Pork Wrap March 1

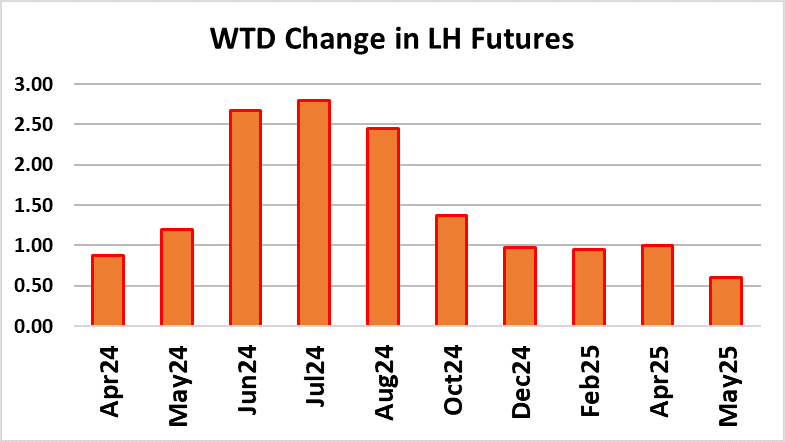

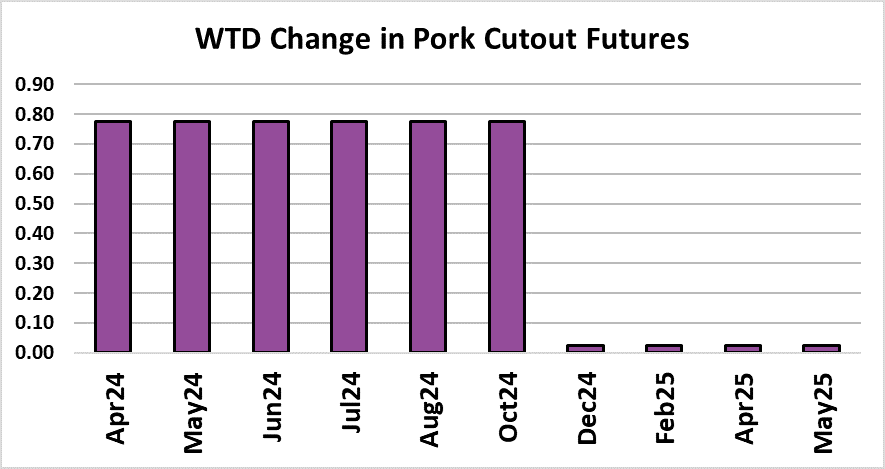

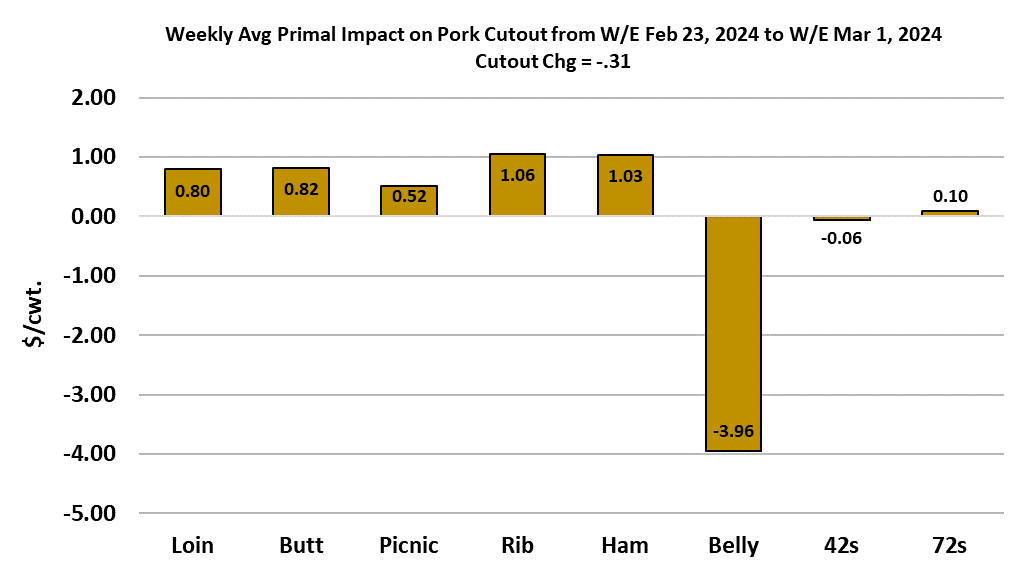

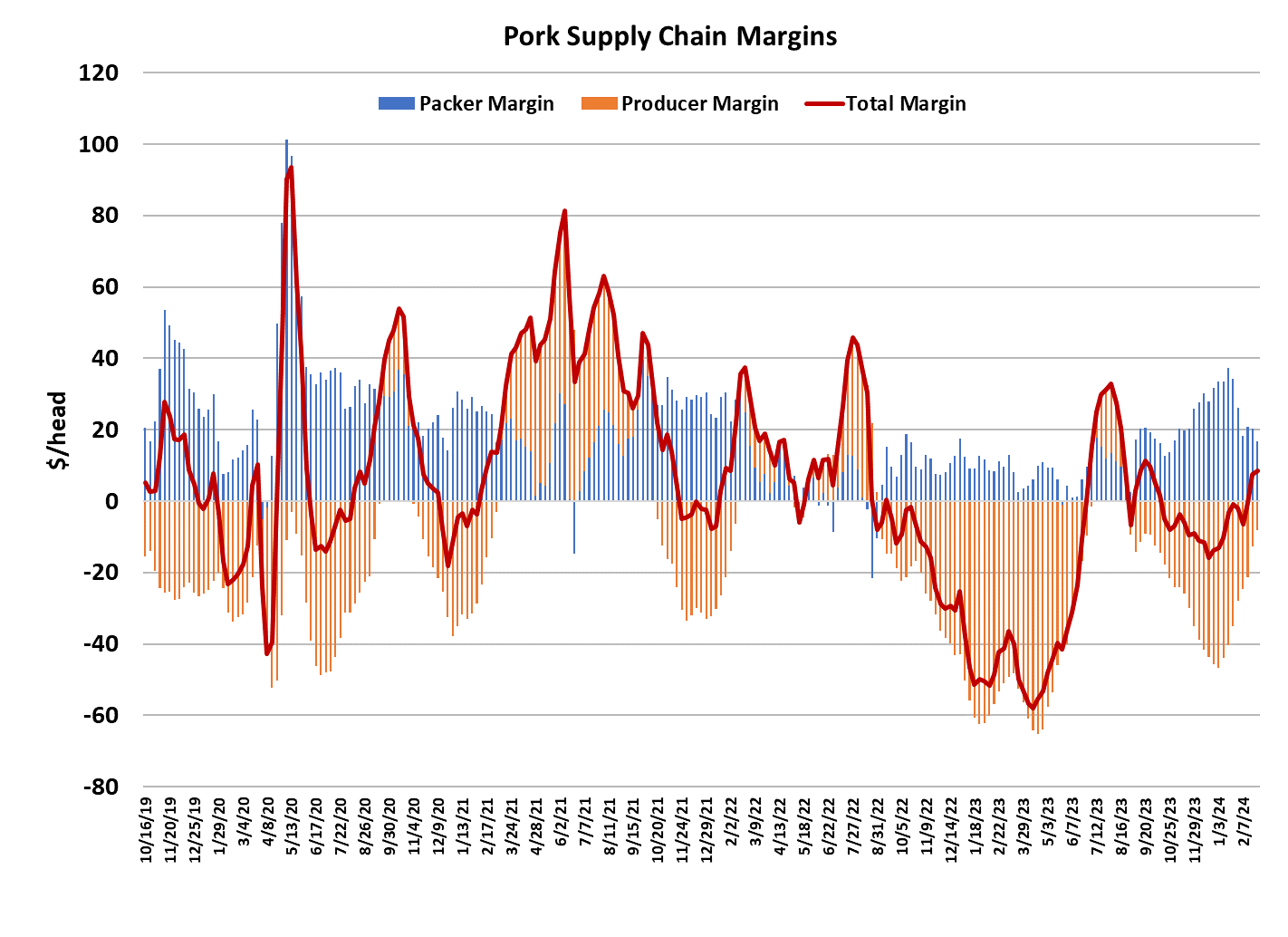

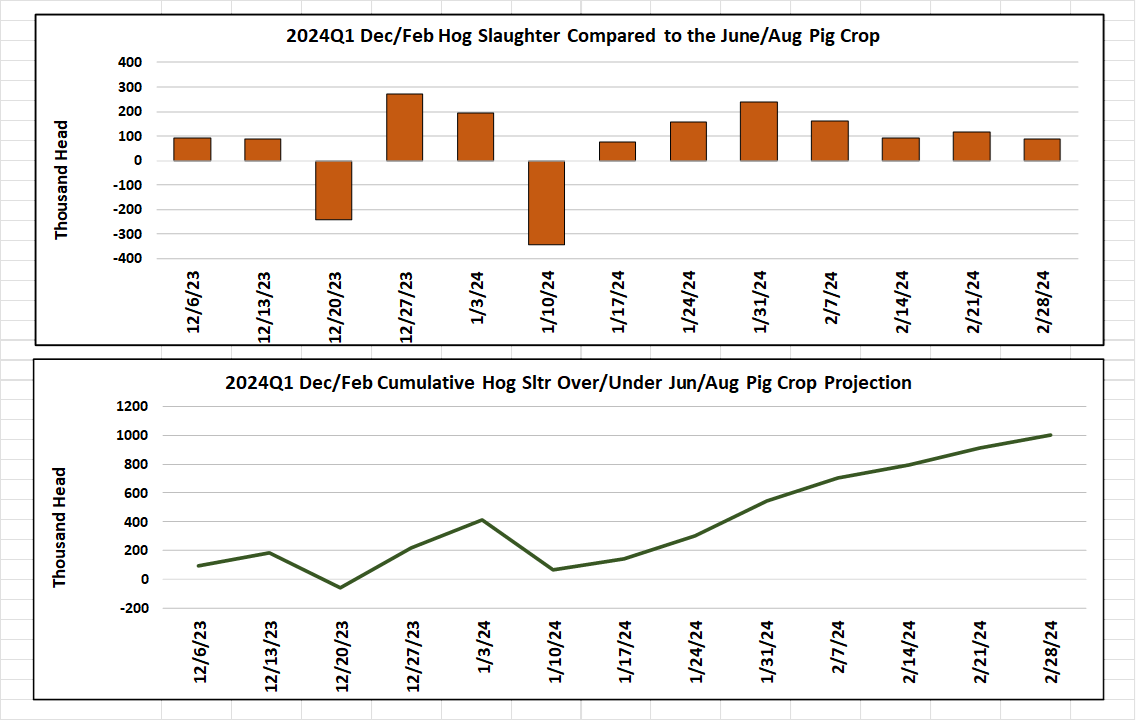

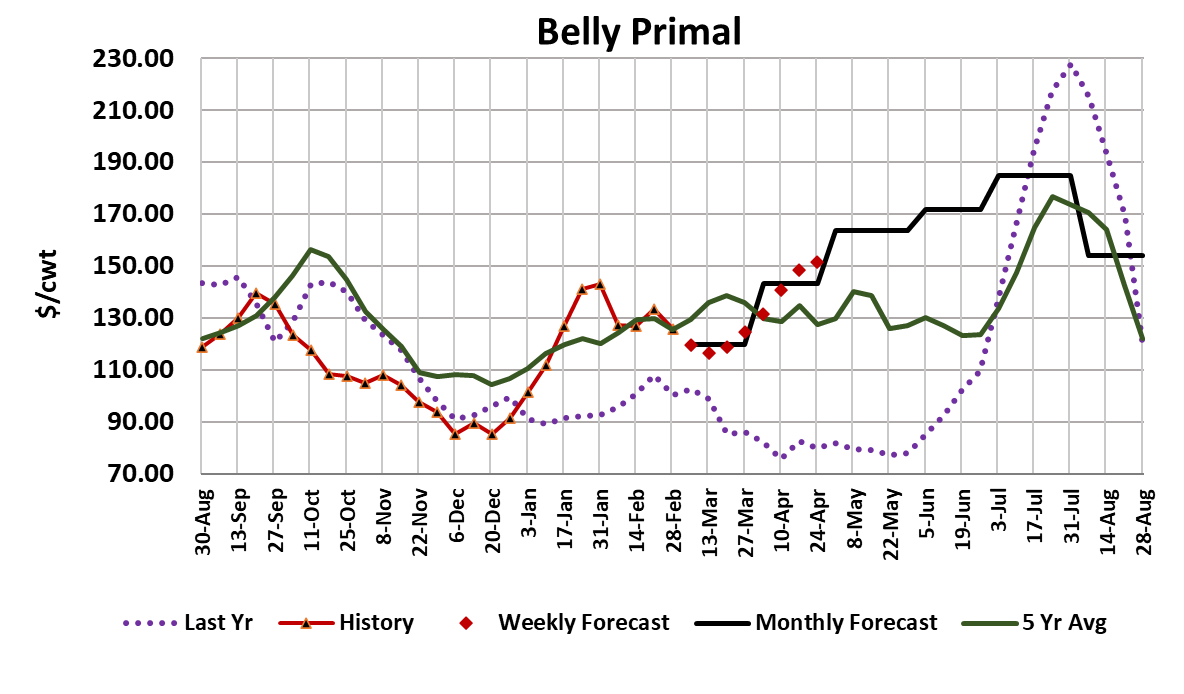

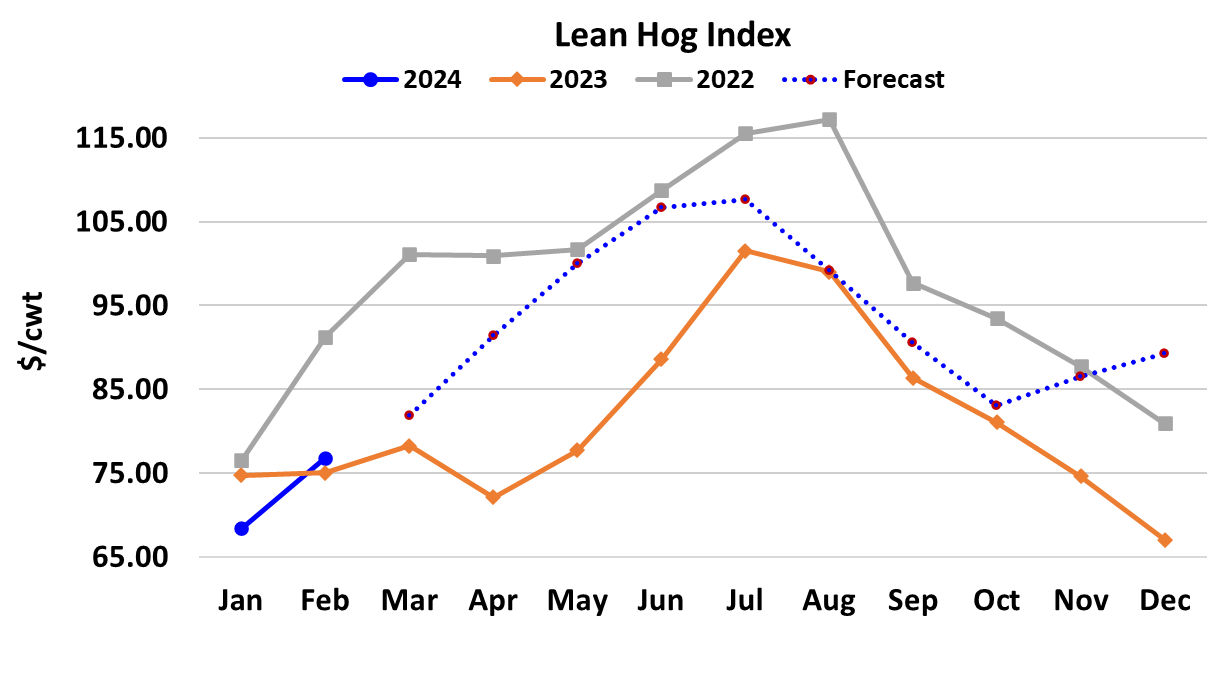

Belly prices stumbled this week and that was enough to move the cutout below the previous week’s level. The cutout averaged $91.57, down $0.31/cwt from the week before. However, it isn’t all bad news because the belly primal is the only part of the carcass that is currently trending lower. All of the retail items and hams moved higher this week. The belly primal averaged about $8/cwt. below last week, but the situation is actually worse than that number makes it look because almost no belly volume was reported on Friday, forcing USDA to print a primal value based on odd-ball items that was up $20 from the day before. That “fake news” boosted Friday’s cutout over $94, but there is little chance that will hold. Once better volumes of bellies trade on Monday, I’d expect to see the cutout pull back to the $90-91 area. And there is still the question of whether or not bellies will continue to trend lower. I don’t think that they will, but last year from this point through most of April, bellies did keep trending lower and that was a big reason why the cutout struggled so much last spring. Hams are another area of concern. The primal moved higher for the fourth week in a row, but the Easter business is close to being done and hams are starting to look a bit toppy. The worst case scenario would have the hams and bellies both trending lower at the same time. That would make it very difficult for the cutout to advance from here. For now, I’m taking a cautious approach and forecasting the cutout sideways for a couple of weeks before it putting it back on an uptrend. It is encouraging to see the retail items all advancing week after week, even if the increases are small. That tells me that overall demand is getting better and the combined margin seems to confirm this. Prices for processing items like bellies and hams tend to be more volatile and can change direction for a week or two just based on a couple of big users needing, or not needing, raw materials, so getting too bearish based on a dip in the bellies and/or hams can be a mistake. Futures traders didn’t seem to have a problem with bearishness this week, however, as all contracts posted gains and all of the summer contracts finally moved solidly over the $100 mark. Apr still looks a couple of dollars too low relative to the LHI forecast for mid-April when it expires, but it could be vulnerable to a pullback in the near term if hams go on the defensive. Sow slaughter continues to run high, suggesting that the breeding herd is being reduced. We will find out a lot more about that later this month when USDA releases its next issue of Hogs & Pigs on March 28. This week marks the last week of the Dec/Feb quarter and I calculate that for the quarter as a whole, the industry over-killed the Jun/Aug pig crop by right at 1 million head. Clearly, USDA will need to revise that pig crop estimate higher in its next report. The Sep/Nov pig crop was estimated to be down 0.2% YOY, so if that is close to correct, then it would make sense to look for a slight YOY decline in hog availability during the upcoming Mar/May quarter. However, they have underestimated the pig crops so often, and so badly, in the past couple of years that it is difficult to expect this one to be correct. As a result, market participants would be wise to look for at least a 1% YOY increase in pork production over the next three months. This week’s slaughter registered 2.55 million head, down about 30k from the week before. Next week’s slaughter could perhaps be a little larger than this week’s, but in general we should see weekly slaughter levels easing lower during March and certainly in April. Negotiated hog prices pressed higher this week, with the WCB base price increasing $2.13/cwt. on a weekly average basis. With hog prices rising and the cutout slightly lower, packer margins compressed, now at a little over $16/head, down about $4 from the week prior. That is still a very good margin for this time of year and it is around $7 better than what they were getting last year at this time. Still, this is the time of year when margins tend to decline and by the middle to end of April we could be seeing single digit margins. This week’s cold storage report showed total pork in cold storage as of Jan 31 down almost 10% YOY. That should help prevent a repeat of last spring’s weak pricing that was at least partially caused by large inventories. Total bellies in cold storage were reported down 8.5% YOY, which is good, but not as good as the 10-30% declines that were posted in Q4 last year. The build up of bellies in cold storage during January was bigger than the average seasonal increase, so that is a little worrisome and might be an indicator that belly demand is struggling more than previously thought. Next week, watch those bellies and hams. Both seem to be at increased risk for a downturn and even if they don’t decline much, we could still see next week’s cutout struggle to post more than a $1 increase.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}