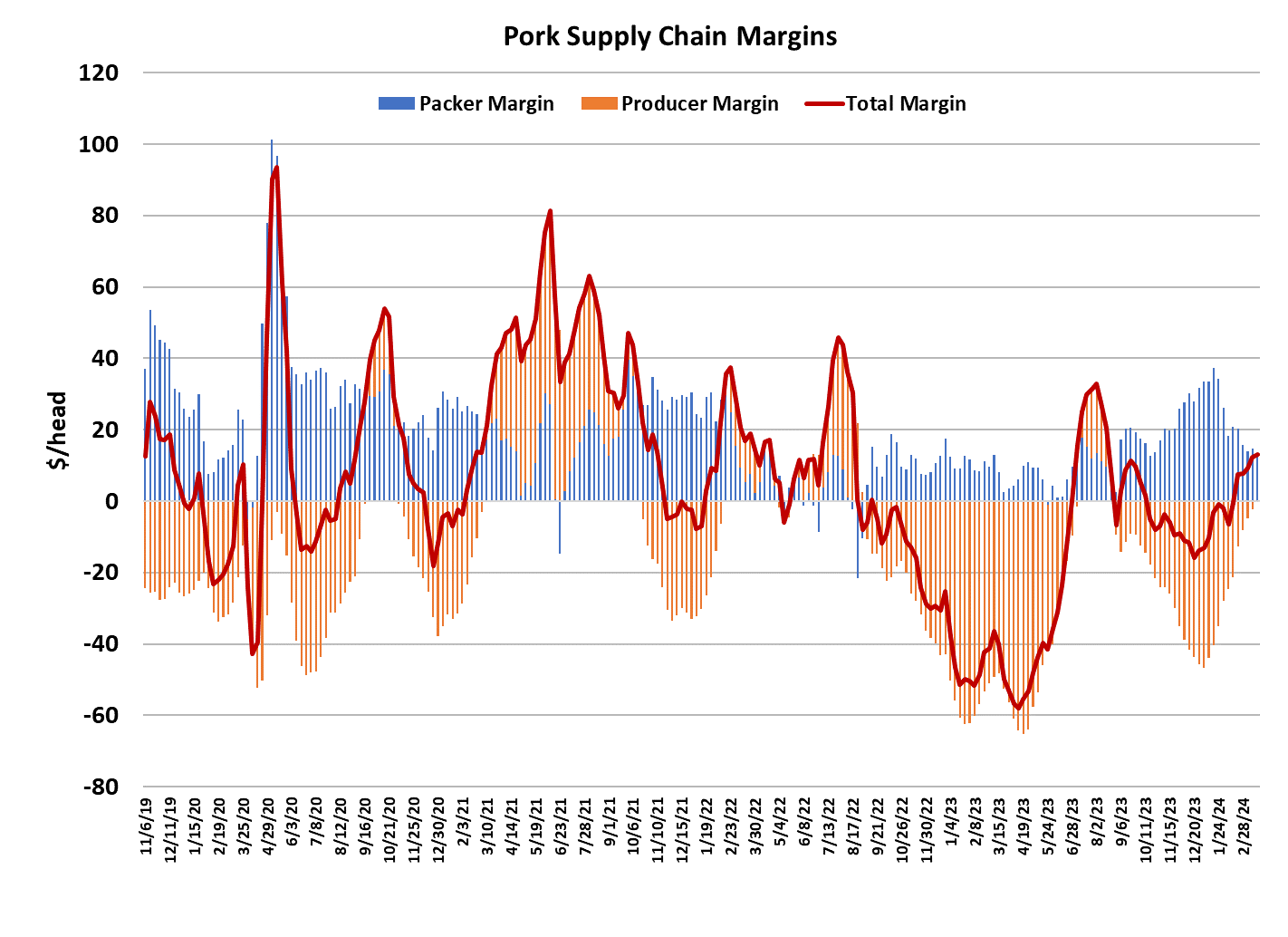

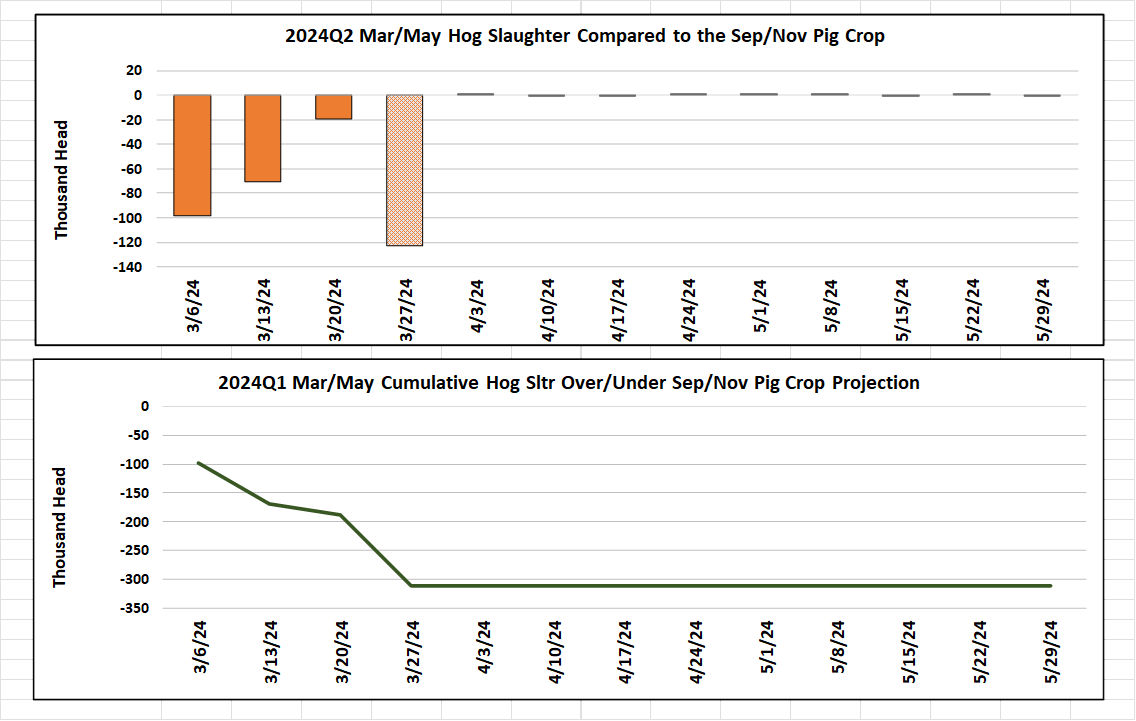

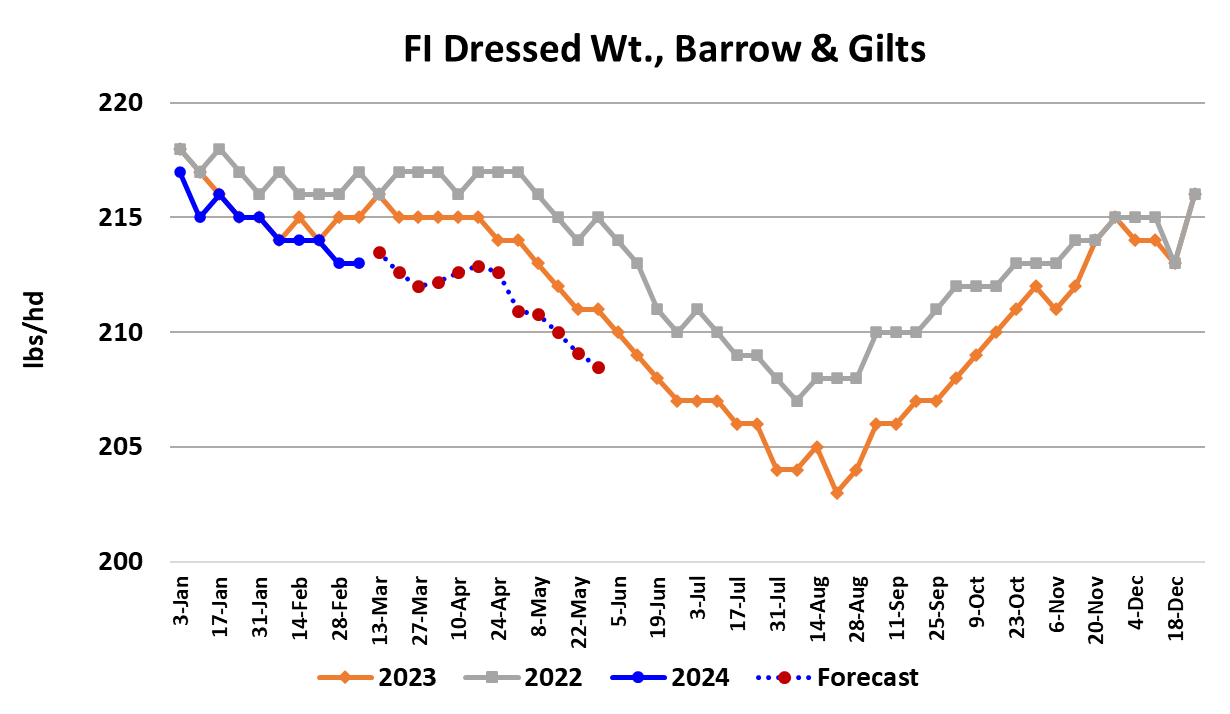

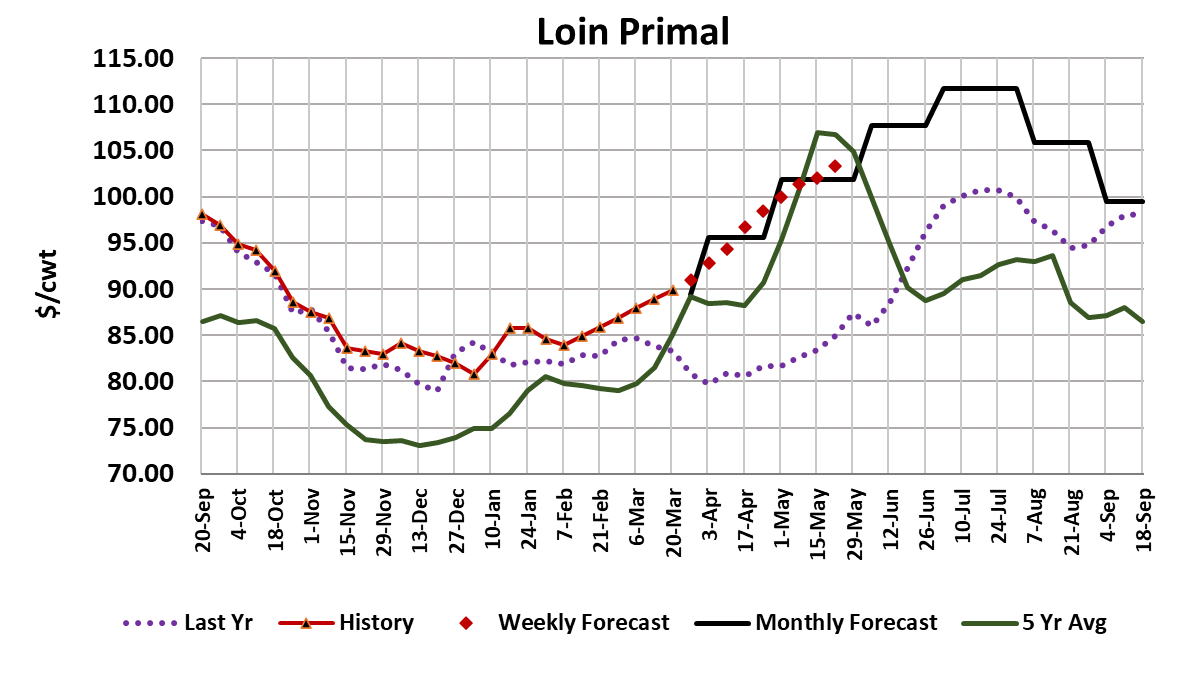

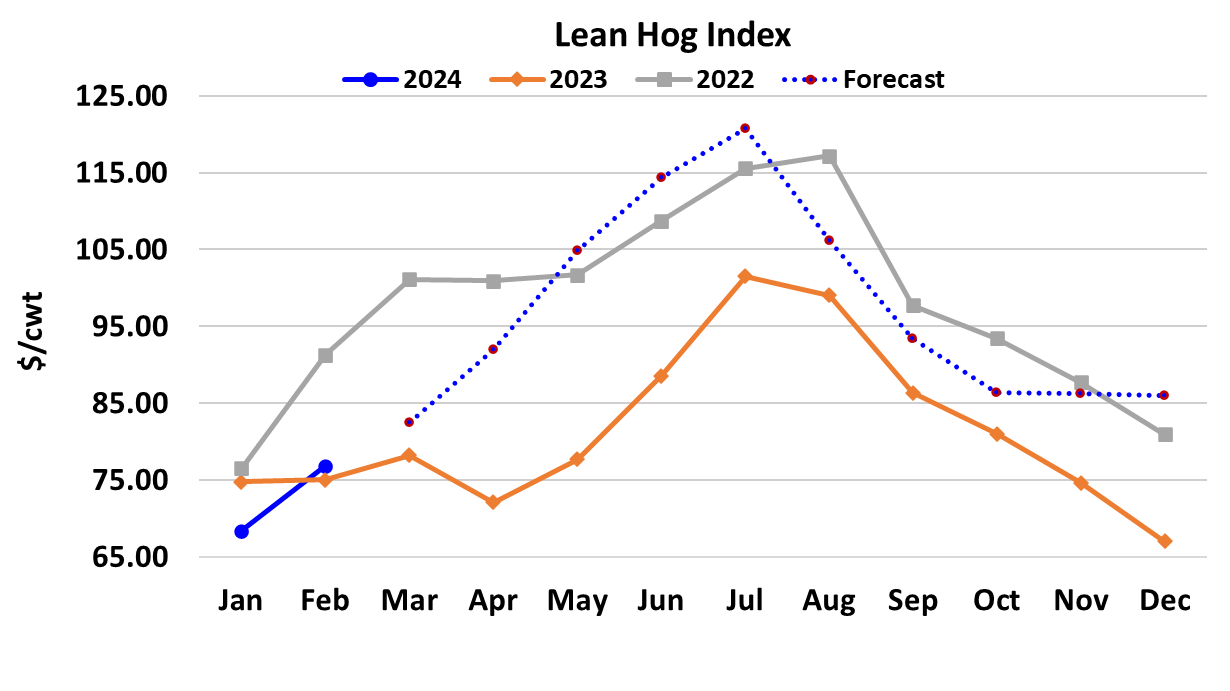

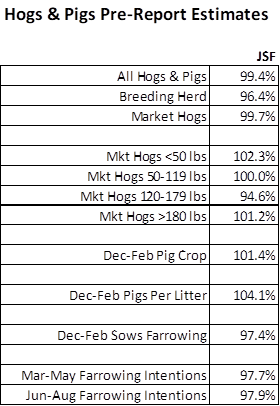

The pork cutout struggled a little this week, averaging $92.83, $0.10/cwt. lower than the week before. As expected, the cutout’s problem was caused by further deterioration in the value of the ham primal. Bellies were nearly unchanged on the week. The good news is that the retail items, and in particular the loins, are still working higher and demand in that sector seems to be solid. Demand for bellies and hams is a little more iffy, but in a little over a week the market will be on the other side of Easter and that should result in better interest for both bellies and hams. While the cutout was going nowhere this week, the negotiated hog market continued higher with the WCB price adding $1.87/cwt. on a weekly average basis, moving slightly over the $80 mark for the first time since the end of last summer. The best news of the week went to hog producers, who saw their margins move into positive territory after 29 straight weeks of losses. I calculate hog margins at about $1/head north of the zero line and expect that they will continue to work higher in coming weeks. While hog margins were moving higher, packer margins headed lower, now near $12/head, down almost $4 from the week before. The combined packer+producer margin was a little higher this week, maintaining the uptrend that has been in place since the first of the year. Last year at this time, the combined margin was near -$50/head and this week it averaged +13/head. That illustrates how much better off the industry is this spring compared to last. To be sure, some of the gain in the combined margin has come from declining corn prices, but it has also been helped from the revenue side by better pork demand this spring. To have producers in the black before April even arrives is a major accomplishment. There is more good news on the supply side. For the third week in a row, the industry under-killed USDA’s Sep/Nov pig crop estimate. In the first two week’s of the quarter, the underkill was helped along by mechanical problems at one of the very largest packing plants, but this week’s underkill appears to be organic. Next week should also see a significant under-kill due to sharply reduced slaughter on Good Friday and the following Saturday. It will be interesting to see if that slowdown is enough to stop the rise in negotiated hog prices. I suspect not. Easter normally marks a turning point for the hog and pork complex as it moves from the cold weather, big kills and low prices to warmer weather, smaller kills and higher prices. Given that Easter can fall anywhere from March 22 to April 25, the fact that we have Easter on March 31 this year qualifies it as an “early Easter”. Theoretically, that allows more runway for the post-Easter ramp-up in prices. This week’s kill was estimated at 2.53 million head, up about 70k from last week’s slightly disrupted slaughter. Next week’s harvest is projected to be 2.42 million head and if the recent trend of not over-killing the pig crop remains intact, we shouldn’t see another 2.5 million head kill until late August. The Sep/Nov pig crop that is fueling the current quarter’s kill was estimated to be down a tiny fraction (0.2%) from the prior year, so if the pig crop is correct then kills this spring are not likely to be much larger than last year. Carcass weights are running two pounds below last year currently, so if that continues for a couple of months, we could have actual pork production a little lower than last year. With pork exports likely to run a few percentage points better than last year, that means that pork availability between now and Memorial Day could actually be a bit snugger than last summer. I’ve already noted that pork demand is definitely tracking stronger than last year, so if that continues as well, it would make sense to expect price levels to be considerably higher than what we saw last year. I wouldn’t be surprised to see the cutout top $100 by the end of April. Futures traders seem to be losing their patience with the hog market however, as the Apr contract finished on Friday at $84.57, only about a dollar over where the LHI is going to print on Monday. There are now three weeks until expiration and the recent lack of upward movement in the cutout has forced me to scale back the forecast, but I still think that we will see enough improvement in both ham and belly prices over the next few weeks to get the cutout into the high $90s for expiration and that means the LHI could be approaching $90 at expiration. If it works out that way, then the May contract, which finished at $90.40 on Friday, is definitely too cheap. Of course, there is always the risk that one of those random air pockets in demand could develop and wreck the forecast completely. Next Thursday, USDA will provide another Hogs & Pigs report and I expect it to show the March 1 breeding herd down 3.6% YOY. However, I’m looking for another very strong print on pigs per litter (+4.1% YOY) and even though I’ve got the Dec/Feb farrowings down 2.6%, the large increase in pigs per litter leads to a Dec/Feb pig crop that is 1.4% bigger than last year. Those are hogs that will be killed in the upcoming Jun/Aug quarter. However, if the spring trends of lower weights, better exports and better domestic demand continue into summer, the industry could easily see prices stronger than last year even if the number of hogs going to slaughter is a little higher YOY. Just for reference, last year the cutout topped at $115 in mid-July. This year I think it could make a run at $125, probably also in July. Time will tell. Next week, look for better performance out of the cutout as participants start to gear up for a post-Easter push. The kill will be reduced and that could generate some temporary tightness in availability in the first few days following Easter.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}