Pork Wrap June 7

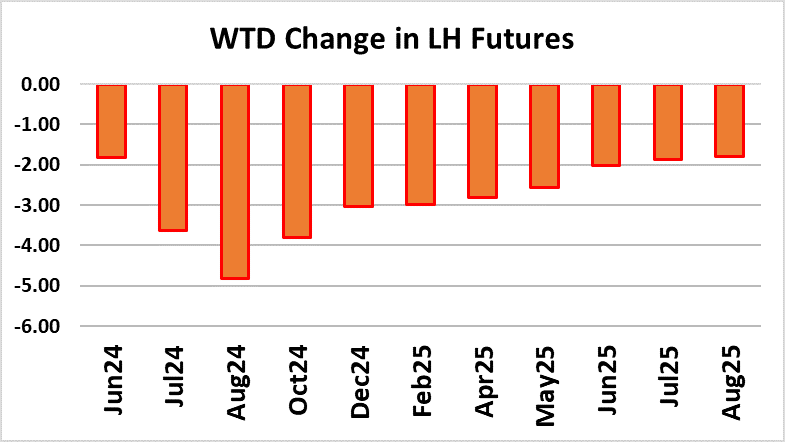

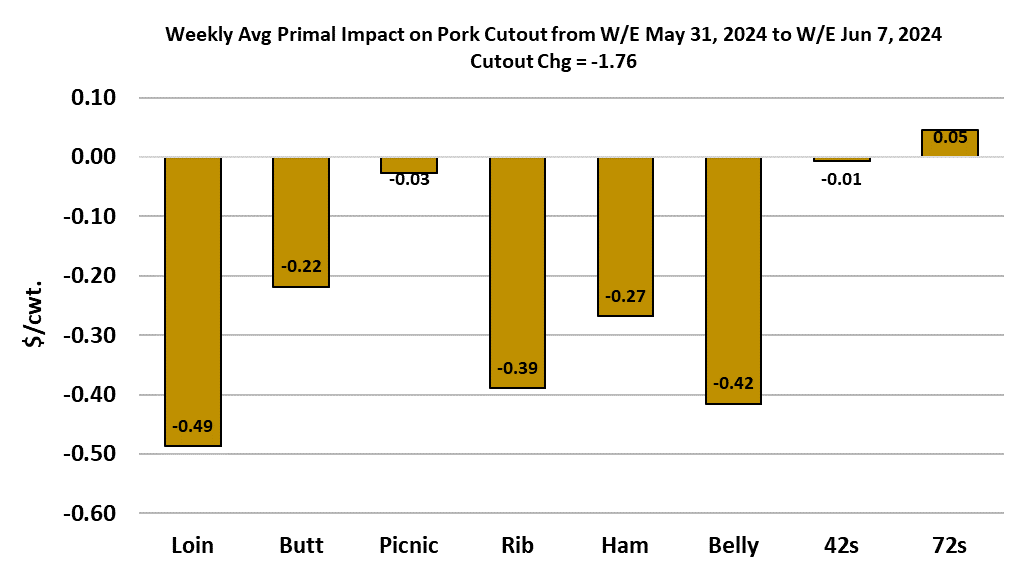

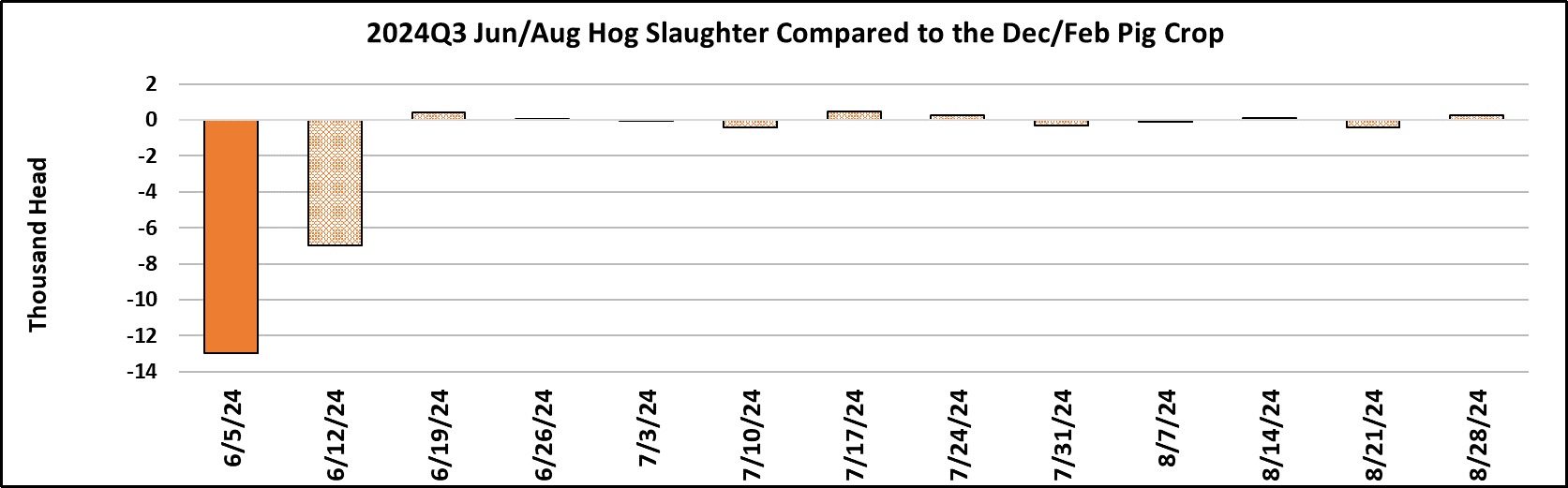

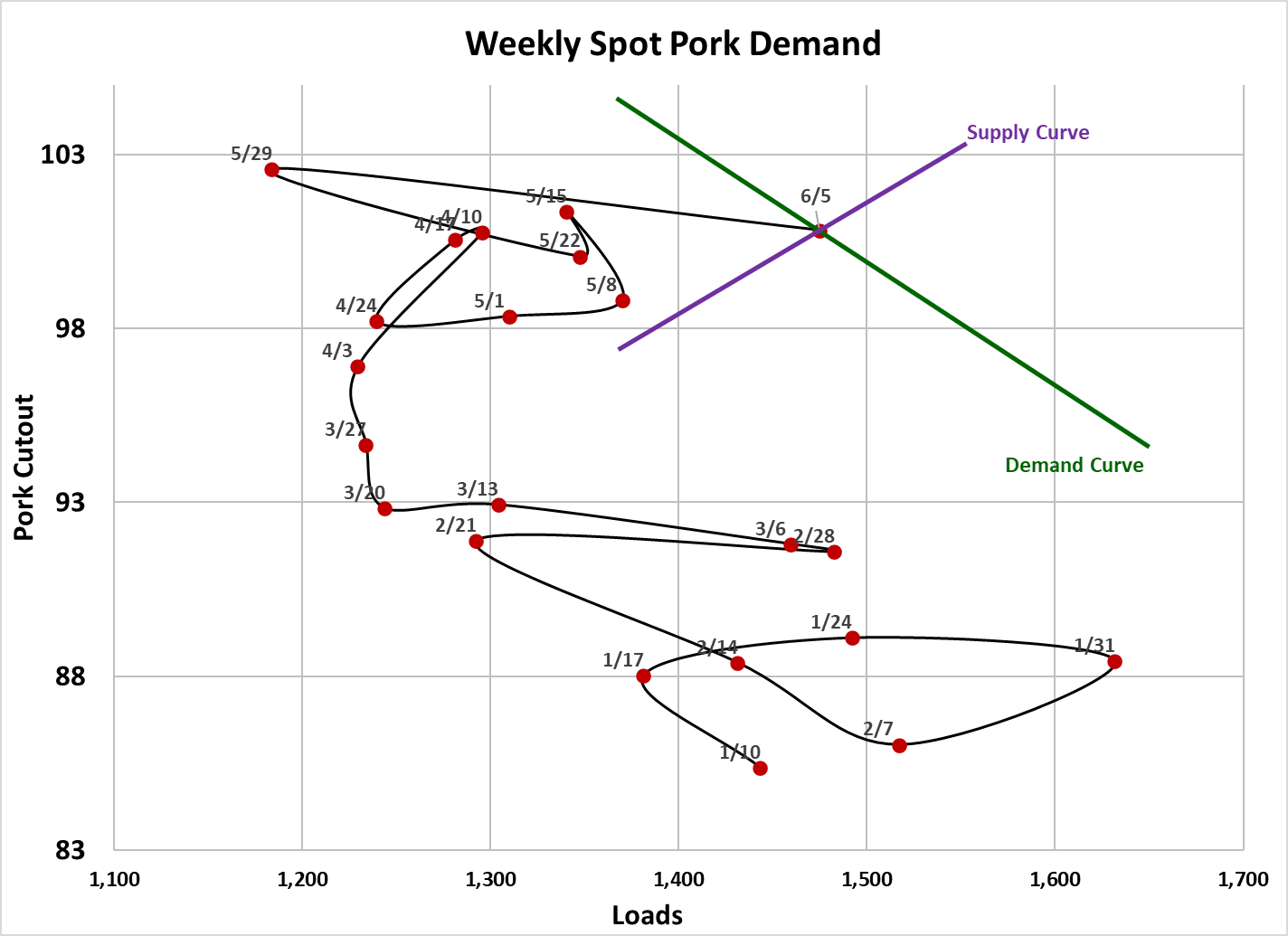

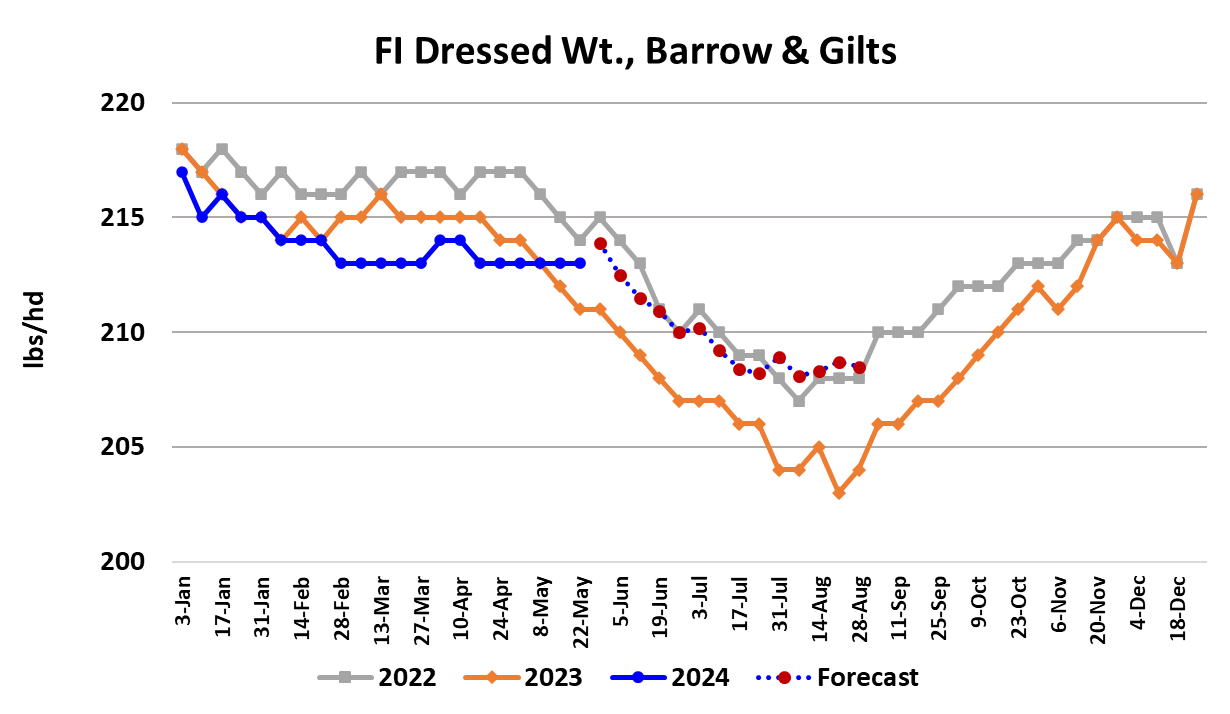

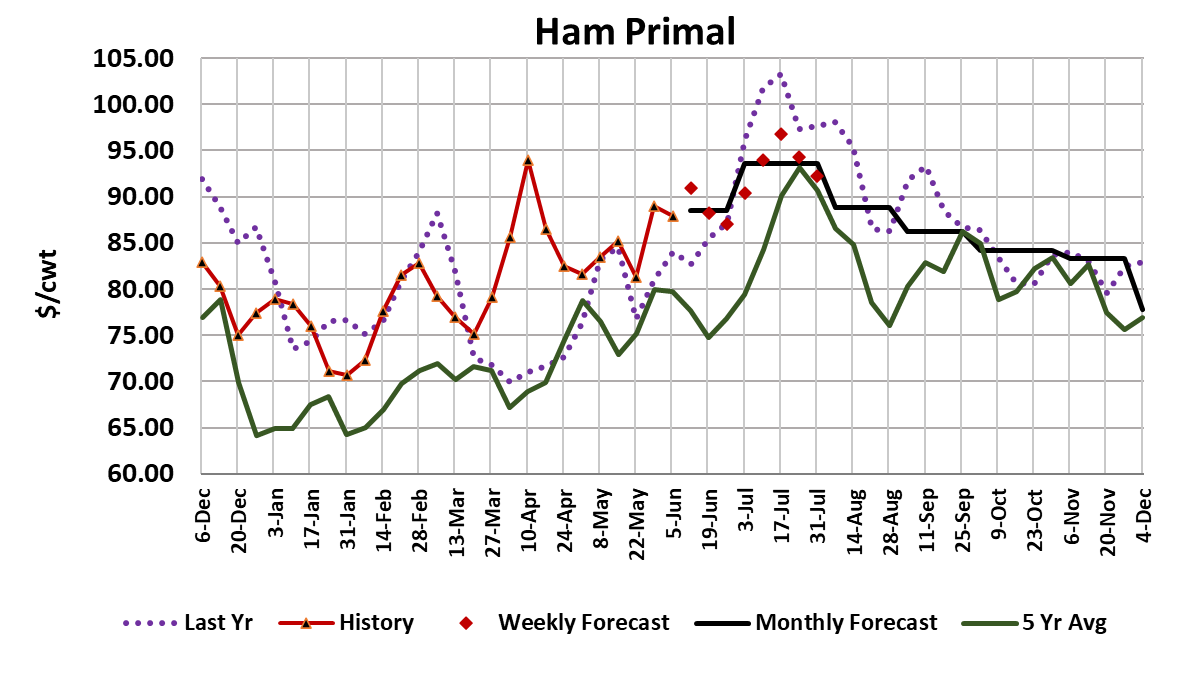

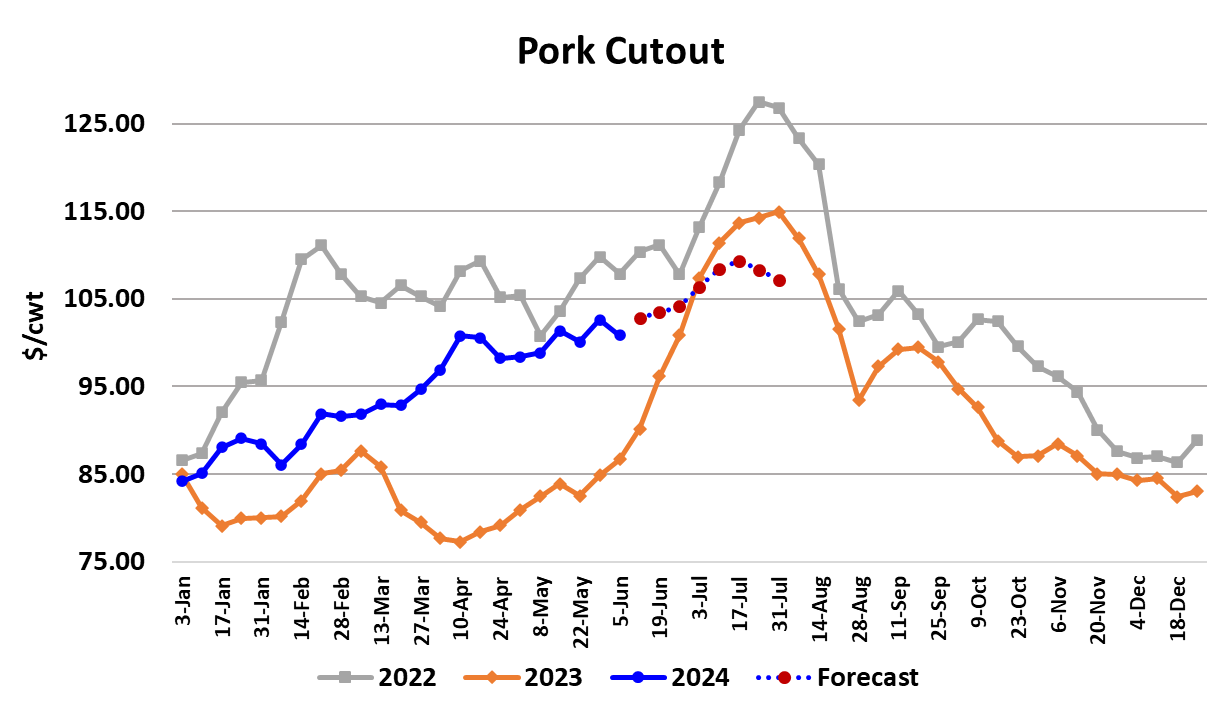

Cash hog markets remained dead in the water this week, with negotiated hogs in the National Direct market averaging $87.43, down $0.36 from last week’s average. The cutout didn’t fare any better, down $1.77 on a weekly average basis to $100.82. As a result, packer margins compressed back down to $10/head from about $16/head the week before. On the surface, this week’s cutout appears to point to a weak demand situation, but that isn’t really the case. The cutout was indeed down, but it was on much bigger volume than was traded in the prior week, which contained Memorial Day. The attached scatter diagram plots the cutout vs the number of negotiated loads traded each week. It is easy to see that the demand curve is further to the right (better demand) than in any week since January. At the end of Feb/early March packers sold nearly the same number of negotiated loads as they did this week, but the cutout was at about $92 instead of the $101 posted this week, so clearly this week’s demand was much better. A reasonable question to ask is “what caused this week’s volume to be so much larger than the volumes seen back in March, April and May?” I think it can mostly be attributed to catch-up following the holiday week when movement was very light. Packers increased the Saturday kill in an effort to make up for shifts lost to Memorial Day and that, along with a return to regular kill schedules this week, left a lot of pork that needed to be moved this week. The fact that they were able to accomplish that with only a $1.77 decline in the cutout is a positive. However, this week’s kill was rather large at 2.42 million head, so packers might still have a lot of pork to move early next week and that could keep the cutout contained. Further, I don’t see much relief on the supply side next week and estimate the total kill will be close to 2.42 million head once again. So it appears that the price stagnation that we’ve seen recently is more a function of large supplies rather than weak demand. The good news is that this week’s kill, which was the first of the Jun/Aug quarter, was slightly below what the Dec/Feb pig crop implied, so maybe USDA was accurate on their estimate and we don’t have to worry about big supply side surprises in the next couple of months. The flip side of that, the bad news if you will, is that the Dec/Feb pig crop was estimated to be up about 2% YOY, which means that non-holiday weekly kills this summer are unlikely to drop below 2.3 million head and might not even get below 2.35 million head. That means not much relief is coming from the supply side this summer, so if prices are going to move higher, it is going to have to come from improving demand. That could happen, because the upcoming July 4 holiday is a big favorite for pork features, with smoke-able items like ribs and butts taking center stage in retail ads, along with hot dogs. Also, it seems likely that bacon demand will strengthen into summer and we should see the belly primal start to climb. That probably won’t come in time to help the Jun lean hog futures, which expire next Friday and seem to be headed for expiration somewhere in the $91-92 range, similar to where both May and April expired. It seems that futures traders have given up on any kind of price rally this summer, pricing the Jun, Jul and Aug contracts all in the low $90s. I’m not quite ready to throw in the towel and thus still look for the cutout to trade the $108 level at some point this summer. Warm weather demand was very late in coming to the beef market, but once it did, the beef cutouts put in a substantial rally. Perhaps pork is just a little late out of the gate too and the price rally may come in July/Aug this year rather than the more-typical May/June time frame. Another thing affecting the supply side of the market is the lack of hot temperatures in the Midwest so far this year. Normally, by mid-June a couple of heat waves have passed through the Midwest and tempered hog performance. Perhaps that is yet to come also. FI barrow and gilt weights were reported steady again this week, well past the point where they should be declining seasonally. Moreover, weights are likely to rise a pound or so next week because that data will correspond to the holiday week. Still, the DTDS weights remain at relatively low levels and don’t suggest that hogs are backing up in the pipeline. Usually, the sharpest increases in negotiated hog prices come in response to a heat wave that causes producers to hold hogs a few more days on feed, thus temporarily shorting the spot hog markets. So far that hasn’t happened but it doesn’t mean that it won’t. There is still a lot of summer yet to come and the experts say it could be the hottest summer on record. USDA provided the official export totals for April today and it showed a 13% YOY increase. Through the first four months of the year, exports are up 9-10% YOY and the cutout was up 13% over that same period. Clearly, international demand for US pork is stronger than it was last year and I don’t see any reason why that wouldn’t continue through the balance of 2024. I can’t believe I got this deep into the weekly report without mentioning hams. The primal was down slightly this week on strong volume and looking for prices to be a little higher next week. On concerning feature in the ham space is that the Mexican peso has weakened recently against the US dollar and that might slow ham sales to that important destination. There isn’t much evidence of that yet, but it bears watching. The retail items looked soft this week, but I chalk that up more to big volumes rather any significant erosion in demand. The forecast has loins regaining some upward momentum in the next couple of weeks while the butts trade mostly sideways near current levels. As usual, the bellies are the holy grail for summer cutout rallies. If they could get some traction and move moderately higher then the summer cutout target should be easily achievable. This summer seems to be shaping up as one where patience will be key for the bulls because any summer rally might get a late start. If it happens, it probably won’t be an explosive rally, simply because hog supplies look ample. Next week, look for some modest improvement in the cutout, but probably very little gain in negotiated hog prices.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}