Pork Wrap June 30

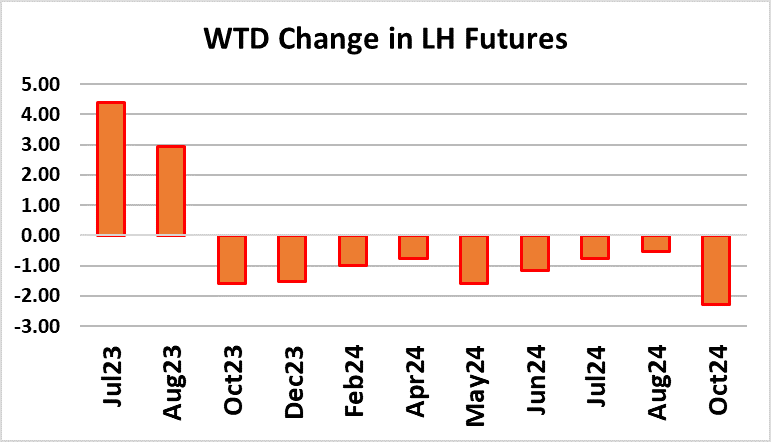

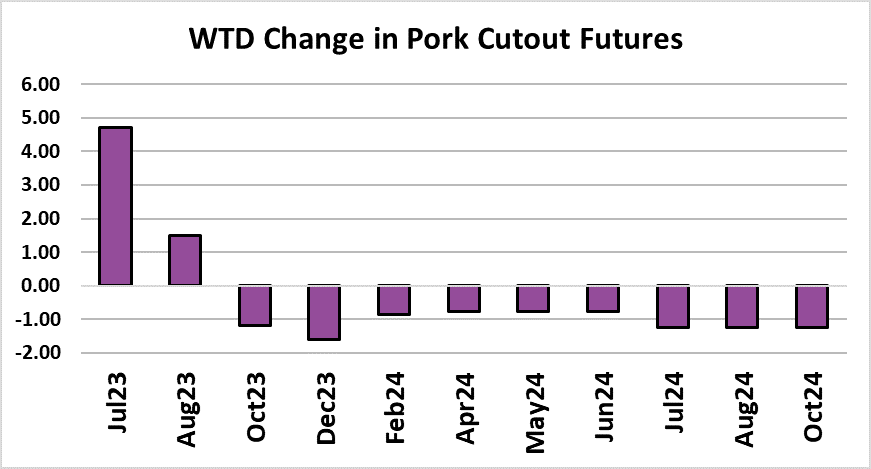

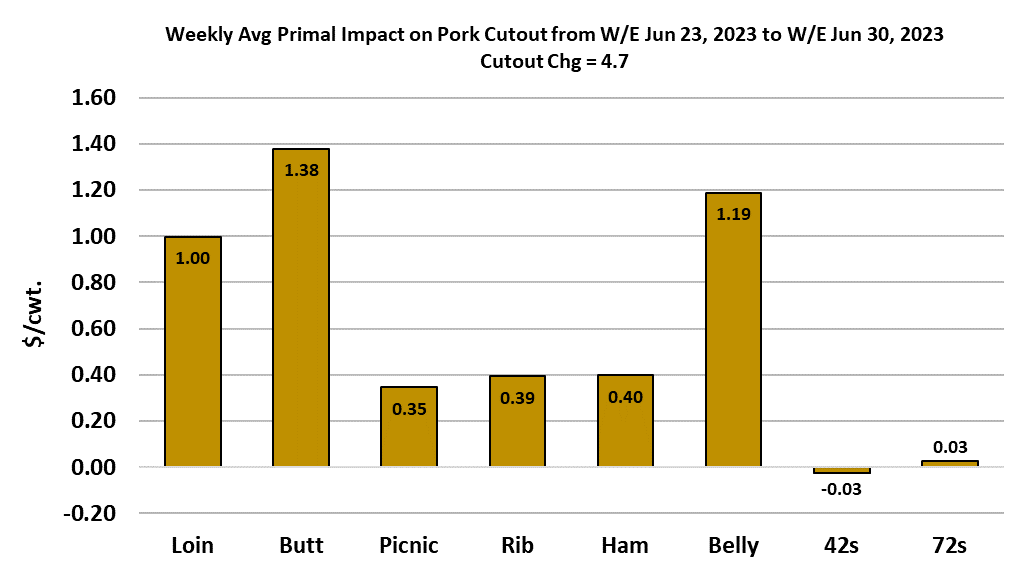

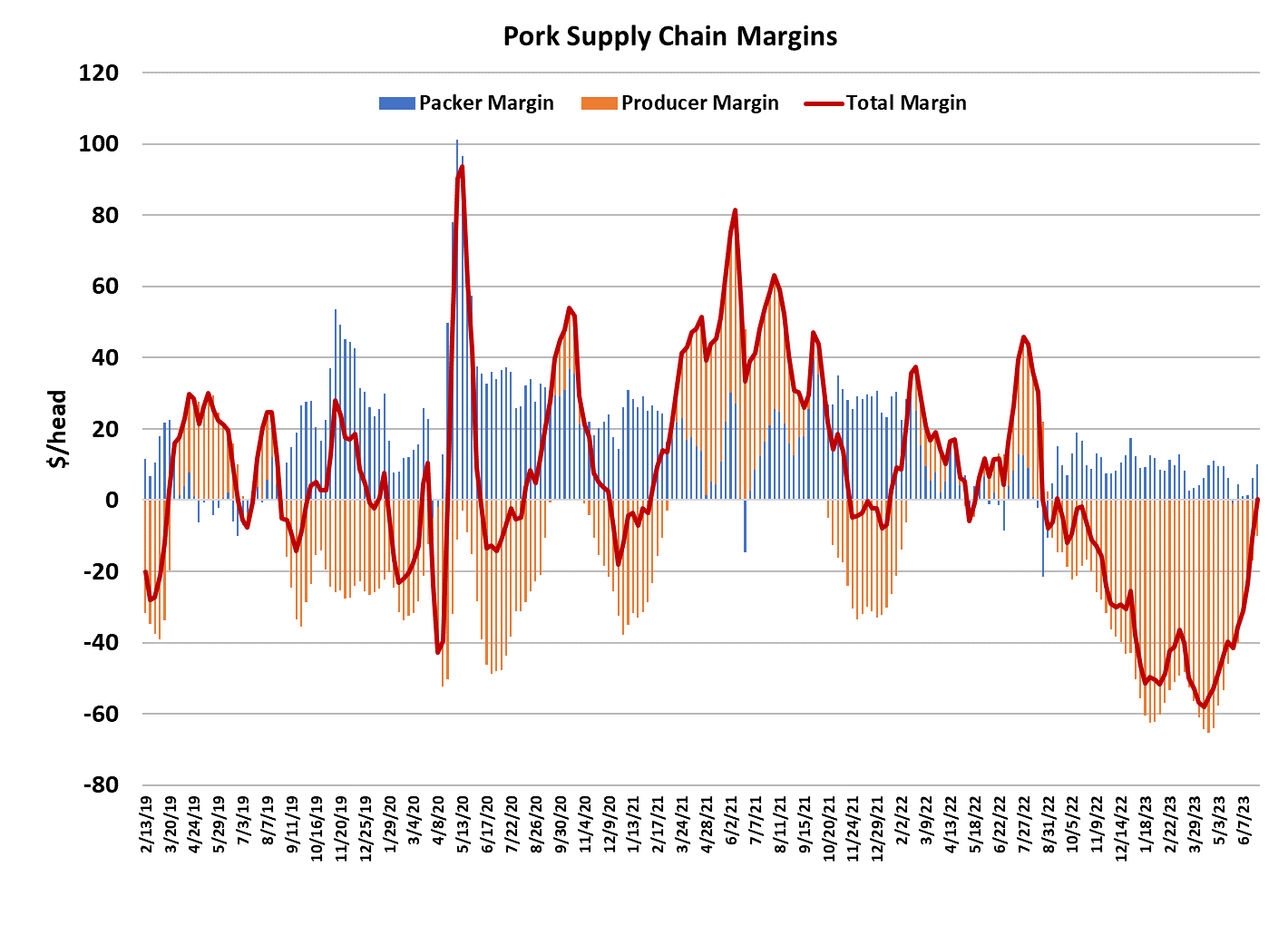

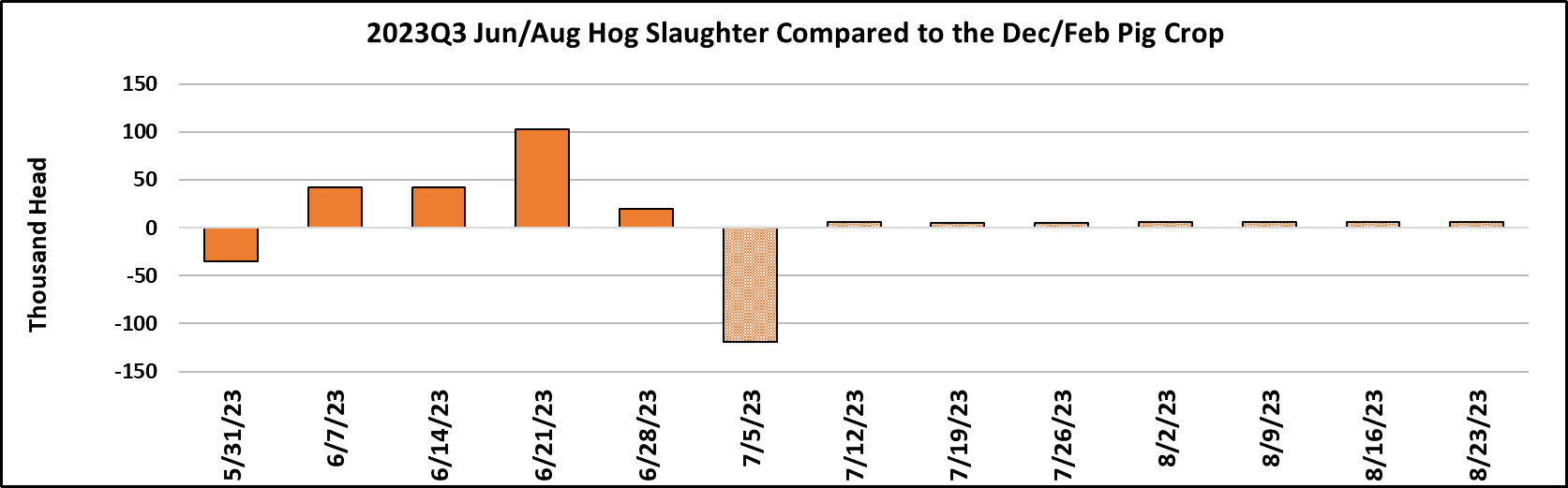

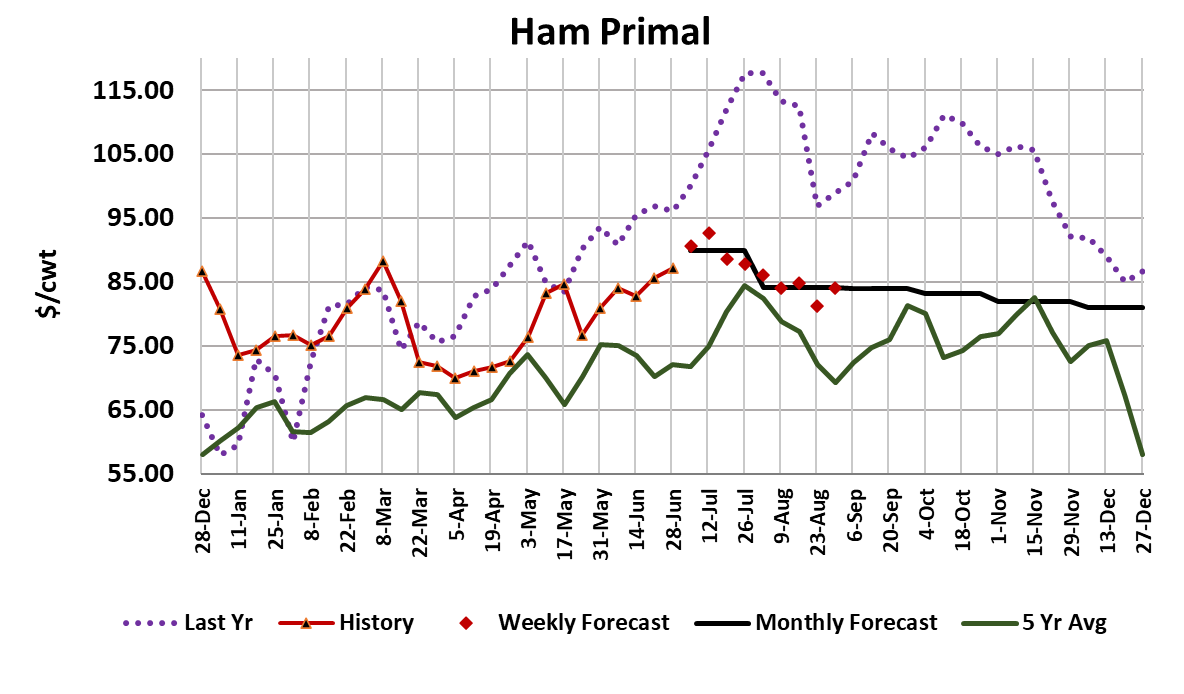

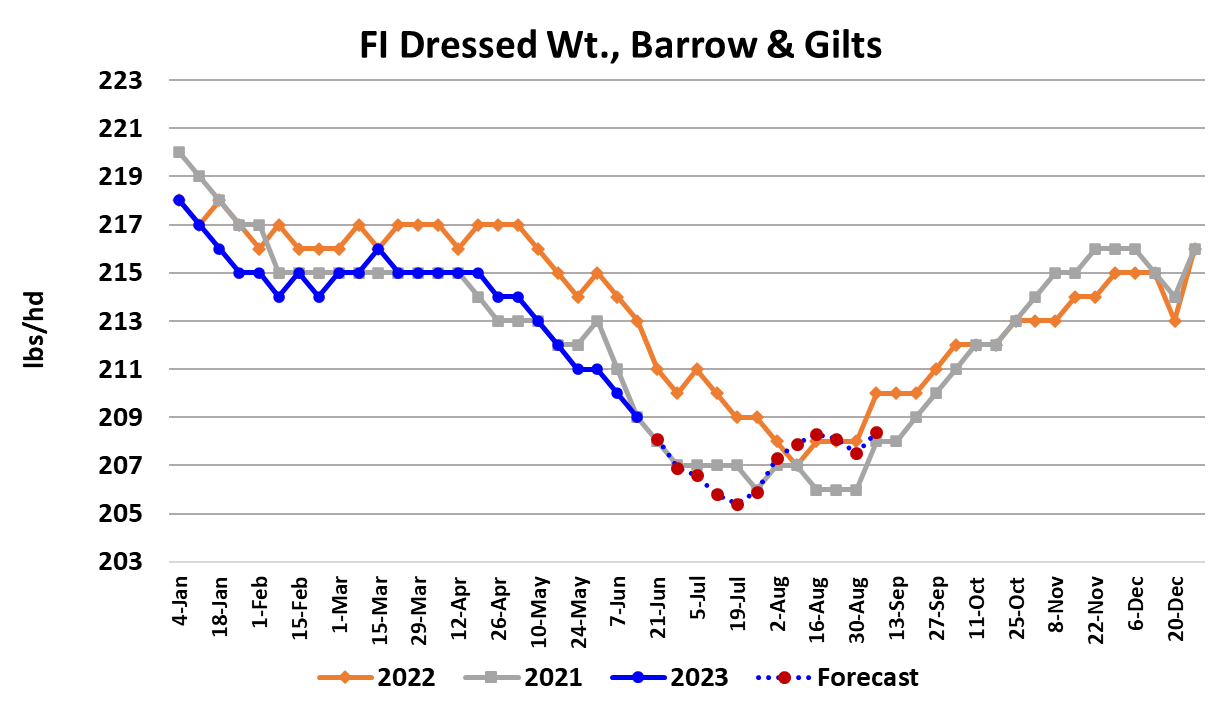

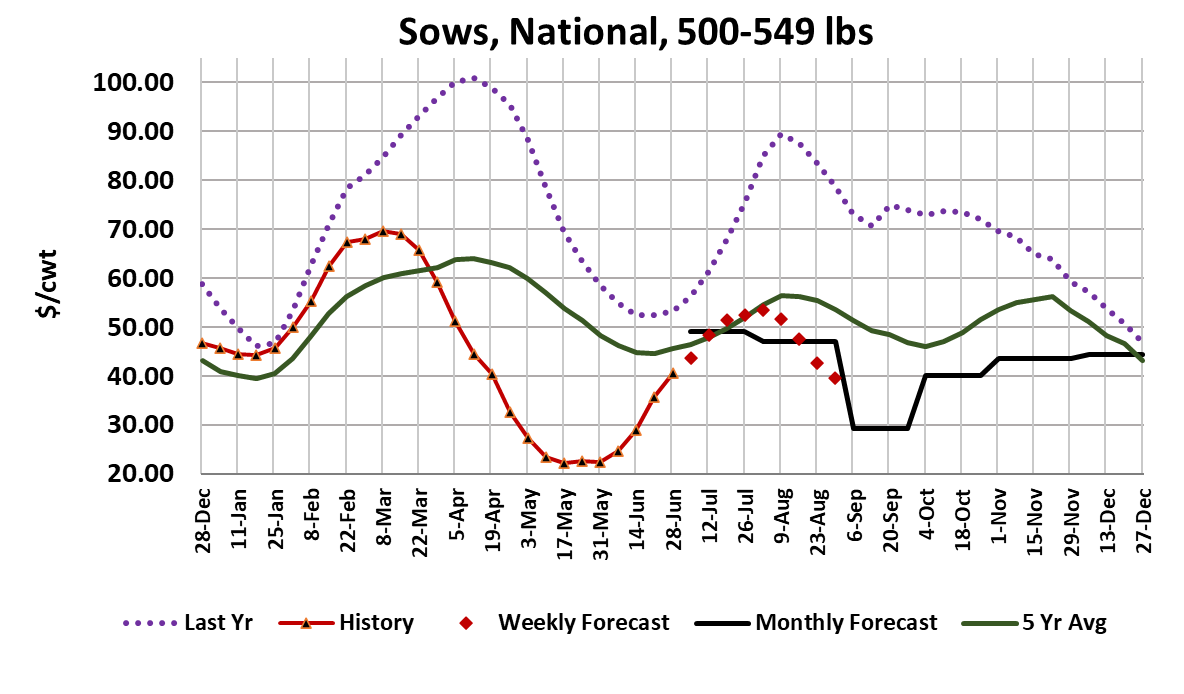

The pork cutout breached the $100 mark this week, the first time that has happened since last October. All of the primals contributed in that effort, but it was the bellies, loins and butts that did the heavy lifting. The cutout averaged $100.83 on the week, up $4.70/cwt from last week’s average. The negotiated hog market went in the other direction, with prices in the WCB region averaging $1.61/cwt lower than the week before. Volumes in the negotiated market were lighter than normal, perhaps suggesting that packer demand was being constrained by the upcoming July 4 holiday. The same thing happened in the week prior to Memorial Day, volumes fell off and prices declined slightly, but they started rising again the very next week. I suspect that will be the case this time also. Nonetheless, rising cutouts combined with lower cash hog pricing is the recipe for better packer margins. This week’s margin registered a little over $10/head—very strong for this time of year when hog supplies are near seasonal lows. Producer margins were only $10/head in the red this week, so the combined margin sat very close to zero. It has been almost a year since there was this much margin in the pork supply chain. I think that there is a reasonable chance that producers get to breakeven next week and after that we could see modest single-digit positive margins. That is a huge turnaround from this spring when producer margins were running $65/head in the red. Perhaps that will give producers hope and perhaps curtail their plans to reduce their herds. USDA released the results of their quarterly Hogs & Pigs survey this week and it showed a very modest 0.4% YOY reduction in the breeding herd. Further, the total swine inventory was just a tad above last year at this time. The March/May pig crop was 0.8% bigger than last year, largely due to a huge jump in the number of pigs saved per litter. The March/May pig crop will come to slaughter in the Sep/Nov quarter, so it is looking like hog supplies will be larger than last year this fall. I am particularly concerned about the unusually low number of sows farrowing reported in the Mar/May quarter. It looks like USDA probably underestimated that vital metric and if I’m right about that then we could see kills in the Sep/Nov quarter exceed what the pig crop estimate implies. Those over-kills have plagued the industry for the past three quarters. This week’s slaughter came in at 2.33 million head, down 40k from the week before, and once again larger than what the Dec/Feb pig crop implied. It seems that producers have done a good job of keeping their marketings current because carcass weights are dropping fast and the DTDS weights are at all-time lows. That leads me to believe that the price gains in the negotiated market are not done yet. Next week’s kill might only be 1.95 million head due to the holiday, so pork buyers may find available supplies to be a little snug next week and the cutout is likely to advance again. Through the balance of July, we should see weekly slaughter hover close to 2.3 million head before it begins to expand seasonally in early August. So, the supply side should be moderately supportive to prices. The important unknown at this point is how much gas the demand side has left in the tank. Will demand continue to march steadily higher over the next few weeks, or will it falter and take the cutout lower? Just eyeballing the combined margin chart, I would say that if demand is going to go back to “normal”, i.e., where it was before the huge downdraft began late last summer, then the combined margin should continue upward into positive territory and that would imply that demand continues improving for a few more weeks. It seems to me that the bellies are seeing improving demand and they probably have more room to run to the upside and, as long as the hams can hold steady or perhaps even advance some, the cutout should continue upward. The retail primals, primarily loins and butts are a little more questionable at this point. Those primals are expected to take the biggest hit if Prop 12 causes a slowdown in product movement. It’s unclear whether or not that will be a problem just yet, but the potential is there. The hams did show some price improvement this week and the forecast has them continuing higher for at least a couple more weeks. Last year, ham prices posted a strong surge during the month of July. Prop 12 is now in effect and I’m sure everyone in the industry is eager to see how it will play out. My guess is that it won’t be much of a factor initially, but could become more of a market influence near the end of the year as enforcement efforts become more concentrated. Futures traders have been pricing the Aug contract about $3 under the July, suggesting that they think the market will top sometime between the July and Aug expirations. My forecasts follow the same pattern. Sow prices are in an uptrend, now at close to $42/cwt after bottoming around $21/cwt near the middle of May. Trim pricing has also been very strong of late, but may be nearing a seasonal top. It seems like the bellies hold the most hope for price appreciation over the next few weeks and the forecast has the primal moving from about $110 this week to a top in the $130-140 range by mid-August. It could surprise me and exceed that. For now, the bullish story of seasonally small hog supplies and improving pork demand remains in place. Next week, look for the short kill to support the cutout and that will likely cause the negotiated hog market to catch up after posting soft results this week.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}