Pork Wrap March 12

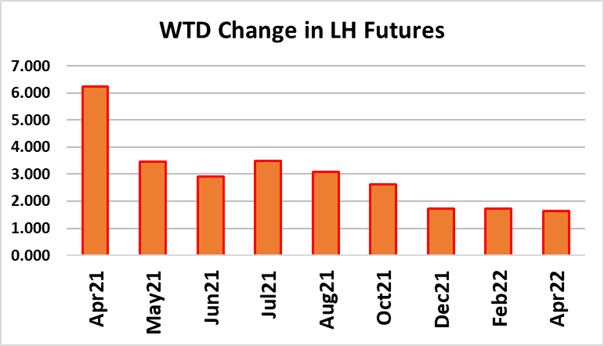

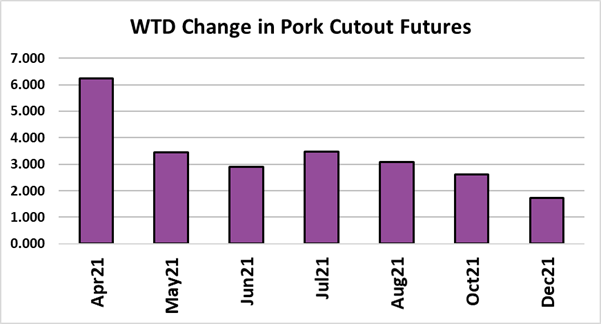

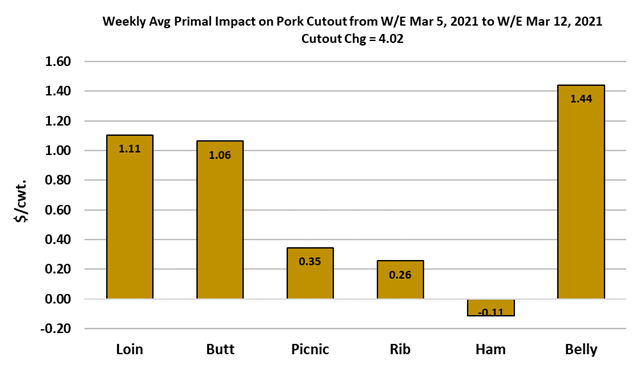

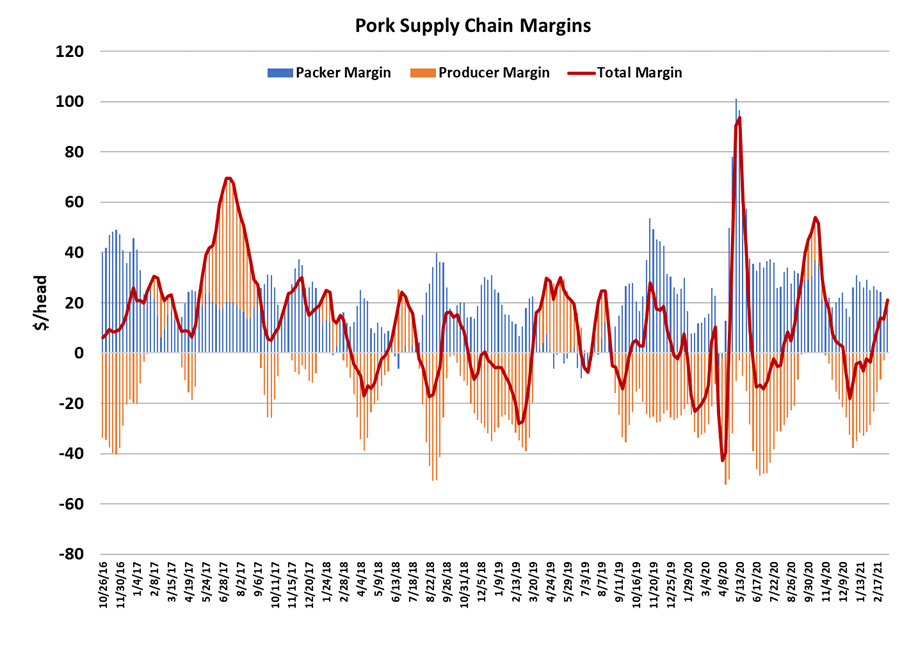

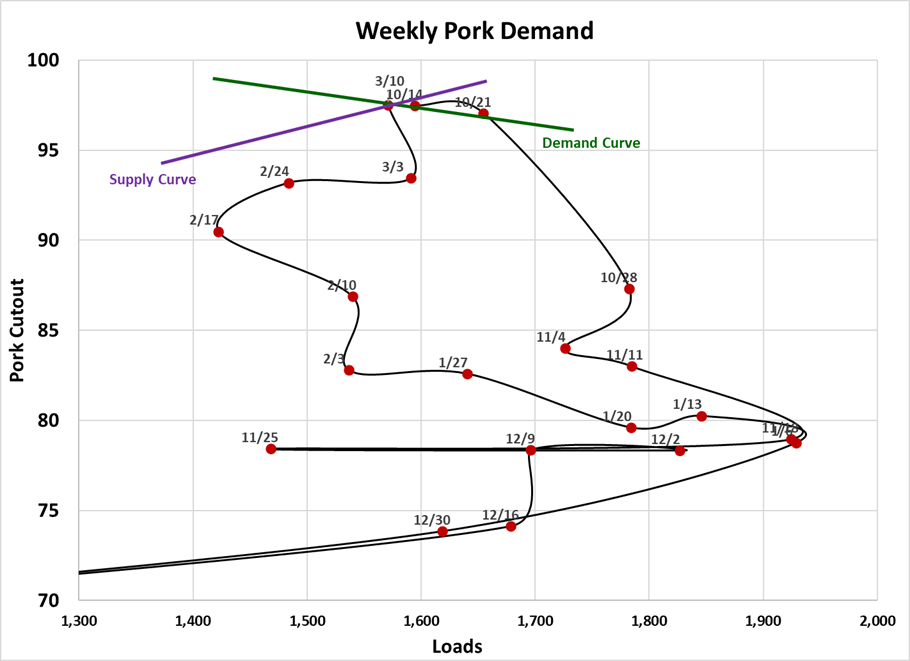

It was yet another week of increasing prices in the hog and pork complex. The cutout gained a little over $4 on a weekly average basis and the negotiated cash markets were up around $3.30. The nearby Apr futures responded by gaining over $6 Friday-to-Friday. The Apr cutout futures gained a similar amount. At one point this week, the cutout came within 31 cents of printing $100. It still looks to me like mostly a case of strong domestic demand driving this market, although there could be some modest tightness in the spot hog supply. On Monday, the negotiated price component of the LHI actually registered above the ¡°swine and pork market formula¡± component¡ªa very rare event indeed. Normally, the negotiated market runs about $10-15 discount. So, there is reason to believe that there is tightness in the producer-owned hog supply. Some of that tightness could be artificial as producers hold back hogs on purpose under the idea that they will be worth more several days down the road. Regardless, packers don¡¯t seem to be having too much trouble putting a sizable kill together. This week¡¯s slaughter totaled 2.58 million head, about 20k stronger than last week. It was also about 40k more than what the Sep/Nov pig crop implied. Packer margins this week were about $18/head, still very healthy and enough to incentivize packers to keep the kill solid. Packers also killed about 35,000 head more on Saturday this week than they did last week, which might be a sign that the tightness in the spot hog supply is loosening a bit. Barrow and gilt carcass weights are still stuck at 215 lbs for the third week in a row, but that is not out of line with historical averages. In fact, the DTDS weights are close to -1 currently, which suggests there is no problem with overweight hogs. So, when does this high price environment come to an end? Whenever pork buyers get tired of paying crazy high prices, would be my answer. We may be getting near that point now. The weekly demand scatter below shows pork demand at nearly the same level as it was when it peaked last October. That peak in the cutout was right around $100, same as this week. The difference between now and last October is that this time around we are moving into a tightening hog supply situation whereas last fall the market was experiencing an expanding hog supply situation. That might mean that once the cutout does start to come down, it will decline at a slower rate than it did last fall. We are still seeing very high belly and trimmings markets. Some of the retail cuts like loins and butts are also very high. When this happened last October, I had a suspicion that pork was leaking undetected into export markets but once the actual export data became available we could see that was not the case. I am reluctant to make that mistake again. Instead, I place the blame squarely on strong domestic demand for this rally. However, domestic demand runs in cycles which are largely driven by retailers switching feature proteins when one gets too high relative to the others. Pork certainly is higher than normal relative to beef right now and so I¡¯d expect the demand cycle to turn lower soon. The combined margin is now over $20/head and many of those cycles seem to top around $25/head, so that might also be pointing toward a downturn in demand relatively soon. USDA released the monthly trade data for January this week and it showed total pork exports 8.6% below last year¡¯s huge number. February is likely to see an even larger percentage decline. But, Q1 last year was exceptionally strong for exports, so I don¡¯t want to give the impression that export demand is soft. It is just having a hard time matching last year¡¯s stellar performance. Some of that might have to do with the well-publicized congestion at ports and lack of containers in the right place. There has been a lot of speculation lately about a resurgence of ASF in China, but no one seems to have reliable data to confirm that. Futures traders generally don¡¯t wait for hard data before casting their vote and the way they have bid up the deferred contracts makes it look like they believe the China is losing ground in its fight with ASF and will need to import more pork from the US in coming months. I¡¯m skeptical, but wouldn¡¯t want to rule that completely out. So far, the weekly export numbers haven¡¯t telegraphed an impending surge in exports to China. Besides, the Chinese are known to be value buyers and today¡¯s cutout levels can hardly be considered a value for the buyer. Bellies could be the first to break lower, but my guess is that once it starts it will be felt across all primals pretty quickly.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}