Pork Wrap March 10

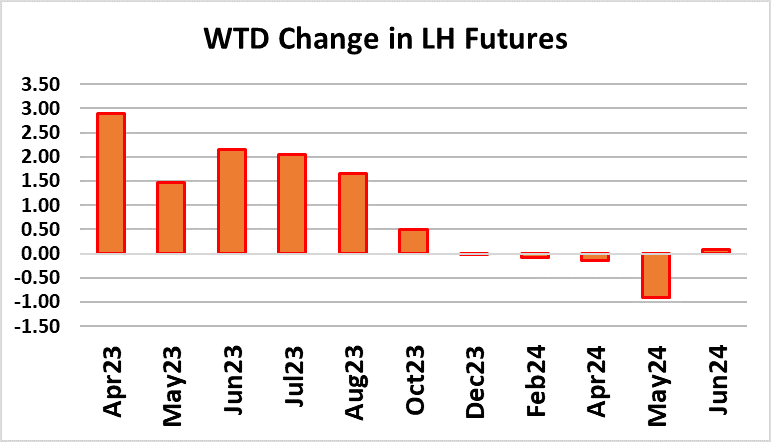

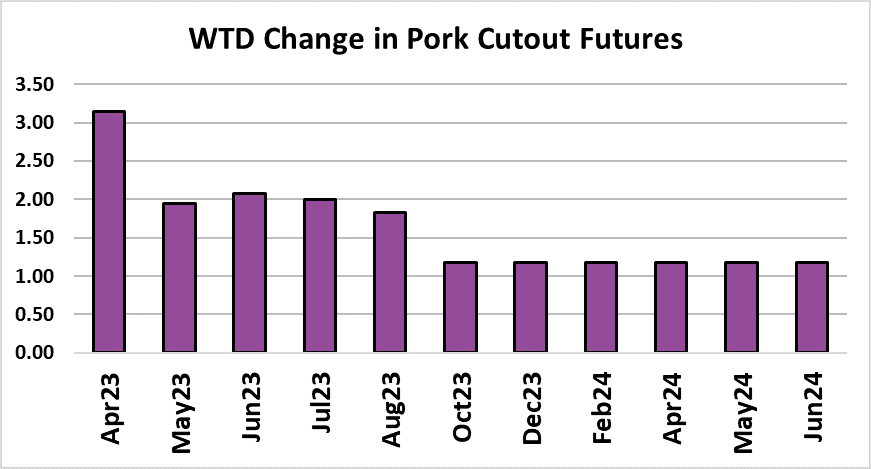

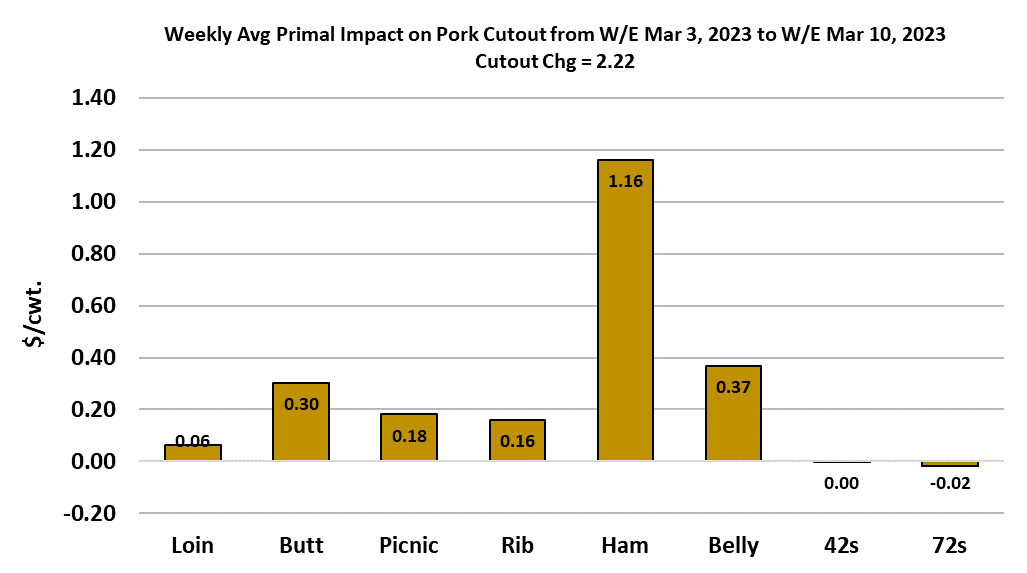

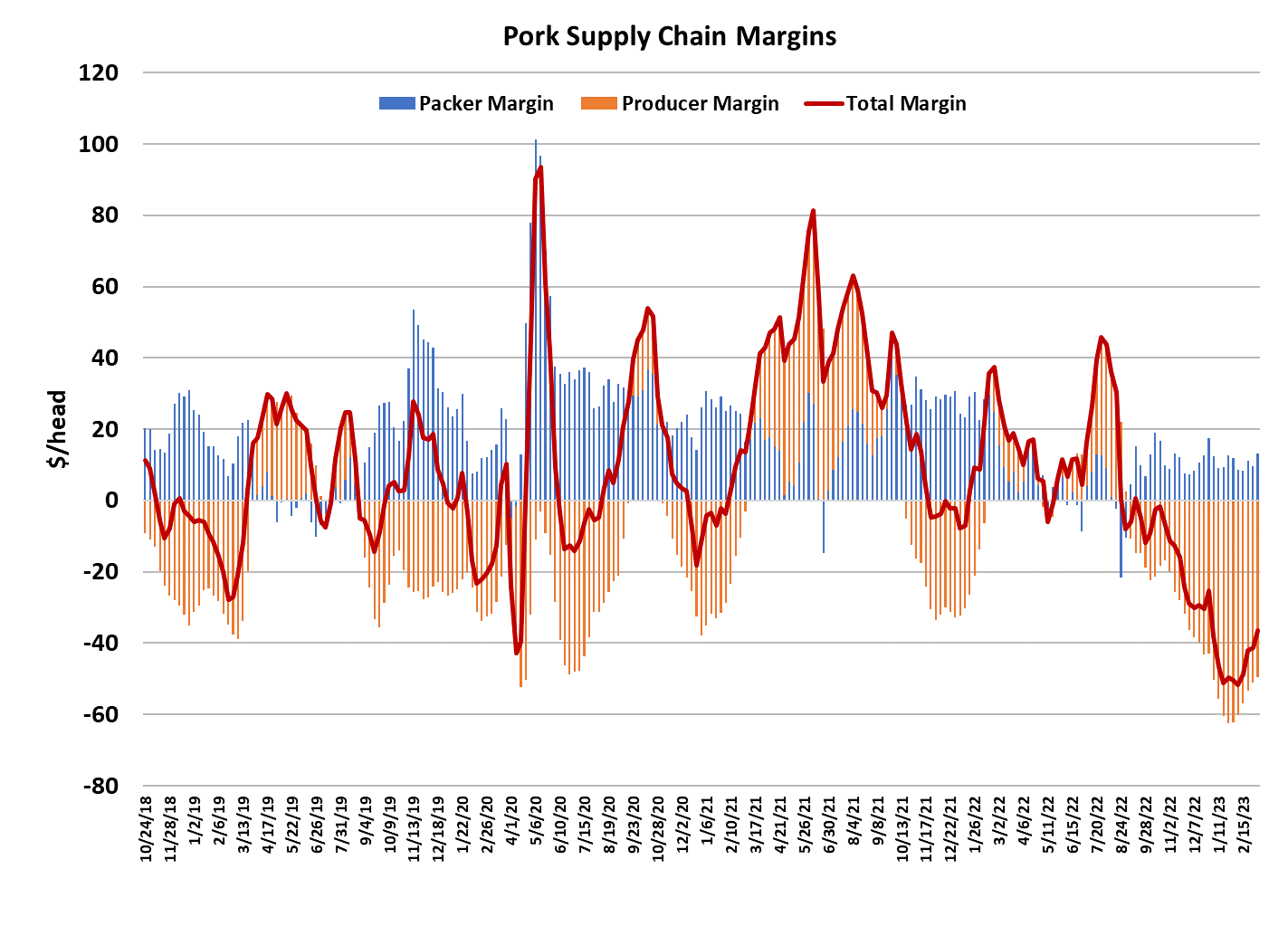

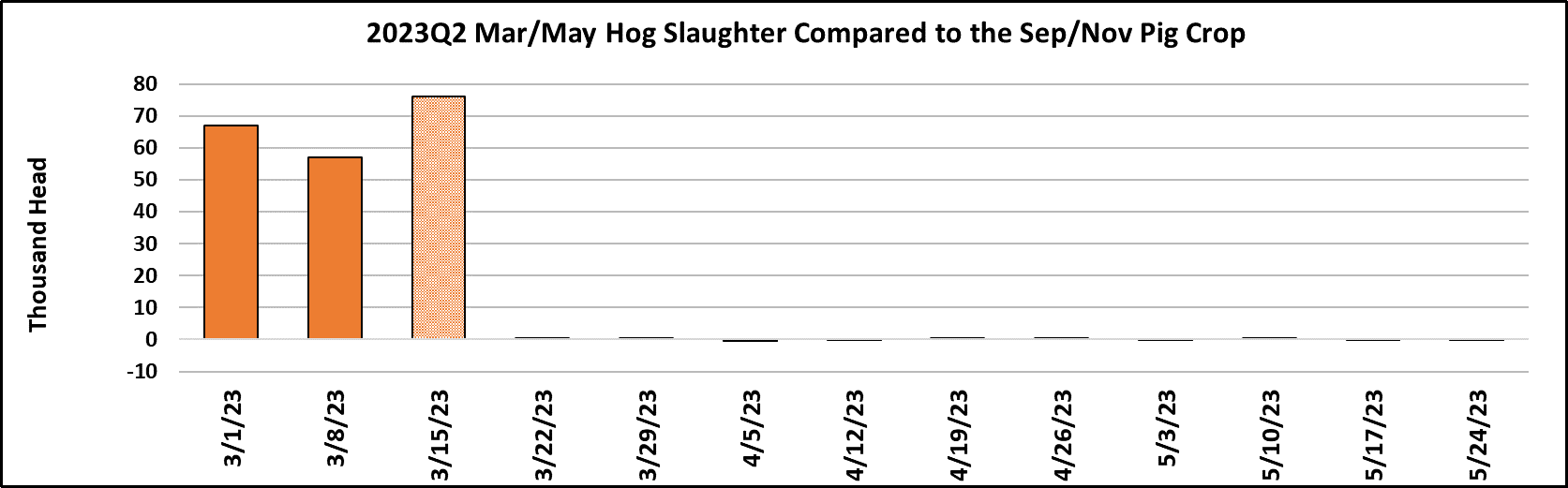

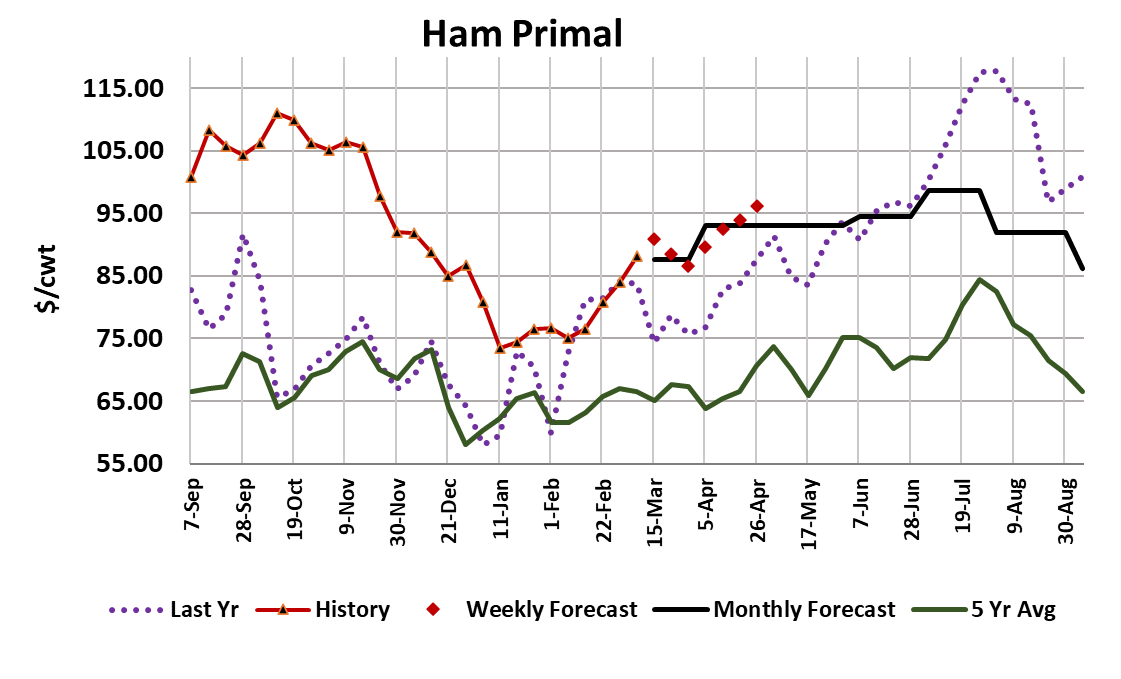

It was another good week for pork prices as the cutout added $2.22/cwt to average $87.64/cwt. Given how little the cutout has moved so far this year, any time that we get a move over $2, I would consider that constructive. The negotiated markets were about as flat as they could be with the WCB gaining only $0.01 and the NDD gaining $0.00 on a weekly average basis. That boosted packer margins to about $13/head and that is the largest packer margin so far this year. Perhaps packers will get a little more aggressive in the spot hog market next week as they try to capitalize on stronger margins. The real hinderance to advancing the negotiated market continues to be larger-than-expected hog supplies. I’ve talked about how the data seem to indicate that USDA underestimated the Jun/Aug pig crop by about 700k and now the for each of the first two weeks in the March/May quarter, the industry has over-killed the Sep/Nov pig crop by about 60k per week. Since there are 13 weeks in a quarter, if the overkilling continues at that rate, then we would see 780k more hogs come to slaughter in the March/May quarter than was advertised by USDA back in December. That is something to keep an eye on. I’ve been raising packer margin forecasts for this spring in anticipation that packers will not have to compete as vigorously for spot hogs as I once imagined. And I have bad news for the summer market bulls too. After fine tuning my supply forecasts for the upcoming H&P report, it has become clear to me that the hog supply for the Jun/Aug quarter will be at least 1% larger than last year and perhaps even 2% larger. Last summer we had the perfect storm of tight hog supplies and very strong demand, but this summer is shaping up to be one of bigger supplies and much softer demand. The futures market seems to be catching on to this because traders pushed the Jun contract below the $100 mark for a time this week. I wouldn’t be surprised if we see all of the summer contracts trade below $100 for a while this spring, likely after the H&P report. Producer profitability improved slightly this week with margins now at -$49/head, which is better than the -$60/head back in February, but still pretty dismal. That might lead you to believe that producers will shrink the breeding herd in the next H&P report. I’m forecasting the breeding herd to be down slightly from last quarter, but up slightly from last year. It will be interesting to see if the consensus forecast also has a YOY increase in the breeding herd. I don’t think futures traders will like that very much. I’m also looking for some growth in the productivity of the hog herd (pigs per litter & farrowing rate), so when I combine that with a modest YOY increase in the breeding herd, I get a scenario where the most recent pig crop could be up almost 2% YOY. If that comes true, it won’t be very helpful to the fall futures. This week packers came in with a stronger-than-expected Friday and Saturday kill, boosting the weekly total to 2.497 million. Technically that is below the magic 2.5 million mark, but not by much. That should create ample product availability next week. FI carcass weights were down one pound this week and are holding in a mostly sideways pattern that is typical for this time of year. The DTDS weights have been relatively low, so I don’t think there is any serious backlog of hogs. Instead, producers are probably just eager to get hogs marketed as rapidly as they can because every hog they sell is losing close to $50. If the Sep/Nov pig crop was correct, we should be seeing weekly kills closer to 2.42 million head per week right now. Fortunately for the bulls, the demand side of the pork complex seems to be perking up. All of the primals were higher on the week, with the hams leading the way. The recent strength in ham pricing has been impressive with the 23/27 lb. hams now being quoted close to $93/cwt. That’s about $23 higher than a month ago. The retail items are also creeping higher and I’d look for that to continue as retailers increasingly turn to pork as an alternative to high wholesale beef prices. The bellies still seem to be treading water but have shown a slight upward tendency from time to time. The forecast has the cutout grinding another $2 higher next week to $89.60 and I’d be really surprised if it can muster more than that. Negotiated hog pricing should also benefit and that means the LHI continues to slowly work higher. We are now about one month from expiration of the Apr LH contract that settled today near $87.50. That is about $2 below my fundamental forecast, but I’d say that the risk to that forecast lies mostly to the downside. Nothing on the board looks all that mis-priced right now. Aug23 looks the most over-priced while the distant 2024 contracts look the most under-priced. Next week, keep an eye on the daily kills for evidence that we are going to have yet another week of over-killing, and look for the LHI to gain at least another dollar, maybe two.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}