Pork Wrap June 9

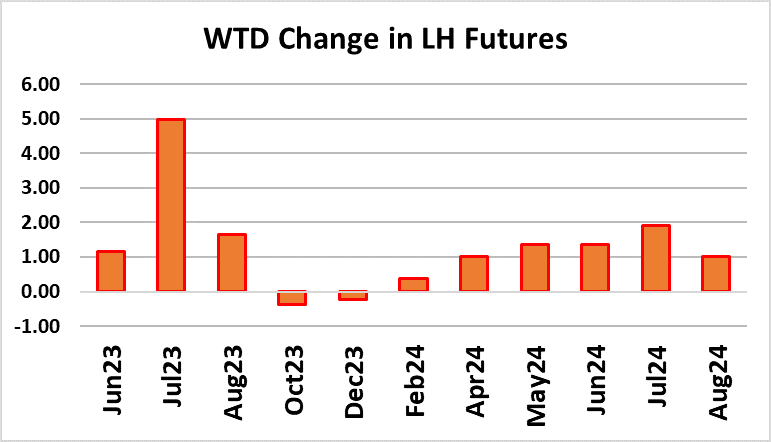

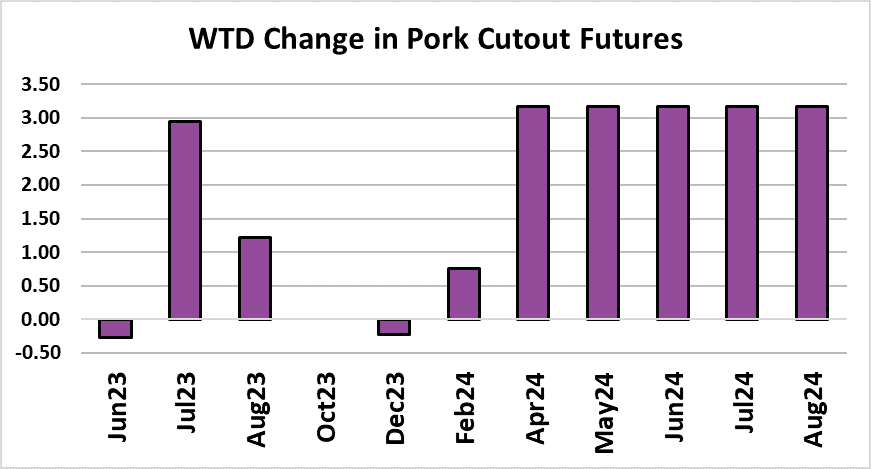

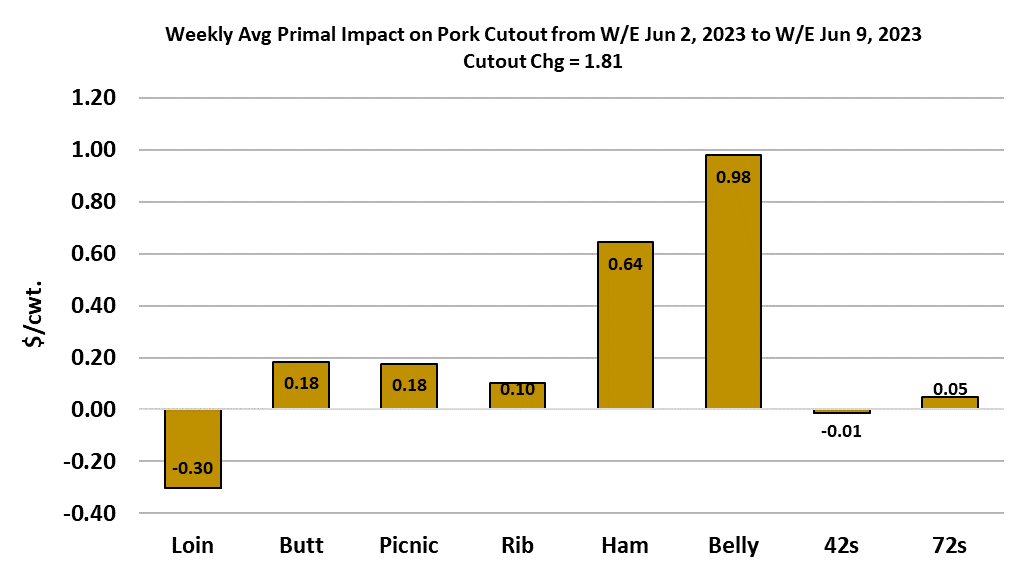

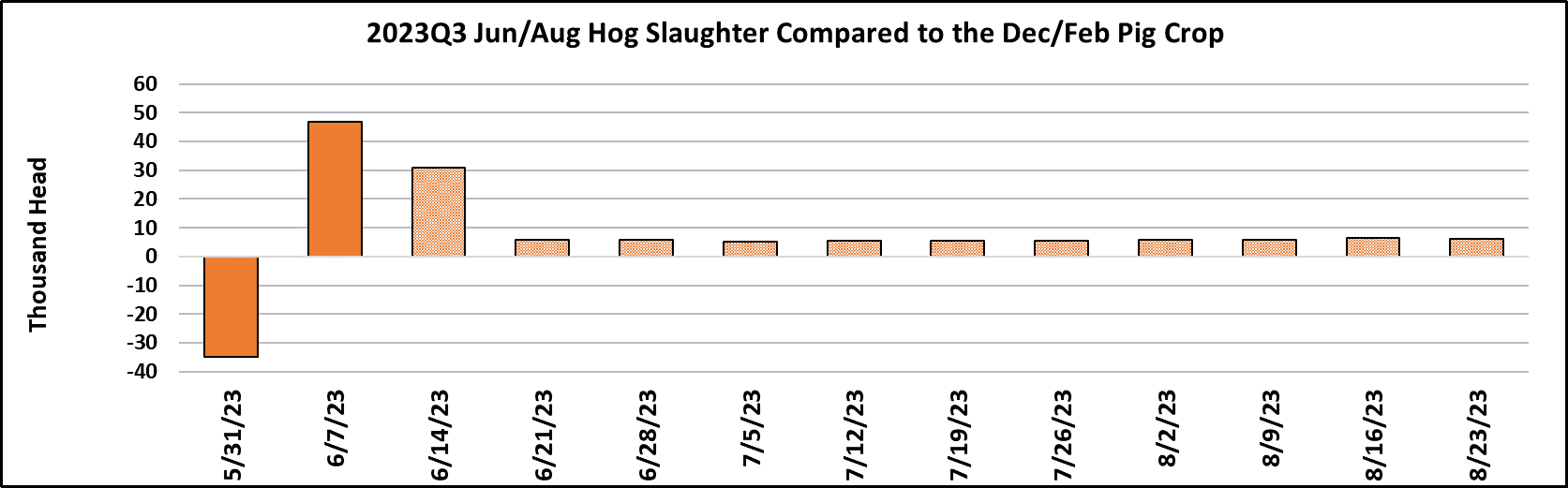

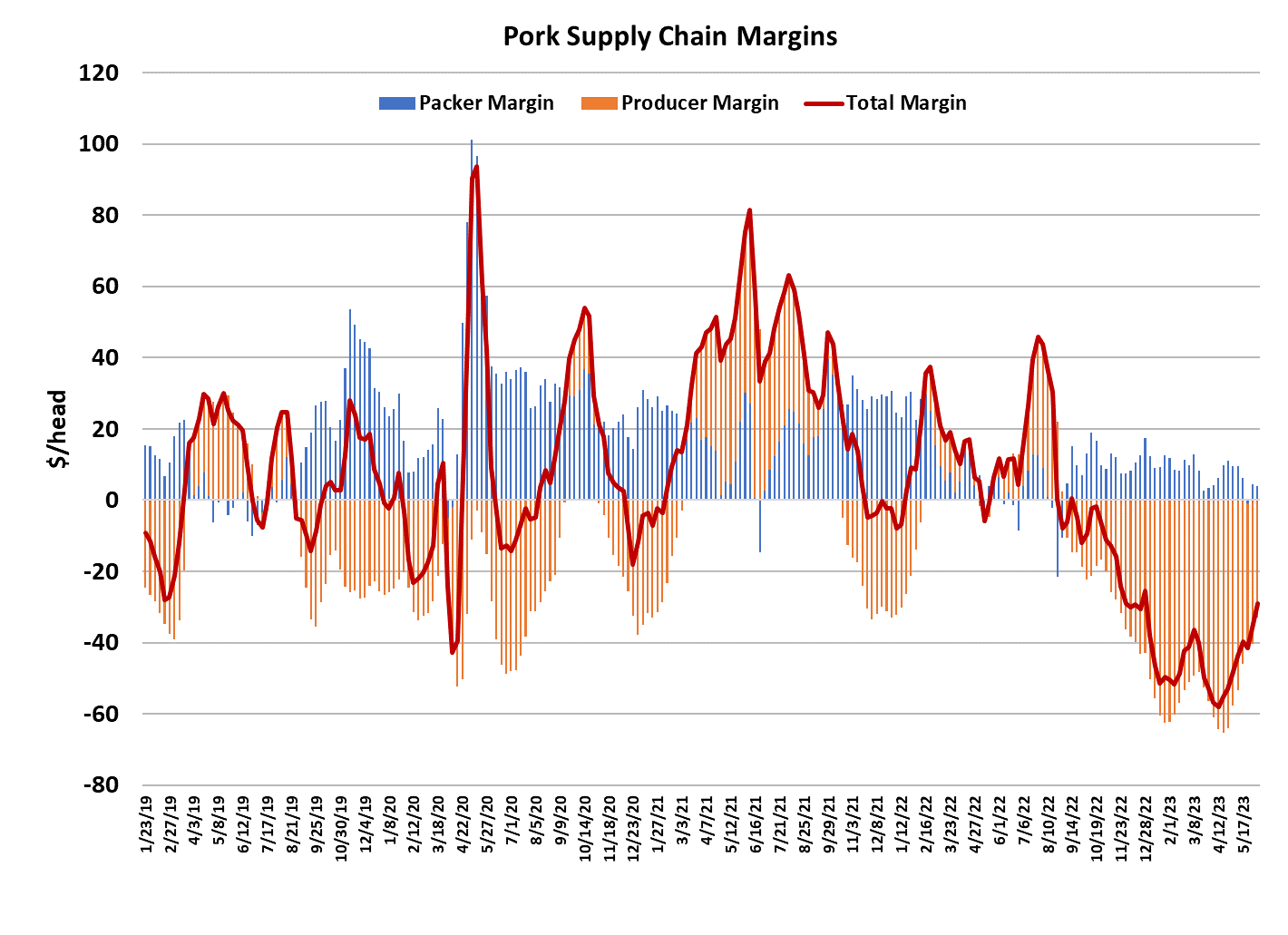

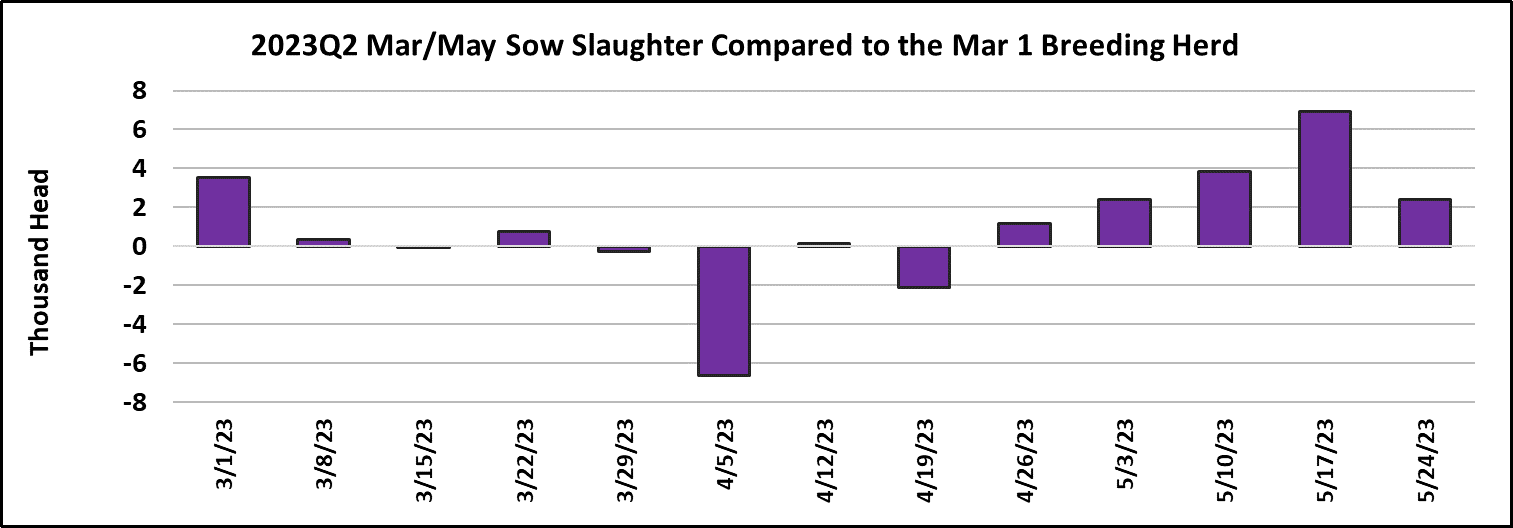

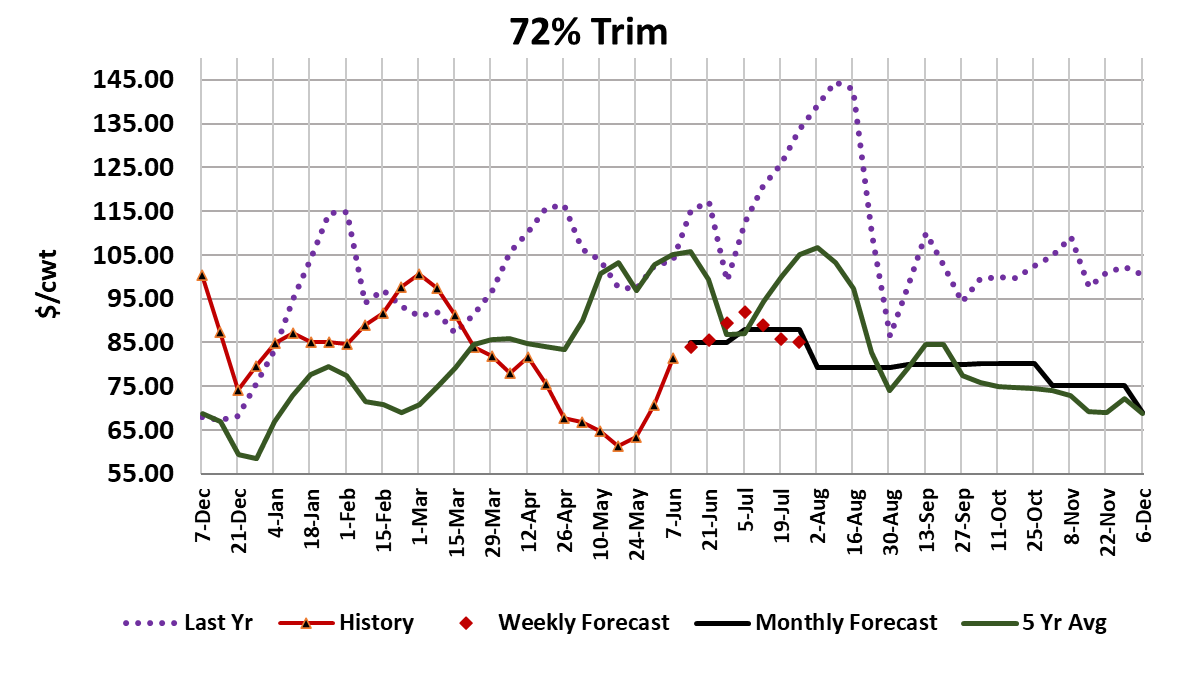

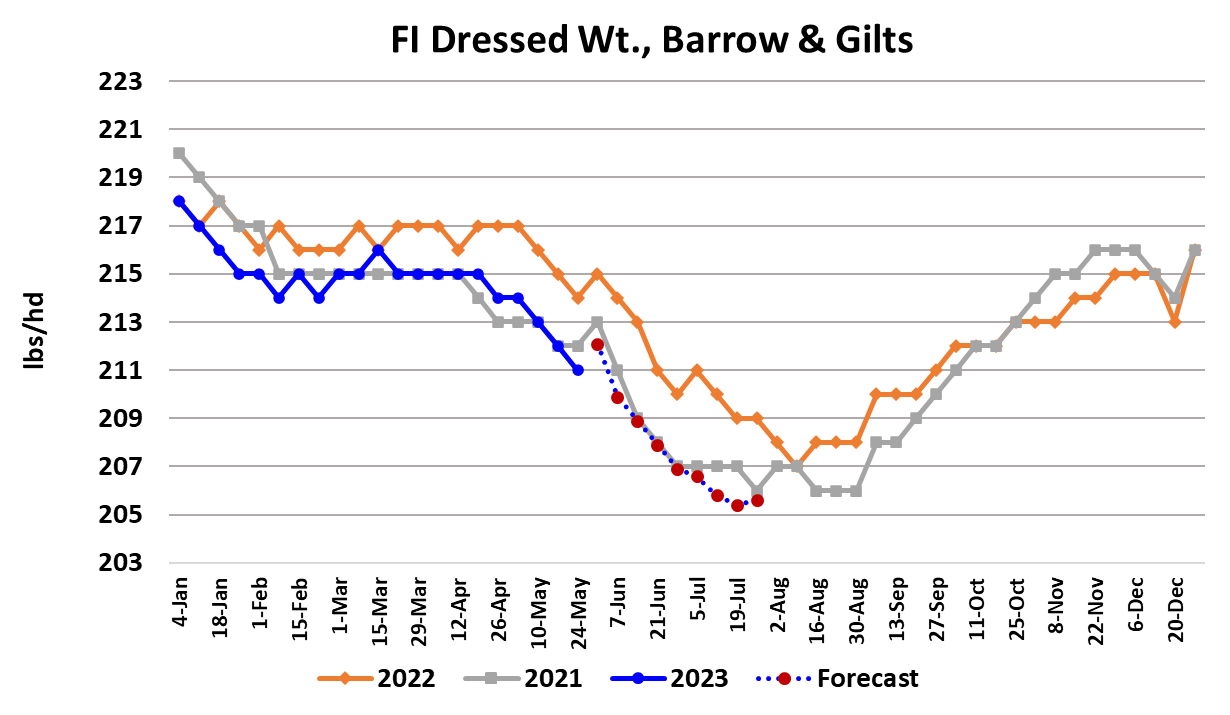

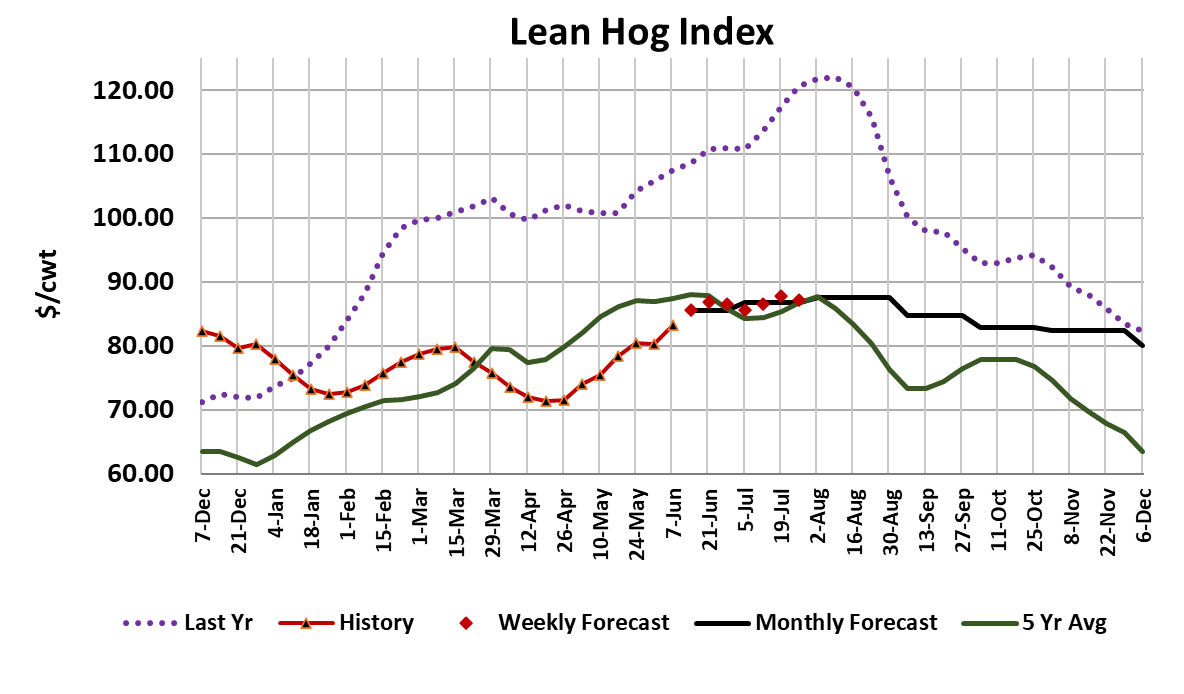

The pork cutout has increased its upward momentum lately. Instead of gaining a dollar a week it is now adding close to $2 per week. This week’s average was $86.65, up $1.81/cwt. The problem for packers is that the negotiated hog markets are rising much faster than the cutout. This week, the prices in the WCB region were up $6.30/cwt on a weekly average basis and the National Daily Direct market was up $7.50. At this rate, packers could very well see negative margins next week unless they can breathe more life into the cutout. To be fair, some of this week’s gain in the cutout was illusory, the result of a sharply higher belly print on very low volume that happened on Monday. That made the belly primal the biggest gainer on the week, but it is probably not something we can count on going forward. Still, the combined margin worked higher again this week as it slowly comes out of the worst downdraft in history. Futures traders’ optimism increased this week, particularly for the near term, with the July contract adding $5/cwt Friday to Friday. Traders are probably more encouraged by what they see going on in the negotiated hog markets than in the pork market. Hog supplies are tightening up seasonally and that means that packers must compete more vigorously to flesh out their kill schedules. Negative packer margins are common in June and July. This week’s kill came in at 2.36 million head and next week could be down close to 2.3 million. We might see a couple of non-holiday weeks down around 2.25 million, but I don’t think it will go any lower than that. The industry actually overkilled the pig crop this week, but that was by almost the same amount as the underkill in the previous week, so the quarter-to-date numbers are tracking the pig crop closely so far. The DTDS weights for hogs moved lower again this week and are now very close to all-time record lows. No wonder producers are finding it easy to move the cash market higher. The weather in the Midwest has been rather benign so far this summer, but it is important to watch it because with hog barns so current, even a modest heat wave could slow down hog weight gains and send negotiated prices sharply higher. Concerns over Prop 12 implementation seem to have faded because the California Dept of Agriculture has made it clear that they won’t be aggressively looking for non-compliant pork on July 1. In fact, since they will allow sellers to clear any non-compliant pork they have in inventory without penalty, it is a good bet that pork users in California will try to build stocks in late June in order to avoid paying the premium for compliant pork as long as they can. That could result in a modest demand boost later this month. As a result, futures traders are no longer afraid to buy the July contract and they correctly recognize that the rapidly increasing negotiated market could push the LHI over $90 in time for the July settlement at mid-month. They seem a little less certain about the more distant contracts, however. Pork that is Prop 12 compliant will almost certainly sell for a higher price than non-compliant pork, but it won’t be included in the normal negotiated cutout. Instead, USDA will put Prop 12 pork into the “Specialty” pork report that is released on a weekly basis every Monday. Thus, all of that higher priced pork won’t have a chance to move the LHI upward. In fact, because prices for non-compliant pork could drop as more of it has to clear the domestic market, the price reporting structure could result in lower cutouts and lower LHIs once the program is up and running. The weekly export data posted a sharp drop this week, but the data was for the week including the Memorial Day holiday, so I don’t want to read too much into it. With pork demand slowly working higher and hog supplies declining seasonally, it is a good bet that pork prices will remain on an upward trajectory over the near term. There has been a huge surge in wholesale beef prices over the past two weeks, so that might shift some retailer demand in the direction of pork if it wasn’t already headed that way. With the gains in hog prices, producer margins continue to improve and this week the increased by about $8/head to -$33/head. By the time we get to the end of July, that margin might only be $10-15 underwater. USDA will release the next issue of Hogs and Pigs on June 29. I will be truing up my supply forecasts in anticipation of that report in the next few days and they should be ready to go next week. I think it is reasonable to look for moderate reductions in the breeding herd given all of the financial pain that producers have endured so far in 2023. Sow slaughter came in a little higher than expected toward the end of the March/May quarter, so that might be the first indication that liquidation is getting underway. Depending upon how much liquidation occurs, there may need to be some scaling back in hog slaughter capacity or else pork packers might find themselves in the same situation as beef packers right now: too many shackles chasing too few animals. Next week, watch for the negotiated market to surge higher again, just in time for Wednesday’s expiration of the Jun futures. The cutout likely moves higher too, but probably not in a big way.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}