Pork Wrap March 11

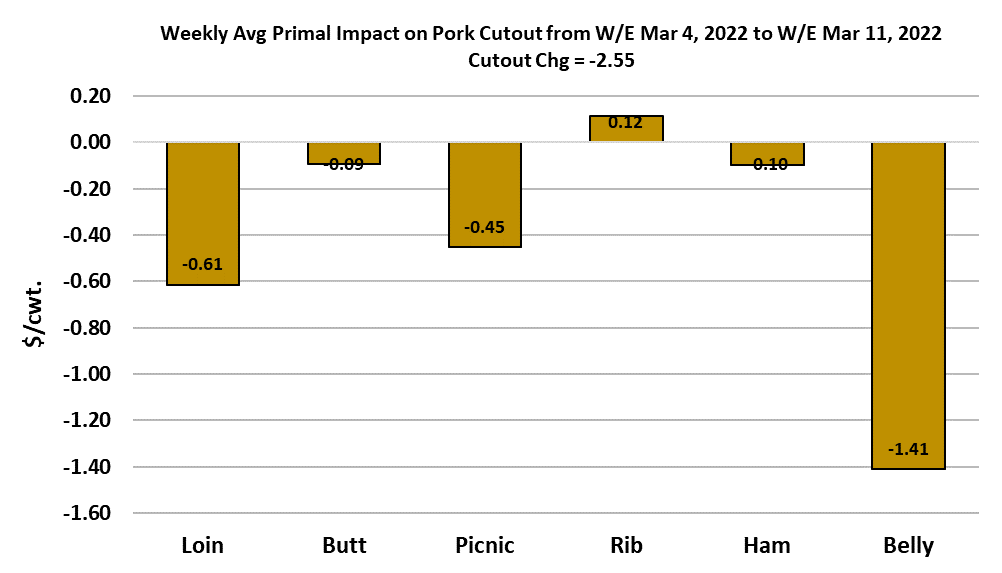

This was not a good week for pork packers. Hog prices increased

sharply, with WCB negotiated prices up $9.25 to average almost

$109/cwt and the NDD price was $8.24 higher. At the same time, the

cutout was softening, dropping about $2.55 from the week before.

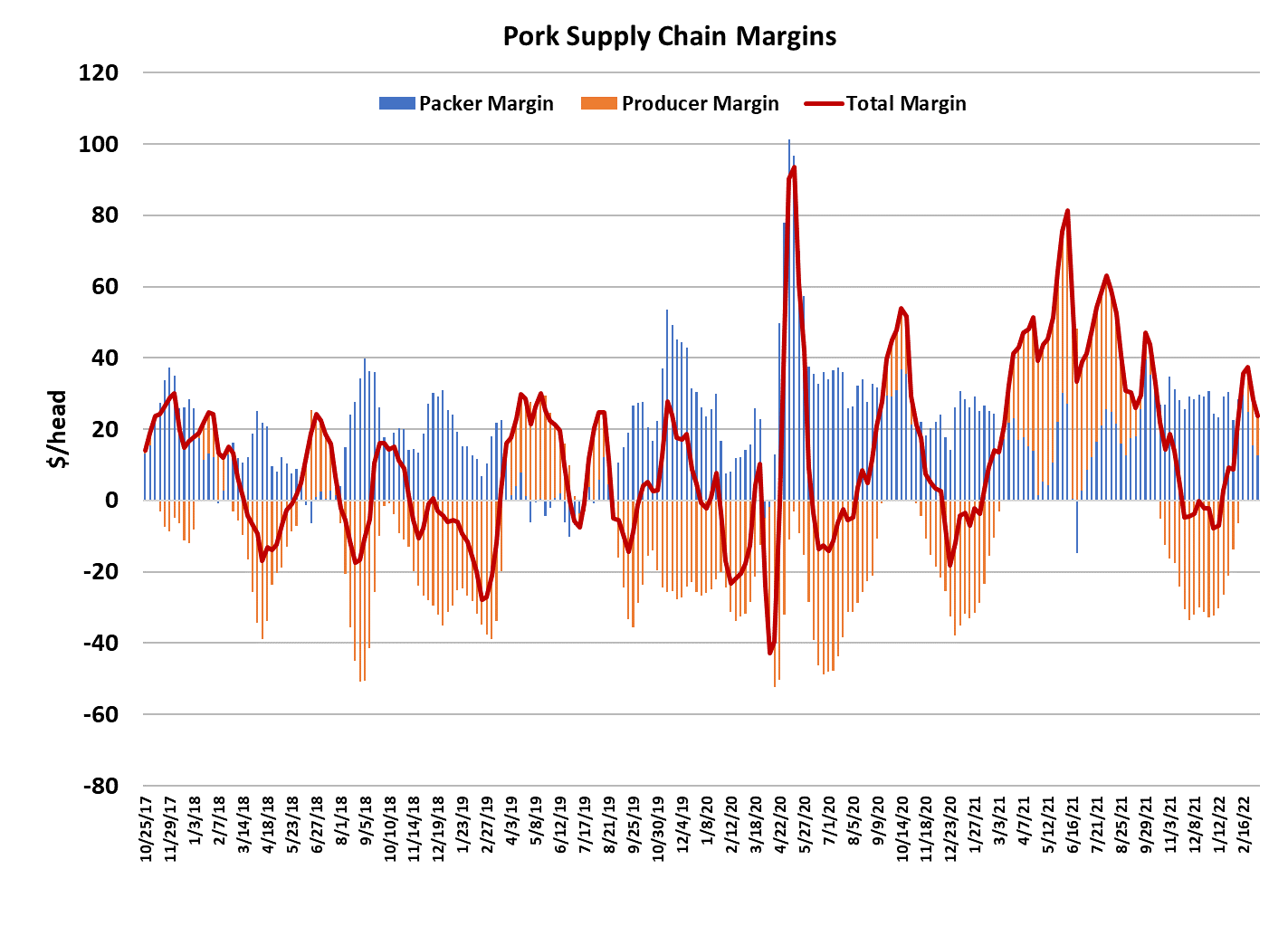

That put a big squeeze on margins and pushed them down to less

than $10 per head. The forecast has margins dipping into the red

next week by about $3/head. Packers can’t be too happy about this

situation. As a result, they have slowed down the Saturday kill, with

this Saturday estimated at 97,000 head and my guess is that next

Saturday could be closer to 50,000 head. All of this has created a

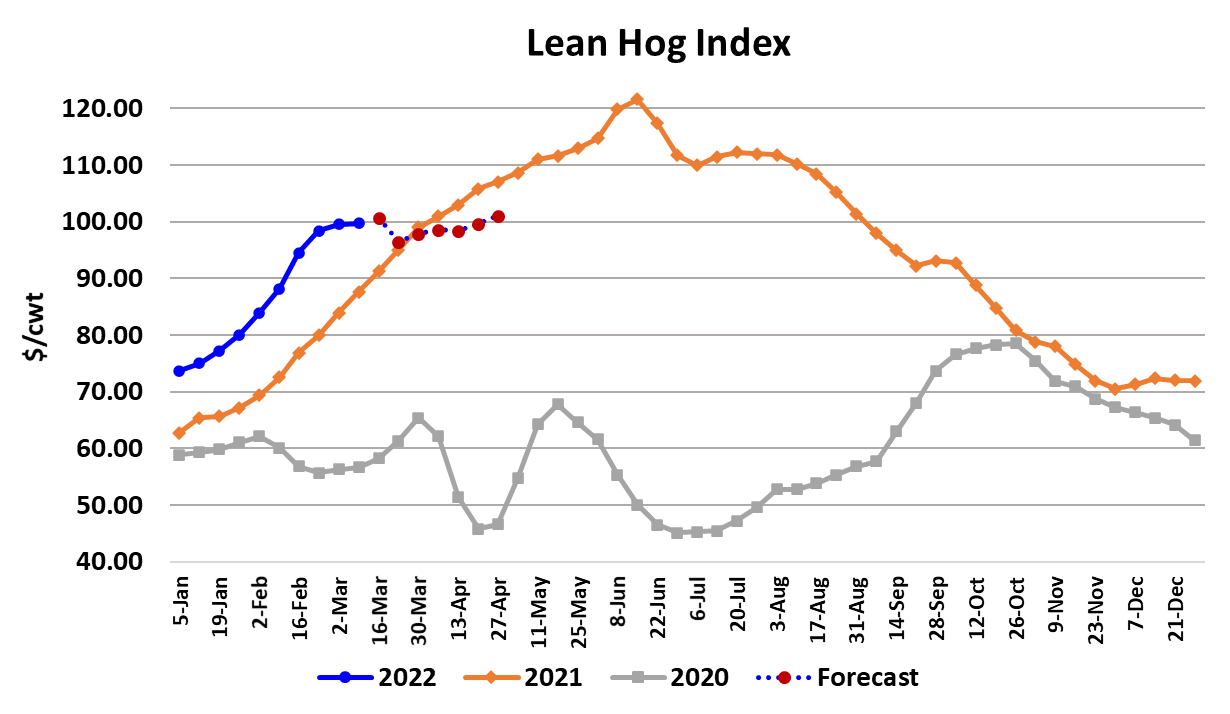

strange market dynamic where cash hog prices are rising, but softer

demand is pushing the cutout lower. It is a huge headache for

futures traders who get all bulled up one day by a strong negotiated

price print and then slapped back down the next day by a weak

cutout print. The two effects have largely offset one another and thus

held the LHI in the $98-100 range for the past 3 weeks.

Once again, it was the bellies that provided the majority of the decline

in the cutout this week, but there was also some help from the loin

primal. The bellies have yet to make another major leg down but I

still think that could be in the cards sometime soon. Hams are

helping to shift the focus away from bellies now as they appear to

have turned lower and that creates a lot of concern. We are still

getting wild moves in the ham primal based on how much boneless

product is included on any given day, but the basic bone-in, 23-27

pound ham has been tracking lower since late last week. Some think

that there are still hams that need to be bought and processed for

Easter, but I’m not so sure about that. The forecast has hams trading

sideways to modestly lower over the next few weeks. The strongest

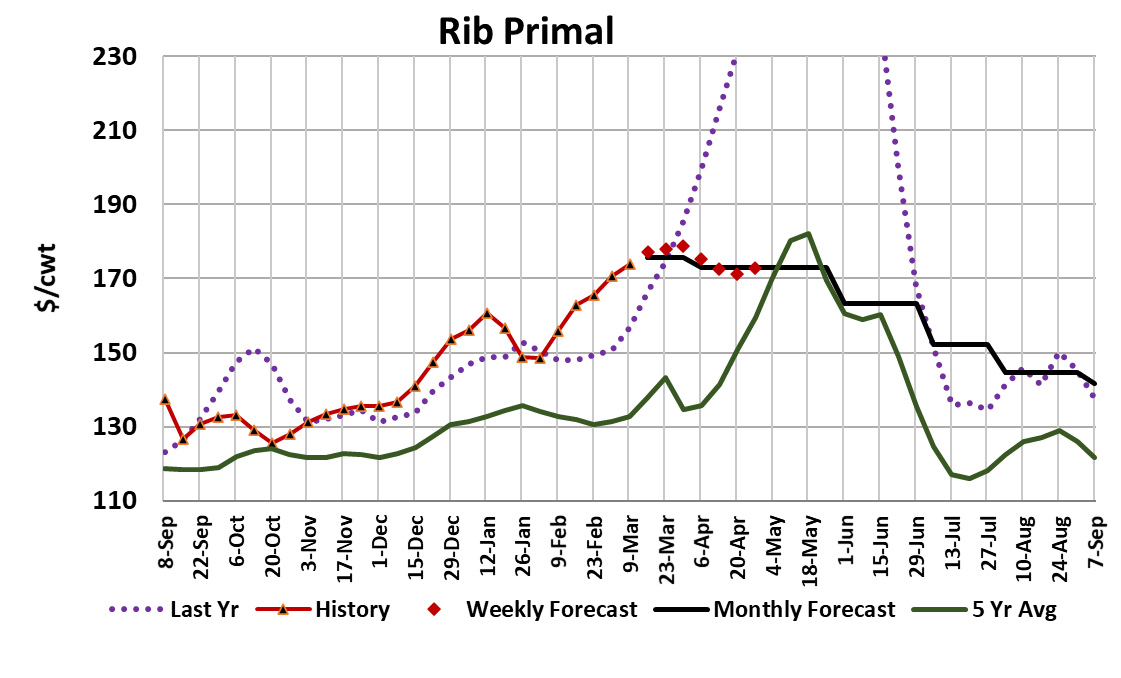

part of the carcass right now is the rib primal, which has been in a

pretty solid uptrend since last October.

The combined margin moved lower again this week, signaling some

further softening of demand. I’m expecting this downcycle to be a

short one, perhaps only lasting 2-3 more weeks, before grilling

season demand starts to kick in. Pork has to contend with much

cheaper beef now for retail ad space and normally beef is the

retailer’s first choice when it come to spring features. If I’m right

about the bellies taking another step lower in coming days, then it is

easy to see how the cutout could move back below $100. It is not

that far from it right now, after printing $102.55 on Friday afternoon. If

it does move back below $100, wouldn’t expect it to trade under $95.

Instead, more of a sideways pattern might develop for a few weeks

until the spring demand kicks in enough to lift it back into triple digits.

I think the pork cutout futures are vastly over-estimating how high

the cutout could get this summer, but I recognize that part of that is

predicated on the idea that there are serious disease problems in

the WCB region and when traders hear the words “disease

problems”, they buy first and ask questions later. This week’s

slaughter came in at 2.475 million head. That was about 30k more

than what the pig crop projected, but it helped to offset a 30k deficit

last week. Thus, in the first two weeks of the March/May quarter,

kills have been almost dead-on with the pig crop estimate. The

flow model suggests that kills should move under 2.45 million head

starting next week and remain below that level until the middle of

August. Going forward from here I think it will be a battle between

shrinking kills wanting to lift prices and softer demand that wants to

push prices lower. The supply side will probably win that battle and

move prices higher as we move into summer, but don’t expect the

cutout to exceed last year’s summer top near $135.

I’m thinking that a top around $115 is more likely this summer. Of

course, if the disease problems are worse than imagined and kills

drop well below the pig crop-implied, then we could stand a chance

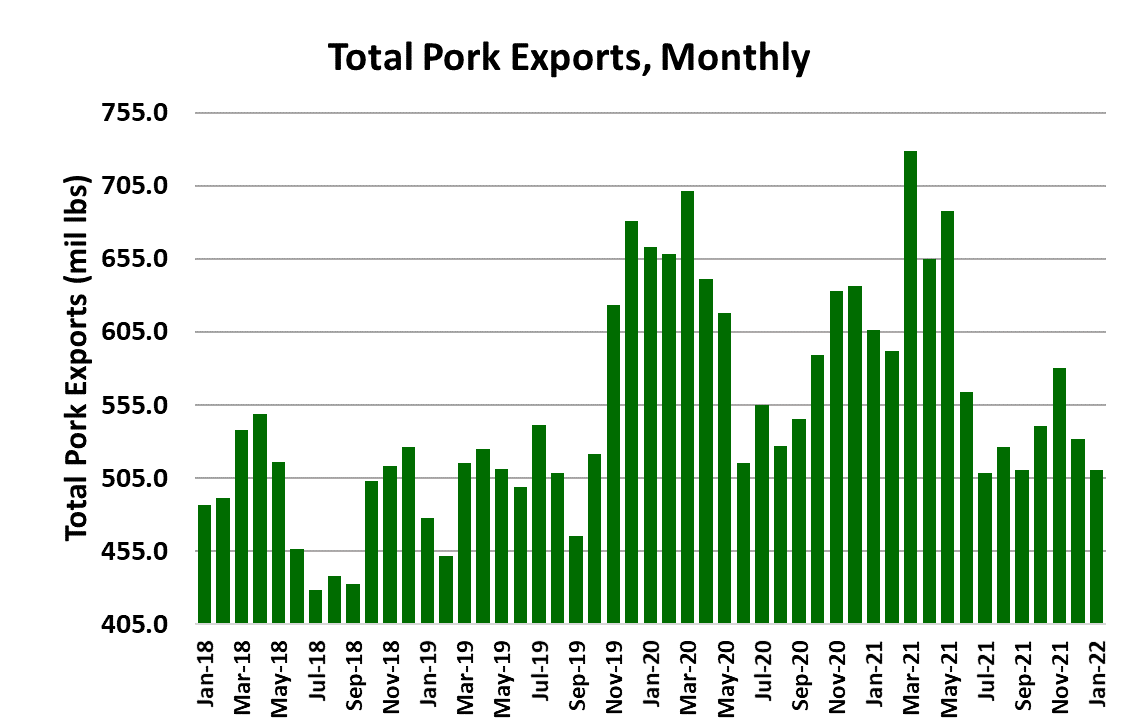

of reaching last year’s top in the cutout. USDA released export

numbers for January this week and they indicated a 15.8% YOY

decline. That is largely driven by much smaller shipments to China

and I don’t hold a lot of hope that movement to China will improve

anytime soon. Imports, on the other hand, were quite strong, up

34% YOY. However, smaller pig crops in recent quarters leading

to smaller YOY kills here in the first half of 2022 will be the

dominant factor keeping per capita availability down 3-5% YOY in

the first two quarters.

Normally, that would point to higher prices than the year before, but

the demand structure in 2022 is expected to fall well short of the

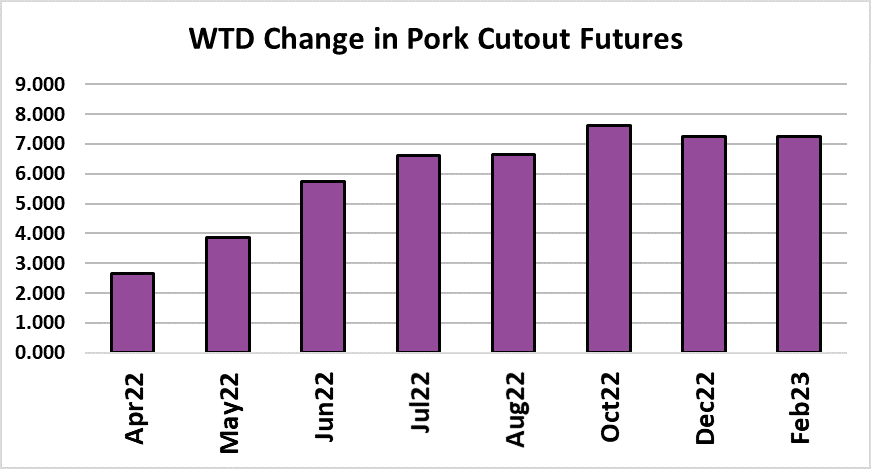

phenomenal demand seen last year. The futures curve was higher

this week, with the biggest gains coming in the summer contracts.

Nearby Apr held in the $100-103 range for most of the week as

traders tried to determine whether stronger negotiated hog prices

would dominate a softer cutout in the LHI or vice versa. That

remains an unanswered question at this point. Next week, watch

the hams for further price erosion. It will be really difficult for the

cutout to make significant gains as long as hams are softening.

Also, don’t be surprised if the bellies express further weakness.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}