Pork Wrap March 17

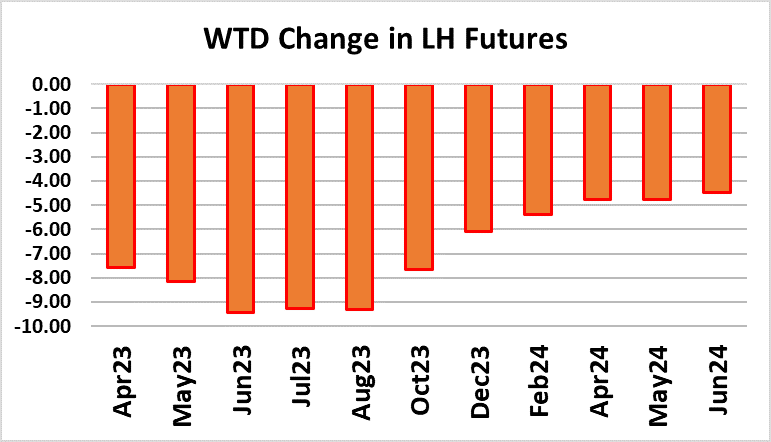

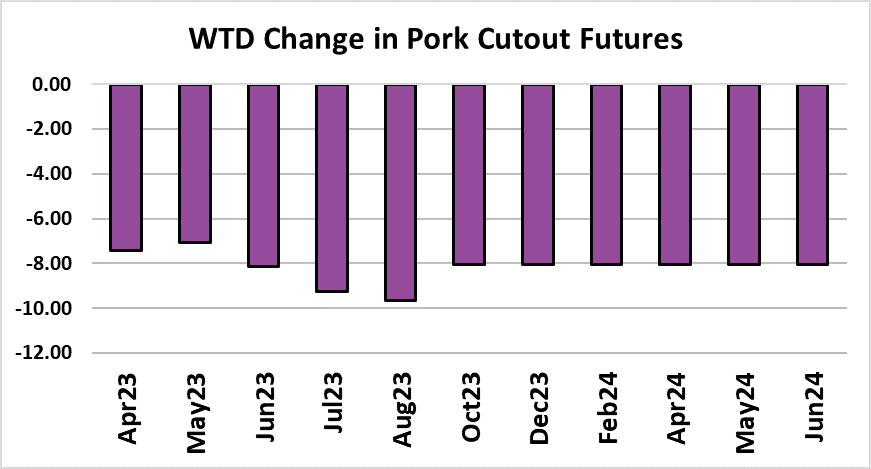

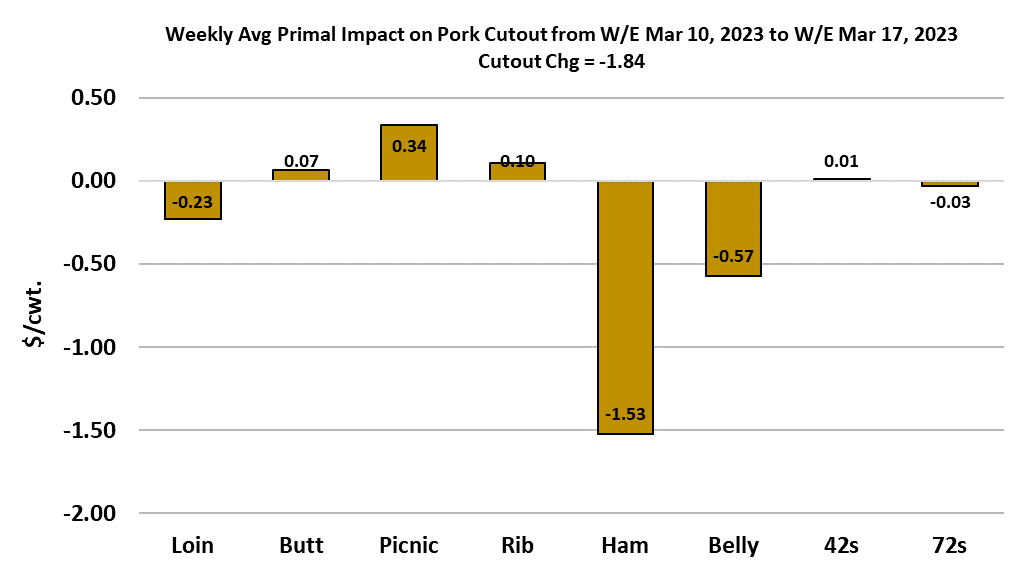

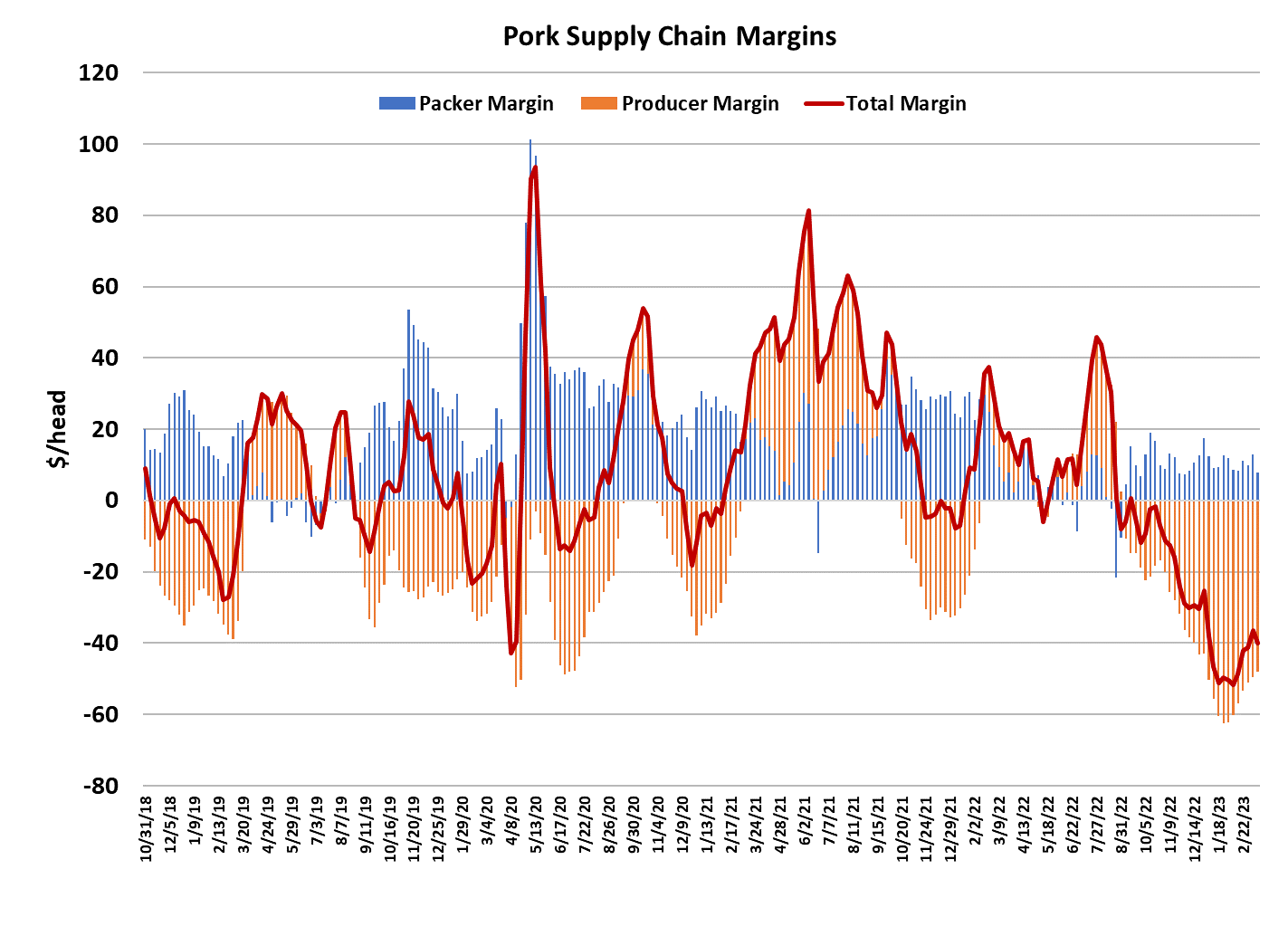

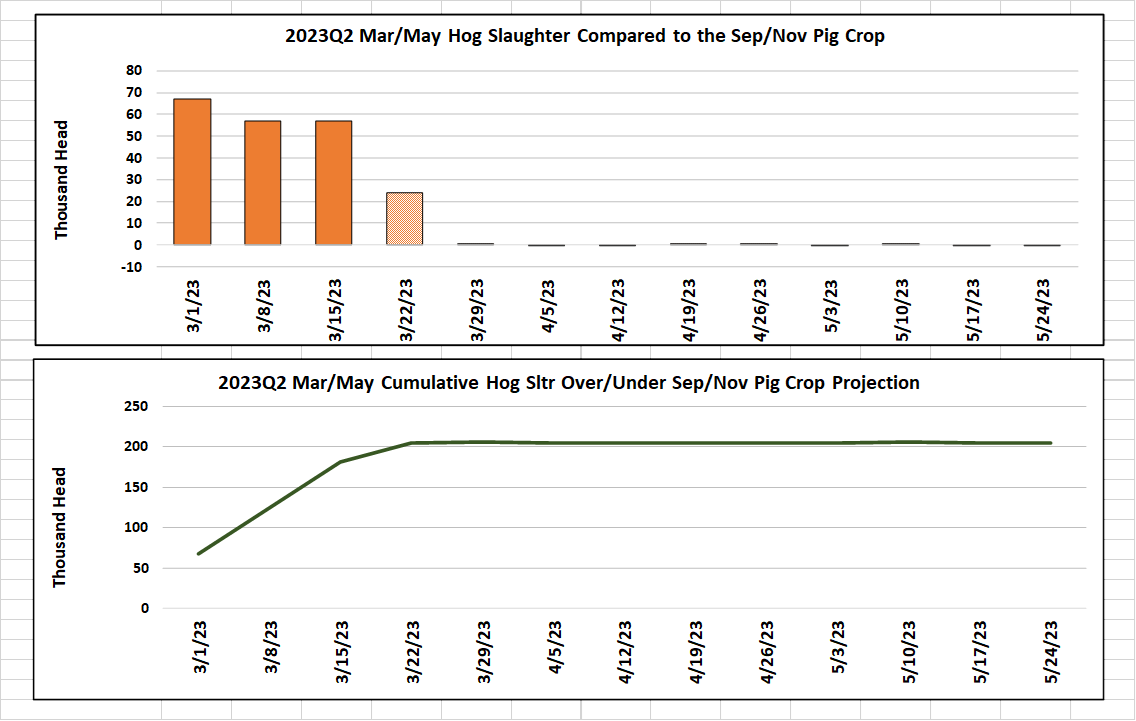

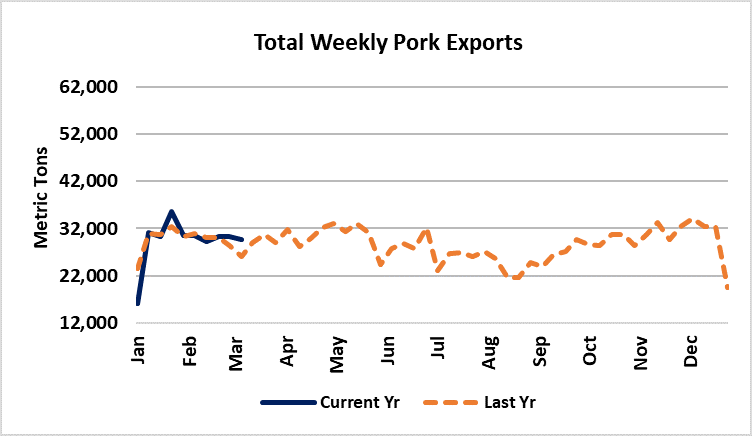

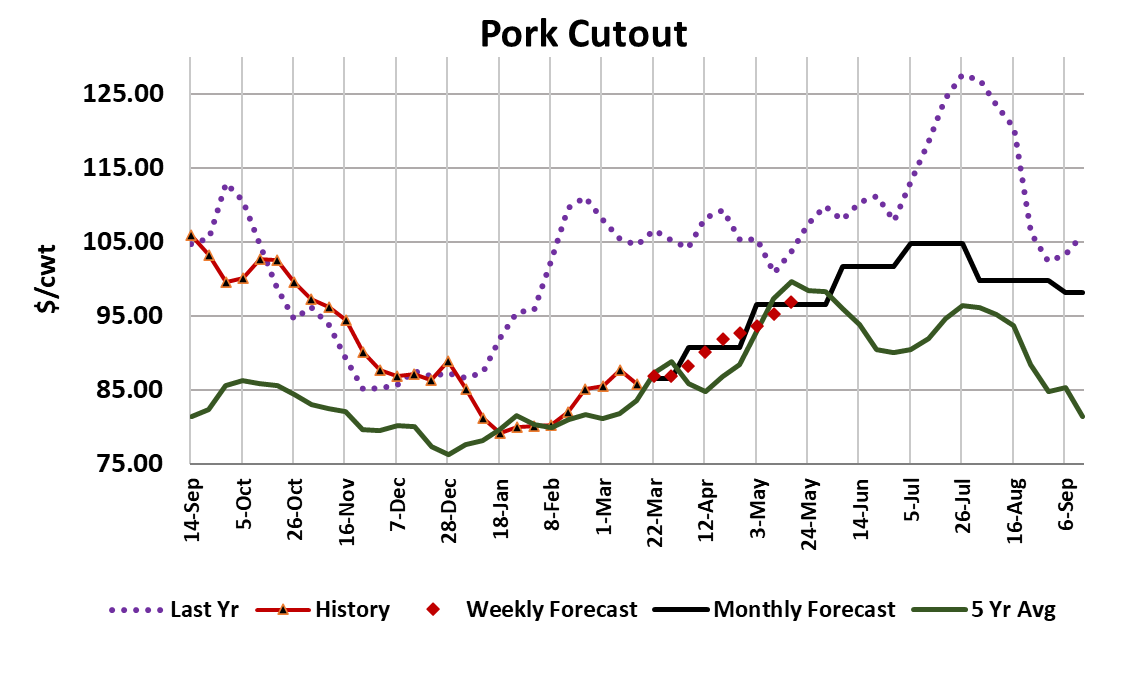

The dam finally broke in Lean Hog futures this week, sending prices cascading lower and forcing market participants to come to grips with the fact that pricing in the summer of 2023 isn’t going to be anywhere near what they saw in 2022. Coming into the week, the Jun contact was priced near $103/cwt and by the end of the week that had been reduced to near $93. At one point on Friday, it traded below $90 before recovering. Traders were probably already a bit nervous about what was going on in the broader financial markets where banks were failing and equity markets were tanking, but the real trigger that cratered the market was a rapid softening of the cutout. That softening first became evident in the noon cutout print on Wednesday, although the hams had been flashing warning signs a lot earlier than that. On Tuesday afternoon, the cutout had printed over $88 and by Friday afternoon it was under $81. That was like a gut punch to all of those bulls that have been expecting summer hog prices over $100/cwt. Suddenly, it became clear that $100 summer hogs might be a bridge too far. Once it got started, the selling took on a life of its own and pushed all of the contracts below my estimate of fair value. If we just look at the cutout on a weekly average basis, it was only down $1.84/cwt., but Friday-to-Friday it was down almost $7/cwt. The attached chart shows that it was the bellies and hams that were largely responsible for the cutout’s weakness—hams more so than bellies. With Easter only about three weeks away, processors have run out of time to procure green hams and get them processed and in the stores in time for the holiday. Post Easter, ham processing shifts towards more lunch meat production and less whole ham items, so I think that hams will regain strength at some point, but it might take a few weeks. Meanwhile, we already knew that bellies were struggling due to big cold storage stocks, so to see them go down in sympathy with the hams wasn’t a huge surprise. It is important to note that the retail items were largely unscathed this week, likely because more retailers are shifting toward pork feature in place of pricey beef this spring. How long the air pocket in demand for the processing items will last is uncertain, but in the near term I would expect futures traders to continue selling until they see evidence that ham and belly prices have stabilized. The downdraft in the cutout is going to take the LHI lower next week and if the cutout and negotiated markets stay where they finished up this week, then it looks like something close to $76.50 is already baked into the LHI. That would be down from the $80.01 the index printed today. At least part of the blame for this week’s big reset in the futures lies with traders who insisted on keeping the nearby futures $5-6 over a cash index that was barely moving. In the last two weeks, the LHI was moving upward by an average of $0.13 per day. It just didn’t have enough momentum to reach the lofty valuation that traders were keeping on the Apr contract. In the negotiated hog markets, the WCB price was unchanged on a weekly average basis and the NDD price was down $0.60/cwt. There isn’t much doubt that packers will be trying to pressure the negotiated markets lower next week in order to protect their margins, which are estimated at only $8/head this week. The may very well have some success because the data continue to suggest that there are way more hogs out there than expected. This week’s slaughter came in at 2.49 million head and, as the attached chart indicates, that was about 60k more than what the pig crop suggested. Three weeks into the March/May quarter and we already have over-killed the pig crop by close to 200,000 head. When we consider that the over-kill in the previous quarter was about 700,000 head, it isn’t surprising that processors are starting to say “no mas”. Consumers too. Even more concerning is that this week’s action reversed the combined margin, turning it lower just when it looked like we were in a new demand upcycle. That combined margin is at such a low level already that if this really is a new turn lower then record soft demand could be just around the corner. Of course, there are reasons to be hopeful. Spring and warmer weather are just around the corner and that could help improve demand, at least for the retail items. Also, beef prices remain very high compared to pork so we should see pork garner more ad space in coming weeks. Finally, even though it isn’t very apparent yet, the seasonal reduction in hog supplies should start to gain steam by the end of this month or in early April. In two weeks, USDA will give us the results of their most recent Hogs & Pigs survey and that should clarify the supply picture for the fall and early winter months. That report should also contains some rather large upward revisions to past pig crops. Producer margins this week were about $48/head in the red and that is the worst margin for this time of year in at least the past 16 years. Raising hogs is hard work and I’m sure many producers are asking themselves why they are doing this for such a dismal return. There should be some herd downsizing in the months to come. The weekly export numbers have been rather flat lately and close to last year. It doesn’t look like producers are going to get bailed out by exports this year. Corn futures have come down a good bit in the last month, but cash corn in Iowa is still running close to $6.50/bushel and cash soymeal in Iowa is higher than it was last year, so hog producers aren’t getting a lot of relief on their input costs. The only way out of this margin trap is to reduce production to the point where prices rise enough to cover the cost of production for those that remain in business. Brutal, yes, but that is the way that a free enterprise system works. Next week, watch those bellies and hams for any further price erosion and watch the negotiated markets for signs that packers are seeking price concessions to help offset what they have lost on the cutout recently.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}