Pork Wrap March 15

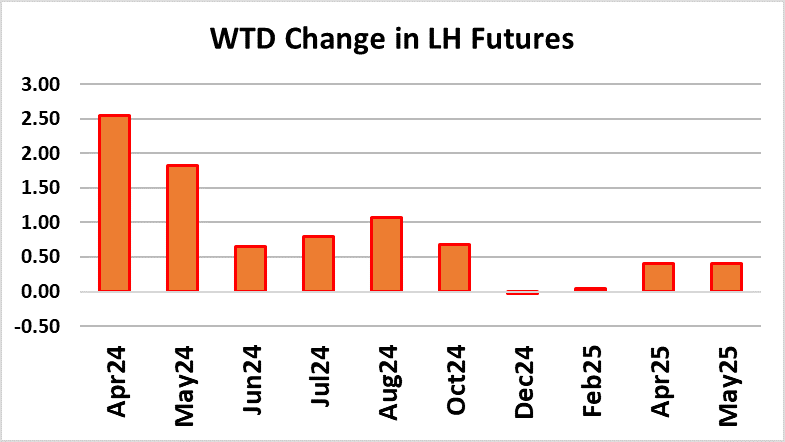

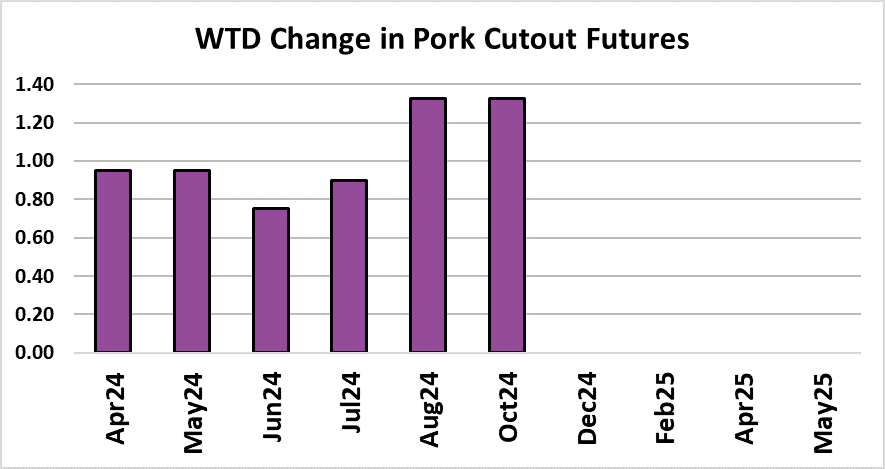

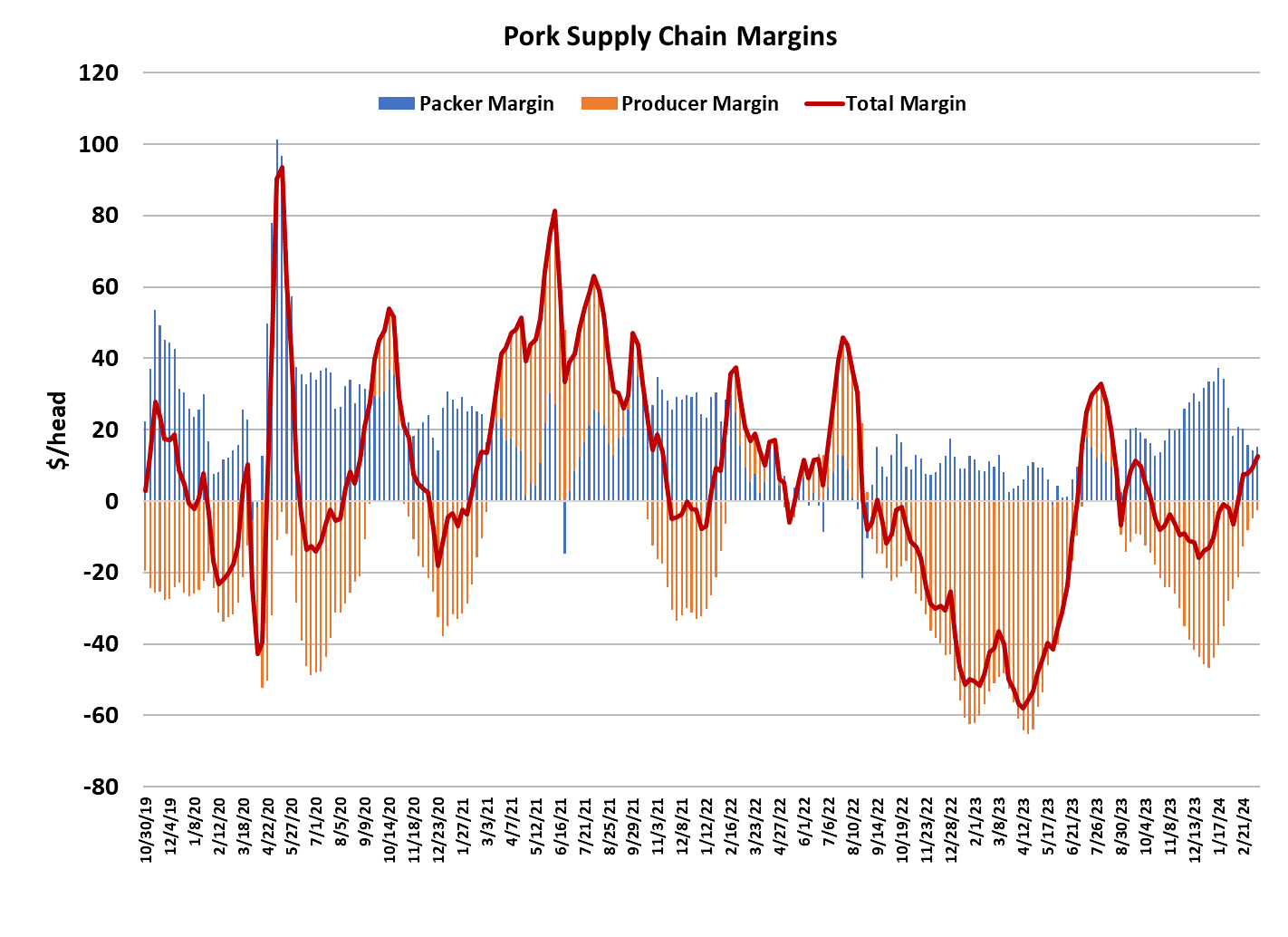

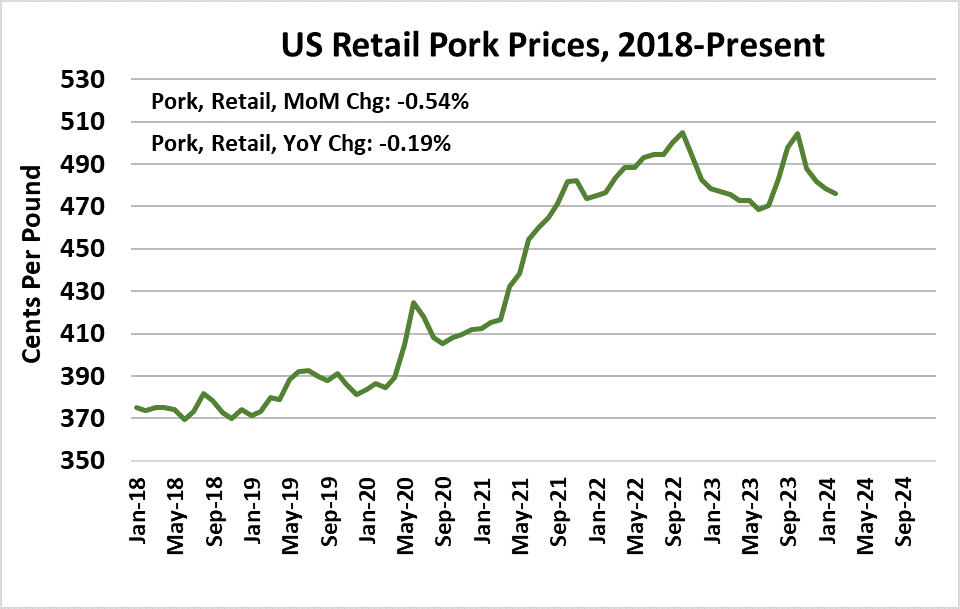

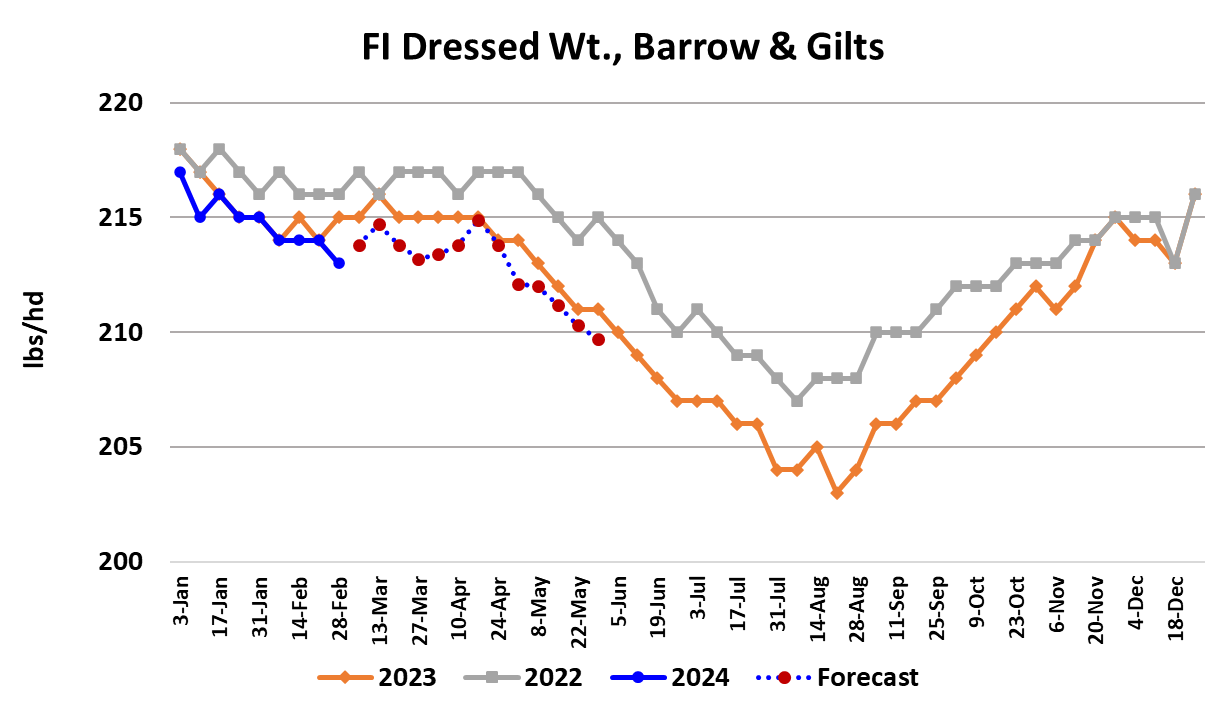

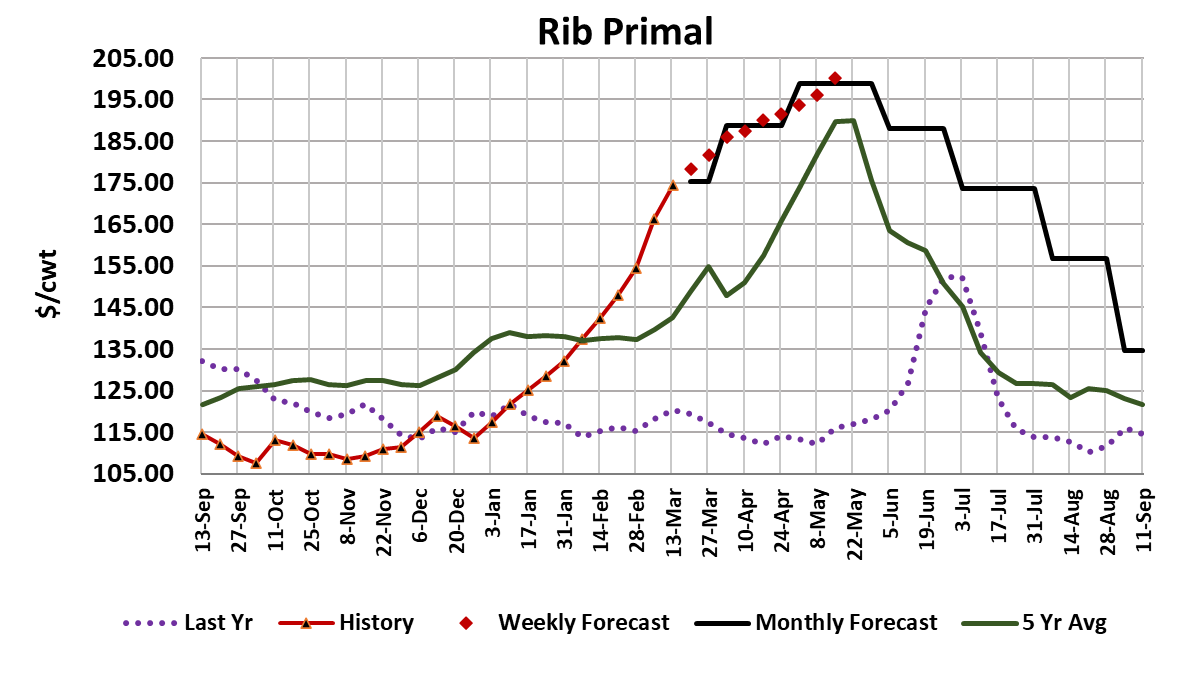

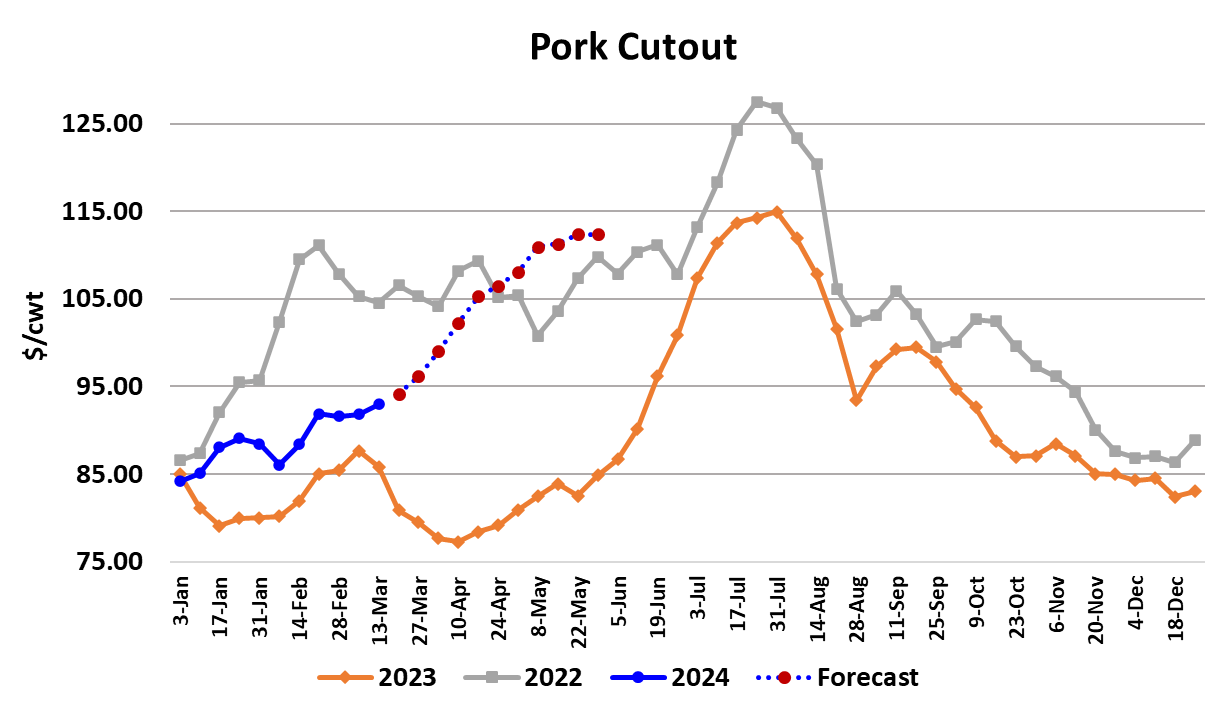

The pork cutout got back to its winning ways this week, advancing $1.13 on a weekly average basis to $92.93. The negotiated hog markets continued higher, with prices in the WCB region averaging $78.41, up $2.65 from the week before. This market is a forecaster’s dream. No need to worry about sharp changes in prices from week to week, just forecast everything to display a small, steady price increase. That said, there are some stark differences between the primals that we need to remain aware of. The retail items all advanced a small amount this week and ribs are simply on fire. If rib prices keep rising at this rate through June, it’s not hard to imagine the primal posting a top in the $220-230 range. I have to conclude that most of the increase in rib prices is due to demand, not supply, since pork production has averaged about 4.4% stronger than last year since the polar vortex in early January. Of course, cold storage stocks of ribs are down about 27 million pounds from last year’s level, so there is some modest contribution from the supply side. Ribs, along with bellies, are the most expensive parts of the carcass. Demand for both of these items is more inelastic than for the other parts of the carcass, which means that rather small changes in supply can result in large price changes. However, prices for ribs are soaring while belly prices remain subdued, so its not hard to conclude that rib demand must be really strong in comparison to belly demand right now. Rib demand is driven by both foodservice and retail accounts and there are a lot of BBQ foodservice establishments that hang their hat on the ribs, so its not something they can substitute away from when prices get high. Retail demand for ribs comes largely from home users that own a smoker. During the pandemic when consumers were forced to stay at home, smoker sales ballooned and so did the price of items like ribs and briskets which are smoker favorites. Maybe now that the pandemic has ended, and consumers have had a year or two to get all of their “revenge” travel done, they are starting to turn back to their old friend, the smoker. Whatever the cause, it doesn’t look like rib demand is going to let up until midsummer or later. The belly primal averaged $0.01/cwt. higher than last week, so it remains in a sideways pattern. The hams were the biggest drag on the cutout this week and may continue to weigh on the cutout for another week or two. Once we get past Easter, I’d look for ham demand to improve and that, combined with seasonally declining production, should help get ham prices back on an upward trajectory. The current forecast has the ham primal topping out this summer near $105, which would be a big improvement over this week’s $77 average. My expectation is for belly prices to also gain traction after Easter, but by that time the Apr futures will be only two weeks from expiration. With both ham and belly pricing on pause until after Easter, that likely would keep the cutout below $96 for a couple of more weeks, but once those two items start appreciating, the cutout could quickly move into the low $100s. By Memorial Day, I look for the cutout to be close to $112 on its way to a top in the low $120s sometime in July. If that sounds like a typical spring/summer hog market, it is. It is worth considering what might cause actual prices to deviate from the forecast. On the demand side, the most obvious thing that would wreck the forecast is if a demand air pocket develops. So far, there’s no sign of that, but those tend to come on quickly and with little warning, so we are not out of the woods yet on that one. On the supply side, I think the surprise might be smaller-than-expected hog supplies, which would push actual prices higher than the forecast. This week’s kill came in at 2.47 million, but it was obvious that at least one very large slaughter plant missed some shifts again this week and without that, the kill would likely be closer to the 2.52 million that I’m forecasting for next week. Because that large plant is located on the East Coast and primarily utilizes company-owned hogs, the missed shifts haven’t affected the spot markets in the Midwest. However, the hogs that would have been killed on those missed shifts haven’t gone away and its possible that the plant will run harder than normal in the next couple of weeks to clear them, putting a little more pork on the market. Or, they could sell them to another packer, which would lessen spot hog demand temporarily. In any case, I’d expect that situation to be sorted out fairly quickly. What could cause smaller-than-expected hog supplies this summer? Well, for starters, the Dec/Feb pig crop that will be reported later this month could be smaller than anticipated if productivity turns out to lower than the strong number I’ve dialed in. Another possibility is that USDA will finally stop under-estimating the pig crop. They have under-estimated it for so long that I think most people fade it higher, so it would be a surprise if they didn’t under-estimate this time around. Another way that we could end up with smaller-than-expected production is if the weather gets exceptionally hot this spring and summer, causing weights to plummet. Outside of the January polar vortex, the weather so far in 2024 has leaned heavily to the warm side. The way that negotiated hog prices have been steadily marching higher, and in most weeks outpacing the cutout, gives me the feeling that hog supplies in the Midwest are already starting to tighten even though the normal seasonal wouldn’t be expecting that for another month or so. Of all of these potential factors, it seems to me that the supply side, under-production scenarios are more likely than the demand air pocket scenario, so that makes me think there is more risk that the actuals exceed the forecast rather than fall short of it. This week’s retail price data showed February pork prices down about a half percent from March and very close to where they were last year at this time. Given that the cutout in February was about $8 higher than last year, this suggests that retail margins on pork are finally shrinking. That is benefiting the packing and producer segments, leading to a persistent uptrend in the combined margin. Next week, look for more of the same, small gains in the cutout and likely larger gains in negotiated hog prices. Hams have risk to the downside, while bellies should continue to tread water.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}