Pork Wrap March 18

This was a week for treading water in the hog and pork complex. There

was very little overall change in the cash market variables. The

negotiated market was $1.08 higher in the WCB and $2.48 higher in the

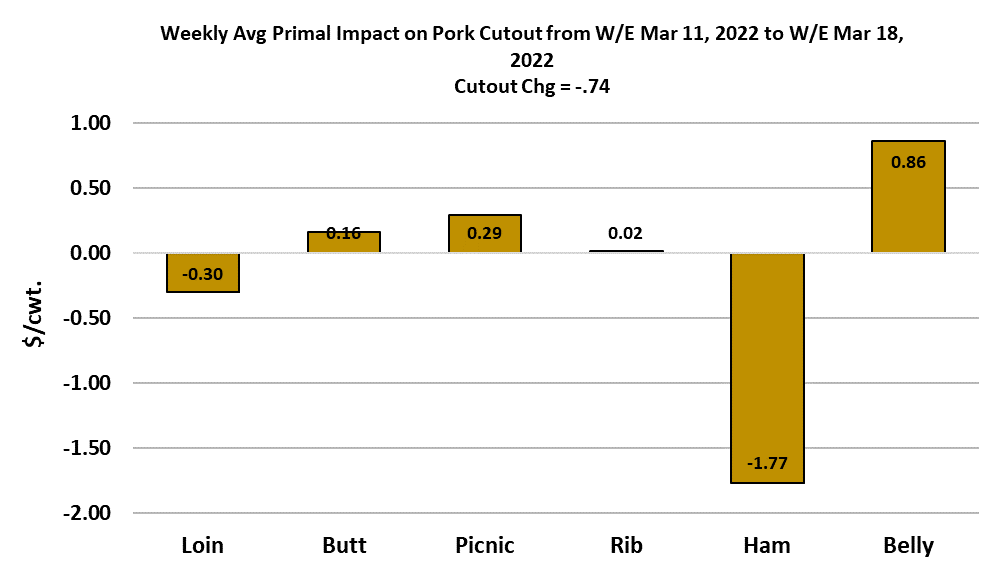

NDD market. The LHI gained a paltry $0.80 and the cutout lost $0.74.

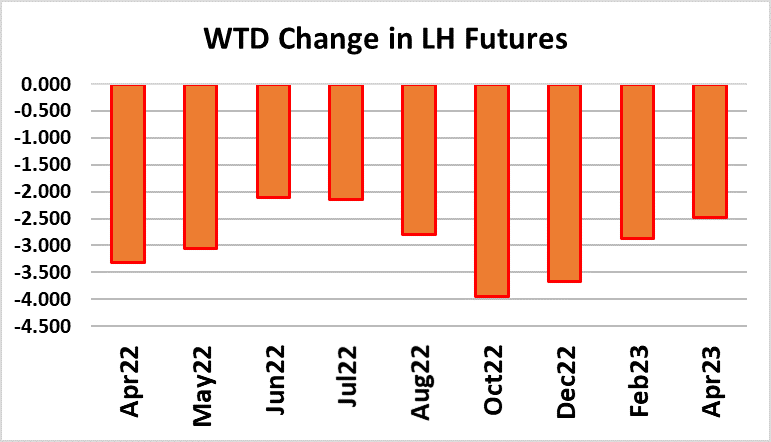

The one thing that didn’t tread water was the futures, where the nearby

Apr contract shed almost $3.50 to finish the week below $100 for the first

time since early February. Speculative traders are apparently growing

frustrated with a market that has no discernable direction and perhaps

are opting to look for greener pastures elsewhere. That leaves less

buying interest to offset commercial hedge selling and thus the futures

move lower. The pullback brought the Apr futures closer in line with my

fundamental price forecast, but my guess is that the futures will have at

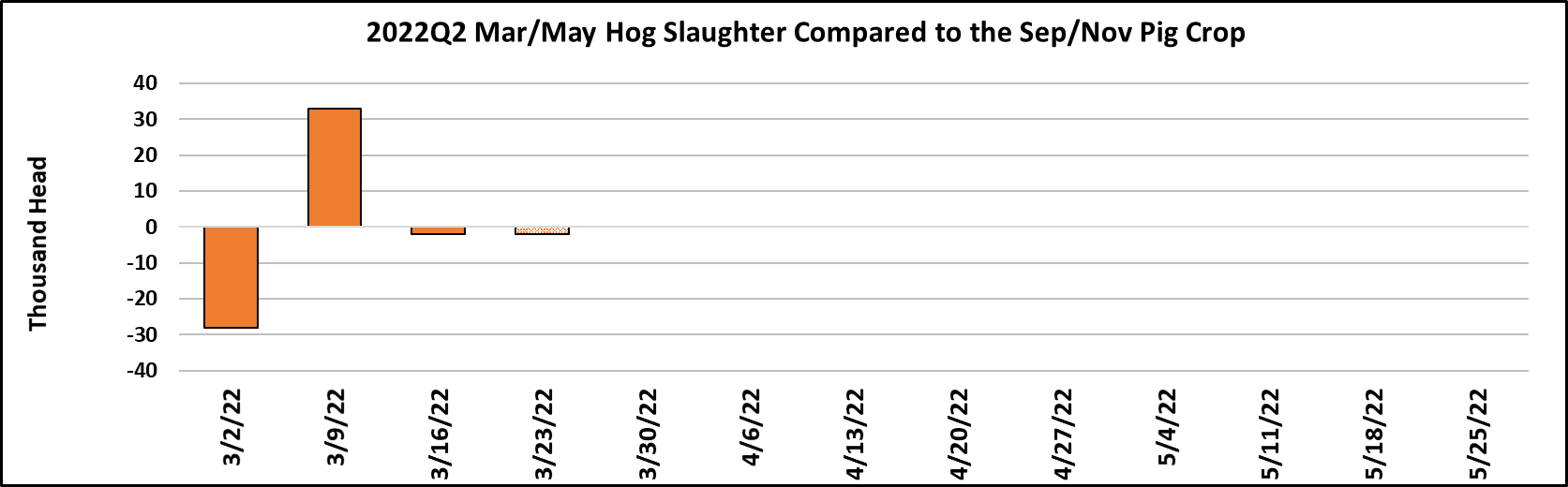

least one or two more runs higher before expiration. Slaughter this

week was estimated at 2.44 million head, which was almost dead-on

with what the Sep/Nov pig crop projected.

Three weeks into this quarter and cumulative slaughter has been very

close to what USDA’s survey suggested, helping to inspire some

confidence about the production forecast for the next couple of months.

We should see 2-3 more weeks of kills above 2.4 million head per week

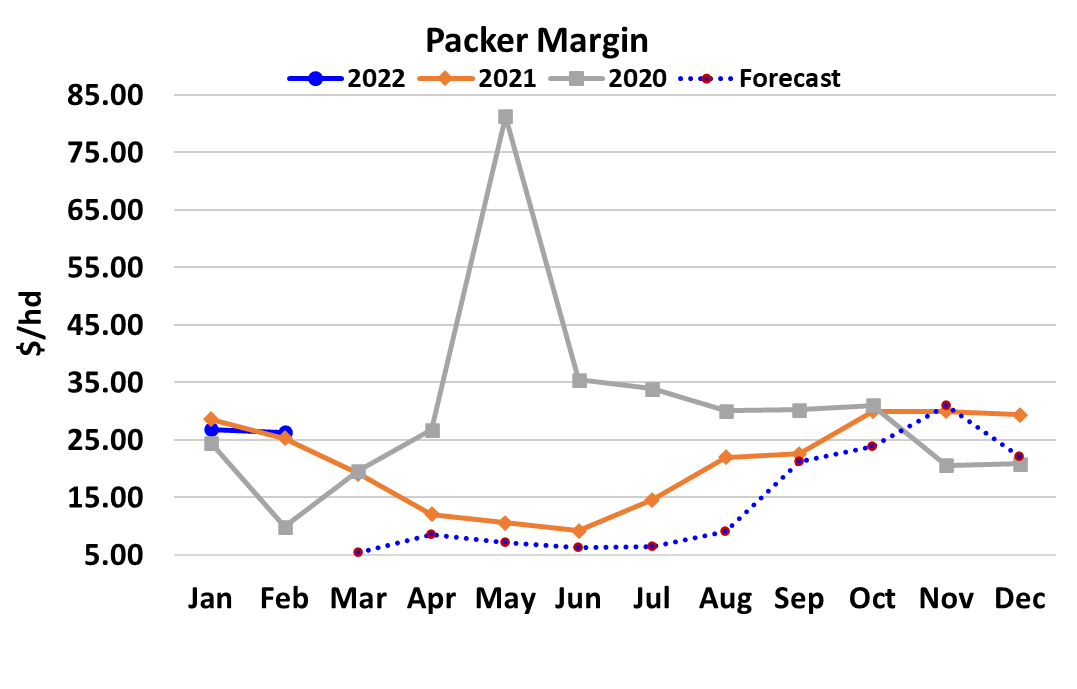

and then they will take another step lower. Packer margins however,

might be the fly in the ointment for kills over the next few weeks. I

calculate this week’s margin at $5.90/head, which is the smallest since

late June of last year. Further, if my cutout forecast is close to correct,

then margins could very well print in the red next week. That might

prompt packers to do a little more maintenance on their plants in order to

slow production and thus hopefully raise the cutout to a level that will

cover the increasing cost of hogs. On the other hand, packers have

worked hard to fully staff their plants post covid and might be reluctant to

schedule downtime that would idle new hires. Packers have already

trimmed the Saturday kill back substantially, with this Saturday coming in

at only 58k, compared to last March when Saturday kills averaged over

110k. There are just not enough hogs to support kills of that size.

It makes me wonder if this might encourage packers to move further into

the hog production sector. They added a lot of new capacity a few years

back and now producers aren’t cooperating by keeping the hog supply

large enough to efficiently utilize all of that capacity. Packers may

decide that the only way to guarantee that they can run their plants at

high capacity utilization is to raise more of the hogs themselves. Of

course, when a packer integrates back into the production segment, he

takes on the producer margin, which is pretty unpredictable and with

corn prices near all-time highs, it could become a bigger drain on

finances than simply running the plant below capacity. However, as of

this moment, producers are making more per head than packers, which

is pretty unusual for this time of year. I have producer margins this week

at almost $11/head. Barrow and gilt carcass weights seem to have

plateaued around 216 pounds, and that is pretty normal for this time of

year. The DTDS weights don’t suggest any problems in the hog pipeline,

but they also don’t suggest that packers are pulling excessively hard on the available supply.

There is still talk circulating about higher disease prevalence this year that seems to be centered in the WCB region. High negotiated prices coming out of that region seem to confirm that there is unexpected tightness there, but overall kills are lining up closely with pig crop estimates, so that

doesn’t seem to support huge disease losses at a national level. The

current demand cycle seems to be leveling, using the combined

margin as a guide. It has been trending lower since mid-February and

moved sideways this week. It could be carving out a bottom, or it

could be just stalled for a bit and will resume its downtrend next week.

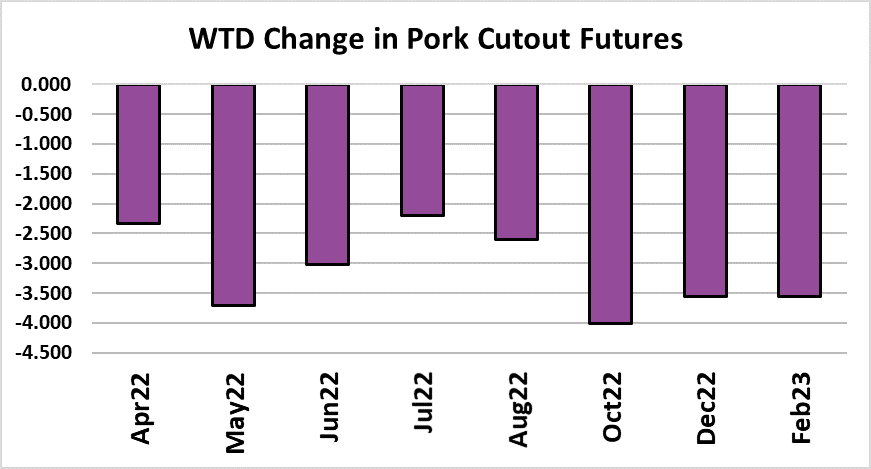

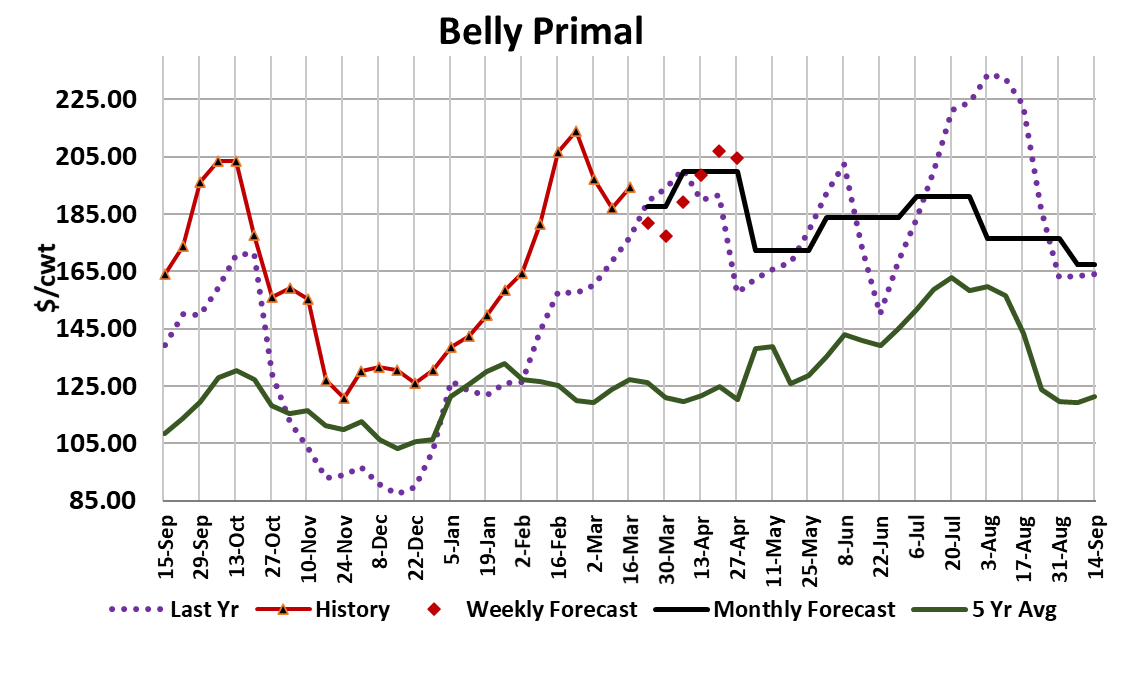

The cutout has not softened as quickly as I had originally imagined.

Hams are weakening now and may stay that way for another couple of

weeks, but the bellies have been pretty resilient after the big drop that

shaved about $25/cwt off the primal a few weeks back. I had thought

that perhaps they held more downside risk, but the primal actually

moved higher this week.

It’s not unusual for a pullback in the bellies to be interrupted by a week

or two of strength, so I’m not yet ready to call the bellies higher. I

have, however, moved my expectation for the bottom upward in recent

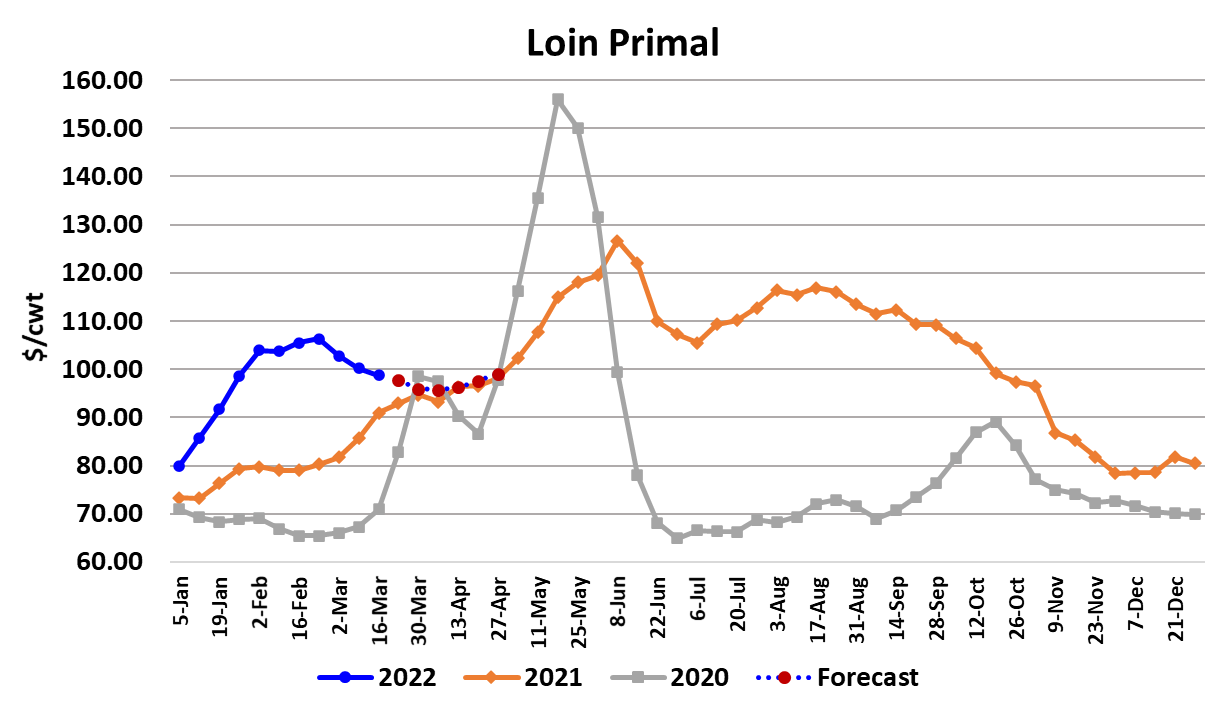

forecast revisions. Loins are another item that have been softening

lately, but soon retailers will want to run those more frequently to

capture some grilling demand and thus I don’t think they hold a lot

more downside risk. Butts and picnics are risk higher as the weather

warms. The sow market broke the $90 mark this week and is actually

running a bit above last year’s exceptional pricing. If consumers are

trading down as inflation rages, then we might expect the sow market

to perform very well this spring and summer. Back in April of 2014

when disease problems were causing significant supply problems, sow

prices actually breached $100 and that is the highest they have ever

been. Right now the cutout has some primals rising and some falling,

so the cutout itself has been drifting lower only very slowly.

Demand could continue to soften, but smaller kills in the weeks and

months ahead may provide enough support to overcome softer

demand and thus move the cutout upward. Futures traders are

currently valuing the June pork cutout futures near $122, so that

suggests that most believe the seasonal decline in pork production will

be very supportive to pork prices this spring and summer. My

forecasts for summer hogs and pork are well below what the futures

are currently implying, but given the recent developments in the

relationship of cash hogs to the cutout, I may need to reduce my

packer margin forecast this summer. Right now, I’m expecting $6-7/

head positive margins, but if those margins actually turn out to be

negative, then it would be much easier to get cash hogs or the cutout

to a level more consistent with the futures. Next week, keep an eye on

the bellies because a price drop there would greatly increase the

bearish sentiment that has been creeping into the market lately.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}